North America Sugar-free Chewing Gum Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

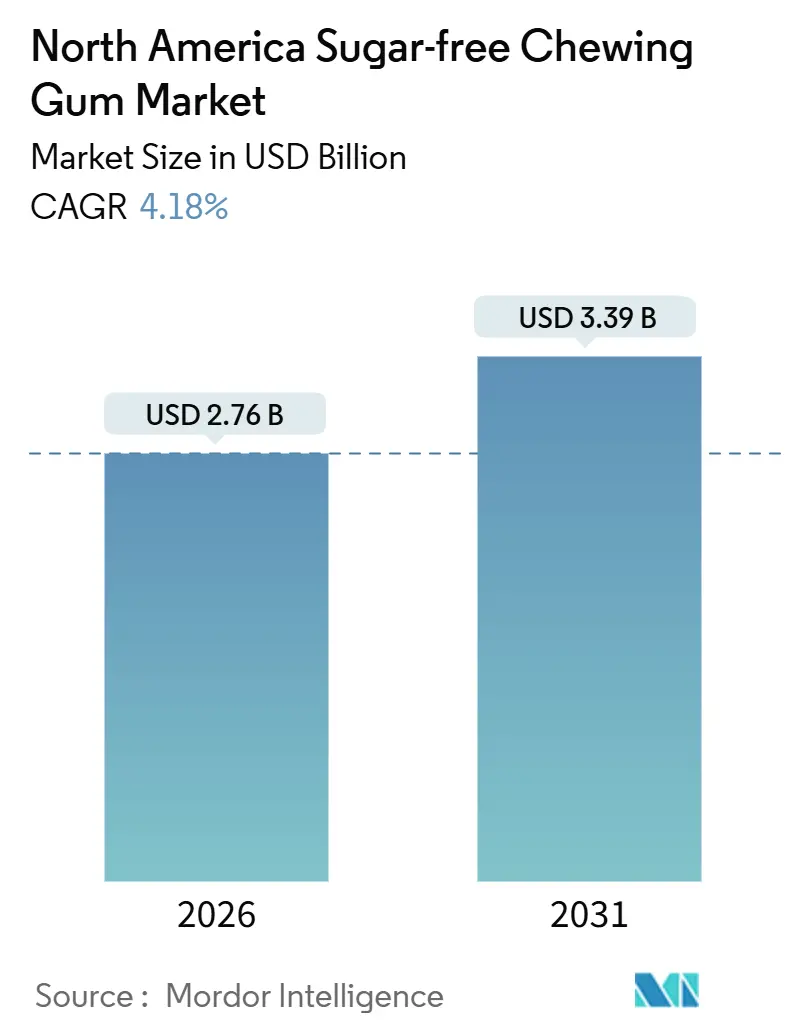

| Market Size (2026) | USD 2.76 Billion |

| Market Size (2031) | USD 3.39 Billion |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

