| Study Period | 2021 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| CAGR | 13.80 % |

| Fastest Growing Market | North America |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Nuclear Power Reactor Decommissioning Market Analysis

The Nuclear Power Reactor Decommissioning Market is expected to register a CAGR of 13.8% during the forecast period.

The nuclear power decommissioning industry is experiencing significant transformation driven by evolving energy policies and environmental considerations worldwide. Several countries, including Germany, the United Kingdom, and South Korea, have implemented nuclear phase-out policies, fundamentally reshaping the industry landscape. This shift is particularly evident in the global nuclear power generation output, which reached 2,653.3 TWh in 2021, reflecting the complex balance between maintaining existing nuclear infrastructure and transitioning to alternative energy sources. The industry is witnessing a growing emphasis on environmental sustainability, with many nations accelerating their transition towards renewable energy sources while simultaneously managing their nuclear legacy.

The industry is witnessing a notable trend toward accelerated nuclear decommissioning processes, particularly in North America and Europe, where operators are increasingly adopting more efficient and cost-effective approaches to nuclear facility closure. This transformation is highlighted by the significant scale of decommissioning nuclear power plants requirements, with approximately 198 reactors permanently shut down globally as of December 2021. The accelerated decommissioning approach allows nuclear facility sites to be released for unrestricted use sooner after shutdown, representing a fundamental shift from traditional decommissioning timelines that could span several decades.

France's nuclear sector exemplifies the complex dynamics within the industry, generating 379 TWh from nuclear sources in 2021, accounting for 69% of its total electricity generation. However, the country is now implementing a strategic transition plan to reduce nuclear's share in its energy mix to 50% by 2035, demonstrating the delicate balance between maintaining energy security and pursuing environmental objectives. This transition is creating new opportunities for nuclear power plant decommissioning service providers while highlighting the technical and logistical challenges associated with large-scale nuclear facility closures.

The Japanese market presents a particularly compelling case study of the industry's evolution, with 27 nuclear reactors totaling 17.12 GWe of capacity having been shut down. The country's experience has led to significant technological advancements in nuclear decommissioning processes, including innovative approaches to handling contaminated materials and managing long-term waste storage. These developments are influencing global best practices and driving improvements in decommissioning methodologies, while also highlighting the importance of international collaboration in addressing complex technical challenges.

Nuclear Power Reactor Decommissioning Market Trends

Aging Nuclear Reactor Fleet & End of Operational Life

The global nuclear power industry is facing a critical juncture as a significant portion of its reactor fleet approaches or exceeds designed operational lifespans. As of October 2022, there were 437 commercial nuclear power plants operating across 32 countries, with many of these facilities approaching their initial 40-year operational life limit. The aging infrastructure presents substantial technical and safety challenges, compelling operators to make crucial decisions between costly life extensions and decommissioning. For instance, in the United States, numerous plant owners are opting for early retirement of their nuclear units at 45 to 50 years old, despite the possibility of extending operations to 80 years through the Nuclear Regulatory Commission's subsequent license renewal program.

The technical complexity of maintaining aging reactors has become increasingly challenging and expensive, particularly for first-generation nuclear facilities. These older plants often require significant upgrades to meet current safety standards and operational requirements, making continued operation economically unfeasible. The situation is particularly evident in countries like France, where 14 nuclear reactors are scheduled for shutdown by 2035, and the United Kingdom, where 34 reactors have already been permanently shut down. The trend of reactor closures is expected to accelerate as more facilities reach their design life limits, with approximately 198 reactors projected to shut down by 2030, creating a substantial demand for nuclear plant decommissioning services.

Understand The Key Trends Shaping This Market

Download PDF

Policy Initiatives and Regulatory Changes

Government policies and regulatory changes have emerged as significant drivers for nuclear power reactor decommissioning, particularly in Western European nations. Several countries have implemented comprehensive nuclear phase-out strategies as part of their energy transition policies. Germany, following its national policy, has committed to shutting down all its reactors, while Switzerland's democratic vote to phase out nuclear power plants demonstrates the public influence on nuclear energy policies. Similarly, Belgium has reaffirmed its commitment to phase out nuclear power by 2025, and Spain has announced plans to close all seven of its operating commercial reactors by 2035.

