Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

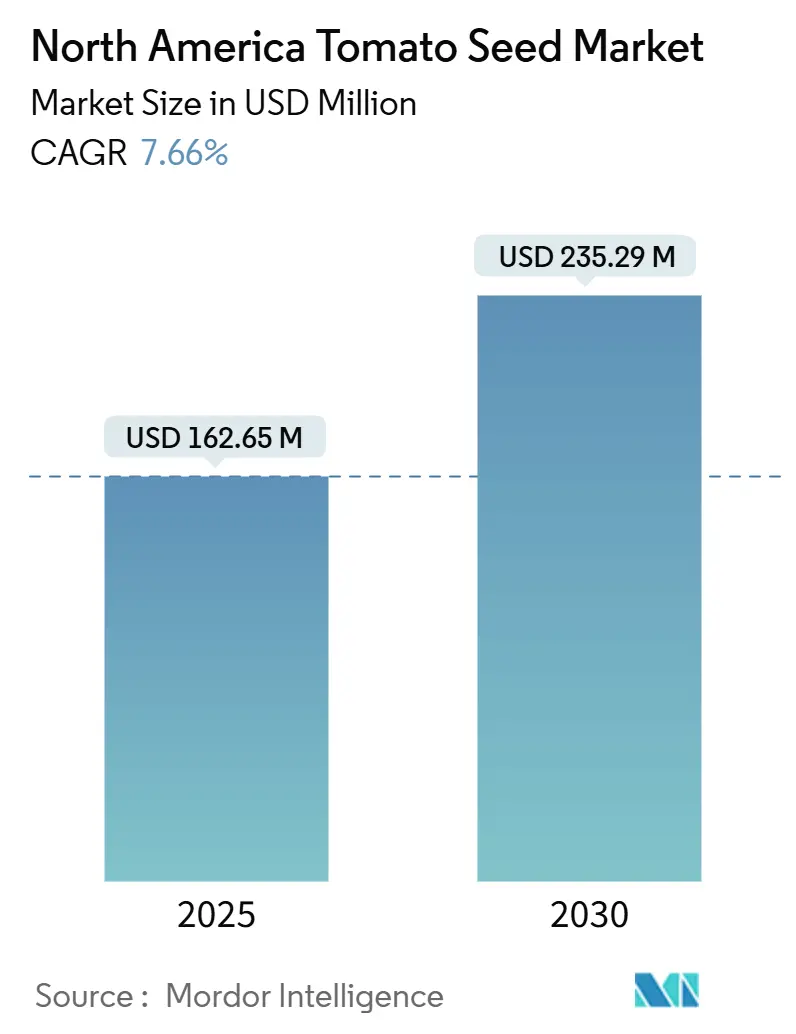

| Market Size (2025) | USD 162.65 Million |

| Market Size (2030) | USD 235.29 Million |

| Growth Rate (2025 - 2030) | 7.66% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Tomato Seed Market Analysis by Mordor Intelligence

The North America tomato seed market size stands at USD 162.65 million in 2025 and is forecast to reach USD 235.29 million by 2030, translating into a 7.66% CAGR over the period. Demand is propelled by rapid greenhouse expansion, a sharp pivot toward nutritionally fortified cultivars, and steady regulatory progress around gene-edited varieties that shorten breeding cycles. Seed producers are channeling R&D funds into ToBRFV-resistant hybrids and compact plants for vertical farms, while climate-smart subsidies in Canada and Mexico widen the customer base beyond high-tech U.S. growers. Competitive intensity revolves around biotechnology platforms, especially where companies can bundle disease resistance, flavor, and yield in a single hybrid. Parallel growth of urban indoor farms and e-commerce produce channels opens additional placement opportunities for premium seed lots.

