Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

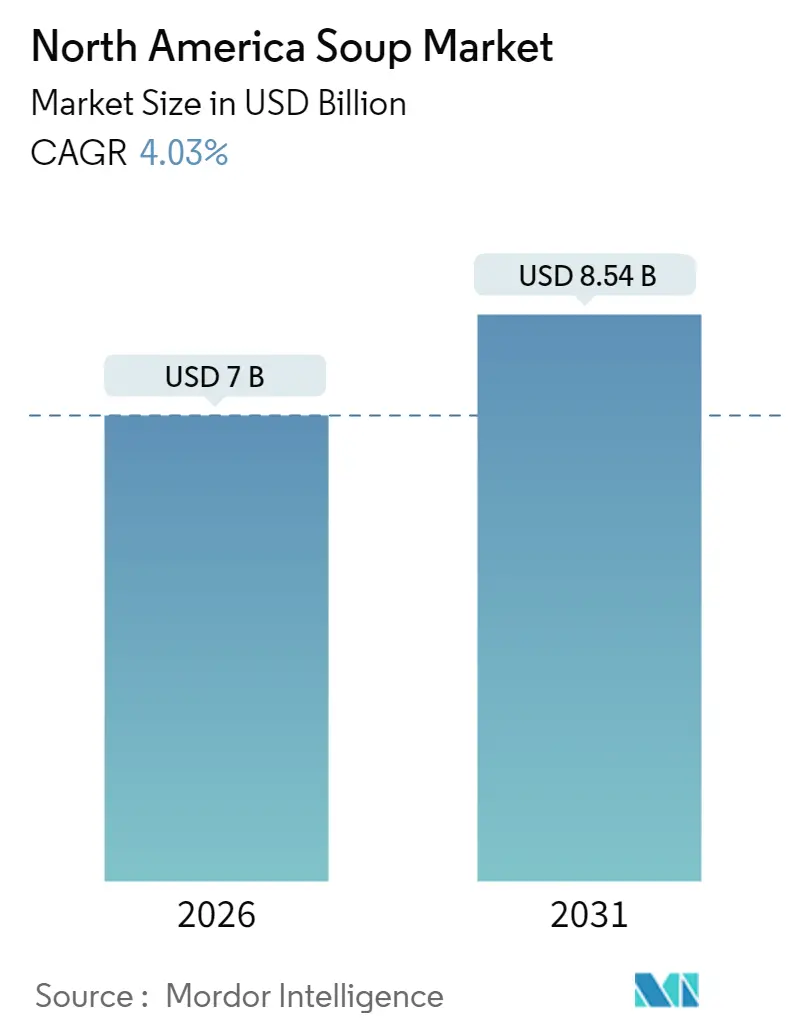

| Market Size (2026) | USD 7 Billion |

| Market Size (2031) | USD 8.54 Billion |

| Growth Rate (2026 - 2031) | 4.03% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Soup Market Analysis by Mordor Intelligence

The North American soup market is expected to grow from USD 6.73 billion in 2025 to USD 7 billion in 2026 and is forecast to reach USD 8.54 billion by 2031 at 4.03% CAGR over 2026-2031. This market expansion is attributed to the evolving consumer preferences toward convenient, nutritious, and diverse soup offerings. Market growth is primarily driven by the increasing demand for ready-to-eat soups, organic and plant-based products, and advanced packaging solutions. The chilled and frozen soup segments exhibit substantial growth rates as consumers increasingly gravitate toward premium and fresh alternatives. Furthermore, the market demonstrates robust demand for organic and clean-label soups, driven by heightened health consciousness, while product innovations in flavors and formulations address diverse consumer preferences and international culinary trends. The proliferation of e-commerce platforms and the modernization of retail channels facilitate enhanced product accessibility throughout urban and suburban regions.

Key Report Takeaways

- By product type, shelf-stable soup led with 46.12% revenue share in 2025, while chilled soup is set to expand at a 4.26% CAGR to 2031.

- By category, non-vegetarian soup accounted for 64.54% of the North American soup market share in 2025; vegetarian soup is forecast to post the fastest growth at a 4.71% CAGR through 2031.