The policy-driven decommissioning trend is further reinforced by stringent regulatory requirements and safety protocols implemented in the post-Fukushima era. These enhanced safety measures have necessitated substantial infrastructure upgrades and increased operational maintenance costs, making it economically challenging for older facilities to continue operations. The regulatory landscape has become particularly demanding in countries with strong renewable energy portfolios, where concerns about environmental impact and operational risks have led to accelerated decommissioning schedules. For instance, France's energy plan confirms the target of reducing nuclear energy's share in electricity generation to 50% by 2035, demonstrating how policy initiatives are reshaping the nuclear power landscape and contributing to growth in the nuclear decommissioning market.

Growth of Alternative Energy Sources

The rapid advancement and increasing economic viability of renewable energy technologies have significantly impacted the nuclear power sector, driving many facilities toward decommissioning. Countries worldwide are developing extensive renewable energy infrastructure, which has effectively reduced the reliance on nuclear power for base-load electricity generation. The declining costs of solar and wind power generation have made these alternatives increasingly attractive compared to maintaining aging nuclear facilities, particularly when considering the high costs of nuclear plant upgrades and life extensions. This shift is evident in the strategic energy policies of numerous nations that are actively replacing nuclear capacity with renewable sources.

The economic competitiveness of alternative energy sources has been further enhanced by technological improvements and economies of scale in renewable energy production. The development of more efficient energy storage solutions and smart grid technologies has addressed many of the traditional challenges associated with renewable energy intermittency, making these sources increasingly viable alternatives to nuclear power. This transition is particularly noticeable in countries with strong environmental policies, where the combination of renewable energy targets and nuclear phase-out plans has accelerated the decommissioning of nuclear facilities. The trend is reinforced by public preference for renewable energy sources and growing concerns about nuclear waste management and environmental impact, leading to increased pressure for nuclear plant closures and subsequent nuclear decommissioning activities.

Segment Analysis: Reactor Type

Boiling Water Reactor (BWR) Segment in Nuclear Power Reactor Decommissioning Market

