North America Wire And Cable Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 37.71 Billion |

| Market Size (2030) | USD 47.90 Billion |

| Growth Rate (2025 - 2030) | 4.90% CAGR |

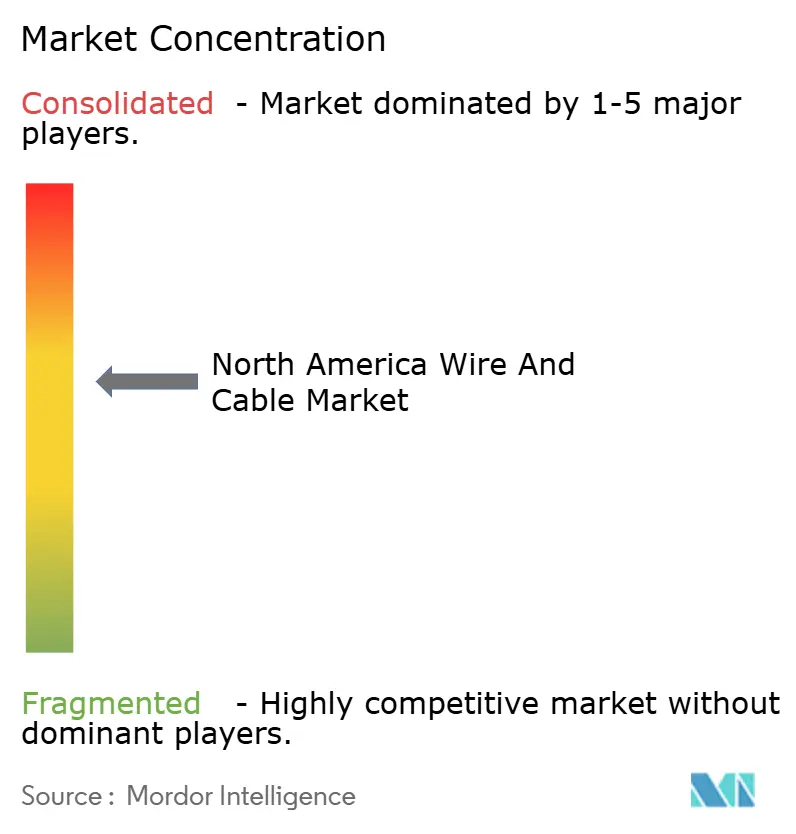

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Wire And Cable Market Analysis by Mordor Intelligence

The North America wire and cable market size stood at USD 37.71 billion in 2025 and is forecast to reach USD 47.90 billion by 2030, reflecting a 4.9% CAGR. This expansion mirrors accelerating grid-modernization programs funded by the Bipartisan Infrastructure Law, a surge in renewable-energy interconnections, and hyperscale data-center construction that together underpin multi-year purchasing pipelines for regional manufacturers. Utilities are re-weighting procurement priorities toward supply-chain resilience over lowest-price bids, incentivizing domestic capacity additions under Buy America content thresholds.[1]U.S. Department of Energy, “Evaluating Electricity Procurement Options for Federal Agencies,” ENERGY.GOV Composite-core conductors, high-density fiber designs, and hybrid power-data cables are gaining traction as utilities and data-center operators seek higher current-carrying headroom and embedded monitoring capabilities. Meanwhile, copper-price volatility and skilled-labor shortages are prompting manufacturers to embed dynamic-pricing clauses and invest in automation to protect margins and sustain delivery schedules.