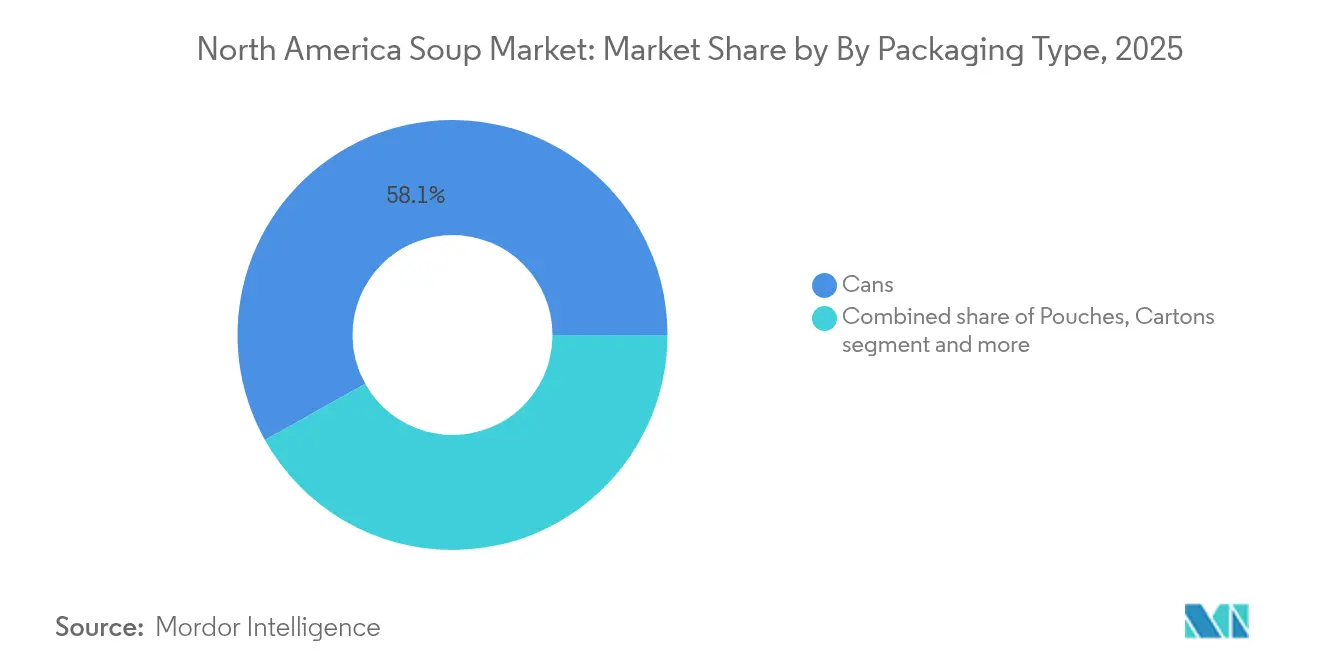

- By packaging, cans controlled 58.12% share of the North American soup market size in 2025, whereas pouches are expected to grow at a 4.95% CAGR during 2026-2031.

- By distribution channel, off-trade outlets captured 71.02% value share in 2025; on-trade sales are projected to register the highest pace with a 6.05% CAGR during 2026-2031.

- By geography, the United States dominated with 69.42% of 2025 revenue, yet Canada represents the fastest-growing market at a 5.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Soup Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenience and ready-to-eat options | +0.8% | North America, strongest in the United States urban markets | Short term (≤ 2 years) |

| Shift toward clean and functional ingredients | +0.6% | North America, premium segments | Medium term (2-4 years) |

| Aging population seeking nutrient-dense, easy-to-open formats | +0.4% | United States and Canada, rural concentration | Long term (≥ 4 years) |

| Product innovation and flavor variety | +0.5% | North America, with an Asian flavor focus in Canada | Medium term (2-4 years) |

| Sustainability and ethical sourcing | +0.3% | North America, coastal markets | Long term (≥ 4 years) |

| Seasonality and cold-weather consumption | +0.2% | Northern regions, Canada emphasis | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Convenience and ready-to-eat Options

Convenience and ready-to-eat options are key drivers of the North America Soup Market, influencing consumer purchasing patterns. The fast-paced lifestyles of North American consumers have increased demand for quick, time-saving meal solutions, particularly ready-to-eat and instant soups. According to the International Food Information Council (IFIC), in 2024, 57% of American consumers considered convenience as a critical factor in their food and beverage purchase decisions [1]Source: International Food Information Council (IFIC), "2024 IFIC Food and Health Survey", ific.org. This consumer preference has prompted manufacturers to develop products requiring minimal preparation time while maintaining nutritional value and taste. The convenience trend extends beyond time-saving to include storage efficiency, portability, and extended shelf life. Shelf-stable and instant soups offer long-lasting options that consumers can store in their pantries, providing reliable meals during busy schedules or emergencies. These features have established soups as a preferred quick meal, snack, or comfort food among various consumer groups, including busy professionals, students, and families.