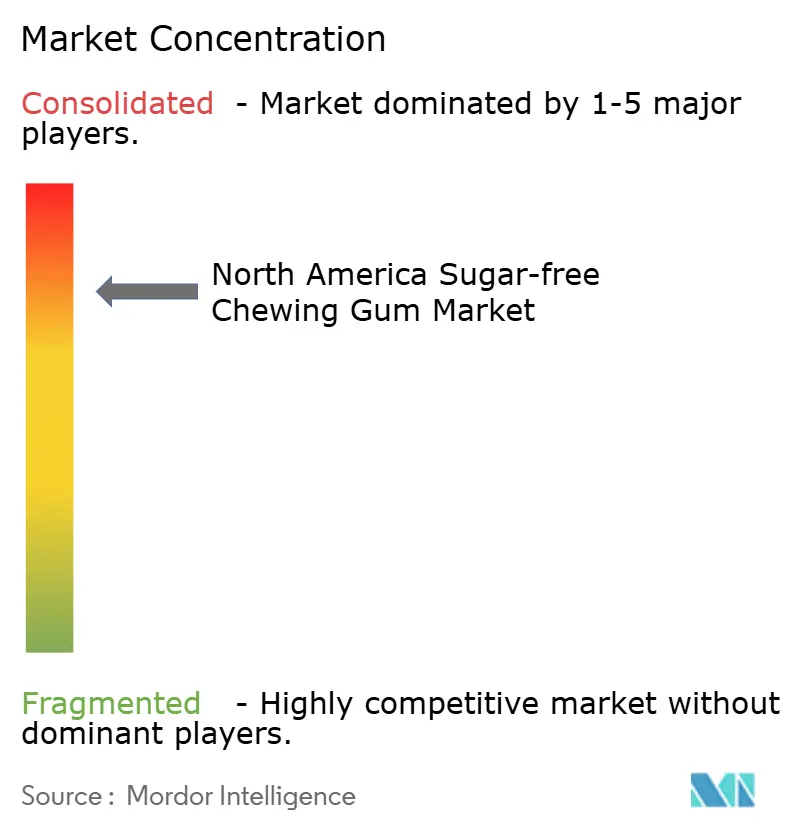

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Sugar-free Chewing Gum Market Analysis by Mordor Intelligence

The North America sugar-free chewing gum market is expected to reach USD 2.76 billion by 2026 and grow further to USD 3.39 billion by 2031, registering a CAGR of 4.18% during the forecast period. This growth highlights the shift of sugar-free gum from being a niche dental product to becoming a regular part of daily wellness routines. Factors such as clinical endorsements, connections to behavioral health, and convenient formats have made it popular in workplaces, during commutes, at schools, and in gyms. The American Dental Association's approval of xylitol gum strengthens its reputation for oral care, while the Centers for Disease Control and Prevention's guidance on nicotine gum positions it at the intersection of dental and behavioral health. Innovations like resealable pouches for cube gums, the adoption of clean-label sweeteners, and the rise of direct-to-consumer subscriptions are driving demand. To stay competitive, companies are focusing on flavor improvements and functional features to maintain shelf space against natural and wellness-focused competitors.

Key Report Takeaways

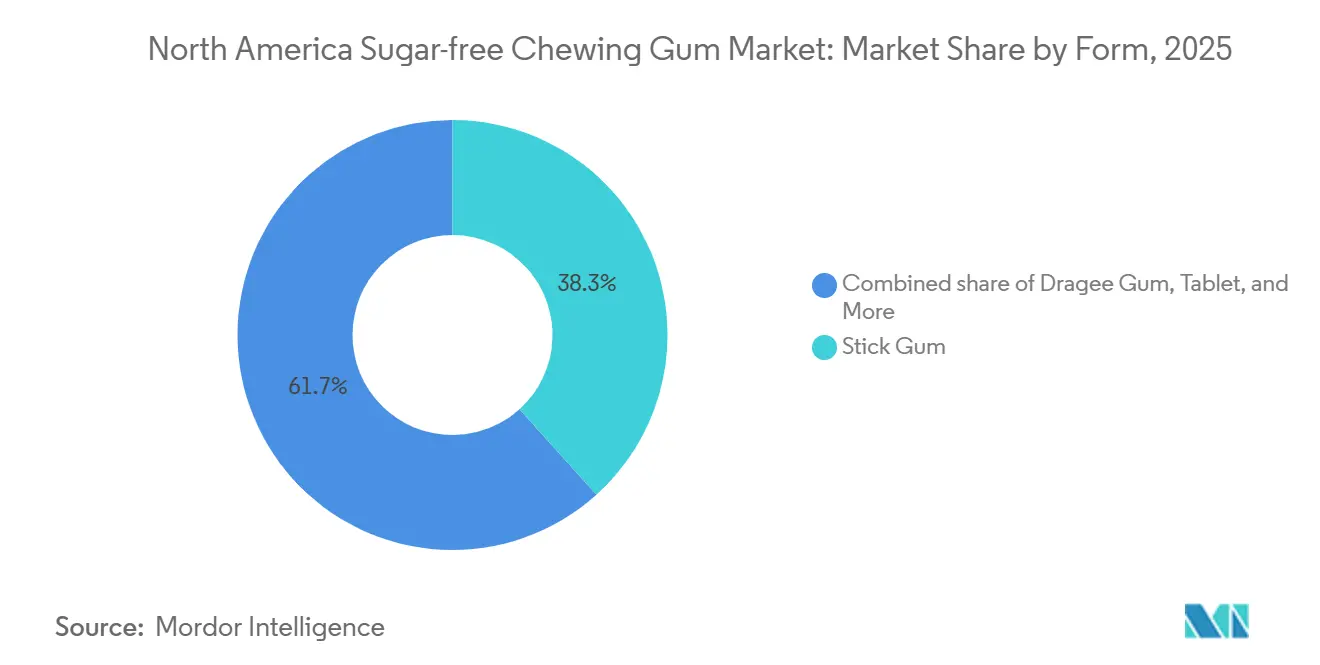

- By form, stick gum led with 38.32% of the North America sugar free chewing gum market share in 2025, while soft chew/cubes are expanding at a 5.22% CAGR through 2031.