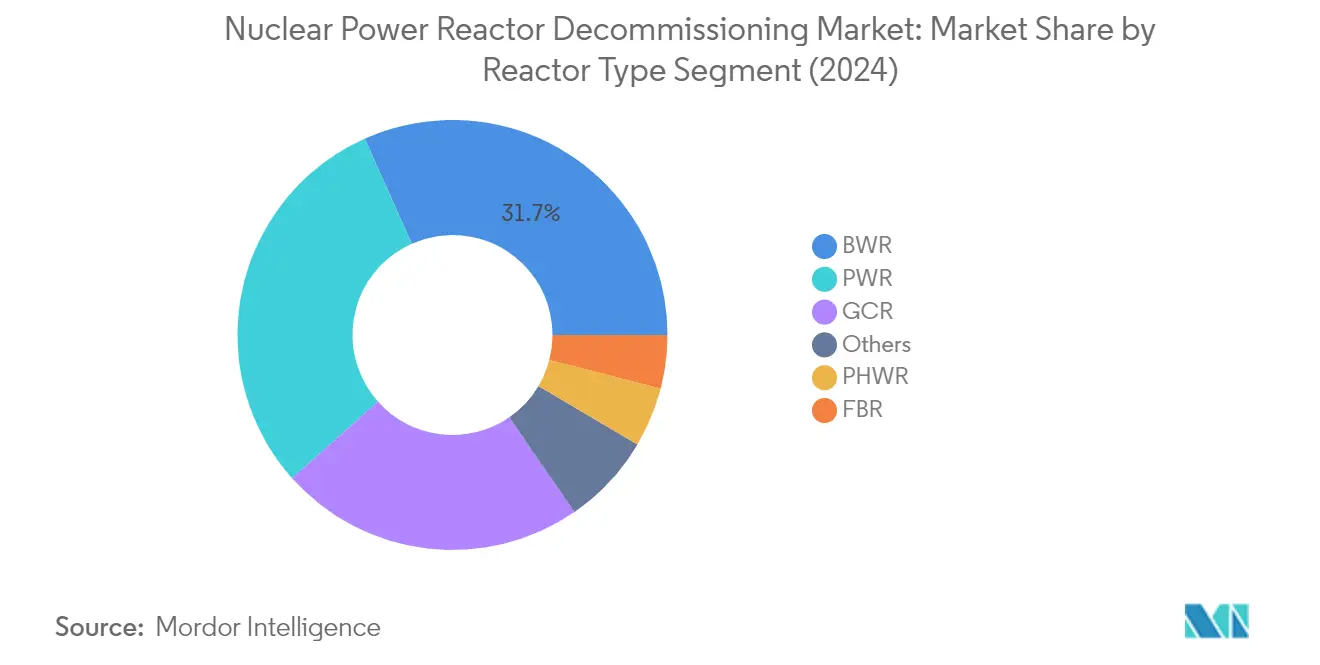

The Boiling Water Reactor (BWR) segment dominates the nuclear reactor decommissioning market, holding approximately 32% market share in 2024. BWR's prominence is particularly evident in countries like the United States, Japan, and Germany, which collectively account for about 80% of worldwide BWR shutdowns. The segment's large market share is attributed to several factors, including the aging BWR fleet globally and the complex decommissioning requirements due to radiation contamination of steam turbines from direct contact with the core reactor. The technical challenges associated with BWR decommissioning, including the need for sophisticated circulation management and nuclear fuel consumption monitoring during the decommissioning process, have contributed to its substantial market value.

Pressurized Water Reactor (PWR) Segment in Nuclear Power Reactor Decommissioning Market

The Pressurized Water Reactor (PWR) segment is emerging as the fastest-growing segment in the nuclear reactor decommissioning market for the period 2024-2029. This growth is driven by several factors, including the increasing number of PWR reactors reaching their operational end-of-life globally. The segment's growth is further supported by the technical advantages of PWR decommissioning, such as the lower risk of radiation contamination compared to other reactor types, due to its separate primary and secondary cooling circuits. Additionally, the established decommissioning protocols and expertise in PWR dismantling, particularly in countries like France and the United States, are facilitating more efficient and cost-effective decommissioning processes.

Remaining Segments in Reactor Type Segmentation

The other significant segments in the nuclear power reactor decommissioning market include Gas-Cooled Reactors (GCR), Pressurized Heavy Water Reactors (PHWR), Fast Breeder Reactors (FBR), and other specialized reactor types. The GCR segment is particularly significant in European markets, especially in the United Kingdom, where numerous Magnox reactors are undergoing decommissioning. PHWRs, predominantly found in Canada and India, present unique decommissioning challenges due to their heavy water moderator systems. The FBR segment, though smaller, requires specialized decommissioning expertise due to the complex handling of plutonium fuel and liquid metal coolants. The remaining specialized reactor types, including high-temperature gas-cooled reactors and light water graphite reactors, contribute to market diversity with their specific decommissioning requirements.

Segment Analysis: Application

Commercial Power Reactor Segment in Nuclear Power Reactor Decommissioning Market

The Commercial Power Reactor segment dominates the global nuclear power decommissioning market, accounting for approximately 91% of the total market share in 2024. This significant market share is driven by the large number of aging commercial nuclear reactors worldwide that are approaching or exceeding their operational lifespans. The segment's dominance is particularly evident in regions like Europe and North America, where numerous commercial reactors are being phased out due to economic, regulatory, and safety considerations. For instance, Germany's commitment to phase out all commercial nuclear power plants, along with similar initiatives in countries like France and Spain, continues to drive the segment's growth. Additionally, the increasing focus on renewable energy alternatives and the high costs associated with maintaining older commercial reactors have led many operators to opt for decommissioning rather than life extension programs.

Prototype Power Reactor Segment in Nuclear Power Reactor Decommissioning Market

The Prototype Power Reactor segment represents a specialized niche in the nuclear decommissioning market, characterized by unique technical challenges and specialized decommissioning requirements. These reactors, which served as intermediate facilities between research reactors and commercial units, require specific expertise and methodologies for safe decommissioning. The segment's growth is supported by ongoing projects like the decommissioning of prototype boiling water reactors in various locations and the increasing focus on clearing legacy nuclear sites. The segment benefits from technological advancements in decommissioning techniques and the growing expertise of specialized contractors in handling these unique facilities. The decommissioning of prototype reactors often serves as valuable learning experiences for the industry, providing insights and methodologies that can be applied to future commercial reactor decommissioning projects.

Research Reactor Segment in Nuclear Power Reactor Decommissioning Market

The Research Reactor segment, while smaller in market share, plays a crucial role in the nuclear decommissioning landscape. These facilities, typically located near population centers and often on university campuses, present unique challenges in terms of decommissioning requirements and safety considerations. The segment is characterized by smaller-scale operations compared to commercial reactors, but often requires more precise and careful handling due to their proximity to populated areas. The decommissioning of research reactors involves specific considerations regarding the handling of experimental materials and specialized research equipment, making it a technically distinct segment within the market. The segment's activities are particularly important in countries with established nuclear research programs, where aging research facilities require proper decommissioning to ensure public safety and environmental protection.

