North America Space Propulsion Market Size and Share

Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 146.6 Billion |

| Market Size (2030) | USD 207.8 Billion |

| Growth Rate (2025 - 2030) | 7.22% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Space Propulsion Market Analysis by Mordor Intelligence

The North America Space Propulsion Market size is estimated at 146.6 billion USD in 2025, and is expected to reach 207.8 billion USD by 2030, growing at a CAGR of 7.22% during the forecast period (2025-2030).

The North American space propulsion industry is experiencing an unprecedented transformation driven by increased private sector participation and technological innovation. NASA's substantial budget allocation of USD 26 billion in 2023, representing a 5.6% increase from the previous year, demonstrates the strong government commitment to space exploration and development. This investment has catalyzed the development of advanced spacecraft propulsion technologies, particularly in electric propulsion and plasma propulsion systems. The emergence of commercial space companies has fostered a competitive environment, leading to cost reductions and improved efficiency in launch services. Private companies are increasingly collaborating with government agencies to develop innovative propulsion solutions, exemplified by NASA's distribution of USD 333 million in research grants in February 2023.

The industry has witnessed significant advancements in propulsion technology, particularly in electric propulsion systems and sustainable solutions. Electric propulsion systems, including ion propulsion and Hall-effect thrusters, have gained prominence due to their superior efficiency and longer operational lifetimes. These systems are increasingly being adopted for both commercial and government space missions, ranging from satellite operations to deep space exploration. In December 2023, NASA awarded Blue Origin a Launch Services II contract for planetary, Earth observation, and scientific satellite launches, highlighting the growing emphasis on versatile propulsion solutions. The industry is also seeing a shift towards eco-friendly propulsion technologies, with companies like Thales Alenia Space securing contracts for developing innovative propulsion systems.

The satellite industry continues to drive market growth, with increasing demand for advanced satellite propulsion systems for both large and small satellites. During the 2017-2022 period, North America witnessed the successful launch of over 4,300 satellites, demonstrating robust growth in satellite deployment. This trend is set to continue, as evidenced by SpaceX receiving FCC approval in December 2022 to launch 7,500 satellites as part of their Starlink constellation. The growing adoption of small satellites and CubeSats has spurred innovation in miniaturized propulsion systems, leading to the development of more efficient and cost-effective solutions for orbital maneuvers and station-keeping.

The market is characterized by strategic collaborations and technological partnerships between established players and emerging companies. Major space agencies are actively investing in start-ups to develop advanced propulsion systems for small satellites, fostering innovation in the industry. In February 2023, Thales Alenia Space secured a contract with the Korea Aerospace Research Institute (KARI) to provide integrated electric propulsion systems, demonstrating the international reach of North American space propulsion capabilities. These partnerships are driving the development of next-generation propulsion technologies, including water-powered systems and advanced electric propulsion solutions, positioning North America as a global leader in space propulsion innovation.

North America Space Propulsion Market Trends and Insights

Investment opportunities in the North American space propulsion market

- Investments in space programs are driving technological innovations and fostering the thriving satellite propulsion market. R&D initiatives associated with space programs lead to the creation of new propulsion systems, which offer increased efficiency and longer operational lifetime. These propulsion systems play a crucial role in spacecraft maneuvering, orbit maintenance, and mission longevity. The region's government and the private sector have dedicated funds for research and innovation in the space sector in terms of grants. In North America, government expenditure for space programs hit a record of approximately USD 24.8 billion in 2022. For instance, in February 2023, NASA distributed USD 333 million as research grants. Additionally, in 2022, the US government spent nearly USD 62 billion on its space programs, making it the world's highest spender in the space sector. Apart from the United States, the Canadian Space Agency budget is modest, and the estimated budgetary spending for 2022-23 is USD 329 million. In terms of funds allocated for NASA under the president's budget request summary for FY 2022-2027, NASA is expected to receive USD 45 million for the development of space power and nuclear propulsion.

- NASA is expected to receive USD 98 million to develop solar electric propulsion (SEP). In March 2021, NASA, Maxar Technologies, and Busek Co. completed a test of the 6-kilowatt (kW) solar electric propulsion subsystem successfully destined for the PPE. The Solar Electric Propulsion project was anticipated to receive the first qualification thruster from Aerojet Rocketdyne at the beginning of the first quarter of FY 2023. The government allocated funding of USD 110 million for developing nuclear thermal propulsion systems.