Key Report Takeaways

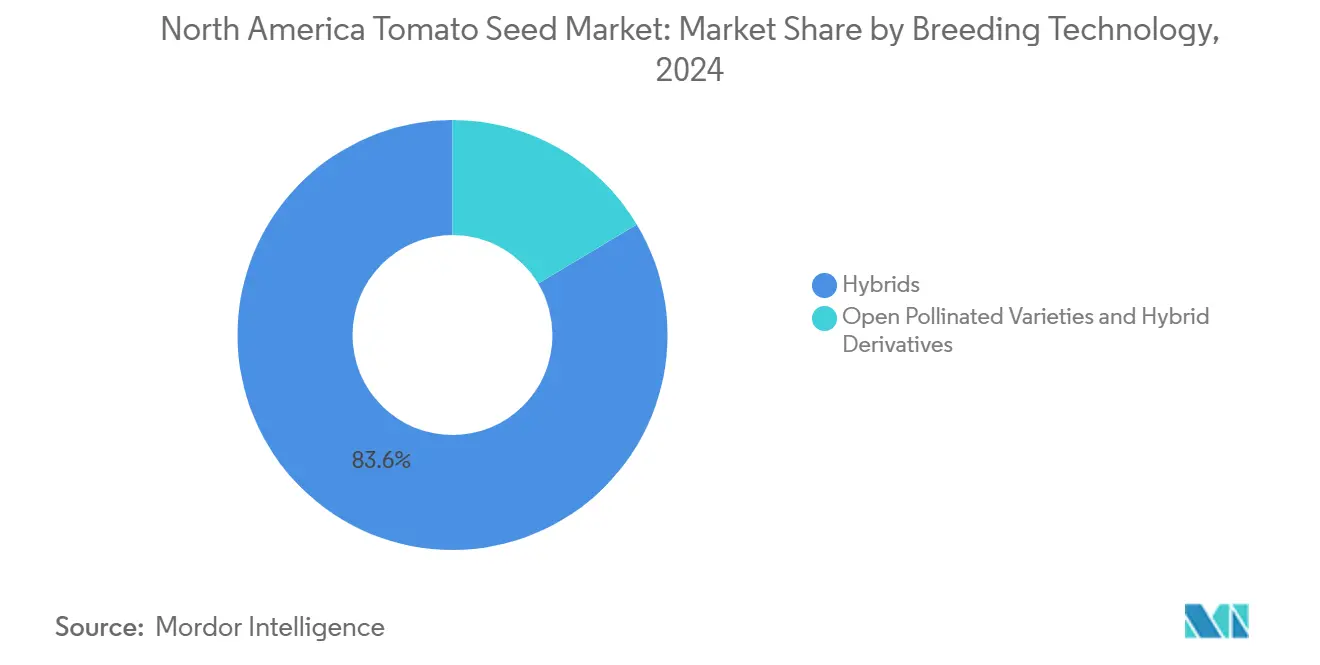

- By breeding technology, hybrid seeds held 83.6% of the North America tomato seed market share in 2024 while advancing at a 7.67% CAGR through 2030.

