Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

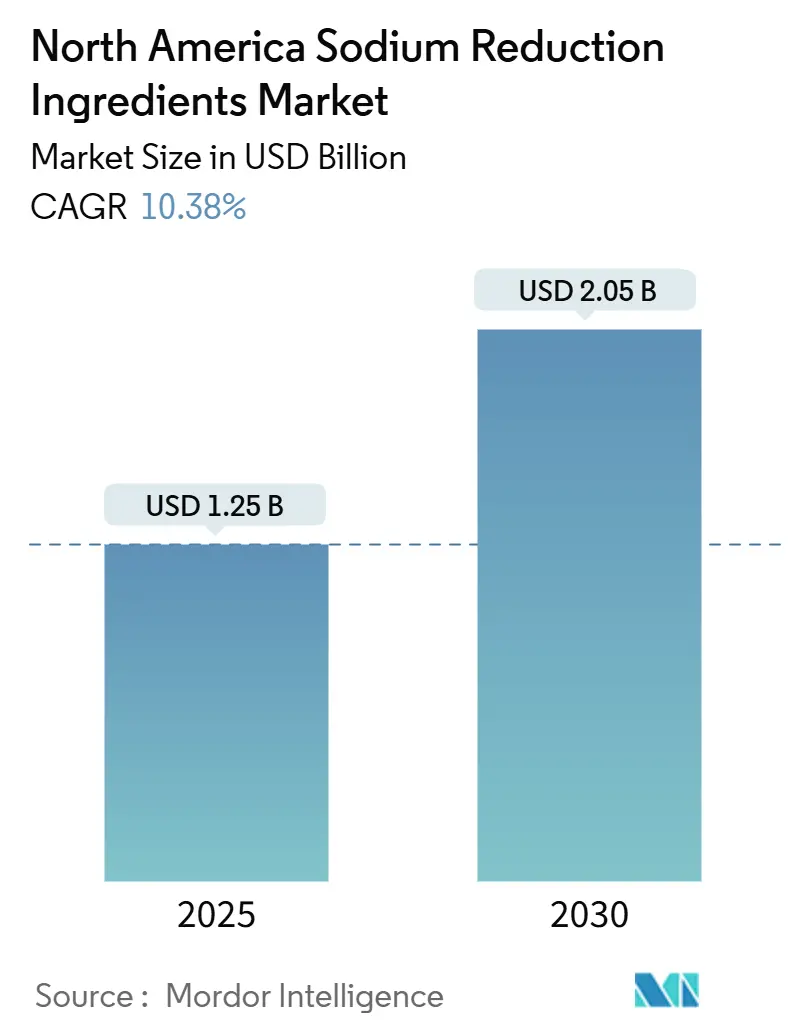

| Market Size (2025) | USD 1.25 Billion |

| Market Size (2030) | USD 2.05 Billion |

| Growth Rate (2025 - 2030) | 10.38% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Sodium Reduction Ingredients Market Analysis by Mordor Intelligence

The North America sodium reduction ingredient market size is valued at USD 1.25 billion in 2025 and is projected to reach USD 2.05 billion by 2030, registering a 10.38% CAGR. Heightened regulatory action, led by the FDA’s Phase II voluntary sodium targets, is compressing reformulation timelines, while front-of-pack warnings in Mexico and a pending “high in” symbol in Canada strengthen regional alignment. Institutional buyers, such as school districts, have added week-average sodium limits to bid specifications, creating priority demand for validated potassium-sodium blends and yeast extracts. Consumer awareness of hypertension has risen as the CDC reports that nearly half of U.S. adults are affected, pushing retail sales of low-sodium SKUs and encouraging meal-kit operators to adopt stricter internal limits. Meanwhile, AI-driven formulation tools are cutting development time by simulating taste interactions in silico, allowing producers to commercialize sodium-reduced snacks and condiments in under a year.