- By sweetener type, artificial sweeteners accounted for 57.43% share of the North America sugar free chewing gum market size in 2025, whereas natural sweeteners are forecast to advance at a 6.55% CAGR to 2031.

- By distribution channel, supermarket/hypermarket commanded 46.76% revenue share in 2025; online retail store is recording the highest projected CAGR at 7.01% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Sugar-free Chewing Gum Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oral Health Positioning and Dental Endorsements | +0.9% | United States, Canada | Medium term (2-4 years) |

| Smoking-Cessation and Behavioral Health Adjacencies Normalizing Gum as Quasi-Health Product | +0.6% | United States, Canada | Long term (≥ 4 years) |

| Flavor and Format Innovation | +0.8% | North America | Short term (≤ 2 years) |

| On-The-Go Convenience and Discreet Consumption Supporting High-Frequency Usage | +0.7% | United States, Canada, Mexico | Medium term (2-4 years) |

| Personalization and Segmented Propositions | +0.5% | United States, Canada | Medium term (2-4 years) |

| Clean-Label and Natural Cues Driving Growth | +0.7% | United States, Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Oral Health Positioning and Dental Endorsements

Sugar-free gum has evolved from being a simple treat to an essential part of oral hygiene, thanks to growing support from professional dental associations. This shift has significantly influenced consumer buying behavior. The Canadian Dental Association endorses xylitol gum as a preventive dental care measure, highlighting its ability to prevent Streptococcus mutans from adhering to tooth enamel, thereby reducing the risk of cavities. A 2024 Cochrane systematic review confirmed that xylitol-containing gum can reduce dental caries in children by 13% compared to those who do not use it, providing strong, evidence-based support for marketing claims. Similarly, the European Food Safety Authority has approved xylitol's benefits for dental health, aligning regulatory standards across North America and Europe. This regulatory harmony enables global brands to promote consistent health claims in both regions. With this clinical validation, xylitol gum has transitioned from being a casual purchase in candy aisles to a prominent product in pharmacy wellness sections. This shift has not only expanded its market potential but also justified the premium pricing of xylitol-enriched gum formulations, making it a valuable addition to preventive oral care routines.

Smoking-Cessation and Behavioral Health Adjacencies Normalizing Gum as a Quasi-Health Product in Everyday Baskets

Nicotine replacement therapy has redefined chewing gum as an effective method for delivering medication, significantly boosting the popularity of the sugar-free gum market. The Centers for Disease Control and Prevention (CDC) identifies nicotine gum as a key tool for smoking cessation. Research shows that 4 mg nicotine gum, when combined with behavioral counseling, can double the chances of quitting smoking compared to a placebo. The U.S. Surgeon General's 2024 report emphasizes over-the-counter nicotine gum as a cost-effective and accessible solution, particularly for low-income populations who may lack access to prescription treatments. This shift has also changed the perception of gum chewing in professional environments. Previously seen as unprofessional, it is now viewed as a health-conscious habit. Capitalizing on this trend, brands like NeuroGum and REV GUM have introduced sugar-free gums infused with caffeine, L-theanine, and B-vitamins, promoting them as products that enhance focus and productivity in the workplace. Furthermore, the American Academy of Pediatric Dentistry's 2024 policy on xylitol gum for children supports its use as a preventive health product. This endorsement has expanded the role of gum beyond helping adult smokers, making it a valuable addition to family health and wellness routines[1]Source: American Academy of Pediatric Dentistry. "Policy on the Use of Xylitol", aapd.org.