Segment Analysis: Propulsion Tech

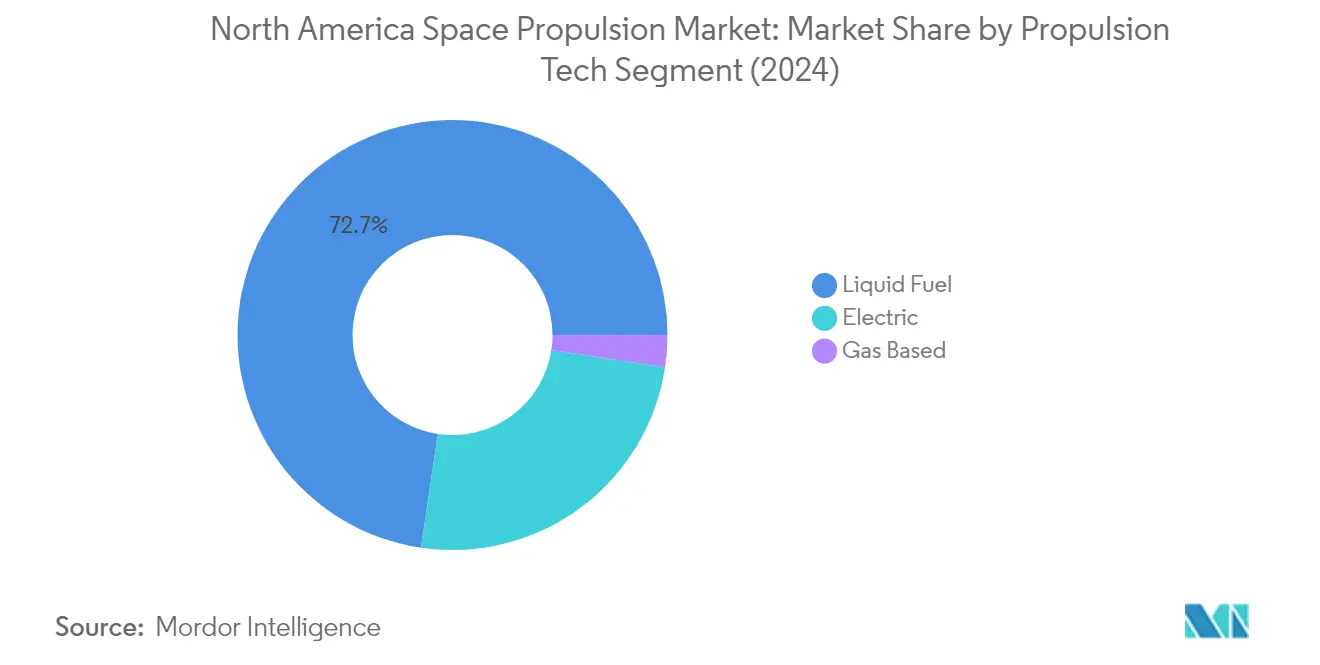

Liquid Fuel Segment in North America Space Propulsion Market

The liquid rocket engine segment dominates the North America space propulsion market, commanding approximately 73% market share in 2024. This significant market position is primarily driven by the segment's superior efficiency, controllability, and reliability characteristics that make it an ideal choice for various space missions. Liquid propulsion systems offer higher specific impulses compared to other propulsion technologies, resulting in greater efficiency and longer operational life for satellites. The ability to precisely control thrust levels and throttle engines allows for optimized maneuvers and efficient fuel usage, enabling extended mission durations and orbital adjustments. Major space agencies and private companies continue to invest heavily in liquid rocket engine technology, particularly for applications in various orbit classes, including geostationary orbit, low Earth orbit, polar orbit, and sun-synchronous orbit.

Gas-Based Segment in North America Space Propulsion Market

The gas-based propulsion segment is projected to experience the fastest growth in the North America space propulsion market, with an estimated CAGR of approximately 12% during 2024-2029. This growth is primarily driven by the increasing adoption of small satellites, particularly CubeSats, where cold gas thrusters eliminate the need for complex heat management systems. The segment's expansion is further supported by the technology's proven efficiency and reliability in enabling movements for various space applications. Gas-based propulsion systems are particularly favored when strong thrust or rapid maneuvering is required, making them the preferred choice for many space missions where their total impulse capacity meets mission requirements. The technology's compatibility with volume and weight limitations of nanosatellites and CubeSats continues to drive innovation and adoption in the market.

Electric Segment in North America Space Propulsion Market

The electric propulsion segment represents a significant portion of the market, offering unique advantages in terms of achieving thrust at high exhaust velocities while reducing propellant requirements compared to conventional methods. This technology has gained considerable traction in both commercial and government space missions, particularly for satellite operations and deep space exploration. The segment's growth is supported by ongoing developments in energy handling technology and high-performance Hall thruster systems, especially for smaller spacecraft. The adoption of electric propulsion has been further accelerated by the emergence of green emission initiatives and the increasing focus on eco-friendly propulsion technologies in the region.