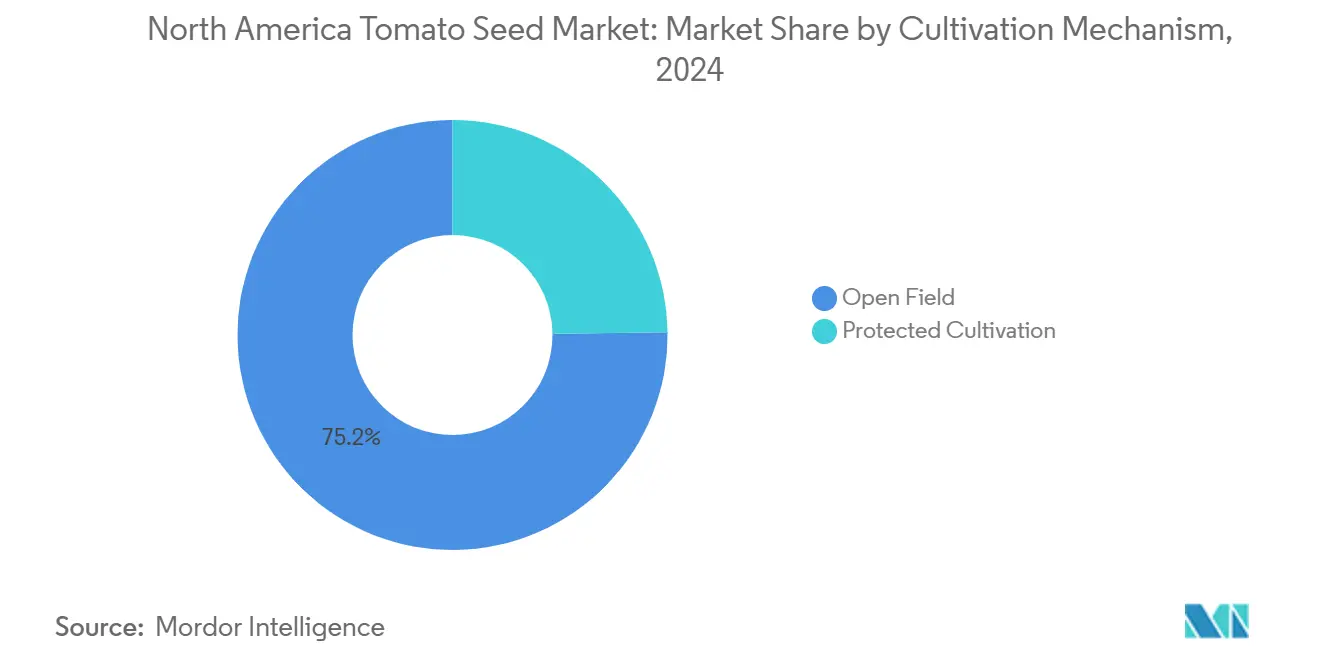

- By cultivation mechanism, open-field systems commanded 75.2% share of the North America tomato seed market size in 2024; protected cultivation is projected to expand at 9.63% CAGR between 2025 and 2030.

- By geography, the United States led with 57.7% revenue share in 2024 and is poised to grow fastest at 8.40% CAGR to 2030.

North America Tomato Seed Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid greenhouse acreage expansion | +1.8% | The United States and Canada, with emerging growth in Mexico | Medium term (2-4 years) |

| Rising demand for high-lycopene cultivars in fresh-cut processing | +1.2% | North America, concentrated in California and Ontario processing hubs | Long term (≥ 4 years) |

| Increased biotech trait approvals post-2025 | +1.5% | The United States is leading, with Canada following regulatory harmonization | Short term (≤ 2 years) |

| Labor-saving dwarf determinate hybrids for vertical farms | +0.9% | Urban centers across the United States and Canada | Medium term (2-4 years) |

| Corporate sustainability pledges favoring disease-resistant seeds | +1.1% | Global, with North American subsidiaries driving implementation | Long term (≥ 4 years) |

| Climate-smart subsidy programs in Canada and Mexico | +0.8% | Canada and Mexico, with spillover effects to border states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Greenhouse Acreage Expansion

Controlled environment agriculture operations have fundamentally reshaped North American tomato production economics, with greenhouse facilities generating yields 10-15 times higher per square foot than traditional open field cultivation. The sector's infrastructure investments exceed USD 2 billion annually, driven by climate volatility and water scarcity concerns that make protected cultivation increasingly attractive to commercial growers[1]Source: USDA Economic Research Service, “Controlled Environment Agriculture: Production, Markets, and Policy Considerations,” ers.usda.gov. Greenhouse operators typically source hybrid seeds engineered for hydroponics, high humidity tolerance, and uniform ripening, driving premium demand. Infrastructure investment continues, illustrated by NatureSweet’s new 44-acre Arizona site that opened in February 2024. LED lighting costs have dropped more than 50% since 2020, lowering operational breakevens and enabling expansion into northern latitudes.