Segment Analysis: Capacity

100-1000 MW Segment in Nuclear Power Reactor Decommissioning Market

The 100-1000 MW capacity segment dominates the nuclear plant decommissioning market, accounting for approximately 65% of the total market value in 2024. This segment's prominence is driven by the large number of aging nuclear reactors within this capacity range reaching their end-of-life phase across major nuclear power generating countries. The segment is also experiencing the highest growth trajectory, with projections indicating an expansion of nearly 50% between 2024 and 2029. This robust growth is attributed to several factors including stringent safety regulations, increasing focus on renewable energy alternatives, and government policies favoring nuclear decommissioning in regions like Europe and North America. The segment's market leadership is further strengthened by the extensive decommissioning projects currently underway in countries such as Germany, France, and Japan, where numerous reactors within this capacity range are being systematically shut down and decommissioned.

Above 1000 MW Segment in Nuclear Power Reactor Decommissioning Market

The above 1000 MW capacity segment represents a significant portion of the nuclear power reactor decommissioning market, with substantial growth potential driven by the increasing number of large-scale nuclear power plants approaching their decommissioning phase. This segment is projected to grow at a considerable rate between 2024 and 2029, supported by major decommissioning projects in developed economies. The growth is particularly notable in countries with extensive nuclear power programs, where larger capacity reactors built during the peak of nuclear power development are reaching their operational end-of-life. The segment's expansion is further fueled by technological advancements in decommissioning processes, increasing safety requirements, and growing public pressure for the closure of aging nuclear facilities. The complexity and scale of decommissioning these large reactors require significant technical expertise and financial resources, making this segment particularly attractive for specialized decommissioning service providers.

Remaining Segments in Capacity Segmentation

The below 100 MW segment, while smaller in market share, plays a crucial role in the nuclear power reactor decommissioning market, particularly in the context of research reactors and smaller experimental facilities. This segment primarily encompasses research reactors, prototype reactors, and early demonstration units that were built for scientific and developmental purposes. The decommissioning of these smaller facilities often serves as valuable testing grounds for new decommissioning technologies and methodologies, which can later be scaled up for larger reactors. These projects, though smaller in scale, are significant for developing expertise in handling specialized decommissioning challenges and maintaining nuclear safety standards. The segment also includes various test reactors in university settings and research institutions, which require unique approaches to decommissioning due to their location in populated areas and specific design characteristics.

