Market Size of north america satellite launch vehicle Industry

| Icons | Lable | Value |

|---|---|---|

|

|

Study Period | 2017 - 2029 |

|

|

Market Size (2024) | USD 1.92 Billion |

|

|

Market Size (2029) | USD 5.04 Billion |

|

|

Largest Share by Orbit Class | LEO |

|

|

CAGR (2024 - 2029) | 21.29 % |

|

|

Largest Share by Country | United States |

|

|

Market Concentration | High |

Major Players |

||

|

|

||

|

*Disclaimer: Major Players sorted in no particular order |

North America Satellite Launch Vehicle Market Analysis

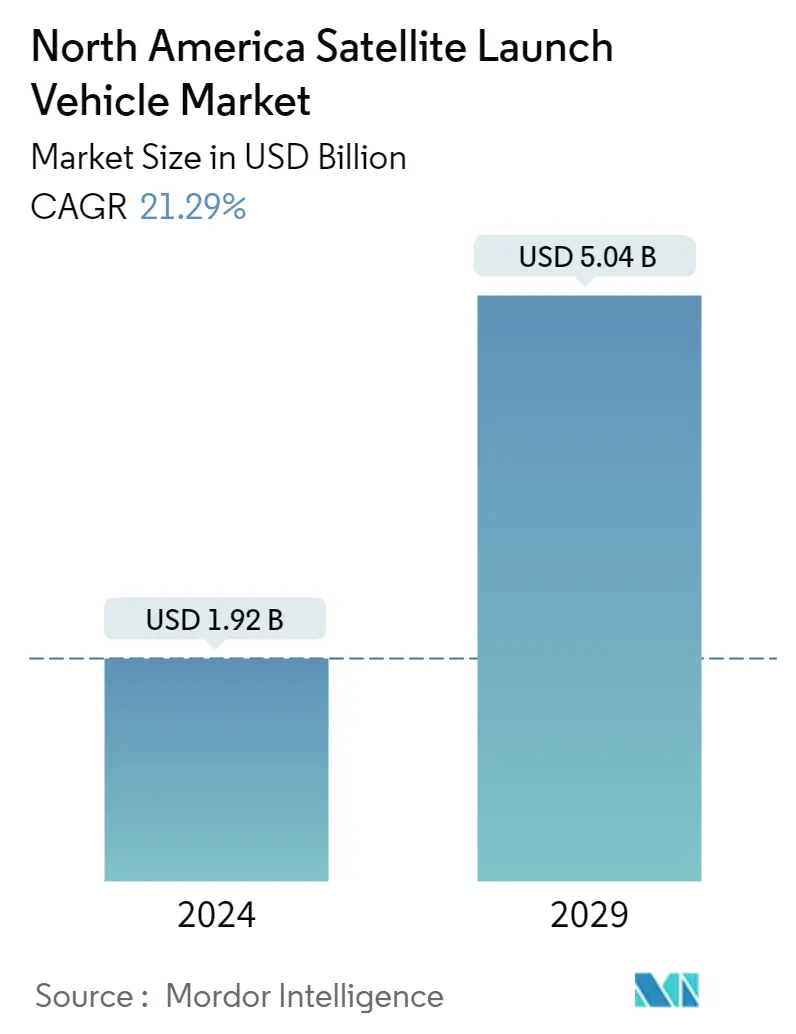

The North America Satellite Launch Vehicle Market size is estimated at USD 1.92 billion in 2024, and is expected to reach USD 5.04 billion by 2029, growing at a CAGR of 21.29% during the forecast period (2024-2029).

1.92 Billion

Market Size in 2024 (USD)

5.04 Billion

Market Size in 2029 (USD)

-2.82 %

CAGR (2017-2023)

21.29 %

CAGR (2024-2029)

Largest Market by Launch Vehicle MTOW

51.11 %

value share, Medium, 2022

The demand for medium launch vehicles is fueled by the granting of multi-year contracts by government and commercial end users to launch vehicle manufacturers and launch service providers.

Fastest-Growing Market by Orbit class

24.46 %

Projected CAGR, LEO, 2023-2029

Government initiatives pertaining to LEO satellites and their numerous uses, such as commercial communications, Earth observation, navigation, and military surveillance, will likely aid in the growth of LEO satellites.

Largest Market by Orbit Class

57.65 %

value share, LEO, 2022

LEO satellites are increasingly being adopted in modern communication technologies as they play an important role in Earth observation applications.

Leading Market Player

49.23 %

market share, Space Exploration Technologies Corp., 2022

SpaceX is the leading player in the North American satellite launch vehicle market and maintains its market share globally through its Starlink project. The company produces 120 satellites per month.

Second Leading Market Player

41.51 %

market share, United Launch Alliance, LLC., LLC.

United Launch Alliance is the second leading player in the market. The company emphasizes its track record of reliability and mission success. By consistently delivering successful launches, ULA instills confidence in its customers, which helps it maintain a strong market share.

Rising demand for orbital launch systems in the North American region has supplemented the growth

- At launch, a satellite or spacecraft is usually placed into one of many special orbits around the Earth, or it can be launched into an interplanetary journey. Satellites orbit the Earth at varying distances depending on their design and primary purpose. Each distance has its own benefits and challenges, including increased coverage and decreased energy efficiency. Satellites in the Medium Earth orbit include navigational and specialized satellites designed to monitor a specific area. Most scientific satellites, including NASA's Earth Observation System team, are in the low Earth orbit.

