Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

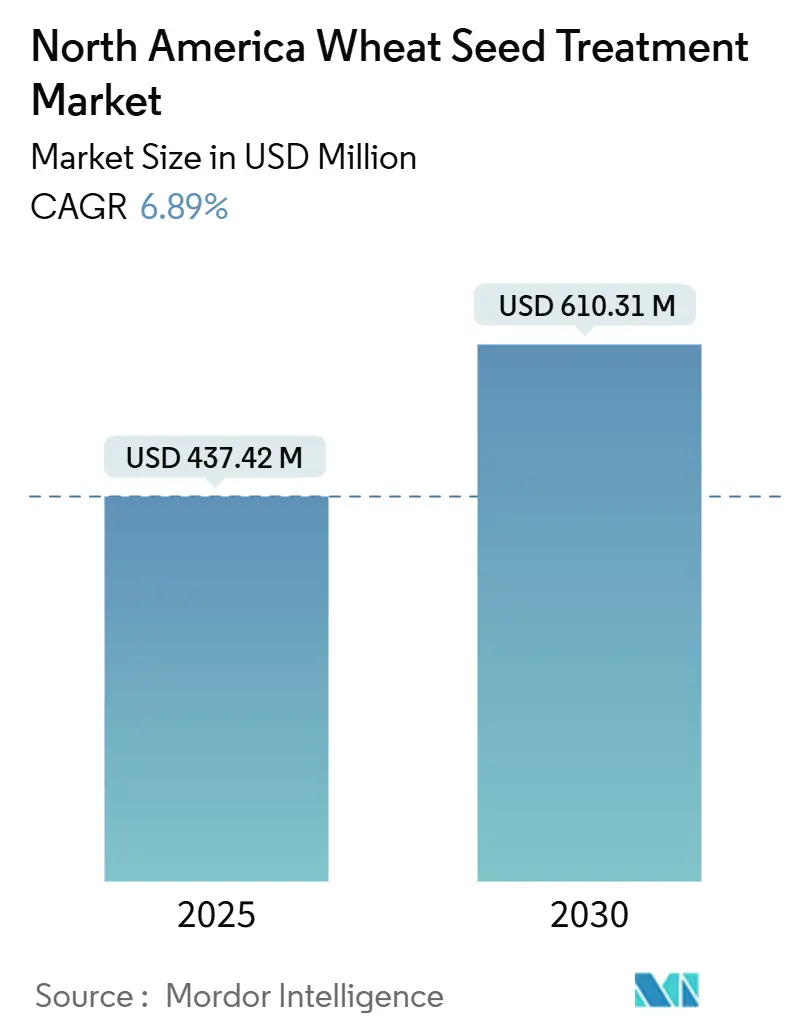

| Market Size (2025) | USD 437.42 Million |

| Market Size (2030) | USD 610.31 Million |

| Growth Rate (2025 - 2030) | 6.89% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Wheat Seed Treatment Market Analysis by Mordor Intelligence

The North America wheat seed treatment market size is estimated to be valued at USD 437.4 million in 2025 and is projected to grow to USD 610.3 million by 2030, registering a CAGR of 6.89%. Farmers are increasingly transitioning from broadcast foliar sprays to precision seed-applied chemistries to address early-season disease and insect pressures while adhering to stricter re-entry regulations. Following the 2024 phase-down of thiram, investments in next-generation active ingredients and polymer film-coat delivery systems have increased. Demand is supported by climate-induced pest migration, the economic benefits of protecting certified seed, and federal programs subsidizing phytosanitary applications. These factors collectively drive the structural growth of the North America wheat seed treatment market, intensifying competition among formulators for shelf space and regulatory approvals.