Key Report Takeaways

- By product type, mineral salts led with 49.15% of the North America sodium reduction ingredient market share in 2024, while yeast extracts are forecast to expand at a 12.83% CAGR through 2030.

- By form, powders and granules accounted for 68.53% of the value in 2024, whereas liquid formats are expected to advance at a 12.03% CAGR between 2025 and 2030.

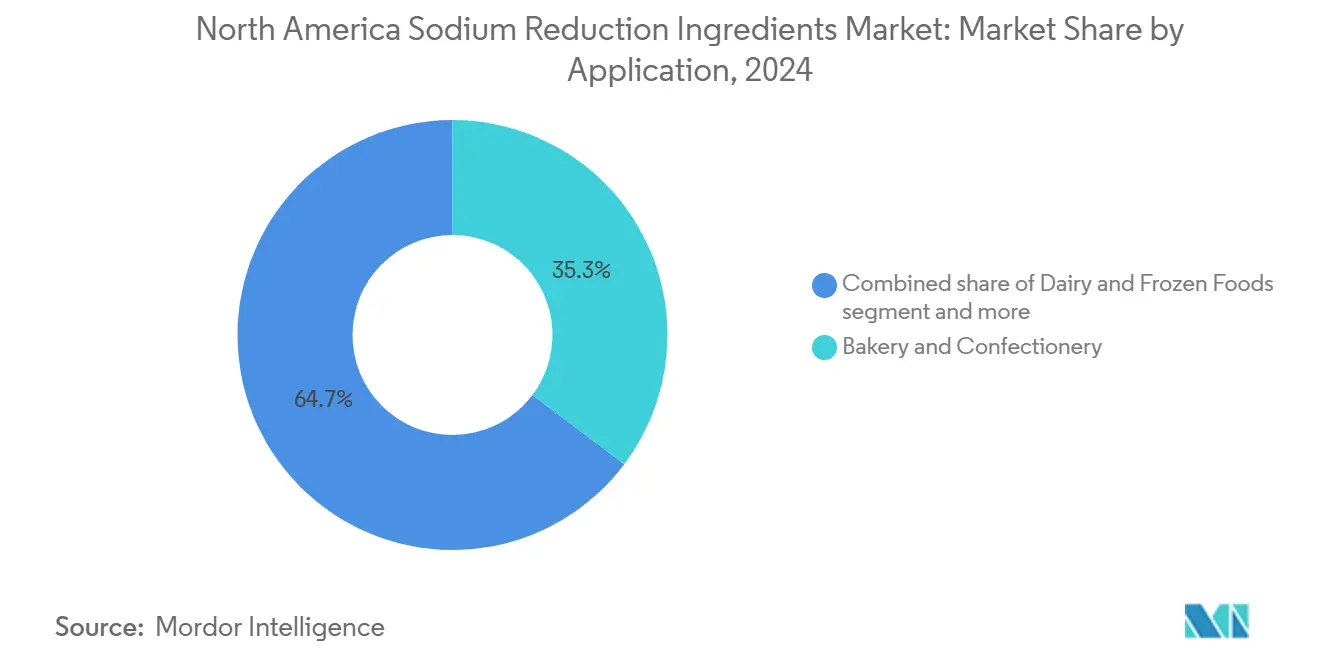

- By application, bakery and confectionery captured 35.26% of revenue in 2024; condiments, seasonings, and sauces are projected to grow at a 12.63% CAGR to 2030.

- By geography, the United States represented 62.41% of 2024 sales, while Mexico is poised to register an 11.58% CAGR through 2030.