- Different satellites manufactured and launched from this region have different applications. For instance, during 2017-2022, out of the seven satellites launched in the MEO orbit, most were built for navigation/global positioning purposes. Similarly, out of the 32 satellites in the GEO orbit, most were deployed for communication and earth observation purposes. Around 3,000 LEO satellites launched were owned by North American organizations.

- The growing use of satellites in areas such as electronic intelligence, Earth science/meteorology, laser imaging, electronic intelligence, optical imaging, and meteorology is expected to drive demand for the North American satellite launch vehicle market, with LEO satellites expected to account for a major share. Between 2023 and 2029, the market is expected to surge by 213%.

Rising demand for low-cost launch systems driving the market

- The demand for low-cost launch systems capable of sending heavy satellites into high-altitude orbits several times a year is growing among governments and commercial organizations in North America. Due to the growing number of small satellite launches, including ride-hailing services on medium and heavy-duty launchers, as well as the growth of small launch capacities, launch prices have decreased Y-o-Y.

- In addition, the satellite manufacturing industry is driven by the demand for satellites for applications ranging from military surveillance, communications, and navigation to earth observation. As a result, the demand for satellites from the civilian/government, commercial, and military industries is increasing. During the historical period, a total of 4,351 satellites were launched in the region. The growth in the number of satellites launched from 2021 to 2022 was 61%, while the growth from 2021 to 2020 was 40%.

- Space agencies and private companies have been trying to reduce the costs of satellite launching systems over the past few years. Many market players have invested in the development of reusable launch systems to recover some or all the component stages. The market is dominated by only a few players due to their huge product offerings. Private companies such as SpaceX and Blue Origin are investing in space technology and driving innovation in the industry. Space organizations such as NASA have partnered with private players like SpaceX for the production and launch of satellites in this region. The market is expected to surge by 219% in the forecast period, and the United States is expected to be the largest country-wise market.

North America Satellite Launch Vehicle Industry Segmentation

GEO, LEO, MEO are covered as segments by Orbit Class. Heavy, Light, Medium are covered as segments by Launch Vehicle Mtow. United States are covered as segments by Country.

- At launch, a satellite or spacecraft is usually placed into one of many special orbits around the Earth, or it can be launched into an interplanetary journey. Satellites orbit the Earth at varying distances depending on their design and primary purpose. Each distance has its own benefits and challenges, including increased coverage and decreased energy efficiency. Satellites in the Medium Earth orbit include navigational and specialized satellites designed to monitor a specific area. Most scientific satellites, including NASA's Earth Observation System team, are in the low Earth orbit.

- Different satellites manufactured and launched from this region have different applications. For instance, during 2017-2022, out of the seven satellites launched in the MEO orbit, most were built for navigation/global positioning purposes. Similarly, out of the 32 satellites in the GEO orbit, most were deployed for communication and earth observation purposes. Around 3,000 LEO satellites launched were owned by North American organizations.

- The growing use of satellites in areas such as electronic intelligence, Earth science/meteorology, laser imaging, electronic intelligence, optical imaging, and meteorology is expected to drive demand for the North American satellite launch vehicle market, with LEO satellites expected to account for a major share. Between 2023 and 2029, the market is expected to surge by 213%.

| Orbit Class | |

| GEO | |

| LEO | |

| MEO |

| Launch Vehicle Mtow | |

| Heavy | |

| Light | |

| Medium |

| Country | |

| United States |

North America Satellite Launch Vehicle Market Size Summary

The North America Satellite Launch Vehicle Market is poised for significant growth, driven by the increasing demand for satellite launches across various sectors, including government, commercial, and military applications. The market is characterized by a surge in the number of satellites launched, with a notable focus on low Earth orbit (LEO) satellites, which are primarily used for electronic intelligence, Earth science, and communication purposes. The region's market dynamics are influenced by the growing interest in commercial space exploration and the need for cost-effective, reliable launch services. This has led to substantial investments in innovative technologies, such as reusable launch systems, which aim to reduce launch costs and enhance operational efficiency. The market is dominated by a few key players, including SpaceX, Blue Origin, and United Launch Alliance, who are at the forefront of driving technological advancements and expanding their launch capabilities.

The market's expansion is further supported by significant government and private sector investments in space programs and research initiatives. North America, particularly the United States, leads in government expenditure on space, with substantial funding allocated to develop advanced launch vehicles and support space exploration missions. The collaboration between government agencies like NASA and private companies has been instrumental in advancing the region's space capabilities. The market's consolidation is evident, with major companies holding a significant share, reflecting their extensive product offerings and strategic partnerships. As the demand for satellite launch vehicles continues to rise, the North American market is expected to experience robust growth, positioning it as a key player in the global space industry.

North America Satellite Launch Vehicle Market Size - Table of Contents

-

1. MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2029 and analysis of growth prospects)

-

1.1 Orbit Class

-

1.1.1 GEO

-

1.1.2 LEO

-

1.1.3 MEO

-

-

1.2 Launch Vehicle Mtow

-

1.2.1 Heavy

-

1.2.2 Light

-

1.2.3 Medium

-

-

1.3 Country

-

1.3.1 United States

-

-

North America Satellite Launch Vehicle Market Size FAQs

How big is the North America Satellite Launch Vehicle Market?

The North America Satellite Launch Vehicle Market size is expected to reach USD 1.92 billion in 2024 and grow at a CAGR of 21.29% to reach USD 5.04 billion by 2029.

What is the current North America Satellite Launch Vehicle Market size?

In 2024, the North America Satellite Launch Vehicle Market size is expected to reach USD 1.92 billion.