Key Report Takeaways

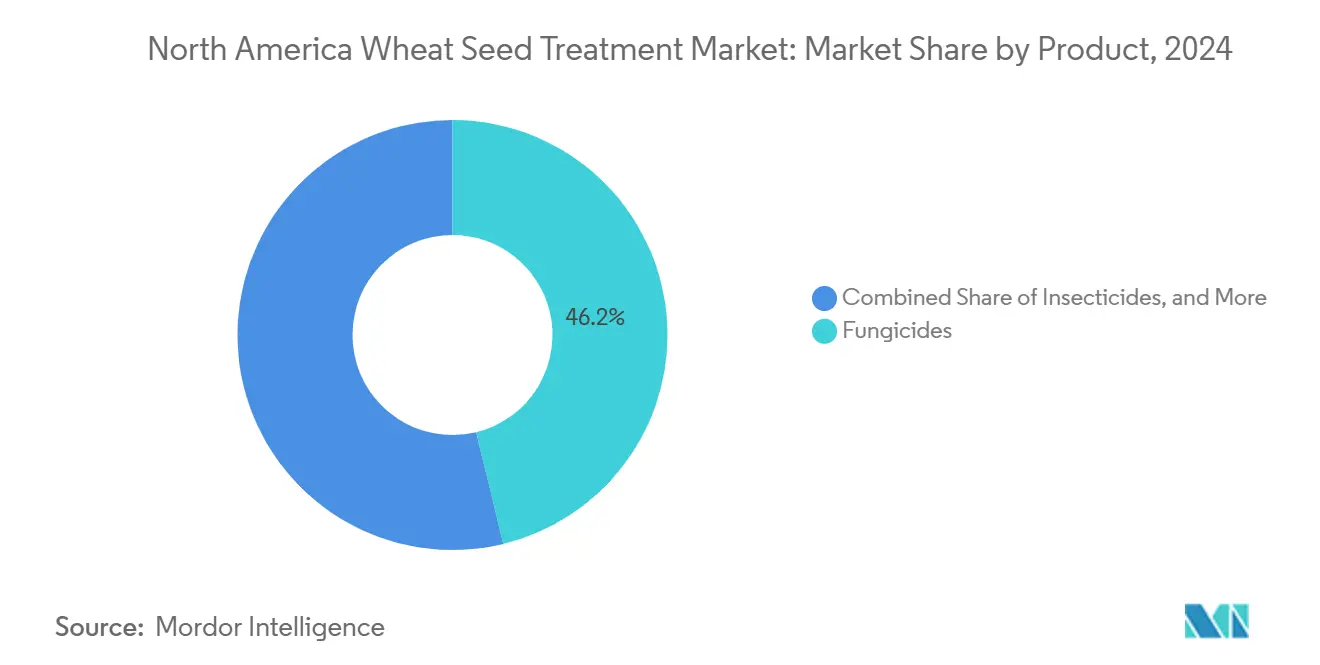

- By product type, fungicides led with a 46.2% of the North America wheat seed treatment market share in 2024, while insecticides are forecast to expand at an 8.2% CAGR through 2030.

- By formulation type, suspension concentrates accounted for 34.3% of the North America wheat seed treatment market size in 2024, whereas polymer film-coat technologies are set to register a 9.1% CAGR through 2030.