Rising Demand for High-Lycopene Cultivars in Fresh-Cut Processing

Fresh-cut processing facilities increasingly specify high-lycopene tomato varieties to meet consumer demand for functional foods with enhanced antioxidant profiles, creating a premium market segment for specialized seed varieties. [2]Source: American Chemical Society, “Lycopene Enhancement in Tomato Varieties Through Genetic Modification,” acs.org. The fresh-cut processing sector's growth, particularly in ready-to-eat salads and food service applications, drives demand for tomatoes with extended shelf life and superior nutritional density. Processing facilities pay premium prices for high-lycopene varieties, creating compelling economics for growers willing to invest in specialized seed genetics. This trend aligns with broader consumer health consciousness and regulatory initiatives promoting functional food consumption, positioning high-lycopene varieties as a strategic growth driver for seed companies with advanced breeding capabilities.

Increased Biotech Trait Approvals Post-2025

Regulatory momentum for biotechnology-enhanced tomato varieties accelerated significantly following Norfolk Healthy Produce's successful FDA consultation for Purple Tomato in June 2023, establishing precedent for anthocyanin-enhanced varieties with demonstrated health benefits. USDA APHIS issued multiple RSR responses in October 2024 for modified tomato plants featuring altered fruit color and enhanced nutritional quality, signaling regulatory acceptance of gene-edited cultivars[3]Source: U.S. Food and Drug Administration, “FDA Completes Consultation on Norfolk Plant Sciences’ Genetically Engineered Tomato,” fda.gov. The regulatory framework's maturation reduces approval uncertainty, encouraging increased R&D investment from major seed companies and accelerating time-to-market for innovative cultivars addressing specific grower and consumer needs.

Labor-Saving Dwarf Determinate Hybrids for Vertical Farms

Vertical farming operations demand compact, determinate tomato varieties optimized for multi-tier growing systems and automated harvesting equipment, creating a specialized market niche for dwarf cultivars with concentrated fruit set. These operations require seeds engineered for specific plant architecture, with determinate growth habits, compact internodes, and synchronized fruit ripening to optimize automated harvesting systems. The labor cost advantages of vertical farming, particularly in high-wage urban markets, justify premium seed pricing and drive demand for specialized cultivars unavailable through traditional breeding programs.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory delays for CRISPR-edited tomato events | -0.7% | The United States leading regulatory framework, and Canada follows | Short term (≤ 2 years) |

| Seed price inflation outpacing grower margins | -1.1% | North America, particularly affecting small-scale open field producers | Medium term (2-4 years) |

| Greenhouse labor shortages in the United States | -0.8% | United States, concentrated in high-wage metropolitan areas | Long term (≥ 4 years) |

| Rising incidence of Tomato Brown Rugose Fruit Virus (ToBRFV) outbreaks | -0.9% | Global, with North American greenhouse operations at the highest risk | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Delays for CRISPR-Edited Tomato Events

Despite regulatory momentum, CRISPR-edited tomato varieties face extended approval timelines that delay market introduction and increase development costs for seed companies investing in gene editing technologies. The USDA APHIS regulatory framework requires extensive documentation for gene-edited crops, with review periods extending 12-18 months beyond initial submission dates. Regulatory harmonization between the United States, Canada, and Mexico remains incomplete, creating additional complexity for companies seeking region-wide market access for gene-edited varieties.

Seed Price Inflation Outpacing Grower Margins

Tomato seed prices increased 15-20% annually over the past two years, significantly outpacing grower revenue growth and pressuring adoption rates for premium varieties among cost-sensitive producers. West Mexico growers reported input cost pressures, including seed expenses, with some operations reducing planted acreage due to margin compression. Small and medium-scale growers increasingly delay variety upgrades or revert to lower-cost open-pollinated alternatives, constraining market expansion for hybrid seed technologies.

Segment Analysis

By Breeding Technology: Hybrids Sustain Performance Leadership

Hybrid seeds secured 83.6% of the North America tomato seed market share in 2024 and are forecast to compound at 7.67% annually through 2030, underscoring their central role in commercial production economics. Superior yield uniformity, combined resistance stacks, and longer shelf life justify price points that are 2-3 times higher than open-pollinated lines. Growers treating tomatoes as a high-value greenhouse crop view hybrids as insurance against disease-induced crop failure. Gene-edited traits now layer on top, promising nutritional upgrades and customized plant architecture without diluting established hybrid vigor.