Flavor and Format Innovation

Manufacturers are adopting encapsulation technologies and multi-sensory flavor systems to address declining per-capita consumption and attract younger consumers. In July 2024, Mars Wrigley launched EXCEL Refreshers, which use microencapsulated cooling agents to release flavor in stages. This innovation provides a 30-minute flavor experience, significantly longer than the 10-minute duration of traditional pellet gums. Similarly, Hershey introduced Ice Breakers Flavor Shifters in May 2025. These gums feature pH-sensitive coatings that change flavors from fruit to mint during chewing, catering to Gen-Z consumers who value unique experiences over brand loyalty. Soft chew and cube formats, which had a small market share in 2024, are expected to grow at a 5.22% CAGR through 2031. These formats are gaining popularity because they offer portion control and eliminate the inconvenience of disposing of stick gum in public. Wrigley's patent US4986991A on extended-release sucralose demonstrates the importance of intellectual property in sweetener delivery systems. This technology enhances sweetness perception by 40% without increasing the amount of sweetener, giving the company a competitive advantage[2]Source: Google Patents. "Extended Release Sweetener Composition, Patent US4986991A", patents.google.com.

On-The-Go Convenience and Discreet Consumption In Workplaces, Commute, School, and Fitness Environments Supporting High-Frequency Usage

With the rise of remote and hybrid work, gum consumption has increased as chewing during video calls is no longer seen as socially awkward. At the same time, fitness enthusiasts have adopted sugar-free gum as a zero-calorie way to suppress appetite. Many workplace wellness programs now include xylitol gum in dental-care kits for employees, promoting it as a tool to reduce mid-afternoon snacking and improve focus during long meetings. Commuters are shifting from traditional stick gum, which requires wrapper disposal, to blister-pack tablets and cubes that are more convenient and less likely to create litter. In schools, several U.S. states have lifted long-standing gum bans after dental associations provided evidence that xylitol gum helps reduce cavities in children who lack regular dental care. On social media, fitness influencers have popularized sugar-free gum as a pre-workout habit, claiming it enhances alertness and suppresses hunger during fasted cardio sessions, though scientific evidence supporting these claims is still limited. The portability of single-serve gum formats has also contributed to their popularity. As consumers make more frequent convenience-driven purchases at lower unit prices compared to bulk packs sold in traditional retail stores.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer Skepticism Toward Artificial Sweeteners | -0.8% | United States, Canada | Medium term (2-4 years) |

| Regulatory and Labeling Complexity | -0.5% | United States, Canada, Mexico | Long term (≥ 4 years) |

| Price Sensitivity and Premium Positioning of Sugar-Free/Formulated SKUs | -0.4% | Mexico, United States | Short term (≤ 2 years) |

| Supply Chain and Ingredient Risks for Specific Sweeteners, Flavors, and Gum Bases | -0.6% | North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer Skepticism Toward Artificial Sweeteners

In 2024, the World Health Organization classified aspartame as a Group 2B carcinogen, meaning it is "possibly carcinogenic to humans" based on limited evidence. This announcement has renewed consumer concerns about artificial sweeteners. Despite this, the Joint FAO/WHO Expert Committee on Food Additives confirmed that an acceptable daily intake of 40 mg/kg body weight remains safe. Social media amplified the WHO's statement, creating a gap between public perception and regulatory assurances. While agencies like the FDA and EFSA continue to affirm aspartame's safety at approved levels, surveys conducted in late 2024 showed a 22% decrease in consumer willingness to buy products containing aspartame as the main sweetener[3]Source: U.S. Food and Drug Administration. "High-Intensity Sweeteners", fda.gov. This shift has particularly impacted legacy brands that relied on aspartame for its affordability and clean taste. These companies are now reformulating their products with alternatives like stevia, monk fruit, or erythritol, which increase ingredient costs by 15-25%. On the other hand, smaller brands such as The PUR Company have taken advantage of this trend by promoting "aspartame-free" products as a key selling point, leveraging regulatory uncertainty to compete with larger players.