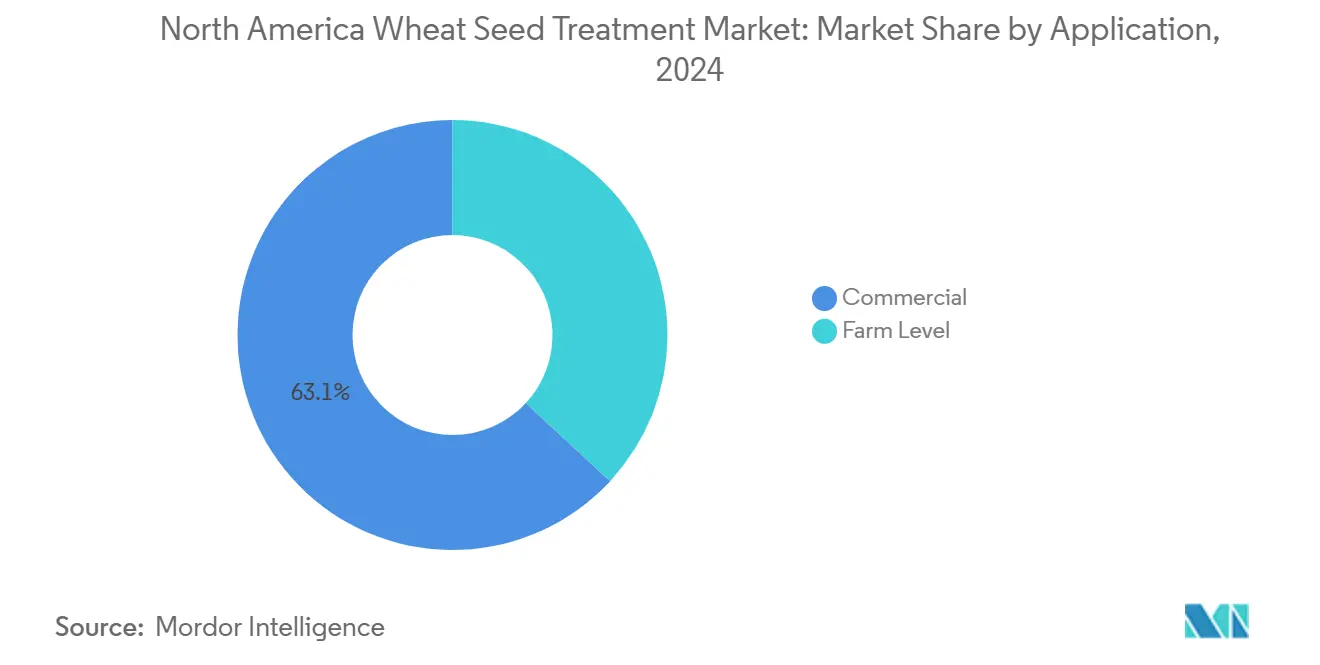

- By application, commercial treatment captured 63.1% of the market share in 2024, and farm-level treatment is projected to grow at the fastest rate, 7.3%, to 2030.

- By geography, the United States dominated with a 71.4% revenue share in 2024; Mexico is poised for the highest growth, at a 7.2% CAGR, during the forecast period.

North America Wheat Seed Treatment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising limitations of soil and foliar pesticide applications | +1.2% | United States and Canada | Medium term (2–4 years) |

| Escalating insect and pest pressure in wheat-growing belts | +1.5% | United States, Canada, and Mexico | Short term (≤ 2 years) |

| Growing demand for certified seed quality and uniform stands | +0.9% | United States and Canada | Long term (≥ 4 years) |

| Stricter United States and Canadian re-entry interval rules favoring seed treatment | +1.3% | United States and Canada | Medium term (2–4 years) |

| Blockchain-enabled grain traceability premiums for treated seed | +0.4% | United States and Canada | Long term (≥ 4 years) |

| Climate-driven expansion of winter-wheat acres in the Northern Plains | +0.8% | United States Northern Plains | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Limitations of Soil and Foliar Pesticide Applications

In the North America wheat seed treatment market, tighter pollinator-protection windows and rising fuel costs have reduced the practicality of broadcast sprays [1]Source: United States Environmental Protection Agency, “Thiram Phase-Down Decision 2024,” EPA.gov. Seed-applied products offer an alternative by avoiding issues such as drift and re-entry restrictions, as the active ingredient remains confined within the furrow. Trials conducted in North Dakota demonstrated that a single seed treatment can achieve the same efficacy as two foliar sprays, while reducing labor and fuel costs by 40% [2]Source: North Dakota State University Extension, “Wheat Seed Treatment Guide 2024,” ag.ndsu.edu. Growers participating in conservation programs are moving away from multiple tillage passes associated with granular soil insecticides, increasing the demand for seed treatments. With 72% of wheat acres in the United States under conservation compliance, the economic benefits of seed treatments are further reinforced.

Escalating Insect and Pest Pressure in Wheat-Growing Belts

Stripe rust, tan spot, and Fusarium head blight caused USD 1.8 billion in crop losses in 2024, significantly driving the demand for fungicides as farmers seek to mitigate these substantial losses [3]Source: United States Department of Agriculture, Agricultural Research Service, “Wheat Disease Losses 2024,” ars.usda.gov. Warmer winters, attributed to changing climatic conditions, now enable pests such as Hessian fly and wheat stem sawfly to survive in regions that were previously too cold, resulting in increased reliance on insecticides to protect wheat crops. In Mexico, the Karnal bunt surveillance program has introduced a requirement for treated seed in interstate movement, effectively transforming what was once a voluntary practice into a legally enforced mandate across 492,404 hectares. This regulatory shift aims to contain the spread of Karnal bunt and safeguard wheat production.