Nuclear Power Reactor Decommissioning Market Geography Segment Analysis

Nuclear Power Reactor Decommissioning Market in North America

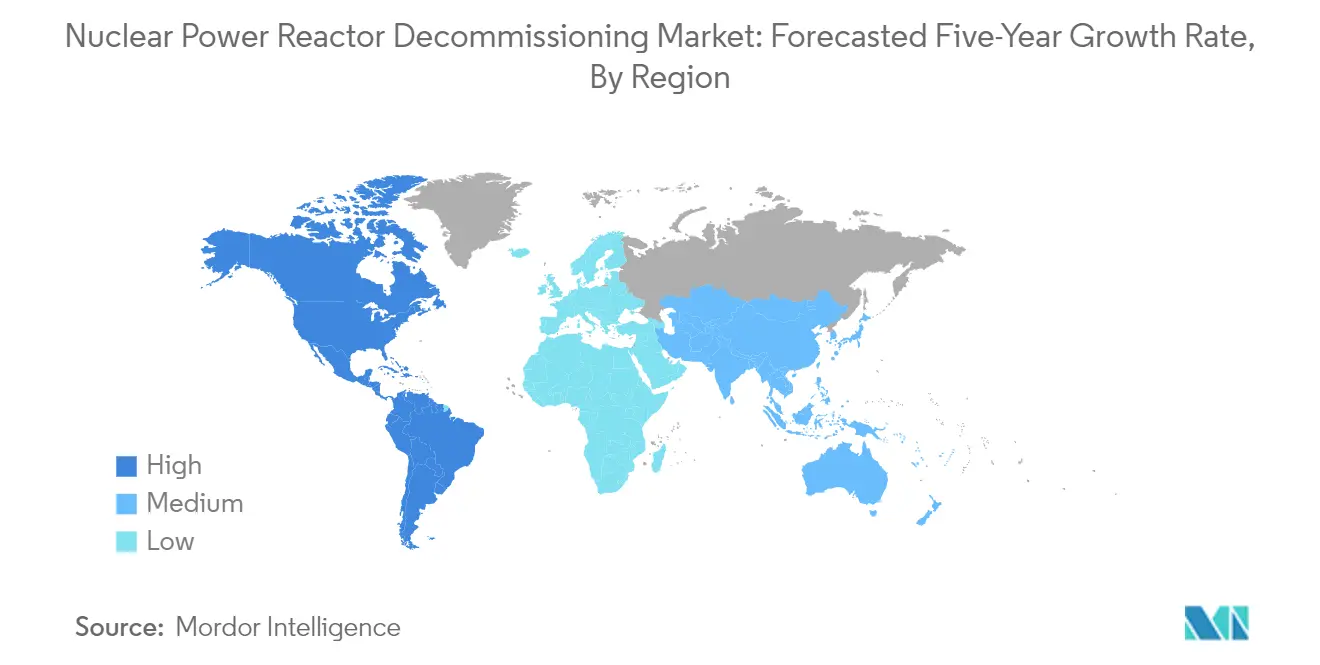

North America represents a dominant force in the global nuclear decommissioning market, commanding approximately 32% of the global market share in 2024. The region's prominence is primarily driven by the United States, which maintains one of the world's largest nuclear reactor fleets. The market dynamics are shaped by aging nuclear infrastructure, stringent regulatory requirements, and increasing adoption of accelerated nuclear power plant decommissioning processes. Private nuclear decommissioning companies are actively acquiring nuclear plants, taking over their licenses, liability, decommissioning funds, and waste contracts. The region's approach to decommissioning is characterized by advanced technological capabilities, well-established regulatory frameworks, and extensive experience in handling complex decommissioning projects. The presence of major industry players and specialized service providers further strengthens North America's position in the global market. The region's commitment to nuclear safety and environmental protection continues to drive investments in decommissioning activities, while also fostering innovations in decommissioning technologies and methodologies.

Nuclear Power Reactor Decommissioning Market in Asia-Pacific

The Asia-Pacific region has demonstrated steady growth in the nuclear decommissioning services market, with a compound annual growth rate of approximately 2% from 2019 to 2024. The market is primarily driven by Japan, China, and South Korea, which are actively pursuing decommissioning projects while simultaneously developing new nuclear facilities. The region's unique approach combines traditional decommissioning methods with innovative technologies, reflecting a balance between safety, efficiency, and cost-effectiveness. China's emergence as a major player in nuclear decommissioning showcases the region's growing capabilities and technological advancement. Japan's extensive decommissioning programs, particularly following regulatory changes, have significantly influenced market dynamics. The region's commitment to developing indigenous decommissioning capabilities, coupled with an increasing focus on environmental safety and regulatory compliance, continues to shape market evolution. International collaborations and knowledge transfer initiatives are playing crucial roles in enhancing the region's decommissioning capabilities.

Nuclear Power Reactor Decommissioning Market in Europe

Europe's nuclear decommissioning market is poised for substantial growth, with projections indicating a robust compound annual growth rate of approximately 19% from 2024 to 2029. The region's market is characterized by a strong regulatory framework, advanced technological capabilities, and significant experience in decommissioning projects. Germany's nuclear phase-out policy, France's strategic reduction in nuclear dependency, and various other national initiatives are driving market growth. The region's approach to decommissioning emphasizes immediate dismantling over deferred strategies, reflecting a shift in industry practices. European countries are actively developing specialized expertise and innovative technologies for decommissioning activities. The presence of established industry players, coupled with substantial government support and funding mechanisms, strengthens the market foundation. Cross-border collaboration and knowledge sharing among European nations continue to enhance decommissioning capabilities and efficiency.

Nuclear Power Reactor Decommissioning Market in South America

The South American nuclear power reactor decommissioning market remains in its nascent stages, with limited activity compared to other global regions. The continent's nuclear energy landscape is primarily concentrated in Argentina and Brazil, both of which maintain operational nuclear facilities without immediate decommissioning requirements. The region's approach to nuclear decommissioning is characterized by careful planning and preparation for future needs, despite current limited demand. Infrastructure development and capacity-building initiatives are underway to prepare for eventual decommissioning requirements. The region's regulatory frameworks continue to evolve, incorporating international best practices and safety standards. South American nations are focusing on developing indigenous capabilities and expertise in nuclear decommissioning while maintaining collaborative relationships with international partners. The market's future development will likely be influenced by aging nuclear infrastructure and evolving energy policies.

