Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

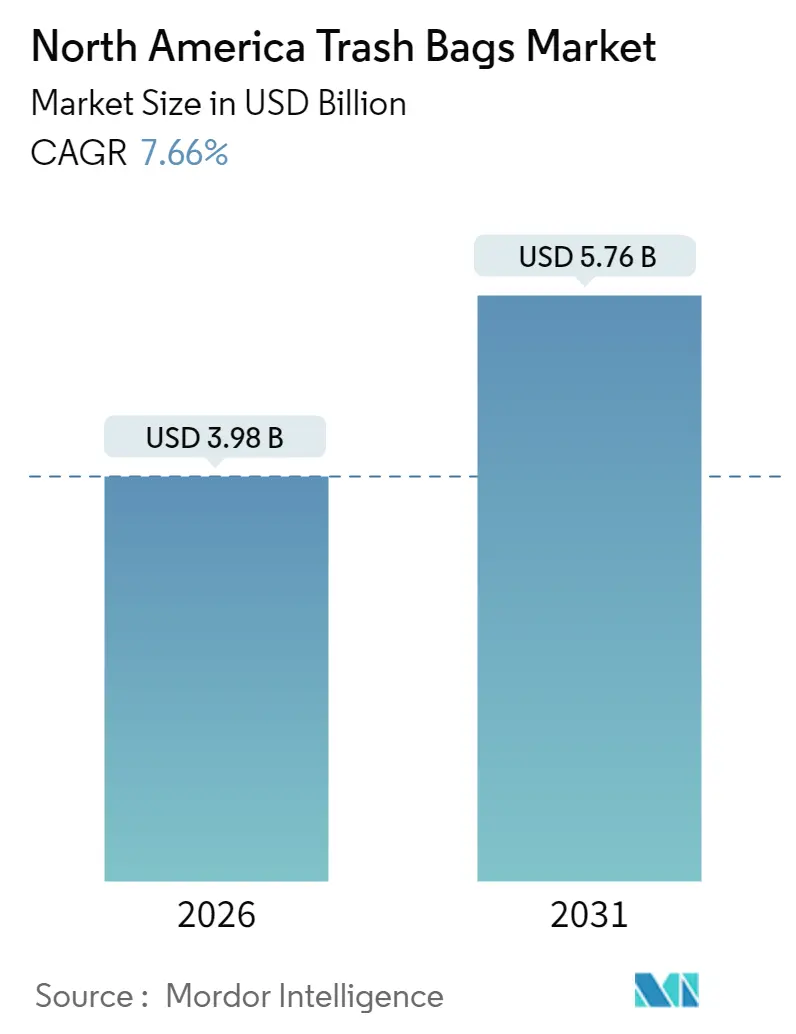

| Market Size (2026) | USD 3.98 Billion |

| Market Size (2031) | USD 5.76 Billion |

| Growth Rate (2026 - 2031) | 7.66% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Trash Bags Market Analysis by Mordor Intelligence

The North America trash bags market was valued at USD 3.70 billion in 2025 and estimated to grow from USD 3.98 billion in 2026 to reach USD 5.76 billion by 2031, at a CAGR of 7.66% during the forecast period (2026-2031). Sustained growth in the municipal waste stream, regulatory incentives for landfill diversion, and corporate zero-waste mandates continue to drive demand across residential, commercial, and industrial channels. State pay-as-you-throw (PAYT) schemes, most notably in New England, continue to lift per-capita bag purchase.[1]New Hampshire Municipal Association, “Cutting Trash in Half,” nhmunicipal.org Biodegradable and recycled-content products are gaining shelf space as seven U.S. states roll out extended producer responsibility (EPR) laws that incentivize the adoption of post-consumer resin. At the same time, polyethylene price volatility has forced producers to diversify their feedstocks and secure supply through new mechanical recycling ventures, including the Nova-Novolex plant in Indiana. Brand owners are courting consumers with scent-infused SKUs, while B2B buyers prioritize contractor-grade liners that withstand heavy, cardboard-rich e-commerce refuse.