Regulatory and Labeling Complexity

In North America, regulatory frameworks for sweetener disclosures often overlap and sometimes conflict, creating challenges that typically favor larger manufacturers with dedicated regulatory teams. The FDA requires sugar alcohols, such as xylitol, erythritol, and sorbitol, to be listed individually in ingredient statements and included in total carbohydrate counts. However, these can be excluded from the "sugars" category if they meet specific metabolic criteria under 21 CFR 101.9. In Canada, Health Canada's Food and Drug Regulations have similar requirements but use the term "polyols" instead of "sugar alcohols." They also impose stricter rules on health claims related to dental benefits, requiring evidence from clinical trials conducted in Canada. In Mexico, the 2024 update to the NOM-051-SCFI/SSA1-2010 labeling standard mandates front-of-package warning labels for products exceeding 10% of the daily sugar intake. However, sugar alcohols are excluded from this calculation, giving sugar-free gums a competitive advantage in a market where sugared products face government stigmatization. Additionally, the FDA's 21 CFR 172.615 regulation allows chewing gum bases to include up to 60 components, such as synthetic elastomers and emulsifiers, without requiring individual disclosure. This lack of transparency has drawn criticism from clean-label advocates. Smaller brands like Simply Gum have responded by listing every gum-base ingredient, accepting higher costs to appeal to consumers who are skeptical of regulatory loopholes.

Segment Analysis

By Form: Portability Reshapes Format Preferences

In 2025, Stick Gum accounted for 38.32% of the North American sugar-free chewing gum market, supported by strong brand loyalty and high visibility at checkout counters. However, this dominance hides a significant weakness. The foil-and-paper wrappers used in this format create disposal challenges, especially in workplaces and public transit, where trash bins are limited, and littering is discouraged. Dragee and Tablet formats offer the convenience of blister packs but do not provide the long chew time preferred by regular users. As a result, these formats are mainly used for specific purposes, such as freshening breath after meals in restaurants. Other categories, including bubble gum and novelty shapes, face challenges as health-conscious consumers associate them with sugary treats and products aimed at children.

Soft Chew/Cubes are expected to grow at a 5.22% CAGR from 2026 to 2031, making them the fastest-growing segment. Their popularity is driven by their suitability for on-the-go lifestyles and their eco-friendly appeal. These formats eliminate the need for wrappers, fit easily into pockets and gym bags, and offer portion control that attracts calorie-conscious consumers. Leading brands like Hershey's Ice Breakers Cubes and Mars Wrigley's EXCEL Refreshers have introduced resealable pouches that keep the product fresh for multiple uses, addressing a key limitation of stick gum's single-use packaging. Changing retail trends also favor this format: while stick gum relies on impulse purchases at checkout counters, soft chews and cubes perform well in e-commerce, where product images can highlight their resealable packaging and portion control features.

Note: Segment shares of all individual segments available upon report purchase

By Sweetener Type: Clean-Label Mandates Accelerate Natural Gains

In 2025, artificial sweeteners accounted for 57.43% of the market, reflecting years of advancements in developing aspartame, sucralose, and acesulfame potassium. These synthetic sweeteners provide intense sweetness at a low cost, helping manufacturers achieve desired sweetness levels without affecting texture or shelf life. Their regulatory approval across North America also ensures a stable supply chain. However, this market dominance hides a growing lack of consumer trust. The WHO's 2024 classification of aspartame as a Group 2B carcinogen, despite reaffirming its safety limits, has increased skepticism, especially on social media, and has significantly influenced younger consumers. Brands using aspartame now face a tough decision: switching to natural sweeteners could raise costs by 15-25%, while continuing with aspartame risks losing health-conscious consumers who associate "artificial" with "unsafe."

Natural sweeteners are projected to grow at a strong 6.55% CAGR through 2031, making them the fastest-growing sweetener type. This growth is driven by their clean-label appeal and alignment with WHO recommendations to reduce free sugar intake. Popular options like stevia, monk fruit extract, and erythritol are gaining traction, but each has its challenges. Stevia has a licorice-like aftertaste that requires masking agents, monk fruit is expensive due to limited supply, and erythritol faces supply chain issues after the U.S. International Trade Commission imposed antidumping duties on Chinese imports in 2024. Companies like The PUR Company and Simply Gum have built their brands around "aspartame-free" claims, accepting higher ingredient costs to attract consumers willing to pay 20-30% more for natural products. Despite the European Food Safety Authority's 2024 confirmation of the safety of both artificial and natural sweeteners, consumer perceptions remain unchanged. This suggests that consumer opinions, rather than scientific evidence, will shape the market. Regulatory influence in this segment is minimal, as both the FDA and Health Canada approve the same sweeteners, leaving marketing strategies to drive differentiation.