North America Sodium Reduction Ingredients Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FDA Phase-II voluntary sodium targets accelerate reformulation | +2.1% | United States, with spillover to Canada and Mexico aligning with FDA guidance | Medium term (2-4 years) |

| Growing consumer awareness of hypertension and CVD risks | +1.6% | North America-wide, with highest penetration in urban U.S. markets and Canadian provinces with active health campaigns | Long term (≥ 4 years) |

| Advances in potassium-salt blends and umami enhancers | +1.2% | United States and Canada, with early adoption in premium and organic segments | Medium term (2-4 years) |

| AI-driven formulation platforms for customised low-sodium solutions | +1.0% | United States, concentrated in R&D hubs (California, New York, Illinois) | Short term (≤ 2 years) |

| Plant-based meat and dairy analog boom needing sodium cutbacks | +1.5% | United States and Canada, with emerging traction in Mexico's urban centers | Medium term (2-4 years) |

| Procurement push from meal-kit and food-service operators | +1.1% | United States, particularly in metropolitan areas with high meal-kit penetration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

FDA Phase-II Voluntary Sodium Targets Accelerate Reformulation

The FDA’s August 2024 Phase II voluntary sodium targets, aiming to lower the average American intake to ~2,750 mg/day, have accelerated reformulation efforts across packaged foods, with Phase I data showing that ~40% of categories are meeting or nearing the targets[1]Source: U.S. Food and Drug Administration, “Sodium Reduction,” FDA.gov. The December 2024 update to the “healthy” nutrient-content claim, capping sodium at 10% of the daily value (230 mg) per reference amount, effectively disqualifies many legacy bakery, snack, and condiment products. USDA school meal sodium limits, phased in from 2025-2026 and enforced via weekly averages starting in July 2027, are driving the adoption of pre-validated ingredients among institutional buyers[2]Source: U.S. Department of Agriculture, “School Meal Sodium Limits,” USDA.gov. FDA guidance allowing “potassium salt” as an alternative label for potassium chloride has eased consumer confusion, but voluntary compliance results in uneven reformulation among smaller manufacturers. Meanwhile, New York City’s sodium warning icon rule, expanded under Assembly Bill A8860B, pressures foodservice suppliers to use mineral-salt blends and yeast extracts to meet menu-item thresholds.

Growing Consumer Awareness of Hypertension and CVD Risks

Hypertension affects 48% of U.S. adults, about 119.9 million people, with 90% exceeding the recommended daily sodium intake of 2,300 mg, averaging 3,400 mg, according to the CDC[3]Source: Centers for Disease Control and Prevention, “Salt,” CDC.gov. This public health burden drives demand for “low-sodium” and “reduced-sodium” products, which require a 25% or 50% sodium reduction under FDA labeling rules. A 2024 Peru-based clinical trial demonstrated that a 75% sodium chloride/25% potassium chloride substitute reduced new hypertension incidence by 50% and lowered blood pressure by ~2 mmHg, supporting the cardiovascular benefits of potassium-enriched formulations. High-sodium condiments, such as soy sauce exceeding 750 mg per tablespoon, have drawn regulatory scrutiny from the American Heart Association. Meanwhile, Health Canada’s 2012 voluntary targets aimed to reduce the average intake to 2,760 mg by 2017, illustrating the impact of sustained public health campaigns[4]Source: Health Canada, “Sodium Policy,” Canada.ca. Front-of-pack labeling initiatives, including Canada’s proposed “high in” symbol and Mexico’s NOM-051 “EXCESS SODIUM” warnings, coupled with PROFECO audits in 2024, are further increasing consumer awareness and encouraging reformulation at retail.

Advances in Potassium-Salt Blends and Umami Enhancers

Potassium chloride can replace sodium on a 1:1 basis, allowing for up to 50% sodium reduction in processed meats when paired with taste-masking agents. However, its bitter and metallic notes typically limit substitution to 20–30% by weight, as per Norway’s VKM protocol (2021). Cargill’s Potassium Pro Ultra Fine, optimized for plant-based meat analogs, achieves a 20–35% reduction by utilizing smaller particle sizes to enhance coverage and mitigate bitterness. Enzymatic treatments that generate glutamate and branched-chain amino acids can reduce sodium by ~20% while maintaining umami. Yeast extracts blended with adenosine monophosphate (AMP) or L-arginine help block bitterness and enhance saltiness. Patented combinations of lysine monohydrochloride, potassium chloride, and succinic acid support clean-label formulations. Cheese applications have successfully substituted 30–50% of the potassium chloride with umami enhancers, highlighting the category-specific effectiveness of mineral-salt blends.