Key Report Takeaways

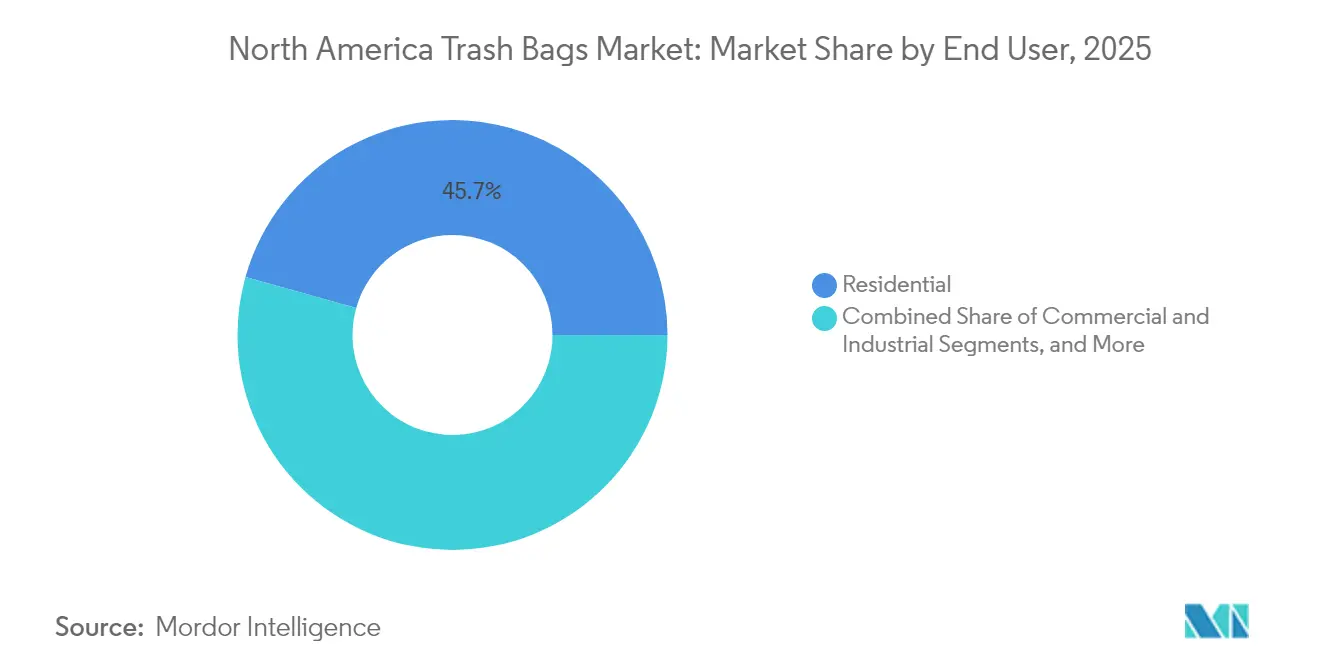

- By end user, the residential segment led with a 45.65% revenue share in 2025; the industrial segment is projected to expand at a 7.88% CAGR through 2031.

- By product type, LDPE bags captured 41.05% of the North America trash bags market share in 2025, whereas biodegradable products are projected to advance at a 7.74% CAGR to 2031.

- By capacity, 13-30 gallon liners commanded 37.55% share of the North America trash bags market size in 2025, while 30-55 gallon contractor bags are set to grow at an 8.05% CAGR through 2031.

- By material source, virgin plastics held a 51.30% share in 2025; however, bio-based resins are forecast to post a 7.95% CAGR through 2031.

- By sales channel, offline retail controlled 70.30% of 2025 revenue; online channels are expected to register a 7.85% CAGR up to 2031.

- By country, the United States accounted for 52.60% of the 2025 value and is anticipated to rise at a 7.90% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Trash Bags Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Residential waste-stream expansion and state landfill-diversion targets | +1.8% | United States and Canada | Medium term (2-4 years) |

| Corporate zero-waste pledges from Fortune 500 facilities | +1.2% | North America | Long term (≥ 4 years) |

| Rapid e-commerce packaging turnover elevating commercial trash volume | +1.5% | United States and Canada | Short term (≤ 2 years) |

| Municipal pay-as-you-throw programs accelerating bag consumption | +0.9% | U.S. New England states | Medium term (2-4 years) |

| High-clarity recycled-content resins enabling premium pricing | +0.7% | North America | Long term (≥ 4 years) |

| Adoption of anti-microbial liners in healthcare and foodservice | +0.6% | United States and Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Residential Waste-Stream Expansion and State Landfill-Diversion Targets