Shift toward clean and functional ingredients

The North American Soup Market is experiencing significant growth driven by consumer demand for clean and functional ingredients. Consumers increasingly prefer soups without artificial additives, preservatives, and genetically modified organisms (GMOs), while seeking organic, plant-based, gluten-free, and dairy-free options. This shift reflects the broader health and wellness trend, where consumers choose nutrient-dense foods that provide additional health benefits. In response, manufacturers are simplifying their ingredient lists and incorporating superfoods, fiber, antioxidants, and plant proteins to support digestive health, immunity, and overall wellness. For example, in January 2025, Natural Grocers introduced six new varieties of savory soups that are certified organic, non-GMO, and made with plant-based, gluten- and dairy-free ingredients. This launch demonstrates how companies are meeting market demands by developing products that combine nutritional benefits with taste, appealing to vegans, vegetarians, and flexitarians seeking convenient, healthy meal options.

Aging population seeking nutrient-dense, easy-to-open formats

The aging population is a significant driver in the North American soup Market, as older consumers seek nutritious, easy-to-consume food options that meet their health requirements. Soups serve this demographic effectively by providing digestible meals rich in essential nutrients, vitamins, and minerals, often featuring low sodium content and natural ingredients that accommodate dietary needs. Convenient packaging formats, including microwavable cups, pouches, and resealable containers, make soup consumption easier for elderly consumers with physical limitations. According to Canada Statistics, approximately 7.6 million Canadians were aged 65 and older as of 2024, representing a substantial demographic that influences soup market demand. This population segment increasingly values soups as a practical meal option, particularly focusing on products that support digestive health, immunity, and overall well-being, while appreciating simple preparation methods.

Product innovation and flavor variety

Product innovation and flavor diversification drive growth in the market. Manufacturers expand their product lines to meet evolving consumer preferences by introducing new flavors, ethnic recipes, functional ingredients, and health-focused formulations. This innovation addresses consumer demands for variety, taste, and wellness benefits, helping companies attract and retain customers. The expansion of flavor options encourages consumer trial and repeat purchases as they explore new taste experiences beyond traditional soups, including spicy, savory, plant-based, and international varieties. In May 2023, Zoup! demonstrated this trend by introducing new flavors at the Fancy Food Show, including Chicken Potpie, Portabella Mushroom Bisque, Black Bean Chili, and Chicken Noodle Soup. Innovation enables companies to differentiate their products in the market. By offering both traditional and innovative options, companies appeal to a wide consumer base, from those preferring familiar flavors to those seeking new taste experiences, supporting sustained market growth.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High sodium and preservative concerns | -0.7% | North America, strongest in health-conscious segments | Medium term (2-4 years) |

| Competition from fresh and home-cooked meals | -0.5% | North America, suburban concentration | Short term (≤ 2 years) |

| Raw material price fluctuations and supply chain issues | -0.4% | North America, strongest in manufacturing-intensive regions | Short term (≤ 2 years) |

| Perception of processed and canned foods | -0.3% | North America, health-conscious demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High sodium and preservative concerns

Sodium content and preservative concerns constrain the North American soup market due to increasing health awareness and regulatory requirements. The Food and Drug Administration (FDA) mandates that low-sodium products contain no more than 140 mg of sodium per reference amount consumed, requiring manufacturers to adapt their formulations. In Mexico, the NOM-051 front-of-package warning label regulation, updated in 2023, requires prominent warnings on high-sodium products, potentially impacting consumer purchasing decisions. These regulatory requirements necessitate significant investment in reformulation research to reduce sodium while maintaining flavor profiles. The reformulation process presents technical challenges, particularly for shelf-stable soups that rely on sodium for preservation and taste. Manufacturers must explore alternative preservation methods, such as high-pressure processing or natural preservatives, which can increase production costs and complexity.