AI-Driven Formulation Platforms for Customised Low-Sodium Solutions

Advanced digital and AI-driven platforms are accelerating sodium-reduction innovation in North America. DSM-Firmenich’s TASTECOMPASS® models taste interactions in silico, cutting formulation cycles from 18 to under 12 months. Unilever’s 2023 zero-salt Knorr stock cube, developed using computational flavor design, replaced sodium entirely with yeast extracts and mineral salts, demonstrating AI’s ability to bypass traditional trial-and-error. Firmenich’s AI-generated flavor molecules create bespoke umami profiles for high-sodium plant-based proteins, while Tate & Lyle’s Sensation™ tool recommends texture and mouthfeel adjustments to offset blandness in bakery and dairy applications. Kerry’s Sodium Reduction Simulator with TasteSense Salt enables up to 40% sodium reduction in snacks without potassium chloride, addressing hyperkalemia concerns, and MANE’s SENSE CAPTURE™ program uses sensory analytics to identify subtle flavor gaps, speeding regulatory approval for “low-sodium” and “reduced-sodium” claims.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Potassium-chloride bitterness and metallic off-notes | -0.8% | North America-wide, with acute challenges in snack and bakery applications | Short term (≤ 2 years) |

| Higher ingredient cost vs. common salt | -0.7% | United States and Canada, particularly affecting mid-tier processors with tight margins | Medium term (2-4 years) |

| Hyper-kalemia safety limits in at-risk populations | -0.6% | United States and Canada, concentrated among CKD patients and those on RAAS inhibitors | Long term (≥ 4 years) |

| Supply tightness for specialty yeast and nucleotide extracts | -0.5% | North America-wide, with bottlenecks in yeast-extract production capacity | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Potassium-Chloride Bitterness and Metallic Off-Notes

Potassium chloride’s bitter and metallic taste remains the main barrier to broader adoption, as sodium ions block bitterness receptors while potassium does not. Norway’s VKM protocol (2021) supports a realistic substitution of 20–30% in processed foods, but reaching 50%, as needed for “reduced-sodium” claims, requires taste modulators such as adenosine monophosphate, L-arginine, or yeast extracts, which increases formulation complexity and cost[5]Source: Norwegian Scientific Committee for Food and Environment, “Potassium Chloride Substitution Protocol,” vkm.no. Cargill’s Potassium Pro Ultra Fine achieves 20–35% sodium reduction in plant-based meats, though acceptance drops sharply above 40%. While adenosine monophosphate can block bitterness and L-arginine enhances saltiness, these modulators are not universally GRAS-approved, which limits their clean-label use. Cheese has achieved 30–50% substitution with umami enhancers, but bakery and snack products remain challenged by potassium’s metallic aftertaste.

Higher Ingredient Cost vs. Common Salt

Potassium-based salt substitutes and yeast extracts carry significant price premiums, with potassium salts costing 1.1-14.6 times more than sodium chloride and low-sodium condiments 2-3 times higher than conventional products, compressing margins for mid-tier processors in snacks and bakery. Yeast extracts, containing 5-10% glutamate, remain costly due to the fermentation and extraction processes, with supply improvements from Angel Yeast’s 11,000-tonne Baiyang plant and Asahi’s acquisition of Leiber GmbH only partially easing the lead times of 8-12 weeks. Specialty ingredients, such as Corbion’s PURASAL potassium lactate, priced three to four times higher than sodium lactate, limit adoption despite their functional benefits. Industry investment, such as ADM’s USD 269 million R&D spend in 2024 on taste-modulation platforms, underscores the need for innovation to deliver cost-effective sodium reduction beyond simple substitution.