Nuclear Power Reactor Decommissioning Market in Middle East & Africa

The Middle East & Africa region represents an emerging market in the nuclear power reactor decommissioning sector, with distinct characteristics and development patterns. The region's nuclear infrastructure is relatively young, with several countries only recently entering the nuclear power generation sector. South Africa stands as the primary market driver, being the only country in Africa with significant nuclear power infrastructure and potential decommissioning requirements. The region's approach to decommissioning is marked by careful planning and international collaboration, focusing on building necessary expertise and infrastructure. Regulatory frameworks are being developed and strengthened to address future decommissioning needs. The United Arab Emirates and other Middle Eastern countries are establishing comprehensive nuclear programs, including provisions for eventual decommissioning requirements. The region's market development is characterized by a strong emphasis on capacity building and knowledge transfer from experienced international partners.

Get Analysis on Important Geographic Markets

Download PDF

Nuclear Power Reactor Decommissioning Industry Overview

Top Companies in Nuclear Power Reactor Decommissioning Market

The nuclear decommissioning companies market features prominent players like AECOM, GE-Hitachi Nuclear Energy, Babcock International Group PLC, Fluor Corporation, and Bechtel Group Inc. These companies are increasingly focusing on technological innovation, particularly in robotics and artificial intelligence integration for safer and more efficient decommissioning processes. Strategic collaborations and joint ventures have become crucial for expanding service portfolios and geographical reach, as evidenced by numerous partnership agreements between major players. Companies are investing heavily in developing specialized expertise and proprietary technologies for complex decommissioning projects, while simultaneously building strong relationships with government agencies and regulatory bodies. The industry has witnessed a significant emphasis on operational efficiency improvements through digital transformation and advanced project management methodologies, enabling companies to handle multiple large-scale decommissioning projects simultaneously.