Second-generation hybrids target niche needs, such as elongated shelf life for e-commerce fulfillment and anthocyanin-rich flesh for functional-food processors. Breeders also integrate CRISPR-enabled alleles that shorten vegetative cycles, boosting annual turnover in vertical farms. Open-pollinated varieties retain pockets of demand among organic producers who value seed-saving rights, yet their market position erodes each year as retailers enforce tighter cosmetic and uniformity standards.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Cultivation Mechanism: Protected Cultivation Rises Fastest

Open-field systems still accounted for 75.2% of the North America tomato seed market size in 2024, due to lower capital barriers and entrenched acreage across California’s Central Valley and Mexico’s Pacific Coast. Protected cultivation, a mix of greenhouses, screenhouses, and vertical farms, shows the strongest momentum, expanding at 9.63% CAGR to 2030. Yield multipliers of 10-15× per square foot, tighter water control, and pesticide reductions create compelling economics, especially as retail contracts shift toward year-round supply.

Seed suppliers differentiate greenhouse lines with traits such as high-density cluster sets, tolerance to diffuse light conditions, and compatibility with high-wire training. Vertical farm breeders go further, engineering dwarf determinate plants under 45 cm that align with robotic harvest windows. Meanwhile, open-field seed portfolios focus on heat tolerance, mechanical harvestability, and cost efficiency to defend volume share against the march of controlled-environment acreage.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The United States led with 57.7% revenue share in 2024 and is poised to grow fastest at 8.40% CAGR to 2030, reflecting the continent’s deepest greenhouse infrastructure and the most advanced regulatory path for biotech cultivars. Expansion continues inland as lower-cost industrial parks adopt LED-equipped glasshouses to supply metropolitan food hubs. Canadian operations concentrate in Ontario and British Columbia; provincial incentives covering up to 20% of greenhouse capex hasten adoption, giving protected systems an outsized influence over national seed orders. Mexico’s Sinaloa and Baja California corridors prioritize export-grade tomatoes, and FIRA loans that trim interest costs have already financed more than 1,000 ha of new glasshouses since 2023.

The United States also anchors R&D activity. Seed giants maintain coastal trial stations that vet resistance and flavor under exacting supermarket protocols, ensuring rapid turnover of elite lines. Canada supports this pipeline with its own variety registration fast-track, enabling simultaneous cross-border launches. Mexico’s climatic diversity serves as a natural screening ground for heat-tolerant lines; varieties proven here often become the default picks for United States desert greenhouses.

Labor availability shapes location decisions. United States growers in Ohio and Pennsylvania tout ample year-round workforce access compared with wage-inflated California. Canadian growers counter high electricity costs by deploying combined heat and power units, while Mexican facilities mitigate summer heat loads with evaporative pad-and-fan systems. Across the region, water scarcity intensifies; the shift toward closed hydroponics underlines the value of seed lines that tolerate slightly elevated EC levels.