Key Report Takeaways

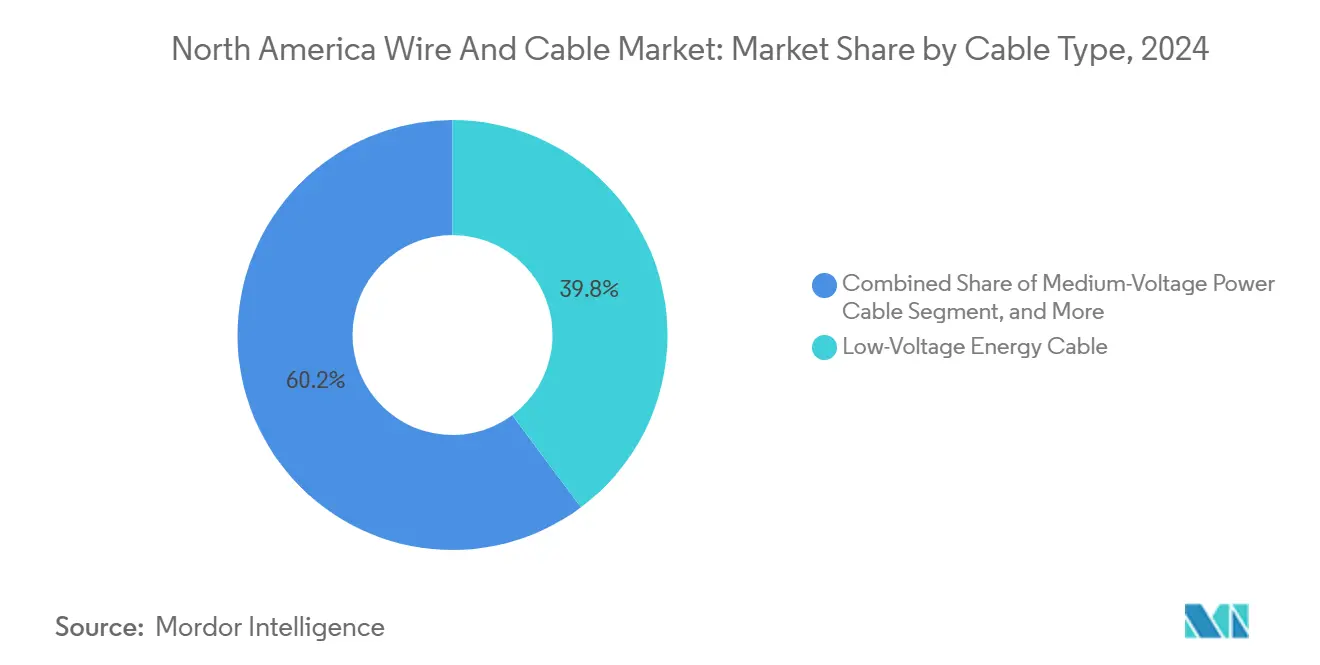

- By cable type, low-voltage energy cables led with 39.8% revenue share of the North America wire and cable market in 2024, while fiber-optic variants are projected to post the fastest 6.5% CAGR to 2030.

- By voltage rating, the < 1 kV class accounted for a 42.8% share of the North America wire and cable market in 2024; the 36-69 kV bracket is expected to register the highest 6.4% CAGR through 2030.

- By installation type, overhead lines dominated at 48.7% share of the North America wire and cable market in 2024, whereas submarine projects are forecast to expand at a 6.2% CAGR over the same period.

- By conductor material, copper maintained a 53.2% share of the North America wire and cable market in 2024, while composite/high-strength core designs are on track for a 5.9% CAGR to 2030.

- By end-user industry, construction contributed a 30.8% share of the North America wire and cable market in 2024; telecommunications and data centers are anticipated to achieve a 6.3% CAGR to 2030.

- By country, the United States commanded 82.4% revenue of the North America wire and cable market in 2024, and Mexico is set to grow the quickest at a 6.0% CAGR through 2030.

- Prysmian, Southwire, and CommScope collectively held about 46% of 2024 shipments, underscoring moderate market concentration.