Competition from fresh and home-cooked meals

The preference for fresh and home-cooked meals poses a significant challenge to the North American soup market. Consumers increasingly choose homemade options, which they perceive as fresher and healthier alternatives. Home cooking allows individuals to control ingredients based on their dietary requirements, taste preferences, and nutritional needs. Despite manufacturers' efforts to develop clean-label and organic products, many consumers view packaged soups as processed alternatives. The increasing emphasis on whole, minimally processed foods has created additional pressure on soup manufacturers. Home-cooked meals are often associated with superior quality and authentic taste, diminishing the convenience advantage of canned, dried, or frozen soups. The market also faces competition from meal kits and fresh meal delivery services, which provide consumers with convenient yet fresh cooking options. These alternatives align with modern consumer preferences for convenient yet wholesome meals, impacting the growth of the ready-to-eat soup segment.

Segment Analysis

By Product Type: Shelf Stable Dominance Faces Chilled Innovation

The Shelf Stable Soup segment holds a 46.12% market share in 2025, driving the overall soup market through its convenience, accessibility, and versatility. The segment's success stems from meeting consumer needs for easy-to-store, long-lasting, and quick-to-prepare food options that align with modern lifestyles. Shelf-stable soups offer extended shelf life without refrigeration, reducing food waste while improving supply chain efficiency and retail distribution. Product innovation continues to strengthen the segment's position by addressing diverse consumer preferences and health considerations. The segment maintains consistent demand throughout the year due to pantry stocking practices and comfort food preferences, regardless of seasonal or economic conditions.

Chilled Soup represents the fastest-growing segment in the North America Soup Market, with a CAGR of 4.26% through 2031. Growth stems from consumer preferences for fresh, minimally processed foods that meet wellness and clean-label requirements. The segment positions itself in the premium category, emphasizing superior taste, nutritional value, and natural ingredients without preservatives. Advances in refrigerated packaging technology support product freshness and convenience. The expansion of modern retail formats has increased the availability and consumption of chilled soups. The segment's growth also benefits from consumer interest in diverse flavors and convenient consumption options.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Category: Plant-Based Gains Ground Against Meat Dominance

In 2025, the Non-Vegetarian Soup category maintains a dominant market share of 64.54%. This segment's performance is attributed to sustained consumer demand for protein-enriched meal solutions, specifically in chicken, beef, and seafood-based variants. The substantial nutritional composition and distinctive flavor profiles attract consumers seeking nutritionally complete meals, particularly during cold seasons. Manufacturing entities continue to enhance their product portfolios through the integration of traditional formulations with international flavor profiles to address evolving consumer preferences. The segment's market position is reinforced by organizations' commitment to premium ingredient procurement protocols.

The Vegetarian Soup segment demonstrates significant market potential with a projected CAGR of 4.71% through 2031. This trajectory is indicative of heightened consumer engagement with plant-based dietary options, health consciousness, and environmental sustainability considerations. The segment's market penetration encompasses both dedicated vegetarians and flexitarian consumers seeking nutritionally optimized meal alternatives. Companies focus on incorporating fresh vegetables, incorporation of premium vegetables, whole grains, and certified organic ingredients to address consumer requirements for natural and sustainable product offerings. For instance, in November 2024, Amy's Kitchen expanded its product portfolio with five new soup variants that synthesize international and American Southern culinary traditions, utilizing organic components and fresh agricultural produce, exemplifying the segment's emphasis on premium, authentic product development.

By Packaging Type: Pouches Challenge Can Supremacy

In 2025, the Cans packaging type maintains a dominant market share of 58.12%. This leadership position stems from the fundamental advantages of cans, including extended shelf life, robust product protection, and efficient storage capabilities, which benefit both manufacturers and consumers. Canned soups remain a household essential due to their convenience, cost-effectiveness, and widespread availability. Recent improvements in canning technology have enhanced product quality, safety, and nutrient preservation, addressing consumer concerns about flavor and nutritional value. The recyclable nature of metal cans also aligns with growing environmental consciousness among consumers.

The pouches packaging segment is projected to grow at a CAGR of 4.95% through 2031 in the North America Soup Market. This growth reflects increasing consumer preference for convenient, portable, and sustainable packaging options. Pouches offer advantages over traditional packaging formats, including reduced weight, space efficiency, and decreased environmental impact. The flexible format enables innovations such as single-serve portions, resealable features, and easy-opening designs. Manufacturers are utilizing pouches for premium, organic, and ready-to-eat soups to meet consumer demand for fresh and convenient meal options. The format's ability to maintain product quality, extend shelf life, and optimize supply chain operations supports its increasing adoption.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Foodservice Recovery Drives On-Trade Growth

In 2025, off-trade channels dominate the North America Soup Market, capturing 71.02% market share. This dominance stems from consumer preference for purchasing soups from retail outlets, including supermarkets, hypermarkets, convenience stores, and grocery stores. These channels provide consumers with extensive product variety, one-stop shopping convenience, and promotional offers that encourage bulk and repeat purchases. Off-trade channels enable manufacturers to maintain strong brand visibility through in-store promotions and sampling activities, building consumer trust and loyalty. The widespread presence of retail outlets ensures soup accessibility across various demographic and regional segments.