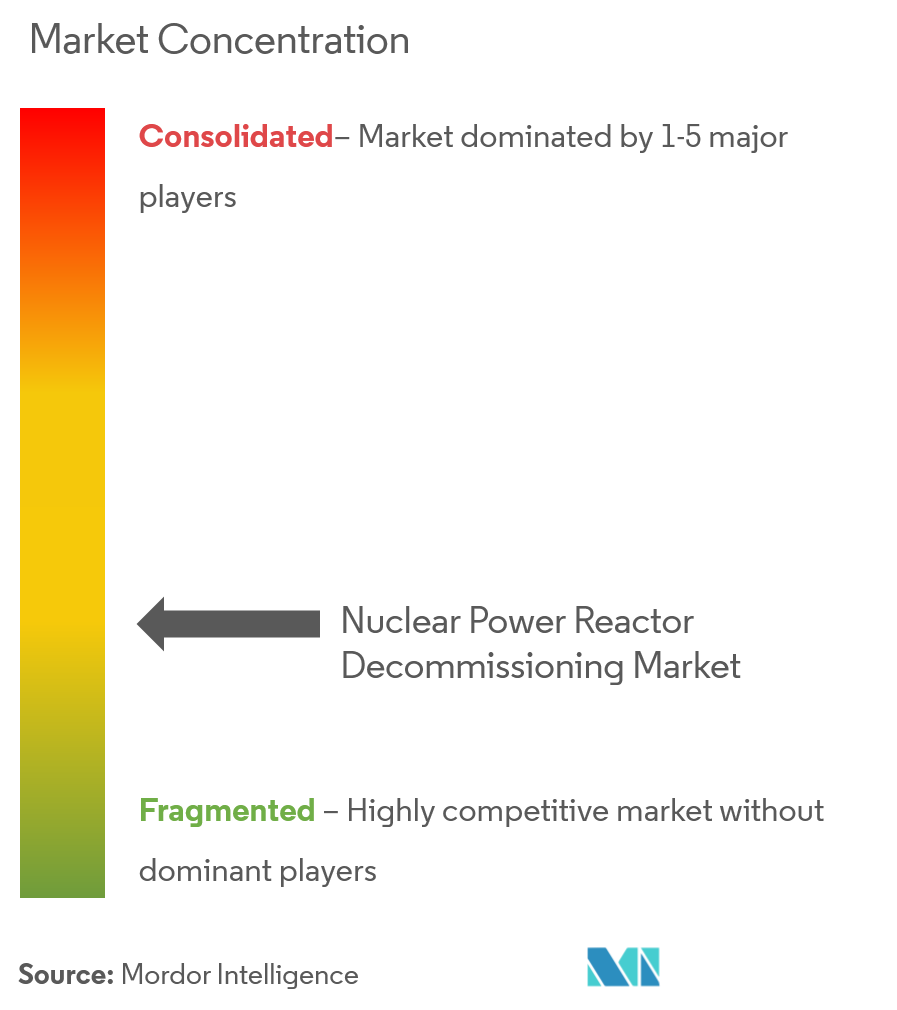

Consolidated Market with Strong Entry Barriers

The nuclear decommissioning market exhibits a highly consolidated structure dominated by large, established engineering and construction conglomerates with extensive nuclear expertise. These major players typically possess comprehensive service portfolios spanning the entire decommissioning lifecycle, from initial planning to final site restoration. The market's high entry barriers stem from stringent regulatory requirements, substantial capital requirements, and the need for specialized technical expertise and safety credentials. Recent years have witnessed strategic consolidation through mergers and acquisitions, particularly among companies seeking to combine complementary capabilities and expand their geographical footprint.

The competitive dynamics are characterized by a mix of global engineering giants and specialized nuclear services providers, with regional players maintaining strong positions in their respective markets through local expertise and established relationships. Market consolidation has been driven by the need to achieve economies of scale, access new technologies, and enhance project execution capabilities. The industry has seen a trend toward the formation of consortiums and joint ventures to pool resources and expertise for large-scale decommissioning projects, particularly in mature nuclear markets like Europe and North America.

Innovation and Expertise Drive Market Success

Success in the nuclear decommissioning market increasingly depends on developing innovative solutions that enhance safety while reducing project timelines and costs. Companies must invest in cutting-edge technologies like robotics and artificial intelligence for remote handling and waste management, while maintaining strong relationships with regulatory authorities and research institutions. Building a track record of successful project completions, maintaining specialized workforce capabilities, and demonstrating financial stability are crucial factors for market leadership. Companies that can offer integrated solutions covering the entire decommissioning lifecycle, while adapting to varying regulatory requirements across different regions, are better positioned to capture market opportunities.

The market's future competitive landscape will be shaped by the ability to manage complex stakeholder relationships, including government agencies, local communities, and environmental groups. Companies must develop robust waste management solutions and demonstrate strong environmental stewardship to maintain their competitive edge. The increasing focus on sustainability and circular economy principles in decommissioning operations presents both challenges and opportunities for market players. Success will depend on balancing cost-effectiveness with safety and environmental considerations, while maintaining flexibility to adapt to evolving regulatory frameworks and technical standards across different markets. The growing demand for power plant decommissioning services further highlights the importance of these capabilities.

Nuclear Power Reactor Decommissioning Market Leaders

-

Babcock International Group PLC

-

GE Hitachi Nuclear Services

-

Fluor Corporation

-

Westinghouse Electric Company

-

AECOM

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Nuclear Power Reactor Decommissioning Market News

In March 2022, Hyundai Engineering & Construction and Holtec signed an agreement to participate in decommissioning a nuclear plant in the United States. The Indian Point Energy Center nuclear power plant in Buchanan, New York, was shut down in April 2021 after 45 years of operation. Hyundai Engineering & Construction would oversee the decommissioning project, dismantling activated parts from nuclear reactors and moving used nuclear fuel from pools into a dry storage system.

In May 2022, Entergy Corporation shut down its Palisades nuclear plant on Lake Michigan. The nuclear power plant had an 800MW power generation capacity. The fuel was removed from the reactor's vessel and placed in the spent fuel pool to cool. After the cooling process, the fuel will be transported to the secured independent spent fuel storage facility on the station property. The company aims to complete decommissioning of the nuclear plant by 2041.

Nuclear Power Reactor Decommissioning Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Scope of Study

- 1.2 Study Assumptions

2. EXECUTIVE SUMMARY

3. RESEARCH METHODOLOGY

4. MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD million, till 2027

- 4.3 Nuclear Power Generation Forecast in TWh, till 2027

- 4.4 Recent Trends and Developments

-

4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

-

4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 By Reactor Type

- 5.1.1 Pressurized Water Reactor

- 5.1.2 Pressurized Heavy Water Reactor

- 5.1.3 Boiling Water Reactor

- 5.1.4 High-temperature Gas-cooled Reactor

- 5.1.5 Liquid Metal Fast Breeder Reactor

- 5.1.6 Other Reactor Types

-

5.2 By Application

- 5.2.1 Commercial Power Reactor

- 5.2.2 Prototype Power Reactor

- 5.2.3 Research Reactor

-

5.3 By Capacity

- 5.3.1 Below 100 MW

- 5.3.2 100-1000 MW

- 5.3.3 Above 1000 MW

-

5.4 By Geography

- 5.4.1 North America

- 5.4.2 Asia-Pacific

- 5.4.3 Europe

- 5.4.4 South America

- 5.4.5 Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

-

6.3 Company Profiles

- 6.3.1 Babcock International Group PLC

- 6.3.2 James Fisher & Sons PLC

- 6.3.3 NorthStar Group Services Inc.

- 6.3.4 Fluor Corporation

- 6.3.5 GE Hitachi Nuclear Services

- 6.3.6 Studsvik AB

- 6.3.7 Enercon Services Inc.

- 6.3.8 Orano Group

- 6.3.9 Aecom

- 6.3.10 Bechtel Group Inc.

- 6.3.11 Westinghouse Electric Company

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Nuclear Power Reactor Decommissioning Industry Segmentation

Decommissioning is the last step in the life cycle of a nuclear power facility. Decommissioning transforms the nuclear facility into an end-state compliant with national regulatory requirements. Earlier, nuclear plants were designed for 30-40 years of operating life, and these power plants had to be decommissioned after the completion of their operational life. However, newer plants are designed for 40-60 years of operating life. At the end of the life of any power plant, the reactor needs to be decommissioned, cleaned up, and dismantled so that the site is available for other users.

The global nuclear power reactor decommissioning market is segmented by reactor type, application, capacity, and geography. By reactor type, the market is segmented into pressurized water reactor, pressurized heavy water reactor, boiling water reactor, high-temperature gas-cooled reactor, liquid metal fast breeder reactor, and other reactor types. By application, the market is segmented into commercial power reactors, prototype power reactors, and research reactors. By capacity, the market is segmented below 100 MW, 100 - 1000 MW, and above 1000 MW. The report also covers the market size and forecasts for the nuclear power reactor decommissioning market across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD million).

| By Reactor Type | Pressurized Water Reactor |

| Pressurized Heavy Water Reactor | |

| Boiling Water Reactor | |

| High-temperature Gas-cooled Reactor | |

| Liquid Metal Fast Breeder Reactor | |

| Other Reactor Types | |

| By Application | Commercial Power Reactor |

| Prototype Power Reactor | |

| Research Reactor | |

| By Capacity | Below 100 MW |

| 100-1000 MW | |

| Above 1000 MW | |

| By Geography | North America |

| Asia-Pacific | |

| Europe | |

| South America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Nuclear Power Reactor Decommissioning Market Research FAQs

What is the current Nuclear Power Reactor Decommissioning Market size?

The Nuclear Power Reactor Decommissioning Market is projected to register a CAGR of 13.8% during the forecast period (2025-2030)

Who are the key players in Nuclear Power Reactor Decommissioning Market?

Babcock International Group PLC, GE Hitachi Nuclear Services, Fluor Corporation, Westinghouse Electric Company and AECOM are the major companies operating in the Nuclear Power Reactor Decommissioning Market.

Which is the fastest growing region in Nuclear Power Reactor Decommissioning Market?

North America is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Nuclear Power Reactor Decommissioning Market?

In 2025, the Europe accounts for the largest market share in Nuclear Power Reactor Decommissioning Market.

What years does this Nuclear Power Reactor Decommissioning Market cover?

The report covers the Nuclear Power Reactor Decommissioning Market historical market size for years: 2021, 2022, 2023 and 2024. The report also forecasts the Nuclear Power Reactor Decommissioning Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Nuclear Power Reactor Decommissioning Market Research

Mordor Intelligence provides comprehensive insights into the nuclear decommissioning market by leveraging extensive industry expertise and robust analytical methodologies. Our detailed analysis covers the full range of nuclear power plant decommissioning activities, from planning to execution. The report examines key nuclear decommissioning companies and their strategic initiatives. It also offers detailed insights into nuclear reactor decommissioning processes and technologies. Our research thoroughly evaluates the nuclear decommissioning services market across major regions, with a particular focus on the nuclear decommissioning services market in Europe and the US nuclear decommissioning market.

Stakeholders can access vital information about power plant decommissioning services through our easy-to-download report PDF. This report includes detailed nuclear decommissioning market analysis and projections for nuclear decommissioning market growth. It provides essential insights for organizations involved in reactor decommissioning activities, offering comprehensive coverage of nuclear power decommissioning trends and developments. Our analysis particularly emphasizes the evolving landscape of the nuclear decommissioning services market intelligence. This enables stakeholders to make informed decisions based on current market dynamics and future opportunities in the sector.