North America Wire And Cable Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising investments in infrastructure modernisation | +1.2% | United States, Canada | Medium term (2-4 years) |

| Accelerated smart-grid and grid-hardening roll-outs | +0.9% | North America | Long term (≥ 4 years) |

| Utility-scale renewable energy cabling demand surge | +0.8% | United States, Mexico | Medium term (2-4 years) |

| Edge-data-centre and hyperscale fibre build-out wave | +0.7% | United States, Canada | Short term (≤ 2 years) |

| "Buy-America" sourcing clauses in Bipartisan Infrastructure Law | +0.5% | United States | Medium term (2-4 years) |

| HVDC underground links for offshore-wind clusters | +0.3% | United States, Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Infrastructure-modernization spending

A dedicated USD 65 billion federal allocation for grid upgrades is accelerating the replacement of aging conductors with advanced aluminum-composite and high-temperature designs, while USD 2.5 billion in resilience grants has shifted utility preferences toward underground routes and fire-resistant insulation.[2]U.S. Department of Energy, “Energy and Project Procurement Development Services,” ENERGY.GOV Domestic-content clauses guarantee local manufacturers sustained order visibility, enabling plants to run at higher asset-utilization rates. Municipal utilities and rural co-operatives are also tapping performance-contracting frameworks that bundle design, build, and maintenance services, compressing project lead times to within two-year budget cycles.

Smart-grid and grid-hardening roll-outs

Utilities piloting fiber-optic temperature-sensing strands across distribution lines obtain real-time ampacity data, deferring costly reconductoring and reducing wildfire risk; Minnesota’s deployment illustrates the proof of concept. Parallel grid-hardening budgets, such as PG&E’s USD 6 billion annual outlay, are steering demand toward insulated tree-wire and covered conductor systems able to withstand extreme weather. Regulatory cybersecurity mandates further elevate specifications for hybrid power-fiber cables that support secure data channels alongside energy transfer.

Utility-scale renewable cabling demand

Offshore wind developments now specify 525 kV HVDC export links with ≥ 2 GW capacity, pushing submarine-cable suppliers to expand steel-armored production lines. Solar and battery-storage farms are standardizing on 1,500 V DC-rated connectors, a shift that multiplies copper and aluminum consumption per megawatt. Long-term supply agreements between independent power producers and cable makers lock in volumes across multi-phase buildouts, smoothing revenue curves for both parties.

Edge-data-center and hyperscale fiber wave

AI training clusters require 800 G to 1.6 T optics, raising fiber counts to 864 strands within ≤ 10 mm diameters; rollable-ribbon formats from OFS satisfy these density targets. At the edge, micro-duct deployments in metro rights-of-way favor ruggedized designs that withstand repeated thermal cycling. Liquid-cooled server halls are piloting hybrid tubes carrying both coolant and fiber, an emerging niche for integrated power-over-fiber assemblies certified up to 430 V DC.[3]Panduit Corp., “Fault Managed Power over Optical Network Channels,” PANDUIT.COM

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High installation costs for underground and submarine cables | -0.8% | North America | Medium term (2-4 years) |

| Copper and aluminium price volatility | -0.6% | North America | Short term (≤ 2 years) |

| Skilled-labour bottlenecks for fibre/HV installations | -0.5% | United States, Canada | Long term (≥ 4 years) |

| Lengthy permitting and ROW approvals for new corridors | -0.4% | United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High underground and submarine installation cost

Underground distribution work can cost 4.5 times more than overhead construction, while submarine installation windows hinge on vessel availability and seasonal weather. Limited specialty-contractor fleets inflate day-rates and prolong project timelines, forcing utilities to balance resilience benefits against capital budgets. Cost-optimization now centers on route-engineering software and joint-trench programs that consolidate electrical, telecom, and gas conduits within a single excavation to dilute per-foot expenses.

Copper and aluminum price volatility

Spot prices swung between USD 8,200–11,500 per t for copper and hovered near USD 2,400 per t for aluminum in 2024, pressuring manufacturers to hedge and adopt pass-through pricing. Utilities increasingly accept indexed clauses pegged to COMEX averages, though that practice complicates multi-year capital planning. Composite-core and aluminum-clad designs offer partial mitigation, yet performance trade-offs restrict substitution in high-load centers. Vertical-integration moves, such as cable-makers acquiring rod mills, aim to curb raw-material exposure.