Competitive Landscape

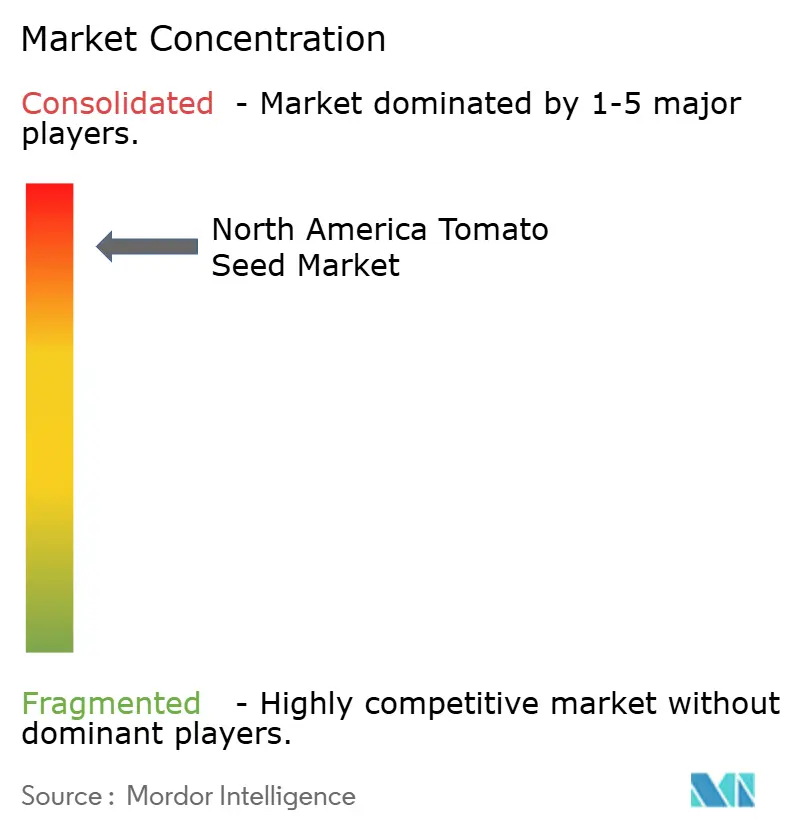

The North America tomato seed market is consolidated. Market leadership rests with a quartet of multinationals—Bayer AG, Syngenta Group, BASF SE, Groupe Limagrain, and Rijk Zwaan Zaadteelt en Zaadhandel B.V. Their integrated breeding networks, genomics platforms, and regulatory teams create significant entry barriers. Strategic focus lies in stacking ToBRFV resistance with flavor enhancements, as evidenced by Syngenta’s 2024 launch of four baby-plum hybrids that promise both virus defense and sugar-acid balance. BASF channels resources into Nunhems’ “Forte” line, pushing texture durability for e-commerce shipments.

Midsize challengers such as Enza Zaden and PanAmerican Seed exploit agility, rolling out niche offerings like pink beefsteaks tailored to farmers’ market aesthetics or striped cocktail types for premium snack packs. Start-ups, including Norfolk Plant Sciences, leverage CRISPR to fast-track traits; its FDA-cleared Purple Tomato validates an alternate innovation path that sidesteps decade-long conventional crosses.

Vertical farm operators emerge as atypical buyers wielding influence disproportionate to acreage. Oishii signs multiyear offtake agreements that grant breeders visibility on trait priorities like compact vines and uniform 20-gram fruit clusters. In response, incumbents set up in-house vertical-farm pilot rooms, collapsing feedback loops from seasons to weeks.

North America Tomato Seed Industry Leaders

-

BASF SE

-

Bayer AG

-

Groupe Limagrain

-

Rijk Zwaan Zaadteelt en Zaadhandel B.V.

-

Syngenta Group

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: Bayer introduced a new suite of ToBRFV-resistant hybrids aimed at mitigating resistance-breaking virus strains across high-wire greenhouse systems.

- March 2025: PanAmerican Seed unveiled WonderStar Pink Beefsteak Tomato for the 2026 spring catalog, touting extended post-harvest firmness for direct-to-consumer channels.

- November 2024: Oishii secured USD 150 million in Series B funding to multiply vertical-farm installations in New York, Los Angeles and Chicago.

North America Tomato Seed Market Report Scope

Hybrids, Open Pollinated Varieties & Hybrid Derivatives are covered as segments by Breeding Technology. Open Field, Protected Cultivation are covered as segments by Cultivation Mechanism. Canada, Mexico, United States are covered as segments by Country.

Breeding Technology

| Hybrids |

| Open Pollinated Varieties and Hybrid Derivatives |

Cultivation Mechanism

| Open Field |

| Protected Cultivation |

Geography

| Canada |

| Mexico |

| United States |

| Rest of North America |

| Breeding Technology | Hybrids |

| Open Pollinated Varieties and Hybrid Derivatives | |

| Cultivation Mechanism | Open Field |

| Protected Cultivation | |

| Geography | Canada |

| Mexico | |

| United States | |

| Rest of North America |

Need A Different Region or Segment?

Customize Now

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms

Get More Details On Research Methodology

Download PDF