Segment Analysis

By Product Type: Mineral Salts Anchor Share, Yeast Extracts Surge

Mineral salts dominated the North America sodium reduction ingredients market in 2024, capturing 49.15% of revenue, led by potassium chloride due to its 1:1 sodium replacement ratio and broad regulatory acceptance across bakery, meat, and snack applications. Potassium chloride enables up to 50% sodium reduction in processed meats when paired with taste-masking agents, with Cargill’s Watkins Glen, New York, facility reflecting the strategic focus on food-grade supply. Other mineral salts, including magnesium sulfate, potassium lactate, and calcium chloride, serve niche roles. Corbion’s PURASAL potassium lactate provides both preservation and sodium-replacement functionality, while its Verdad Essence WH100 extends applications into bakery mold inhibition. Yeast extracts, containing ~5% free glutamate and 10% total glutamate, are increasingly blended with nucleotide extracts to mask potassium’s metallic notes, supported by Angel Yeast’s 11,000-tonne Baiyang plant, which addresses supply constraints delaying condiment reformulation.

Amino acids and glutamates are gaining traction in plant-based meat applications, where DSM-Firmenich’s Maxavor® RYE LS process flavor delivers savory depth while enabling 20–30% sodium reductions. Enzymatic treatments generating glutamate and branched-chain amino acids have also proven to reduce sodium by ~20% in savory foods, validating amino-acid platforms. The “Others” segment, including proprietary blends and novel modulators, is benefiting from innovations like Kerry’s TasteSense Salt, which achieves up to 40% sodium reduction in snacks without potassium chloride, and MANE’s SENSE CAPTURE™ system, which identifies flavor gaps in sodium-reduced prototypes. Consolidation is shaping the yeast-extract space, exemplified by Asahi Group Foods’ 2025 acquisition of Leiber GmbH, with the segment’s projected 8.5% CAGR through 2029 outpacing mineral salts as manufacturers increasingly prioritize umami-rich, clean-label solutions.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Form: Powder Dominates, Liquid Gains in Beverages

Powder and granule formats dominated the North American sodium reduction ingredients market in 2024, holding a 68.53% share due to their compatibility with dry-blend seasonings, bakery mixes, and snack toppings, where heterogeneous salt distribution can achieve up to 50% sodium reduction without compromising taste. Technologies like Tate & Lyle’s SODA-LO hollow sodium bicarbonate microspheres enable similar reductions in baked goods while maintaining leavening and clean-label compliance. Salt microspheres are increasingly used in surface-salted snacks, and Cargill’s Potassium Pro® Ultra Fine powder reduces bitterness in plant-based meats for dry-blend applications.

Liquid formats are projected to grow at a 12.03% CAGR from 2025 to 2030, driven by beverage and sauce applications that require in-line dosing for flavor consistency and reduced batch variability. Corbion’s PURASAL® potassium lactate liquid supports sodium reduction while extending shelf life via antimicrobial activity, and liquid yeast extracts maintain umami intensity in condiments and sauces, enabling 17–50% sodium reductions. DSM-Firmenich’s TasteElements toolkit and Givaudan’s Nutri TasteSolutions Sodium provide liquid and powder solutions for plant-based proteins, sauces, and extrusion processes, enhancing formulation precision and operational efficiency across diverse processing environments.

By Application: Bakery Leads, Condiments Accelerate

Bakery and confectionery led the North American sodium reduction ingredients market in 2024, capturing a 35.26% share, driven by high baseline sodium levels and advances in sodium bicarbonate substitution technologies. Tate & Lyle’s SODA-LO hollow microspheres enable up to 50% sodium reduction in baked goods while maintaining leavening and clean-label compliance. Corbion’s Verdad® Essence WH100 natural mold inhibitor addresses microbial stability challenges in lower-sodium formulations. Studies on heterogeneous salt distribution confirm that strategic crystal placement can reduce sodium by ~50% without compromising sensory properties in bread and savory biscuits.