By Distribution Channel: E-Commerce Disrupts Impulse Economics

In 2025, Supermarkets and Hypermarkets made up 46.76% of the distribution market. Their success is driven by strategic checkout-aisle placements and their suitability for weekly grocery shopping. These stores benefit from a well-established trade-marketing system, including slotting fees, promotional schedules, and optimized shelf layouts, which give larger, established players an advantage. Convenience Stores, on the other hand, focus on immediate purchases during commutes or road trips. However, their higher prices per unit and limited product variety restrict their growth. Other Distribution Channels, such as vending machines and specialty health stores, remain small players due to high servicing costs and scattered consumer traffic.

Between 2026 and 2031, Online Retail Stores are expected to grow at a strong 7.01% CAGR, making them the fastest-growing distribution channel. This growth is fueled by direct-to-consumer subscription models and functional gum brands that bypass traditional retail barriers. E-commerce platforms allow niche brands like NeuroGum and Mastiqe to reach a wide audience without needing to secure shelf space. Subscription services also provide consistent, recurring revenue, which physical stores cannot easily replicate. Amazon, a leader in North American e-commerce, offers an easy entry point for new brands. However, its 15% referral fees and advertising costs can reduce profit margins, especially for products priced under USD 5. The growth of online channels also reflects changing consumer habits. Shoppers looking for specific functional ingredients or sweetener options prefer online platforms, where detailed product descriptions and reviews offer more information than physical packaging.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

In 2024, the U.S. leads the North American sugar-free chewing gum market, driven by high per-capita consumption, a robust retail infrastructure, and endorsements from the American Dental Association. These endorsements have positioned xylitol gum as a preventive oral-health tool. Workplace wellness programs are increasingly including sugar-free gum in dental-care kits. Moreover, with the rise of remote work, the previous social stigma around chewing gum during video calls has diminished, leading to more frequent consumption. The FDA's regulation (21 CFR 172.615) on gum base allows up to 60 undisclosed components. This creates a niche for clean-label brands like Simply Gum, which emphasize full ingredient transparency. However, this approach comes with a 20-30% increase in production costs. Additionally, the U.S. International Trade Commission's 2024 antidumping duties on Chinese erythritol imports have tightened supplies for natural-sweetener formulations. As a result, brands are now sourcing from European or domestic producers, often at higher prices.

Canada's regulatory and cultural landscape moderates its growth in the sugar-free gum market compared to the U.S. Health Canada's stringent requirements for dental-health claims curtail the marketing flexibility that U.S. brands enjoy. While the Canadian Dental Association endorses xylitol gum, echoing American sentiments, provincial retail regulations introduce complexities. For instance, Quebec's ban on English-only packaging poses challenges for multinational brands. Furthermore, smoking-cessation programs, backed by provincial health ministries, distribute nicotine gum at subsidized rates, creating competition for commercial sugar-free products. Canada's colder climate extends gum shelf life but dampens impulse purchases during winter when outdoor activities wane. Still, Canada's high health literacy and premium pricing for natural sweeteners make it a prime testing ground for stevia and monk fruit formulations before they debut in the U.S.

Mexico stands out as North America's fastest-growing market for sugar-free gum. This growth is fueled by rising disposable incomes, urbanization, and a 2024 update to labeling standards (NOM-051-SCFI/SSA1-2010). These standards mandate front-of-package warnings for high-sugar products but exempt sugar alcohols. This regulatory gap gives sugar-free gums a competitive edge, as consumers keen on avoiding warning labels are drawn to xylitol and erythritol formulations. Distribution is primarily through convenience stores, which dominate sales thanks to small-format tiendas catering to local foot traffic. However, these stores lack refrigeration and climate control, posing challenges for natural-gum formulations that need cooler storage. Meanwhile, the rest of North America, including Central America and the Caribbean, remains a minor player in the market. This is due to a fragmented retail infrastructure and limited cold-chain logistics. Yet, diaspora communities in the U.S. and Canada create a niche demand for regional flavors like tamarind and hibiscus.

