Market Size of north america satellite manufacturing Industry

| Icons | Lable | Value |

|---|---|---|

|

|

Study Period | 2017 - 2029 |

|

|

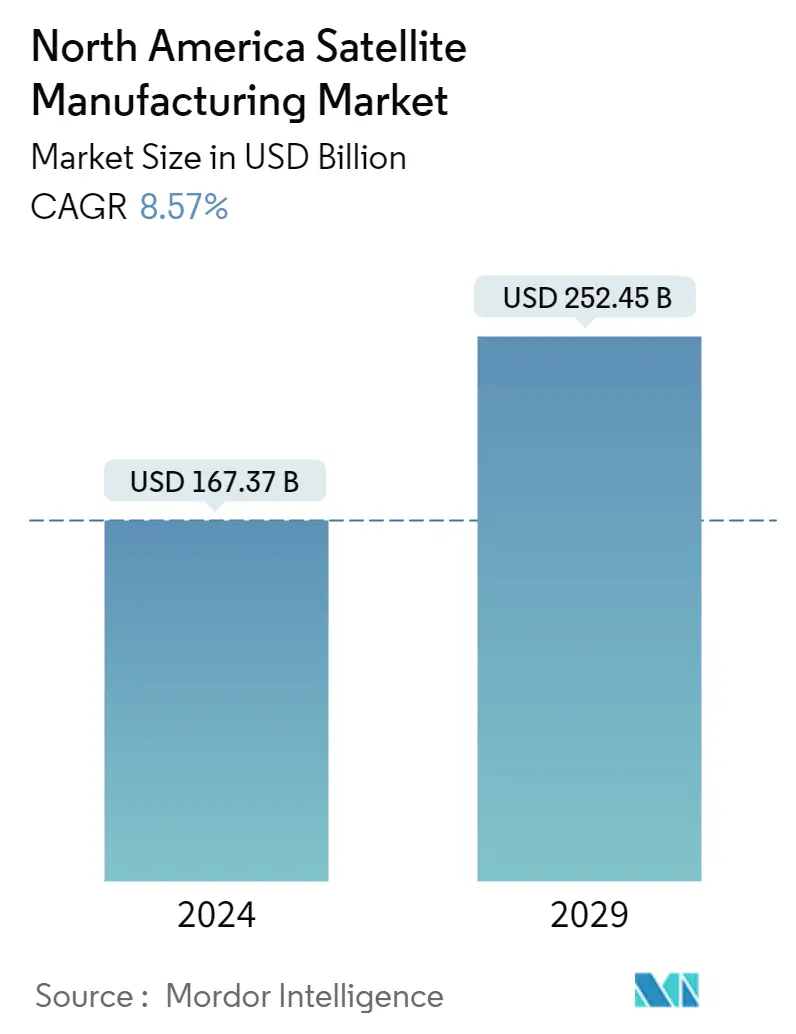

Market Size (2024) | USD 167.37 Billion |

|

|

Market Size (2029) | USD 252.45 Billion |

|

|

Largest Share by Orbit Class | LEO |

|

|

CAGR (2024 - 2029) | 8.57 % |

|

|

Largest Share by Country | United States |

|

|

Market Concentration | High |

Major Players |

||

|

|

||

|

*Disclaimer: Major Players sorted in no particular order |

North America Satellite Manufacturing Market Analysis

The North America Satellite Manufacturing Market size is estimated at USD 167.37 billion in 2024, and is expected to reach USD 252.45 billion by 2029, growing at a CAGR of 8.57% during the forecast period (2024-2029).

167.37 Billion

Market Size in 2024 (USD)

252.45 Billion

Market Size in 2029 (USD)

22.17 %

CAGR (2017-2023)

8.57 %

CAGR (2024-2029)

Largest Market by Satellite Mass

87.56 %

value share, 100-500kg, 2022

Minisatellites that offer a higher capacity for enterprise data (retail, banking), oil, gas, mining, and governments in developed countries are in high demand. Demand for minisatellites with LEOs is on the rise due to their expanded capacity.

Largest Market by Application

87.45 %

value share, Communication, 2022

Governments, space agencies, defense agencies, private defense contractors, and private space industry players are emphasizing the enhancement of communication network capabilities for various public and military reconnaissance applications.