Segment Analysis

By Cable Type: Fiber Optics Accelerate Digital Links

Low-voltage energy conductors sustained 39.8% revenue in 2024 on the back of resilient residential and commercial construction. Conversely, fiber-optic variants are registering a 6.5% CAGR to 2030, propelled by telco 5G roll-outs and cloud-provider AI clusters. The North America wire and cable market size for fiber segments is projected to add USD 3.1 billion by 2030. Signal-and-control lines also benefit from factory-automation retrofits that embed sensors across production lines.

Composite fiber designs with rollable ribbons enable 2,000-strand vaults in compact footprints, trimming duct-leasing costs for carriers. Low-smoke zero-halogen jackets are gaining code acceptance in data centers, while bend-insensitive single-mode cores improve slack management in tight trays. In power, medium-voltage shielded cables remain the workhorse for distribution upgrades, whereas high-voltage XLPE and HVDC extruded systems service 300 km offshore wind export runs. As utilities converge data and energy networks, hybrid power-fiber cables reinforce synergies within the North America wire and cable market.

Note: Segment shares of all individual segments available upon report purchase

By Voltage Rating: Mid-Range Leads Grid Modernization

The sub-1 kV bracket accounted for 42.8% shipments in 2024, anchored in residential feeders and building wiring. Yet, the 36–69 kV span exhibits the fastest 6.4% CAGR, mirroring feeder-backbone enhancements and renewable interconnections. This tier often delivers the best cost-capacity trade-off for suburban substations, explaining its outsized traction in planned capital budgets.

Utilities are specifying advanced aluminum-composite and high-temperature low-sag variants within 69–220 kV upgrades to double ampacity without wider rights-of-way. Such specifications lift conductor-per-mile revenues, reinforcing the North America wire and cable market’s profitability. IEEE C57 revisions covering higher continuous-operating temperatures further legitimize adoption. Simultaneously, code cycles in commercial real estate push smart-building LV cabling to support PoE lighting and occupancy analytics, expanding the low-voltage revenue base.

By Installation Type: Submarine Lines Ride Offshore Wind Wave

Overhead networks still dominate at 48.7% in 2024 due to lower CAPEX and rapid build rates. However, submarine segments are projected for a 6.2% CAGR as coastal states approve 30 GW of offshore wind through 2030. Each 2 GW cluster can consume ≥ 1,000 km of 525 kV HVDC export cable, translating into multi-billion-dollar procurement lots.[4]Prysmian Group, “Prysmian Signs Offshore Wind HVDC Contracts,” PRYSMIAN.COM

Underground urban feeders gain relevance where wildfire mitigation or aesthetic mandates override initial cost premiums. Utilities are coupling underground builds with fiber backbones to justify the spend through telecom lease income. Aerial micro-duct systems around metropolitan poles enable carriers to deploy fiber quickly without trenching, a niche but expanding slice within the North America wire and cable market.

Note: Segment shares of all individual segments available upon report purchase

By Conductor Material: Composite Cores Gain Momentum

Copper retained 53.2% revenue in 2024 owing to unrivaled conductivity and entrenched standards. Composite-core conductors are forecast for a 5.9% CAGR as transmission owners validate 2× ampacity and lower thermal sag. Aluminum remains favored in sub-transmission spans where tower loading and budget constraints outweigh marginal losses.

Composite adoption is accelerating after successful pilots showed compatibility with existing hardware, easing retrofit risk. Manufacturers are publicizing total-lifecycle economics that combine reduced tower counts and deferred corridor acquisition, strengthening the North America wire and cable market’s value proposition. Meanwhile, copper-clad aluminum finds uptake in branch circuits and EV-charging whips, balancing cost with higher-frequency performance.

By End-User Industry: Telecom Outpaces Traditional Segments

Construction led with a 30.8% share in 2024, but telecommunications and data centers delivered the highest 6.3% CAGR through 2030, fueled by hyperscale expansion and FTTP drives. Power-utility demand remains steady, anchored in regulated rate-base investment. Industrial automation upgrades in discrete manufacturing plants unlock fresh volumes for shielded control lines.

EV-platform assembly lines require high-temperature magnet wire and silicone-jacketed flex cables, bolstering specialty wire revenues. Renewable facilities integrate 1,500 V DC arrays and battery BESS tie-ins, demanding thicker insulation and temperature-cycling resilience. The wide application mix cushions cyclic slowdowns in any one vertical, supporting resilient growth across the North America wire and cable market.

Geography Analysis

The United States held 82.4% revenue in 2024 on the strength of federal infrastructure outlays and advanced manufacturing bases. Intensive U.S. federal funding paired with Buy America clauses funnels predictable volume into domestic plants, encouraging multinationals to expand Gulf Coast copper-rod casting and Southeast optical-fiber extrusion lines. Data-center developers in Virginia, Ohio, and Texas continue to rank among the world’s largest single-site fiber consumers, often pre-purchasing cable reels 12 months ahead to lock in allocations. Utilities in wildfire-prone California, Oregon, and Washington are pivoting to covered conductors and underground circuits to cut outage risk, a trend that increases copper weight per circuit and reinforces revenue in the North America wire and cable market.

Mexico tracks a 6.0% CAGR through 2030 as Comisión Federal de Electricidad accelerates its USD 4.2 billion grid-expansion blueprint that includes 145 transmission and 86 distribution projects. In Mexico, CFE’s expansion program allocates USD 3.6 billion to distribution-level improvements through 2030, driving medium-voltage demand. Offshore Gulf wind prospects and the Santa Catarina solar complex require bespoke HVDC export designs, introducing submarine suppliers to new Latin bids. Government incentives for semiconductor and EV assembly clusters are spurring greenfield industrial park construction, boosting low-voltage building-wire pull-through.

Canada’s major utilities are reinforcing hydro-powered export corridors to the United States, necessitating high-ampacity composite lines over long northern spans. Remote mining operations in the Yukon and Nunavut employ armored aluminum cables resistant to low-temperature embrittlement. Provincial broadband schemes targeting 50/10 Mbps universal service accelerate rural fiber builds, enlarging the addressable base within the North America wire and cable market.

Competitive Landscape

The market reflects moderate concentration: the five largest players contributed about 60% of 2024 shipments as measured by revenue. Prysmian’s USD 950 million buyout of Channell Commercial Corporation signals a pivot toward integrated connectivity kits spanning conduits, cabinets, and high-density cable assemblies. Southwire is automating rod-mill lines to dampen copper-price shocks and claims a 15% unit-cost drop on new AI-aided packaging cells. CommScope is leveraging fiber-jacketing know-how to supply hybrid power-fiber structures for edge micro-data halls.

Material security is driving vertical integration; several incumbents have secured off-take agreements with North American copper-smelter restarts, linking cathode supply to in-house wire-drawing capacity. Technology roadmaps prioritize conductor ampacity and embedded analytics: Far East Cable’s chip-embedded products transmit conductor-core temperature data every five seconds, aiding predictive maintenance. New entrants centered on composite cores face qualification hurdles but can win niche projects through single-circuit uprating proposals.

Strategic partnerships are forming between cable vendors and EPC firms to submit turnkey bids that bundle design, supply, and installation. Patent filings around fault-managed power over optical networks reached record levels in 2025, confirming a convergence pathway between energy and data plumbing. Given the capital intensity of extrusion and stranding assets, incumbents continue to enjoy scale economics, yet differentiated digital add-ons may unlock premium margins and shift share in the North America wire and cable market.

North America Wire And Cable Industry Leaders

-

Prysmian Group USA, Inc.

-

Nexans AmerCable Incorporated

-

Southwire Company, LLC

-

CommScope Holding Company, Inc.

-

Belden Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Prysmian agreed to acquire Channell Commercial Corporation for USD 950 million to deepen digital-solutions offerings and strengthen its North American footprint.

- March 2025: CFE approved its 2025-2030 expansion plan covering 12 new power plants and 145 transmission projects valued at USD 4.2 billion.

- January 2025: Minnesota utilities began field deployment of fiber-optic sensing strands that transform existing cables into distributed smart sensors.

- December 2024: Prysmian unveiled EcoSpan FlexRibbon cables manufactured in Tennessee and the Carolinas for rural broadband buildouts.

North America Wire And Cable Market Report Scope

A cable consists of more insulated wires wrapped in a single jacket that permits them to pass through, whereas a wire is a single conductor. The scope of the study includes various forms of wire and cable installations deployed in essential end-user facilities such as telecommunications, construction, and power infrastructure.

The study tracks the revenue accrued from the sales of various types of wires and cables, such as low voltage energy, power cables, fiber optic cables, and signal and control cables that are shipped for various end-user applications in North America. The market forecast depends on many factors, including historical trends, automation trends, sales projections by various segments, government initiatives, and the impact of various macro trends. The study also offers a detailed analysis of trends, market estimates and projections, and growth dynamics across various types of cables and end-user industries.

The North American wire and Cable Market is segmented by Cable Type (Low Voltage Energy, Power Cable, Fiber Optic Cable, Signal and Control Cable, Other Cable Types (Co-Axial, Telecom and Data Cables), End-user Industry (Construction (Residential and Commercial), Telecommunications (IT and Telecom), Power Infrastructure (Energy and Power and Automotive), Other End-user Industries (BFSI, Railway, Defense/Military, Industrial, Medical)), and Country (United States, Canada). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Low-Voltage Energy Cable |

| Medium-Voltage Power Cable |

| High / Extra-High-Voltage Cable |

| Fiber-Optic Cable |

| Signal and Control Cable |

| Co-axial and Data Cable |

| Specialty Wire (Magnet, Stranded, etc.) |

| < 1 kV |

| 1 – 35 kV |

| 36 – 69 kV |

| 69 – 220 kV |

| Overhead |

| Underground |

| Submarine |

| Indoor/Building |

| Aerial Micro-duct |

| Copper |

| Aluminium |

| Copper-Clad Aluminium |

| Composite/High-Strength Core |

| Construction (Residential and Commercial) |

| Power Transmission and Distribution Utilities |

| Telecommunications and Data Centres |

| Industrial Manufacturing |

| Automotive and Transportation (EV/Rail) |

| Renewable Energy (Solar, Wind) |

| Oil, Gas and Mining |

| Military and Defence |

| Other End-user Industries |

| United States |

| Canada |

| Mexico |

| By Cable Type | Low-Voltage Energy Cable |

| Medium-Voltage Power Cable | |

| High / Extra-High-Voltage Cable | |

| Fiber-Optic Cable | |

| Signal and Control Cable | |

| Co-axial and Data Cable | |

| Specialty Wire (Magnet, Stranded, etc.) | |

| By Voltage Rating | < 1 kV |

| 1 – 35 kV | |

| 36 – 69 kV | |

| 69 – 220 kV | |

| By Installation Type | Overhead |

| Underground | |

| Submarine | |

| Indoor/Building | |

| Aerial Micro-duct | |

| By Conductor Material | Copper |

| Aluminium | |

| Copper-Clad Aluminium | |

| Composite/High-Strength Core | |

| By End-user Industry | Construction (Residential and Commercial) |

| Power Transmission and Distribution Utilities | |

| Telecommunications and Data Centres | |

| Industrial Manufacturing | |

| Automotive and Transportation (EV/Rail) | |

| Renewable Energy (Solar, Wind) | |

| Oil, Gas and Mining | |

| Military and Defence | |

| Other End-user Industries | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the North America wire and cable market in 2025?

It reached USD 37.71 billion in 2025 and is projected to grow at a 4.9% CAGR to 2030.

Which cable type is growing fastest in North America?

Fiber-optic cables are advancing at a 6.5% CAGR due to AI-driven data-center and 5G builds.

Why are submarine cables gaining attention in North America?

Offshore-wind export links require 525 kV HVDC submarine systems, driving a 6.2% CAGR for this installation class.

What drives Mexico’s cable demand?

CFE’s USD 4.2 billion grid-modernization program and near-shoring industrial projects boost medium- and high-voltage needs.

Which materials are utilities adopting for capacity upgrades?

Composite-core conductors that double ampacity without new towers are gaining momentum across 69-220 kV lines.