The On-trade distribution channel is growing at a CAGR of 6.05% through 2031 in the North America Soup Market, driven by increased dining out, convenience snacking, and foodservice consumption. This growth comes from rising demand in restaurants, cafes, quick-service outlets, and hospitality sectors that provide fresh soup options as part of their dining offerings. On-trade channels meet consumer demand for freshly prepared, premium soups made with quality ingredients, often customized to regional preferences and health trends. According to the United States Department of Agriculture (USDA), food sales at foodservice outlets reached USD 1.54 trillion in 2024, with full-service establishments contributing USD 546.6 billion and limited-service establishments adding USD 548.9 billion . These figures demonstrate the significant role of the foodservice industry in driving soup consumption through on-trade channels.

Geography Analysis

The United States holds a 69.42% share in 2025, dominating the North American soup market. This position stems from the country's established retail infrastructure, strong consumer preferences, and widespread brand presence across demographic segments. The market thrives on a diverse population that generates demand for various soup varieties, from traditional recipes to health-focused options. The combination of brand trust and continuous product development maintains consumer loyalty and market growth, establishing the United States as the region's primary market driver.

Canada demonstrates the highest growth rate in the North American Soup Market, with a projected CAGR of 5.29% through 2031. This expansion results from population growth and higher disposable incomes, enabling consumers to purchase premium soup varieties. Canadian consumers show increasing interest in international flavors and premium products, while emphasizing quality ingredients. The market benefits from growing demand for healthy, organic, and specialized soups, allowing Canada to expand its regional market presence.

Mexico presents significant growth potential in the market. The country's position as a major soup and broth importer is evidenced by its USD 446 million import value in 2023, ranking second globally according to the Observatory of Economic Complexity (OEC) . This import volume indicates increasing consumer demand for soup products, supported by health consciousness, urban development, and middle-class expansion. Mexico's exposure to global cuisines and growing retail and e-commerce channels positions it as an important growth market in North America.

Competitive Landscape

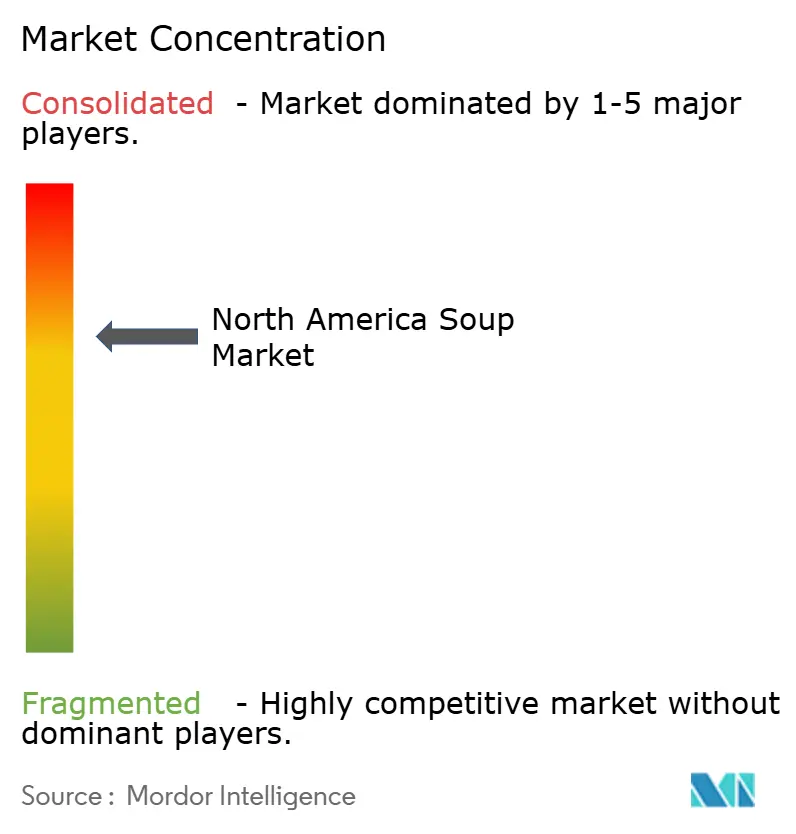

The North American soup Market operates as an oligopoly, with established companies like Campbell's, General Mills, Kraft Heinz, and Nestlé holding dominant positions. These companies maintain their market leadership through strong brand recognition, well-developed distribution networks, and manufacturing economies of scale. Their sustained investments in innovation, brand development, and operational improvements help maintain their competitive positions. The companies' extensive distribution capabilities across multiple channels, combined with consistent product quality, reinforce their market dominance.