Largest Market by Orbit Class

95.71 %

value share, LEO, 2022

LEO satellites are increasingly being adopted in modern communication technologies as they play an important role in Earth observation applications.

Largest Market by Propulsion Tech

73.93 %

value share, Liquid Fuel, 2022

Because of its high efficiency, reliability, and long lifespan, liquid fuel-based propulsion technology is becoming an ideal choice for space missions. It can be used in various orbit classes for satellites.

Leading Market Player

85.92 %

market share, Space Exploration Technologies Corp., 2022

SpaceX is the leading player in the global satellite launch vehicle market and maintains its market share globally through its Starlink project. The company produces 120 satellites per month.

LEO satellites are driving demand in the North America satellite manufacturing market

- During launch, a satellite or spacecraft is usually placed into one of many special orbits around the Earth, or it can be launched into an interplanetary journey. There are three types of Earth orbit: geostationary orbit (GEO), medium Earth orbit (MEO), and low Earth orbit (LEO). Many weather and communication satellites tend to have high Earth orbits farther from the surface. Satellites in medium Earth orbit include navigational and specialized satellites designed to monitor a specific area. Most science satellites, including NASA's Earth Observation System, are in low Earth orbit.

- Different satellites manufactured and launched in this region have different applications. For instance, during 2017-2022, out of the seven satellites launched in the MEO orbit, most were built for navigation/global positioning purposes. Similarly, out of the 32 satellites in the GEO orbit, most were deployed for communication and Earth observation purposes. Around 3,000+ LEO satellites owned by North American organizations were launched during this period.

- The growing use of satellites in areas such as electronic intelligence, Earth science/meteorology, laser imaging, and optical imaging is expected to drive the North American satellite manufacturing market during the forecast period. By orbit class, the market is expected to register a CAGR of 68% during the forecast period, and LEO satellites are expected to dominate the market.

The increased importance of satellite miniaturization has aided growth in the region

- The North American satellite manufacturing market is characterized by the presence of several players. However, the market is dominated by only a few players because of their wide range of product offerings. Private companies like SpaceX, Blue Origin, and Boeing are investing heavily in space technology and driving innovation in the industry. Space organizations like NASA have partnered with private players like SpaceX in the production and launch of satellites in the region.

- In addition, the satellite manufacturing industry is driven by demand for satellites for applications ranging from military surveillance, communications, and navigation to Earth observation. As a result, the demand for satellites from the civilian/government, commercial, and military sectors is increasing. During 2017-2022, 4,351 satellites were launched in the region. The number of satellites launched from 2021 to 2022 grew by 61%, while it grew by 40% from 2020 to 2021.

- In terms of the number of satellites operated by a country, the United States is the leading country, with over 2900+ satellites launched during 2017-2022, followed by Canada and Mexico. Major technological changes, such as miniaturization and the introduction of reusable satellite launch systems, are expected to open new opportunities in the North American satellite manufacturing market during the forecast period. The market is expected to surge by 68% in the forecast period, and the United States is anticipated to dominate the market.

North America Satellite Manufacturing Industry Segmentation

Communication, Earth Observation, Navigation, Space Observation, Others are covered as segments by Application. 10-100kg, 100-500kg, 500-1000kg, Below 10 Kg, above 1000kg are covered as segments by Satellite Mass. Eliptical, GEO, LEO, MEO are covered as segments by Orbit Class. Commercial, Military & Government are covered as segments by End User. Propulsion Hardware and Propellant, Satellite Bus & Subsystems, Solar Array & Power Hardware, Structures, Harness & Mechanisms are covered as segments by Satellite Subsystem. Electric, Gas based, Liquid Fuel are covered as segments by Propulsion Tech. Canada, United States are covered as segments by Country.

- During launch, a satellite or spacecraft is usually placed into one of many special orbits around the Earth, or it can be launched into an interplanetary journey. There are three types of Earth orbit: geostationary orbit (GEO), medium Earth orbit (MEO), and low Earth orbit (LEO). Many weather and communication satellites tend to have high Earth orbits farther from the surface. Satellites in medium Earth orbit include navigational and specialized satellites designed to monitor a specific area. Most science satellites, including NASA's Earth Observation System, are in low Earth orbit.

- Different satellites manufactured and launched in this region have different applications. For instance, during 2017-2022, out of the seven satellites launched in the MEO orbit, most were built for navigation/global positioning purposes. Similarly, out of the 32 satellites in the GEO orbit, most were deployed for communication and Earth observation purposes. Around 3,000+ LEO satellites owned by North American organizations were launched during this period.

- The growing use of satellites in areas such as electronic intelligence, Earth science/meteorology, laser imaging, and optical imaging is expected to drive the North American satellite manufacturing market during the forecast period. By orbit class, the market is expected to register a CAGR of 68% during the forecast period, and LEO satellites are expected to dominate the market.

| Application | |

| Communication | |

| Earth Observation | |

| Navigation | |

| Space Observation | |

| Others |

| Satellite Mass | |

| 10-100kg | |

| 100-500kg | |

| 500-1000kg | |

| Below 10 Kg | |

| above 1000kg |

| Orbit Class | |

| Eliptical | |

| GEO | |

| LEO | |

| MEO |

| End User | |

| Commercial | |

| Military & Government | |

| Other |

| Satellite Subsystem | |

| Propulsion Hardware and Propellant | |

| Satellite Bus & Subsystems | |

| Solar Array & Power Hardware | |

| Structures, Harness & Mechanisms |

| Propulsion Tech | |

| Electric | |

| Gas based | |

| Liquid Fuel |

| Country | |

| Canada | |

| United States |

North America Satellite Manufacturing Market Size Summary

The North American satellite manufacturing market is poised for significant growth, driven by advancements in space technology and increasing demand for satellite applications across various sectors. The market is characterized by a few dominant players, such as SpaceX, Blue Origin, and Boeing, who are heavily investing in innovation and expanding their product offerings. The region's market is further bolstered by partnerships between private companies and government space agencies like NASA, which are collaborating on satellite production and launches. The market's expansion is fueled by the growing need for satellites in military surveillance, communications, navigation, and Earth observation, with the United States leading in the number of satellites launched and operated.

Technological advancements, such as miniaturization and reusable launch systems, are opening new opportunities in the North American satellite manufacturing market. The preference for small satellites, which offer cost-effective solutions for scientific research and military applications, is increasing. The United States, in particular, is at the forefront of small satellite production, supported by ongoing investments in startups and nano/microsatellite projects. Government expenditure on space programs in North America is substantial, with the United States being the highest spender globally. The Canadian space sector is also contributing to the region's growth, with a focus on developing skills for nanosatellite technology. The market remains consolidated, with major players like Capella Space Corp., Lockheed Martin Corporation, Maxar Technologies Inc., Northrop Grumman Corporation, and Space Exploration Technologies Corp. dominating the landscape.

North America Satellite Manufacturing Market Size - Table of Contents

-

1. MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2029 and analysis of growth prospects)

-

1.1 Application

-

1.1.1 Communication

-

1.1.2 Earth Observation

-

1.1.3 Navigation

-

1.1.4 Space Observation

-

1.1.5 Others

-

-

1.2 Satellite Mass

-

1.2.1 10-100kg

-

1.2.2 100-500kg

-

1.2.3 500-1000kg

-

1.2.4 Below 10 Kg

-

1.2.5 above 1000kg

-

-

1.3 Orbit Class

-

1.3.1 Eliptical

-

1.3.2 GEO

-

1.3.3 LEO

-

1.3.4 MEO

-

-

1.4 End User

-

1.4.1 Commercial

-

1.4.2 Military & Government

-

1.4.3 Other

-

-

1.5 Satellite Subsystem

-

1.5.1 Propulsion Hardware and Propellant

-

1.5.2 Satellite Bus & Subsystems

-

1.5.3 Solar Array & Power Hardware

-

1.5.4 Structures, Harness & Mechanisms

-

-

1.6 Propulsion Tech

-

1.6.1 Electric

-

1.6.2 Gas based

-

1.6.3 Liquid Fuel

-

-

1.7 Country

-

1.7.1 Canada

-

1.7.2 United States

-

-

North America Satellite Manufacturing Market Size FAQs

How big is the North America Satellite Manufacturing Market?

The North America Satellite Manufacturing Market size is expected to reach USD 167.37 billion in 2024 and grow at a CAGR of 8.57% to reach USD 252.45 billion by 2029.

What is the current North America Satellite Manufacturing Market size?

In 2024, the North America Satellite Manufacturing Market size is expected to reach USD 167.37 billion.