Growing Demand for Certified Seed Quality and Uniform Stands

Certified seed accounts for 38% of plantings in the United States, an increase from 32% in 2020, driven by demand from export buyers for varietal purity. This growth reflects the increasing importance of certified seed in ensuring consistent quality and meeting international trade standards. Several states mandate seed treatment to ensure certification when seedborne diseases pose a risk to trade acceptance, highlighting the critical role of disease management in maintaining market access. The Federal Seed Act requires visible colorants and label declarations, serving as a quality indicator that enables a 15%–20% price premium, further incentivizing the adoption of certified seed. Canada’s Seed Synergy digital records enhance traceability, supporting identity-preserved contracts and fostering greater confidence in the supply chain.

Blockchain-Enabled Grain Traceability Premiums for Treated Seed

Pilot blockchain programs in the Northern Plains track seed treatment status from the field to the elevator, generating premiums of USD 0.15–0.25 per bushel. These systems support food-safety certifications by ensuring compliance with stringent standards and reducing the risk of contamination. They also mitigate commingling risks, which led to USD 120 million worth of rejected export shipments in 2023. Although currently less than 5% of wheat acres are involved in these programs, early results demonstrate the potential for traceability premiums to significantly influence purchasing decisions, encouraging the adoption of treated seed and enhancing overall supply chain transparency.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited grower awareness of optimal application rates | –0.6% | United States and Mexico | Short term (≤ 2 years) |

| Rapid adoption of wheat hybrids with stacked pest-resistant traits | –0.9% | United States Northern Plains and Canadian Prairies | Long term (≥ 4 years) |

| Retailer pressure for lower chemical residues in value-chain certified wheat | –0.5% | United States and Canada | Medium term (2–4 years) |

| Active-ingredient shortages following the Environmental Protection Agency phase-down of thiram | –0.7% | United States, Canada, and Mexico | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Grower Awareness of Optimal Application Rates

Surveys conducted in Kansas and Oklahoma indicate that 42% of farm-level applicators either underdose or overapply seed treatments, reducing their effectiveness and, in some cases, causing phytotoxicity, according to the Kansas State University (K-State). Similarly, smallholders in Mexico encounter knowledge gaps, as extension services are concentrated in irrigated regions. Misapplication of seed treatments can result in excess active ingredients leaching into groundwater, leading to increased regulatory scrutiny and potential restrictions on product labels. Training programs under SENASICA’s NOM-022 aim to improve application standards; however, there are fewer than 200 certified providers currently available to meet national demand.

Retailer Pressure for Lower Chemical Residues in Value-Chain Certified Wheat

Sustainability programs require stricter maximum residue limits, often set at half the federal vomitoxin threshold, to obtain premium flour contracts. These stringent requirements are driven by the growing demand for higher-quality and safer food products, emphasizing the importance of compliance with regulatory standards. This necessitates the development of shorter half-life chemistries, which presents a significant technical challenge. The complexity of this process leads to increased research and development costs and longer time-to-market cycles, which in turn impact the overall efficiency of product development. Additionally, the European Union's default limit of 0.01 mg/kg for unlisted pesticides effectively restricts the use of certain neonicotinoids. This regulation forces growers to adapt by relying on a narrower range of active ingredients, which may affect crop protection strategies and agricultural productivity.

Segment Analysis

By Product Type: Fungicides Remain the Mainstay

Fungicides accounted for 46.2% of the North America wheat seed treatment market revenue in 2024, as growers addressed challenges from stripe rust, tan spot, and Fusarium head blight, which collectively resulted in USD 1.8 billion in crop losses. Strobilurin and succinate dehydrogenase inhibitor combinations provided systemic protection for four to six weeks of seedling growth, driving high adoption rates. Following the phase-down of thiram, growers transitioned to premium sedaxane and fludioxonil blends, increasing the average per-acre expenditure to USD 5.20 and contributing to the current market size for this segment.