Condiments, seasonings, and sauces are projected to grow at a 12.63% CAGR from 2025 to 2030, fueled by consumer health awareness and industry initiatives such as Kraft Heinz’s 2023 commitment to reduce sodium in BBQ sauces and salad dressings. Yeast extracts, with ~5% free glutamate, are increasingly used in the reformulation of soy and fish sauces, supported by Angel Yeast’s 11,000-tonne Baiyang facility. Other applications, including dairy and frozen foods, meat products, and snacks, also contribute significantly. Snacks, for instance, leverage Kerry’s TasteSense Salt for up to 40% sodium reduction without potassium chloride, while meat products adopt potassium lactate and yeast extracts to maintain flavor while complying with “reduced-sodium” claims.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The United States dominated the North American sodium reduction ingredients market in 2024, accounting for 62.41% of the regional share, driven by regulatory and public health initiatives. The FDA's Phase II voluntary sodium targets (August 2024) and the December 2024 update to the “healthy” nutrient-content claim, which caps sodium at 230 mg per reference amount, are accelerating reformulation efforts across packaged foods. USDA school meal sodium limits, effective from the 2025–2026 school year and enforced via weekly averages from July 2027, are prompting institutional buyers to pre-validate sodium-reduced SKUs, while New York City’s sodium warning icon rules and California’s state-level disclosure legislation create further downstream pressure. CDC data showing 48% of adults with hypertension and 90% exceeding the recommended sodium intake reinforce retail demand for “low-sodium” and “reduced-sodium” claims. Investments such as Cargill’s expansion of its Watkins Glen Potassium Pro® facility, Kerry’s TasteSense Salt, and DSM-Firmenich’s TASTECOMPASS® predictive system highlight the U.S. leadership in AI-driven and formulation-focused R&D.

Canada maintains a smaller but stable share, shaped by Health Canada’s 2012 voluntary sodium targets, which achieved an 8% reduction in average intake to 2,760 mg/day by 2017. Proposed front-of-pack “high in” sodium symbols, aligned with FDA thresholds, are expected to harmonize reformulation strategies for manufacturers serving both markets. North American ingredient supply chains are increasingly integrated, exemplified by Tate & Lyle’s 2024 Sensation™ formulation tool, which leverages machine learning to optimize texture and mouthfeel in sodium-reduced foods. Provincial health campaigns in Ontario and British Columbia have heightened consumer awareness of hypertension and cardiovascular risk, driving demand for low-sodium SKUs across dairy, bakery, and snack categories.

Mexico is forecast to grow at 11.58% CAGR through 2030, driven by NOM-051 front-of-pack “EXCESS SODIUM” warnings, COFEPRIS and PROFECO compliance audits, and rising urbanization and flexitarian trends. Regulatory pressures are prompting manufacturers to adopt potassium chloride blends and yeast extracts, though price sensitivity remains a barrier, with low-sodium condiments costing 2–3× more than conventional products. Ingredient suppliers such as Angel Yeast are expanding into the Mexican condiment and snack markets, while plant-based meat analogs exceeding 400 mg sodium per 4-ounce serving present opportunities for validated sodium-reduction solutions. Smaller Caribbean and Central American markets remain nascent but are expected to benefit from spillover demand as multinational manufacturers harmonize low-sodium formulations across the region.