North America Space Propulsion Market Geography Segment Analysis

Space Propulsion Market in the United States

The United States dominates the North American space propulsion market, commanding approximately 100% of the total market share in 2024. The country's leadership position is driven by significant investments in space transportation missions conducted by NASA and increasing satellite launches by the U.S. Department of Defense. The demand for spacecraft propulsion systems is particularly fueled by the launch of mass satellite constellations into space, with companies like SpaceX leading innovative developments in the field. The increasing demand for small satellites, including CubeSats and nanosatellites, has catalyzed the development of miniaturized propulsor appliances that are compact, lightweight, and cost-effective while maintaining sufficient thrust capabilities for orbital maneuvers and station-keeping. The country's robust space infrastructure and strong presence of major market players have created a conducive environment for technological advancements in propulsion systems. NASA's continued investment in startups to develop advanced propulsion systems for small satellites further strengthens the market's growth trajectory. The integration of advanced technologies and the focus on developing sustainable propulsion solutions have positioned the United States as a global leader in space propulsion innovation.

Space Propulsion Market in Canada

Canada's space propulsion market is experiencing steady growth, with a projected CAGR of approximately 5% from 2024 to 2029. The country has demonstrated a strong commitment to advancing its satellite capabilities through strategic investments and partnerships with private space companies. The Canadian government's focus on expanding vehicle network equipment and enabling connectivity to deployed vehicles and headquarters has created new opportunities in the satellite propulsion sector. The country's space industry benefits from collaborative initiatives between the Canadian Space Agency (CSA) and private enterprises, fostering innovation in propulsion technologies. Canada's emphasis on developing high-powered electric propulsion systems through research grants and funding programs has attracted international partnerships and technological collaborations. The government's ambitious plan for nationwide high-speed internet coverage by 2030 has created additional momentum for satellite launches and operations. The integration of advanced propulsion technologies in Canadian satellites has positioned the country as an emerging player in the global space propulsion market. The focus on developing eco-friendly propulsion solutions aligns with Canada's commitment to sustainable space exploration.

Competitive Landscape

Top Companies in North America Space Propulsion Market

The North American space propulsion market is characterized by significant technological advancement and innovation among key players like Moog Inc., Ariane Group, Busek Co., SpaceX, and Blue Origin. Companies are heavily investing in research and development to create more efficient and sustainable spacecraft propulsion systems, with a particular focus on electric propulsion technologies and reusable launch vehicles. Strategic partnerships and collaborations with space agencies and other industry players have become increasingly common to share expertise and resources. Market leaders are expanding their manufacturing capabilities and facilities to meet growing demand, particularly in the United States. Product innovation is centered around developing advanced propulsion solutions for both large spacecraft and small satellites, with emphasis on improving specific impulse, thrust control, and operational lifetime. Companies are also pursuing vertical integration strategies to maintain better control over their supply chains and reduce operational costs.

Consolidated Market with Strong Technical Barriers

The North American space propulsion market exhibits a highly consolidated structure dominated by established aerospace conglomerates and specialized propulsion system manufacturers. The market's high entry barriers stem from substantial capital requirements, complex technological expertise, and stringent regulatory compliance needs. Major players leverage their extensive experience, established relationships with space agencies, and comprehensive research capabilities to maintain their market positions. The industry is characterized by long-term contracts and strategic partnerships, particularly with government space agencies and defense departments, creating stable revenue streams for incumbent players.

The market shows limited merger and acquisition activity, with companies focusing more on organic growth and strategic partnerships rather than consolidation. This trend is driven by the specialized nature of orbital propulsion technologies and the importance of maintaining technological independence. Local players, particularly in the United States, benefit from government support and preference for domestic suppliers in strategic space programs. The presence of both traditional aerospace giants and innovative new space companies creates a dynamic competitive environment where technical expertise and innovation capabilities are key differentiators.

Innovation and Adaptability Drive Future Success

Success in the North American space transportation market increasingly depends on companies' ability to develop cost-effective and efficient propulsion solutions while maintaining high reliability standards. Market players must invest in next-generation technologies like electric propulsion systems and sustainable fuel alternatives to meet evolving customer requirements. Building strong relationships with key customers, particularly government space agencies and commercial satellite operators, remains crucial for long-term success. Companies need to maintain flexible manufacturing capabilities to address both large-scale missions and the growing small satellite market.

Future market leaders will need to demonstrate expertise in multiple propulsion technologies while maintaining cost competitiveness. The ability to quickly adapt to changing market demands and regulatory requirements, particularly regarding environmental sustainability and space debris mitigation, will be crucial. Companies must also focus on developing comprehensive service offerings, including post-launch support and maintenance capabilities. Success will depend on maintaining strong research and development capabilities while building efficient supply chain networks to ensure reliable component sourcing. The increasing commercialization of space activities presents opportunities for companies that can balance innovation with operational efficiency.

North America Space Propulsion Industry Leaders

Ariane Group

Busek Co. Inc.

Moog Inc.

Northrop Grumman Corporation

Safran SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2023: NASA awarded Blue Origin a NASA Launch Services II Indefinite Delivery Indefinite Quantity (IDIQ) contract to launch planetary, Earth observation, exploration, and scientific satellites for the agency aboard New Glenn, Blue Origin’s orbital reusable launch vehicle.

- February 2023: NASA’s Launch Services Program (LSP) awarded Blue Origin the Escape and Plasma Acceleration and Dynamics Explorers (ESCAPADE) contract. Under the contract Blue Origin will provide its New Glenn reusable technology for the mission.

- February 2023: Thales Alenia Space has contracted with the Korea Aerospace Research Institute (KARI) to provide the integrated electric propulsion on their GEO-KOMPSAT-3 (GK3) satellite.

North America Space Propulsion Market Report Scope

Electric, Gas based, Liquid Fuel are covered as segments by Propulsion Tech. Canada, United States are covered as segments by Country.| Electric |

| Gas based |

| Liquid Fuel |

| Canada |

| United States |

| Propulsion Tech | Electric |

| Gas based | |

| Liquid Fuel | |

| Country | Canada |

| United States |

Market Definition

- Application - Various applications or purposes of the satellites are classified into communication, earth observation, space observation, navigation, and others. The purposes listed are those self-reported by the satellite’s operator.

- End User - The primary users or end users of the satellite is described as civil (academic, amateur), commercial, government (meteorological, scientific, etc.), military. Satellites can be multi-use, for both commercial and military applications.

- Launch Vehicle MTOW - The launch vehicle MTOW (maximum take-off weight) means the maximum weight of the launch vehicle during take-off, including the weight of payload, equipment and fuel.

- Orbit Class - The satellite orbits are divided into three broad classes namely GEO, LEO, and MEO. Satellites in elliptical orbits have apogees and perigees that differ significantly from each other and categorized satellite orbits with eccentricity 0.14 and higher as elliptical.

- Propulsion tech - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Mass - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Subsystem - All the components and subsystems which includes propellants, buses, solar panels, other hardware of satellites are included under this segment.

| Keyword | Definition |

|---|---|

| Attitude Control | The orientation of the satellite relative to the Earth and the sun. |

| INTELSAT | The International Telecommunications Satellite Organization operates a network of satellites for international transmission. |

| Geostationary Earth Orbit (GEO) | Geostationary satellites in Earth orbit 35,786 km (22,282 mi) above the equator in the same direction and at the same speed as the earth rotates on its axis, making them appear fixed in the sky. |

| Low Earth Orbit (LEO) | Low Earth Orbit satellites orbit from 160-2000km above the earth, take approximately 1.5 hours for a full orbit and only cover a portion of the earth’s surface. |

| Medium Earth Orbit (MEO) | MEO satellites are located above LEO and below GEO satellites and typically travel in an elliptical orbit over the North and South Pole or in an equatorial orbit. |

| Very Small Aperture Terminal (VSAT) | Very Small Aperture Terminal is an antenna that is typically less than 3 meters in diameter |

| CubeSat | CubeSat is a class of miniature satellites based on a form factor consisting of 10 cm cubes. CubeSats weigh no more than 2 kg per unit and typically use commercially available components for their construction and electronics. |

| Small Satellite Launch Vehicles (SSLVs) | Small Satellite Launch Vehicle (SSLV) is a three-stage Launch Vehicle configured with three Solid Propulsion Stages and a liquid propulsion-based Velocity Trimming Module (VTM) as a terminal stage |

| Space Mining | Asteroid mining is the hypothesis of extracting material from asteroids and other asteroids, including near-Earth objects. |

| Nano Satellites | Nanosatellites are loosely defined as any satellite weighing less than 10 kilograms. |

| Automatic Identification System (AIS) | Automatic identification system (AIS) is an automatic tracking system used to identify and locate ships by exchanging electronic data with other nearby ships, AIS base stations, and satellites. Satellite AIS (S-AIS) is the term used to describe when a satellite is used to detect AIS signatures. |

| Reusable launch vehicles (RLVs) | Reusable launch vehicle (RLV) means a launch vehicle that is designed to return to Earth substantially intact and therefore may be launched more than one time or that contains vehicle stages that may be recovered by a launch operator for future use in the operation of a substantially similar launch vehicle. |

| Apogee | The point in an elliptical satellite orbit which is farthest from the surface of the earth. Geosynchronous satellites which maintain circular orbits around the earth are first launched into highly elliptical orbits with apogees of 22,237 miles. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.