Mandatory diversion policies are reshaping waste collection norms, prompting municipalities to specify certified compostable or recycled-content liners in public procurement. California’s SB 1383 has already increased organic recycling tonnage by 14% in Sacramento, while landfill inputs fell by 10% during the same period. Canada’s draft methane rule aims for a 50% reduction in landfill emissions by 2030, a goal that encourages public facilities to adopt ASTM D6400-compliant organics bags [CANADA.CA]. Such rules keep municipal bid volumes growing, particularly for 13-30 gallon liners that fit curbside carts

Corporate Zero-Waste Pledges from Fortune 500 Facilities

Enterprise-wide diversion targets are converting multi-site buyers into large, long-term accounts. Cox Enterprises has diverted 750 million lb from landfill and credited waste programs with USD 340 million in financial value.[3]Cox Enterprises, “92% Waste Diversion,” coxenterprises.com Target now processes organics at 1,680 U.S. locations and has already reached 85% operational diversion. These programs demand consistent SKU specifications, clear-film sortation bags, and industrial compostable liners that can handle food scraps and corrugated offcuts simultaneously.

Rapid E-Commerce Packaging Turnover Elevating Commercial Trash Volume

E-commerce in the U.S. surpassed USD 11 trillion in sales in 2024, resulting in packaging that generates 4.8 times more waste than traditional retail channels. Fulfillment hubs accumulate dense loads of corrugated and poly-mailers, upping demand for 30-55 gallon contractor sacks with reinforced seams. Online returns exacerbate the load, adding 14% more landfill waste and creating high-volume collection points that require frequent liner change-outs.

Municipal Pay-As-You-Throw Programs Accelerating Bag Consumption

PAYT creates price signals that both reduce tonnage and encourage households to use municipality-branded liners. Concord, New Hampshire, reduced its annual trash from 14,722 tons to 8,311 tons, resulting in a savings of USD 2 million in disposal fees. Massachusetts now counts 143 PAYT towns,, 58% of which use bag-based models, fueling steady liner turnover at USD 1.50-4.00 per bag in retail. The guaranteed sales volumes entice converters to offer color-coded, city-logo options in 15- and 30-gallon sizes.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile polyethylene and bioplastic feedstock prices | -1.4% | North America | Short term (≤ 2 years) |

| Single-use-plastic bans and extended-producer-responsibility laws | -0.8% | United States and Canada | Medium term (2-4 years) |

| Supply-demand mismatch for certified composting infrastructure | -0.6% | United States | Long term (≥ 4 years) |

| Quality variability in post-consumer resin streams | -0.5% | North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Polyethylene and Bioplastic Feedstock Prices

Polyethylene spot values fell 11.95% year-on-year in 2025 after hurricane-linked outages on the Gulf Coast squeezed inventories before producers pushed a USD 0.05-0.07-per-lb contract hike. Buyers responded by trimming stock cover to 18 days, leaving converters exposed to price spikes. Similar volatility affects biopolymer markets, where fermenter output depends on corn and sugar feedstocks, which have their own price fluctuations. Margin uncertainty hinders capital investment in new extrusion lines and can delay the commercial launch of innovative SKUs.

Single-Use-Plastic Bans and Extended-Producer-Responsibility Laws

California’s SB 1053 eliminates all grocery plastic bags by 2026, removing a major downstream channel for LDPE film. Seven states now impose EPR levies, and British Columbia bans even compostable shopping bags while charging CAD 2.00 for reusables. Differing rules by state and province raise compliance costs, force bespoke formulations, and fragment economies of scale—particularly painful for mid-tier converters without multi-plant flexibility.

Segment Analysis

By End User: Industrial Momentum Outpaces Established Residential Demand

The residential channel still accounts for the largest slice of the North America trash bags market size, posting 45.65% share in 2025 as curbside collection and PAYT schemes keep kitchen liners moving through grocery aisles. Yet, industrial buyers, from automotive plants to data center campuses, are ramping up purchases at a 7.88% CAGR through 2031. Many are locked into zero-landfill targets that necessitate heavier-gauge liners rated for metal shavings, resin pellets, or bulky packaging. Supplier contracts often bundle color-coded segregation bags, anti-static drum liners, and 55-gallon builders’ sacks, boosting average selling price relative to household SKUs.