Competitive Landscape

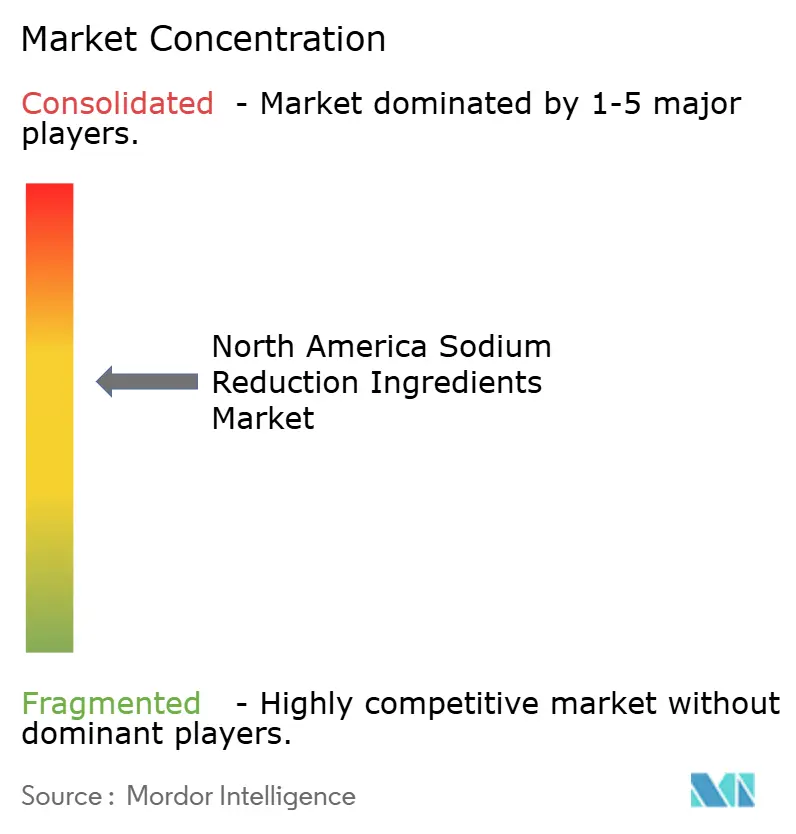

The North American sodium reduction ingredients market exhibits moderate concentration, led by major players such as Cargill, Kerry Group, Tate & Lyle, Givaudan, and DSM-Firmenich. However, white-space opportunities are emerging in AI-driven formulation platforms and enzymatic taste-masking systems that mitigate potassium chloride’s sensory limitations. Strategic moves focus on vertical integration and technology acquisition: Asahi Group Foods’ 2025 acquisition of Leiber GmbH secures yeast-extract supply across Europe, while ADM’s 2024 purchases of Revela Foods, FDL, and Totally Natural Solutions, backed by USD 269 million in R&D, underscore the focus on taste-modulation capabilities. Cargill’s Watkins Glen expansion for Potassium Pro® potassium chloride addresses specialty mineral-salt supply bottlenecks, and Angel Yeast’s 11,000-tonne Baiyang plant positions the company to capture 8.5% CAGR demand growth for yeast extracts. Smaller innovators, including NuTek Natural Ingredients and Salt of the Earth, leverage proprietary mineral-salt blends to serve niche organic and clean-label segments, though limited scale constrains their distribution relative to incumbents.

Technology is increasingly the main differentiator in sodium-reduction solutions. DSM-Firmenich’s TASTECOMPASS® predictive modeling reduces formulation cycles from 18 to under 12 months by simulating taste interactions, while Kerry’s May 2024 TasteSense Salt platform enables up to 40% sodium reduction in snacks without potassium chloride, addressing hyperkalemia concerns. Academic-industry partnerships, such as the Michigan State University patent covering lysine monohydrochloride, potassium chloride, and succinic acid combinations, validate taste-masking innovations for commercial use. Corbion’s AI-powered Listeria control and refrigerated-food protection expansions address microbial-stability challenges in sodium-reduced formulations, compensating for higher water activity at lower salt levels.

Regulatory compliance is increasingly embedded in procurement and innovation strategies. FDA GRAS status, ISO 22000 food-safety certification, and third-party verification are now baseline requirements for institutional and food-service channels. Angel Yeast’s September 2025 FDA GRAS approval for AngeoPro yeast protein exemplifies the regulatory rigor required for market entry, ensuring that sodium-reduction ingredients not only meet functional and sensory standards but also satisfy safety and traceability expectations across North American supply chains.

North America Sodium Reduction Ingredients Industry Leaders

-

Givaudan SA

-

Tate & Lyle Plc

-

Kerry Group Plc

-

DSM-Firmenich

-

Cargill Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Corbion launched Verdad® Essence WH100, a natural mold inhibitor for bakery applications, addressing the microbial stability challenges inherent in sodium-reduced formulations where lower salt concentrations increase water activity and necessitate compensatory preservation strategies.

- March 2025: Asahi Group Foods acquired Leiber GmbH, a German yeast-extract manufacturer with six factories across Germany, Spain, and Poland, signaling a consolidation effort aimed at securing a stable yeast-extract supply.

- March 2025: Angel Yeast showcased its yeast-extract solutions at FIC2025, highlighting the company's 11,000-tonne plant in Baiyang, Yichang, operational in 2025, and its AngeoPro yeast protein, which received FDA GRAS status in September 2025.

- December 2024: Corbion expanded its refrigerated-food protection portfolio by integrating potassium lactate and calcium propionate solutions to address microbial stability risks in sodium-reduced meat and dairy applications.

North America Sodium Reduction Ingredients Market Report Scope

The North America sodium reduction ingredients market includes functional compounds used to lower sodium content in foods while maintaining flavor, texture, and shelf life. These ingredients encompass amino acids and glutamates, mineral salts such as potassium chloride, magnesium sulphate, potassium lactate, and calcium chloride, yeast extracts, and other proprietary solutions. They are available in powder/granule and liquid forms to suit diverse applications, including bakery and confectionery, condiments, seasonings and sauces, dairy and frozen foods, meat and meat products, snacks, and other prepared foods. The market spans the United States, which leads in demand due to strict labeling regulations and health-conscious consumers; Canada, supported by sodium reduction initiatives and regulatory frameworks; Mexico, driven by rising urbanization and packaged food consumption; and the rest of North America, including Caribbean markets with niche demand and limited production. These ingredients enable food manufacturers to meet regulatory sodium targets and consumer demand for healthier, clean-label products without compromising taste. Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

By Product Type

| Amino Acids and Glutamates | |

| Mineral Salts | Potassium Chloride |

| Magnesium Sulphate | |

| Potassium Lactate | |

| Calcium Chloride | |

| Yeast Extracts | |

| Others |

By Form

| Powder/Granules |

| Liquid |

By Application

| Bakery and Confectionery |

| Condiments, Seasonings and Sauces |

| Dairy and Frozen Foods |

| Meat and Meat Products |

| Snacks |

| Others |

By Country

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Amino Acids and Glutamates | |

| Mineral Salts | Potassium Chloride | |

| Magnesium Sulphate | ||

| Potassium Lactate | ||

| Calcium Chloride | ||

| Yeast Extracts | ||

| Others | ||

| By Form | Powder/Granules | |

| Liquid | ||

| By Application | Bakery and Confectionery | |

| Condiments, Seasonings and Sauces | ||

| Dairy and Frozen Foods | ||

| Meat and Meat Products | ||

| Snacks | ||

| Others | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected value of the North America sodium reduction ingredient market in 2030?

The market is forecast to reach USD 2.05 billion by 2030, growing at a 10.38% CAGR.

Which product type is expanding fastest in sodium-reduction formulations?

Yeast extracts are expected to grow at a 12.83% CAGR through 2030 as they mask off-notes and add umami depth.

How are U.S. regulations influencing ingredient demand?

FDA Phase II voluntary targets and USDA school meal limits push food makers to adopt validated low-sodium blends ahead of 2027 compliance checks.

Why are liquid sodium-reduction ingredients gaining popularity?

Beverage and sauce producers use in-line dosing to maintain flavor consistency, driving liquids at a 12.03% CAGR.

What competitive edge do AI formulation tools provide?

Platforms like TASTECOMPASS® reduce development cycles to under a year by modeling taste interactions digitally, lowering R&D cost and risk.

Page last updated on: