Market Trends of Norway Oil and Gas Industry

This section covers the major market trends shaping the Norway Oil & Gas Market according to our research experts:

The Upstream Sector to Dominate the Market

- The upstream oil and gas investment in Norway has witnessed significant changes since 2014. Though oil production increased during 2014-2016, the operating cost declined during the same period. However, over the past few years, there has been a resurgent demand for increasing gas production to sustain the European economy.

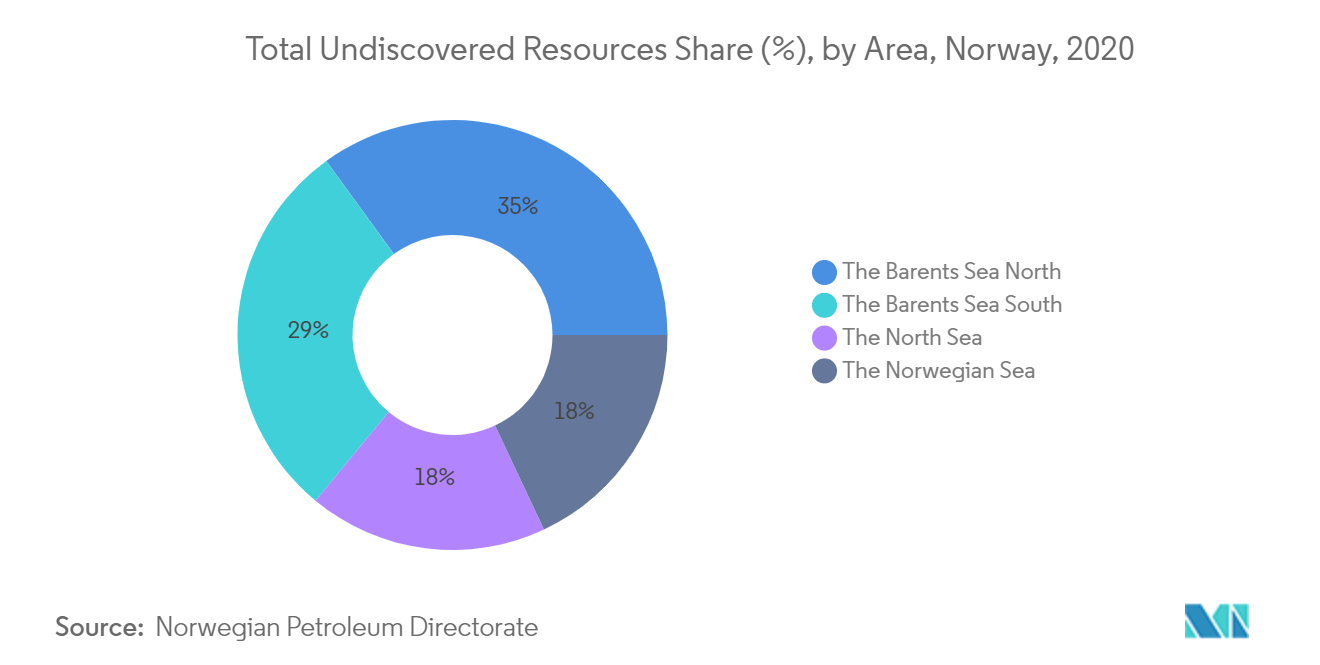

- This can be seen in an uptick in the number of licenses being distributed. For instance, in January 2021, Norwegian Petroleum Directorate announced that the authorities of Norway offered 30 companies with ownership interests in a total of 61 production licenses on the Norwegian Shelf in the Awards in Predefined Areas (APA ) 2020. Out of the 61 new production licenses, 34 were awarded in the North Sea region, which exhibits the 18% of undiscovered oil and gas potential in the country.

- Furthermore, in December 2020, Equinor and its license partners agreed to invest NOK 3 billion in the North Sea Statfjord Øst field to improve recovery by 23 million barrels of oil equivalent. The installation of a pipeline for gas lift, modifications on Statfjord C, and drilling of new wells are planned to start in 2022, while the production is likely to be scheduled for 2024.

- In recent years, companies previously involved in the oil and gas activities in the North Sea are becoming more focused on reducing greenhouse gas emissions from the industry. Further, Norway is seriously targeting to achieve the short-term goals set by European Union for 2030, which are major steps in achieving zero carbon emissions by 2050. Overall, this has led to the creation of more carbon-neutral models with companies using various upstream technologies to reduce greenhouse gas emissions.

- Hence, the upstream sector in Norway is expected to dominate the market due to its increasing exploration activities and the demand shown by countries in Europe for reliable natural gas.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Investments in the Oil and Gas Sector Expected to Drive the Market

- In the European power sector, the gradual phase-out of over 50 GW of nuclear, coal, and lignite-fired power generation capacity is likely to create demand for gas-fired power plants. This change from coal to natural gas is expected to provide room for growth for Norwegian oil and gas as almost all of its natural gas goes to Europe.

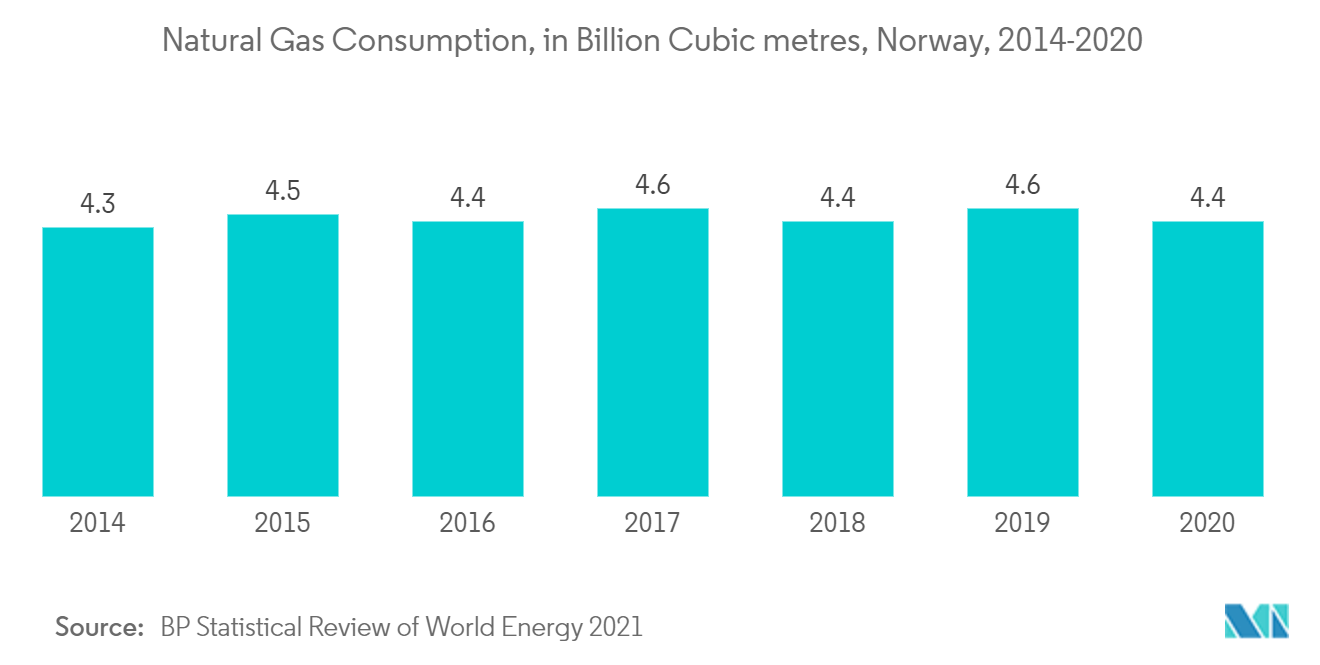

- In 2021, natural gas demand was expected to recover to its pre-crisis levels and increase slightly across the country during the forecast period. In 2020, the consumption of natural gas in the country was around 4.4 billion cubic meters (bcm), which decreased mostly due to COVID-19 from around 4.6 bcm in 2019.

- Therefore, in order to meet the demand and offset the production decline from maturing assets, investments in new oil and gas fields are being undertaken by the operators in the North Sea. These new project sanctions are likely to have a direct impact on increased drilling activity over the next three years, with more than 20 development wells associated with these projects.

- In July 2020, Equinor along with Source Energy AS and Wellesley Petroleum announced the discovery of gas and condensate in the Norwegian North Sea. Preliminary estimates put the proven reserves at between 3 and 10 million standard cubic meters of recoverable oil equivalent, which corresponds to 19-63 million barrels. The gas produced would majorly be exported to meet the demand of other European nations.

- Hence, investments and policies for new oilfields are expected to be the biggest and the most dominating drivers for the Norwegian oil and gas upstream market during the forecast period.