Market leaders are implementing advanced technologies to improve operations and consumer insights. Companies use artificial intelligence (AI) and data analytics to optimize supply chains, improve demand forecasting, and accelerate product development. AI applications enable efficient development of new soup flavors based on consumer preferences while reducing waste and improving production efficiency. These technological implementations help companies maintain market responsiveness.

The market presents growth opportunities in functional soups, plant-based proteins, and sustainable packaging. Consumer demand is increasing for products that combine convenience with health benefits, including immune support, digestive health, and enhanced nutrition. This trend creates opportunities for soups fortified with vitamins, minerals, and plant-based proteins. The growing preference for vegan and flexitarian diets expands the market for plant-based options. Additionally, consumer environmental awareness drives demand for sustainable packaging that maintains product quality while reducing environmental impact.

North America Soup Industry Leaders

-

The Campbell's Company

-

General Mills Inc.

-

Kraft Heinz Company

-

Nestlé SA

-

Unilever PLC

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2025: Campbell Soup Company and Pabst Blue Ribbon collaborated to develop two limited-edition beer-infused soups. The products combine PBR's malt flavor profile with Campbell's Chunky soup recipes.

- July 2025: General Mills, Inc. introduced five new barbecue-inspired soups under its Progresso Pitmaster line, each containing 14g or more of protein per can. The soups deliver barbecue flavors in a convenient, ready-to-eat format.

- July 2025: Samyang Foods introduced a Korean-inspired instant ramen noodle soup in three flavors: black pepper and beef, garlic and clam, and red pepper chicken with cilantro.

- September 2024: Fuchs North America introduced the Sensational Soups and Stews Collection, featuring three seasoning varieties: Afghan pumpkin soup seasoning, tamarind chili mix, and gingered carrot blend.

North America Soup Market Report Scope

Soup is primarily liquid food, generally served warm or hot, that is made by combining ingredients of meat or vegetables with stock, milk, or water.

The North American soup market has been segmented by type, category, distribution channel, and country. By type, the market is segmented into canned/preserved, chilled, dehydrated/instant, and other types. By category, the market is segmented into conventional and organic. By distribution channel into supermarkets/hypermarkets, convenience stores, online stores, and other distribution channels. Also, the study provides an analysis of the soup market in the emerging and established markets across the region, including the United States, Mexico, Canada, and Rest of North America. For each segment, the market sizing and forecasts have been done on the basis of value in USD million.

By Product Type

| Dry Soup |

| Shelf Stable Soup |

| Chilled Soup |

| Frozen Soup |

| Others |

By Category

| Vegetarian Soup |

| Non-Vegetarian Soup |

By Packaging Type

| Cans |

| Pouches |

| Cartons |

| Other Packaging types |

By Distribution Channel

| On-Trade | |

| Off-trade | Supermarkets/Hypermarkets |

| Convenience/ Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Dry Soup | |

| Shelf Stable Soup | ||

| Chilled Soup | ||

| Frozen Soup | ||

| Others | ||

| By Category | Vegetarian Soup | |

| Non-Vegetarian Soup | ||

| By Packaging Type | Cans | |

| Pouches | ||

| Cartons | ||

| Other Packaging types | ||

| By Distribution Channel | On-Trade | |

| Off-trade | Supermarkets/Hypermarkets | |

| Convenience/ Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the north america soup market in 2026?

It is valued at USD 7 billion in 2026 with expectations of reaching USD 8.54 billion by 2031.

What is the projected CAGR for soup sales across North America?

The category is forecast to register a 4.03% CAGR between 2026 and 2031.

Which product type is growing the fastest?

Chilled soup leads growth, expanding at a 4.26% CAGR as consumers equate refrigerated placement with freshness.

Which country is the fastest-growing market in the region?

Canada is expected to rise at a 5.29% CAGR through 2031 due to premium flavor exploration and rising disposable income.