Insecticides represent the fastest-growing category, with a projected CAGR of 8.2% through 2030, driven by warmer winters that are expanding the range of pests such as the Hessian fly and wheat stem sawfly. Alternatives like chlorantraniliprole are gaining traction in regions where concerns over neonicotinoid exports persist, highlighting a strategic shift projected to expand the insecticide segment of the North America wheat seed treatment market by the end of the decade. Nematicides continue to play a niche role due to their inconsistent standalone efficacy.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Formulation Type: Liquids Lead While Polymer Films Gain Speed

Suspension concentrates accounted for 34.3% of the North America wheat seed treatment market size in 2024, valued for their compatibility with automated coating lines and multi-active blending. These formulations are particularly advantageous for large-scale operations requiring efficient and uniform seed coverage. Challenges such as nozzle clogging during cold seeding periods and concerns over dust drift have prompted the exploration of alternative solutions.

Polymer film-coat systems, which reduce airborne particles by 85%, are projected to grow at an annual rate of 9.1%, making them the fastest-growing formulation category. This growth is driven by increasing regulatory focus on minimizing environmental impact and the rising demand for advanced seed treatment technologies that enhance planting efficiency. Film-coat adoption is most prominent in the United States, where commercial treater capacity offsets the USD 500,000 line-cost barrier. Liquid flowables remain a preferred choice for farm-level applicators due to their lower capital requirements and ease of use, maintaining a balance in the North America wheat seed treatment market between cost-efficient liquid platforms and premium film-coating technologies. This equilibrium ensures that both small-scale and large-scale operations can access suitable seed treatment solutions tailored to their specific needs.

By Application: Commercial Dominates, Farm-Level Accelerates

Commercial treatment is projected to account for 63.1% of the North America wheat seed treatment market in 2024. This dominance is attributed to large seed companies offering uniform coverage, regulatory compliance, and traceability. By embedding treatment costs directly into seed invoices rather than farm budgets, commercial treatment provides a streamlined and efficient solution for farmers, ensuring consistency and adherence to industry standards. This approach not only simplifies the procurement process but also enhances the overall value proposition for growers by reducing administrative burdens and ensuring high-quality treatment outcomes.

The farm-level application is experiencing an annual growth rate of 7.3%, driven by prairie producers utilizing slurry systems to treat retained seeds at a cost of USD 4–6 per acre, thereby avoiding the USD 8–15 commercial premium. This method allows producers to achieve cost savings while maintaining control over the treatment process. The expansion of farm-level application is contingent on several critical factors, including the availability of extension training programs to educate farmers on best practices, access to proprietary treatment products that meet regulatory and performance standards, and the ability to manage recordkeeping requirements effectively. These factors can present challenges, particularly for smaller operations with limited resources, which may impact their ability to adopt farm-level treatment methods at scale.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The United States accounted for 71.4% of the North America wheat seed treatment market share in 2024, supported by 38.5 million harvested acres and an extensive commercial treatment network. The demand for fungicides is driven by hard red winter wheat in the Southern Plains, where high pressure from stripe rust is prevalent. In the Northern Plains, the cultivation of spring wheat has led to an increase in insecticide usage to combat pests such as the Hessian fly and sawfly. The adoption of polymer film coatings has accelerated following the phase-down of thiram, ensuring compliance with stricter dust-drift regulations. While hybrid wheat may reduce insecticide usage later in the decade, overall demand in the United States is projected to continue growing.

Mexico is the fastest-growing market in the region, with an annual growth rate of 7.2%, driven by intensified Karnal bunt surveillance and government subsidies covering 30%–40% of growers’ phytosanitary costs. Although there are fewer than 200 certified treaters, harmonized NOM-032 standards have simplified cross-border registrations, enabling access to premium products. Increasing pest pressure in regions such as Sonora and Guanajuato, combined with year-round cropping practices, is contributing to a steady rise in treatment volumes.

Canada’s 24.7 million wheat acres support consistent demand for seed treatments as growers address challenges like Fusarium head blight and leaf rust. Provincial associations promote shared treatment facilities, and 28% of growers now self-treat retained seed to reduce costs. Although breeding programs valued at CAD 19.9 million (USD 14.5 million) aim to reduce chemical reliance after 2028, seed protection remains a critical strategy until stacked traits are widely adopted.

Competitive Landscape

Market concentration is moderate, with the top five companies, Syngenta Group, Bayer AG, BASF SE, Corteva Agriscience, and FMC Corporation, collectively holding a significant share in 2024. These firms link proprietary chemistries to branded seed genetics, creating pull-through demand. Syngenta’s hybrid wheat expansion has driven increased sales of Vibrance fungicide, while Corteva’s Lumisena received PMRA approval in 2025, addressing triazole resistance. The replacement of Thiram has led to higher per-acre treatment prices, improving margins for suppliers with diversified portfolios.

Smaller companies, such as Vive Crop Protection and Meristem Crop Performance, specialize in creating custom blends that enhance rainfastness and root uptake, catering to growers who seek tailored solutions. Polymer film-coat technology presents a growth opportunity but requires significant capital investment, which discourages mid-sized treaters. FMC experienced a 23% rebound in seed treatment revenue in late 2024, demonstrating elastic demand as inventories normalized.

Digital agronomy tools are introducing new switching costs. Bayer’s Climate FieldView pilot in Montana and North Dakota integrates live pest and weather data to optimize treatment prescriptions. The adoption of stacked pest-resistant traits could reduce chemical demand by approximately 15% after 2028. Slow trait deployment and hesitancy in export markets are likely to limit near-term disruption. Overall, competition in the market is driven by regulatory agility, formulation patents, and digital service ecosystems rather than price alone.

North America Wheat Seed Treatment Industry Leaders

Syngenta AG

BASF SE

Corteva Agriscience

Bayer AG

FMC Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2025: Syngenta has launched its latest product for cereals, CruiserMaxx Vibrance Elite seed treatment, which the U.S. Environmental Protection Agency has registered. CruiserMaxx Vibrance Elite, a fungicide and insecticide seed treatment premix, is an enhanced formulation of CruiserMaxx Vibrance, specifically designed for use on cereals, including wheat.

- September 2025: Bayer AG introduced the Raxil Rise cereal fungicide seed treatment for Canadian cereal farmers, including those cultivating wheat. Raxil Rise enhances the existing Raxil formulation, which includes Group 3 Tebuconazole, Group 3 Prothioconazole, and Group 4 Metalaxyl, by incorporating Group 7 Penflufen.

- May 2024: BASF SE launched the fungicide Sistiva for treating wheat seeds. This solution contains the active ingredient Xemium (Fluxapyroxad), which belongs to the carboxamide group. It is designed to target powdery mildew and leaf rust.

North America Wheat Seed Treatment Market Report Scope

Seed treatment products are biological, physical, and chemical agents and techniques applied to seeds to protect and improve the establishment of healthy crops. The North America wheat seed treatment market is segmented by Chemical Type (Synthetic, Biological), Product Type (Insecticide, Fungicide, Nematicide, and Other Product Types), Application (Commercial, and Farm Level), and Geography (United States, Canada, Mexico, and the Rest of North America). The report offers market size and forecasts in value (USD) for all the above segments.

By Product Type

| Insecticides |

| Fungicides |

| Nematicides |

| Other Product Types |

By Formulation Type

| Liquid Flowable |

| Suspension Concentrate |

| Dry Powder |

| Polymer Film-Coat |

By Application

| Commercial |

| Farm Level |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Insecticides |

| Fungicides | |

| Nematicides | |

| Other Product Types | |

| By Formulation Type | Liquid Flowable |

| Suspension Concentrate | |

| Dry Powder | |

| Polymer Film-Coat | |

| By Application | Commercial |

| Farm Level | |

| By Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the North America wheat seed treatment market in 2025?

It is valued at USD 437.42 million and is forecast to climb to USD 610.31 million by 2030.

Which product type generates the most revenue?

Fungicides lead with 46.2% of revenue due to effective control of major wheat diseases.

Why is Mexico the fastest-growing territory?

Federal subsidies and stricter Karnal bunt surveillance fuel a forecast 7.2% CAGR through 2030.

What drives polymer film-coat adoption?

Film coats cut dust drift by 85% and meet new EPA guidelines while improving seed flowability.

How will hybrid wheat affect seed treatment demand?

Stacked pest-resistant traits could trim chemical use by 15% after 2028, but slow deployment tempers near-term impact.