Industrial volume gains reflect healthy construction spending and the onshoring of manufacturing. Large projects generate concentrated waste nodes, creating predictable, pallet-level orders that shave logistics costs for converters. The North America trash bags market share for industrial applications is therefore expected to approach the residential share by decade-end as new plants come online and legacy facilities retrofit waste-sorting zones to meet ESG metrics.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Product Type: Biodegradable Lines Challenge LDPE Fortification

LDPE retained 41.05% revenue share in 2025 thanks to its balance of tear resistance and cost efficiency. However, legislative tailwinds are sending ASTM D6400-certified bags up the adoption curve, with the sub-category tracking a 7.74% CAGR. California’s SB 1046 requires compostable pre-checkout bags with a minimum 15-inch mouth width, effective starting in 2025. Echo effects include supermarket chains sourcing matching compostable trash liners for back-of-house organics totes. At the same time, mechanical-recycling investments are improving the clarity of recycled LDPE pellets, helping traditional film retain customer loyalty where certified composting facilities remain scarce.

Overall, the North America trash bags market is shifting toward a dual-portfolio model, featuring mainstream LDPE or HDPE for general refuse and premium-priced biodegradable options for organics, as well as brand-led sustainability messaging. This bifurcation provides converters with the flexibility to hedge against feedstock swings while meeting regional compliance requirements.

By Capacity: Contractor Bags Capture Growth from Infrastructure Spending

Kitchen liners in the 13-30 gallon band still generated 37.55% of the revenue in 2025, reflecting standard household bin sizes and weekly pickup rhythms. Contractors and institutional custodians, however, are embracing 30-55 gallon sacks, a segment that is expanding at an annual rate of 8.05%. Job-site debris, dense cardboard from fulfillment centers, and renovation waste all benefit from higher-volume, puncture-resistant film grades. Municipal PAYT quirks add intrigue: Lebanon, New Hampshire, prices 15- and 30-gallon PAYT bags identically at USD 4.00, nudging residents toward maximizing capacity.

As infrastructure legislation unlocks new civil works budgets, demand for heavy-gauge liners should stay elevated. The North America trash bags market size for contractor liners is therefore projected to surpass the USD 1 billion threshold before 2031, closing the gap with kitchen trash stalwarts.

By Material Source: Bio-Based Resins Gain Ground on Virgin Dominance

Virgin polymer feed still underpins 51.30% of 2025 shipments, yet volumes remain flat as corporate buyers seek to incorporate recycled content to meet their scope-3 carbon goals. Hefty Ultra Strong now blends 50% recovered resin comprising 30% plant scrap and 20% post-consumer flakes—without sacrificing tensile strength.Bio-based PE and PLA blends are advancing at the fastest rate, with an 7.95% CAGR, aided by state EPR rules, such as New Jersey’s mandate on recycled content levels.

The North America trash bags market share of hybrids that combine virgin and recycled streams is expanding, as quality-controlled PCR feedstock from the Nova-Novolex Connersville line becomes available at scale. In the long term, converters with in-house reclaim and certified compostable portfolios will enjoy a cost-of-goods edge as landfill fees and carbon taxes rise.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Sales Channel: E-Commerce Subscriptions Chip Away at Store Shelves

Offline retail controlled 70.30% of the 2025 value, thanks to high-traffic grocery aisles and hardware chains that cross-merchandise liners with cleaning goods. PAYT municipalities also rely on local store networks for distributing color-coded bags. But online channels are scaling at a 7.85% CAGR, buoyed by auto-ship subscriptions for jan-san suppliers and bulk case packs targeting micro-fulfillment nodes.

Interestingly, the surge in e-commerce generated packaging waste, thereby expanding addressable volumes for the same online channel. For manufacturers, direct-to-consumer logistics unlock richer margins and consumer insights but require investment in digital advertising and parcel-optimized master packs. As a result, the North America trash bags market is likely to see an omnichannel equilibrium, wherein e-commerce accounts for a double-digit share without displacing the convenience of brick-and-mortar replenishment.

Geography Analysis

The United States accounted for 52.60% of 2025 revenue and is forecast to achieve an 7.90% CAGR through 2031. State-level leadership on EPR, organic waste bans, and PAYT programs keeps the policy landscape dynamic. California’s plastic-bag sunset in 2026 and its compostable mandate effective 2025 instantly redirect procurement toward certified liners. Colorado’s Plastic Pollution Reduction Act and Oregon’s Producer Responsibility Program complement a multi-state framework that rewards adopters of recycled content.

Corporate influence is equally pronounced. Fortune 500 operators, such as Target and Cox Enterprises, link supplier scorecards to landfill diversion, thereby accelerating the regional uptake of post-consumer resin SKUs.. Municipalities from Sacramento to Boston deploy PAYT or organics separation, feeding liner volume into both big-box retail and jan-san distribution. Consequently, the North America trash bags market size in the United States is on track to exceed USD 3.06 billion by 2031. Canada, although smaller, leverages federal methane-reduction targets and provincial rules, such as British Columbia’s ban on compostable shopping bags [GOV.BC.CA]. Integrated North American supply chains funnel U.S. resin and film southward, yet currency fluctuations intermittently bolster the competitiveness of Canadian converters. Ongoing landfill levies and circular-economy roadmaps suggest the nation will continue to prioritize recycled-content and organics-friendly liners, supporting a healthy 6-6.8% growth clip through 2031.

Competitive Landscape

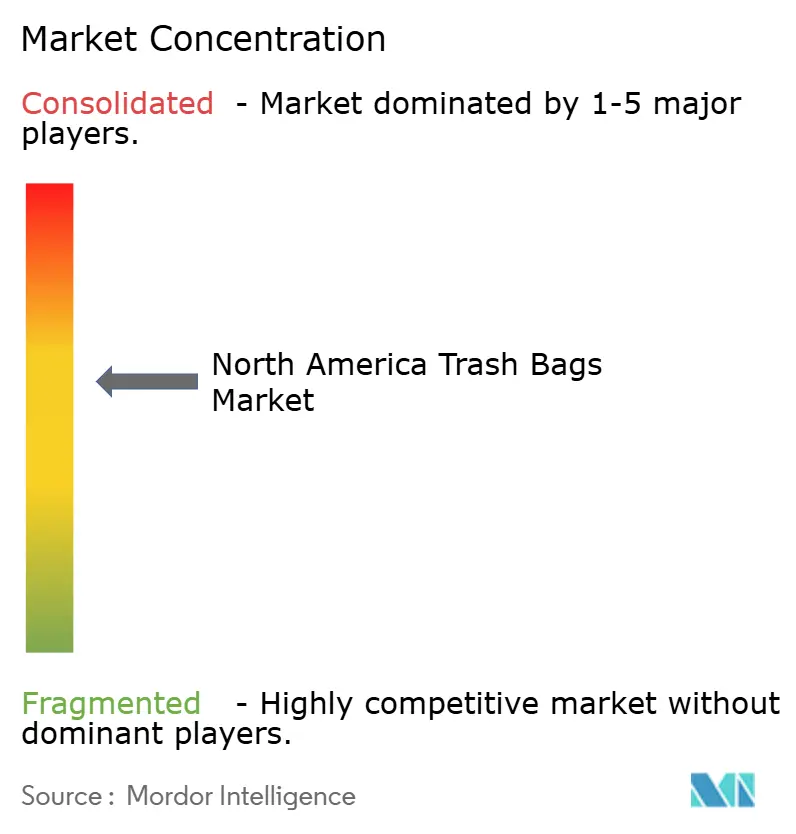

Market structure is moderately consolidated. Reynolds Consumer Products leads with the Hefty portfolio, posting USD 240 million in Q1 2025 segment revenue, buoyed by USD 152 million in annual sales of scent-infused SKUs. Glad, owned by The Clorox Company, leverages odor-shield technology and broad supermarket access to retain premium positioning. Mid-tier firms such as Novolex and Inteplast supply private-label programs for mass merchants, competing mainly on cost and logistics reach.

Strategic pivots center on recycled-resin integration. Novolex’s joint recycling venture with Nova Chemicals secures 50,000 metric tons of annual LDPE PCR supply, insulating both partners from the volatility of virgin materials. Brand owners are also utilizing fragrance licensing, drawstring patterns, and flex-fit gussets to differentiate themselves in a category often perceived as commoditized. Healthcare-grade antimicrobial liners and custom-printed PAYT bags represent profitable niches for smaller converters willing to navigate regulatory certification hurdles.

Private-label penetration remains elevated, yet branded players retain shelf advantage via national advertising and co-marketing with retailers. Forward integration into e-commerce storefronts enables direct customer feedback loops, accelerating scent or thickness tweaks ahead of bulk retail resets. Given that the top five suppliers control roughly 55-60% of the overall value, the North America trash bags market earns a concentration score of 6, indicating a balanced competitive milieu with room for challenger disruption.

North America Trash Bags Industry Leaders

-

Reynolds Consumer Products Inc. (Hefty)

-

Novolex Holdings LLC

-

Inteplast Group Corporation

-

Cosmoplast Industrial Company LLC

-

International Plastics Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Nova Chemicals and Novolex inaugurated a mechanical-recycling plant in Connersville, Indiana, adding 50,000 metric tons of LDPE PCR capacity.

- May 2025: Reynolds Consumer Products broadened its Hefty Ultra Strong line with Fabuloso Watermelon Scent across 13- and 30-gallon variants.

- April 2025: Reynolds reported Q1 2025 Hefty revenue of USD 240 million, up 3% year-on-year on volume gains for scented bags.

- January 2025: California enforced SB 1046, obliging grocers to offer only recycled-paper or certified compostable pre-checkout bags.

North America Trash Bags Market Report Scope

Trash bags are disposable garbage bags used to handle and dispose of trash. Trash bags are typically made of plastic material that comes in various sizes and options. The market includes revenue accrued from the sales of trash bags offered by various vendors operating in the market.

The North American Trash Bags Market is classified according to end-user industry (residential, commercial, and industrial) and country (the United States and Canada). The market sizes and forecasts are provided in terms of value (in USD billions) for all the above segments.

By End User

| Residential |

| Commercial |

| Industrial |

By Product Type

| Low-Density Polyethylene (LDPE) Bags |

| High-Density Polyethylene (HDPE) Bags |

| Biodegradable / Compostable Bags |

By Capacity (Gallons)

| < 8 Gal (Bathroom) |

| 8 - 30 Gal (Kitchen) |

| 30 - 55 Gal (Contractor) |

| > 55 Gal (Industrial Drum Liners) |

By Material Source

| Virgin Plastic |

| Post-Consumer Recycled Plastic |

| Hybrid (Recycled + Virgin) |

| Bio-based Resins |

By Sales Channel

| Offline Retail (Grocery, Mass Merchandiser) |

| Online Retail |

| Jan-San / Institutional Distribution |

By Country

| United States |

| Canada |

| By End User | Residential |

| Commercial | |

| Industrial | |

| By Product Type | Low-Density Polyethylene (LDPE) Bags |

| High-Density Polyethylene (HDPE) Bags | |

| Biodegradable / Compostable Bags | |

| By Capacity (Gallons) | < 8 Gal (Bathroom) |

| 8 - 30 Gal (Kitchen) | |

| 30 - 55 Gal (Contractor) | |

| > 55 Gal (Industrial Drum Liners) | |

| By Material Source | Virgin Plastic |

| Post-Consumer Recycled Plastic | |

| Hybrid (Recycled + Virgin) | |

| Bio-based Resins | |

| By Sales Channel | Offline Retail (Grocery, Mass Merchandiser) |

| Online Retail | |

| Jan-San / Institutional Distribution | |

| By Country | United States |

| Canada |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the North America trash bags market in 2026?

The North America trash bags market size is valued at USD 3.98 billion in 2026.

What is the projected CAGR for trash bag demand through 2031?

Aggregate demand is expected to rise at a 7.66% CAGR from 2026 to 2031.

Which capacity segment is growing fastest?

Contractor-grade 30-55 gallon liners are forecast to post an 8.05% CAGR because of construction and e-commerce waste volumes.

Why are biodegradable trash bags gaining traction?

State mandates such as California’s SB 1046 and corporate zero-waste procurement policies are boosting adoption of ASTM D6400-certified products.

How do pay-as-you-throw programs influence sales?

PAYT schemes require residents to purchase city-branded bags, generating predictable liner demand while cutting overall tonnage.