Competitive Landscape

The North America sugar-free chewing gum market is consolidated, with a small number of multinational players such as Chocoladefabriken Lindt & Sprüngli AG, Mars Incorporated, Mondelēz International Inc., Perfetti Van Melle BV, and The Hershey Company dominating category sales through strong brand recognition and widespread retail penetration. These companies leverage extensive marketing capabilities, well-established distribution networks, and continuous product innovation to maintain leadership in both traditional retail and convenience channels. Their scale advantages in sourcing, formulation, and promotional investment create high entry barriers for smaller competitors.

Product innovation is a key competitive tool, with leading brands focusing on functional extensions such as long-lasting flavor, oral-care positioning, and added benefits like tooth-whitening or breath-freshening technologies. Companies are also responding to growing health consciousness by using natural sweeteners such as xylitol and stevia, improving clean-label formulations, and introducing plant-based or biodegradable gum bases. These innovations help major players retain consumer interest while differentiating themselves in an otherwise mature category.

Consolidation is further reinforced by strong retail partnerships with supermarkets, hypermarkets, convenience stores, and fuel stations, where shelf visibility and impulse placements are critical. Digital channels and subscription models are also emerging, but brick-and-mortar dominance continues to favor incumbent brands with established relationships. As consumer preferences shift toward sugar-free and functional gums, the market structure is expected to remain concentrated, with leading players expanding through premium variants, sustainability initiatives, and targeted marketing to maintain their competitive edge.

North America Sugar-free Chewing Gum Industry Leaders

-

Chocoladefabriken Lindt & Sprüngli AG

-

Mars Incorporated

-

Mondelēz International Inc.

-

Perfetti Van Melle BV

-

The Hershey Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Wrigley Extra, one of the leading chewing gum brands, partnered with dental professionals around the world to promote the use of sugar-free chewing gum to improve oral health. The brand’s Wrigley Oral Health Program states that: “Gum base puts the 'chew' in chewing gum, binding all the ingredients together for a smooth, soft texture.

- October 2024: Mars Wrigley has expanded its portfolio with the launch of its new EXTRA plant-based chewing gum. According to the brand, the new EXTRA plant-based sugar-free chewing gum meets the growing demand for quality products with ingredients of plant or natural origin.

- April 2024: Refresh Gum expanded its portfolio of plant-based, sugar-free chewing gum with three new flavors. According to the brand, the new products are available in flavors like Garden Mint and Raspberry, Peppermint, Bubble Gum and Peach.

North America Sugar-free Chewing Gum Market Report Scope

Convenience Store, Online Retail Store, Supermarket/Hypermarket, Others are covered as segments by Distribution Channel. Canada, Mexico, United States are covered as segments by Country.| Stick Gum |

| Dragee Gum |

| Tablet |

| Soft Chew / Cubes |

| Others |

| Natural Sweeteners |

| Artificial Sweeteners |

| Supermarket/Hypermarket |

| Online Retail Store |

| Convenience Store |

| Other Distribution Channels |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| Form | Stick Gum |

| Dragee Gum | |

| Tablet | |

| Soft Chew / Cubes | |

| Others | |

| Sweetener type | Natural Sweeteners |

| Artificial Sweeteners | |

| Distribution Channel | Supermarket/Hypermarket |

| Online Retail Store | |

| Convenience Store | |

| Other Distribution Channels | |

| Country | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Market Definition

- Milk and White Chocolate - Milk chocolates is a solid chocolate made with milk (in the form of either milk powder, liquid milk, or condensed milk) and cocoa solids. White chocolate is made from cocoa butter and milk and contains no cocoa solids whatsoever. The scope includes regular chocolates, low-sugar, and sugar-free variants

- Toffees & Nougats - Toffees include hard, chewy, and small or one-bite candies marketed with labels as toffee or toffee-like confectionery. Nougat is a chewy confection with almond, sugar, and egg white as a basic ingredient; and it originated in Europe and Middle East countries.

- Cereals Bars - A snack composed of breakfast cereal that has been compressed into a bar shape and is held together with a form of edible adhesive. The scope includes snack bars made with cereals such as rice, oats, corn, etc. mixed with a binding syrup. These also include products labeled as cereal bars, cereal treat bars, or grain bars.

- Chewing Gum - This is a preparation for chewing, usually made of flavored and sweetened chicle or such substitutes as polyvinyl acetate. The types of chewing gums included in the scope are sugar-chewing gums and sugar-free chewing gums

| Keyword | Definition |

|---|---|

| Dark Chocolate | Dark chocolate is a form of chocolate containing cocoa solids and cocoa butter without the milk. |

| White Chocolate | White chocolate is the type of chocolate containing the highest percentage of milk solids, typically around or over 30 percent. |

| Milk Chocolate | Milk chocolate is made from dark chocolate that has a low cocoa solid content and higher sugar content, plus a milk product. |

| Hard Candy | A candy made of sugar and corn syrup boiled without crystallizing. |

| Toffees | A hard, chewy, often brown sweet that is made from sugar boiled with butter. |

| Nougats | A chewy or brittle candy containing almonds or other nuts and sometimes fruit. |

| Cereal bar | A cereal bar is a bar-shaped food product, made by pressing cereals and usually dried fruit or berries, which are in most cases held together by glucose syrup. |

| Protein bar | Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats. |

| Fruit & Nut bar | These are often based on dates with other dried fruit and nut additions and, in some cases, flavorings. |

| NCA | The National Confectioners Association is an American trade organization that promotes chocolate, candy, gum and mints, and the companies that make these treats. |

| CGMP | Current good manufacturing practices are those conforming to the guidelines recommended by relevant agencies. |

| Unstandardized foods | Unstandardized foods are those that do not have a standard of identity or that deviate from a prescribed standard in any manner. |

| GI | The glycemic index (GI) is a way of ranking carbohydrate-containing foods based on how slowly or quickly they are digested and increase blood glucose levels over a period of time |

| Skimmed milk powder | Skimmed milk powder is obtained by removing water from pasteurized skim milk by spray-drying. |

| Flavanols | Flavanols are a group of compounds found in cocoa, tea, apples, and many other plant-based foods and beverages. |

| WPC | Whey protein concentrate- the substance obtained by the removal of sufficient nonprotein constituents from pasteurized whey so that the finished dry product contains greater than 25% protein. |

| LDL | Low density Lipoprotein- the bad cholesterol |

| HDL | High density Lipoprotein- the good cholesterol |

| BHT | butylated Hydroxytoluene is a lab-made chemical that is added to foods as a preservative. |

| Carrageenan | Carrageenan is an additive used to thicken, emulsify, and preserve foods and drinks. |

| Free form | Not containing certain ingredients, such as gluten, dairy, or sugar. |

| Cocoa butter | It is a fatty substance obtained from cocoa beans, used in the manufacture of confectionery. |

| Pastellies | A type of of Brazilian candy made from sugar, eggs, and milk. |

| Draggees | Small, round candies that are coated with a hard sugar shell |

| CHOPRABISCO | Royal Belgian Association of the chocolate, pralines, biscuit, and confectionery industry- A trade association that represents the Belgian chocolate industry. |

| European Directive 2000/13 | A European Union directive that regulates the labeling of food products |

| Kakao-Verordnung | The German chocolate ordinance, a set of regulations that define what can be labeled as "chocolate" in Germany. |

| FASFC | Federal Agency for the Safety of the Food Chain |

| Pectin | A natural substance that is derived from fruits and vegetables. It is used in confectionery to create a gel-like texture. |

| Invert sugars | A type of sugar that is made up of glucose and fructose. |

| Emulsifier | A substance that helps to mix to liquids that does not mix together. |

| Anthocyanins | A type of flavonoid that is responsible for the red, purple, and blue colors of confectionery. |

| Functional Foods | Foods that have been modified to provide additional health benefits beyond basic nutrition. |

| Kosher certificate | This certification verifies that the ingredients, production process including all machinery, and/or food-service process complies with the standards of Jewish dietary law |

| Chicory root extract | A natural extract from the chicory root that is a good source of fiber, calcium, phosphorous, and folate |

| RDD | Recommended daily dose |

| Gummies | A chewy gelatin-based candy that is often flavored with fruit. |

| Nutraceuticals | Food or dietary supplements that are claimed to have health benefits. |

| Energy bars | Snack bars that are high in carbohydrates and calories are designed to provide energy on the go. |

| BFSO | Belgian Food Safety Organization for the food chain. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms