Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

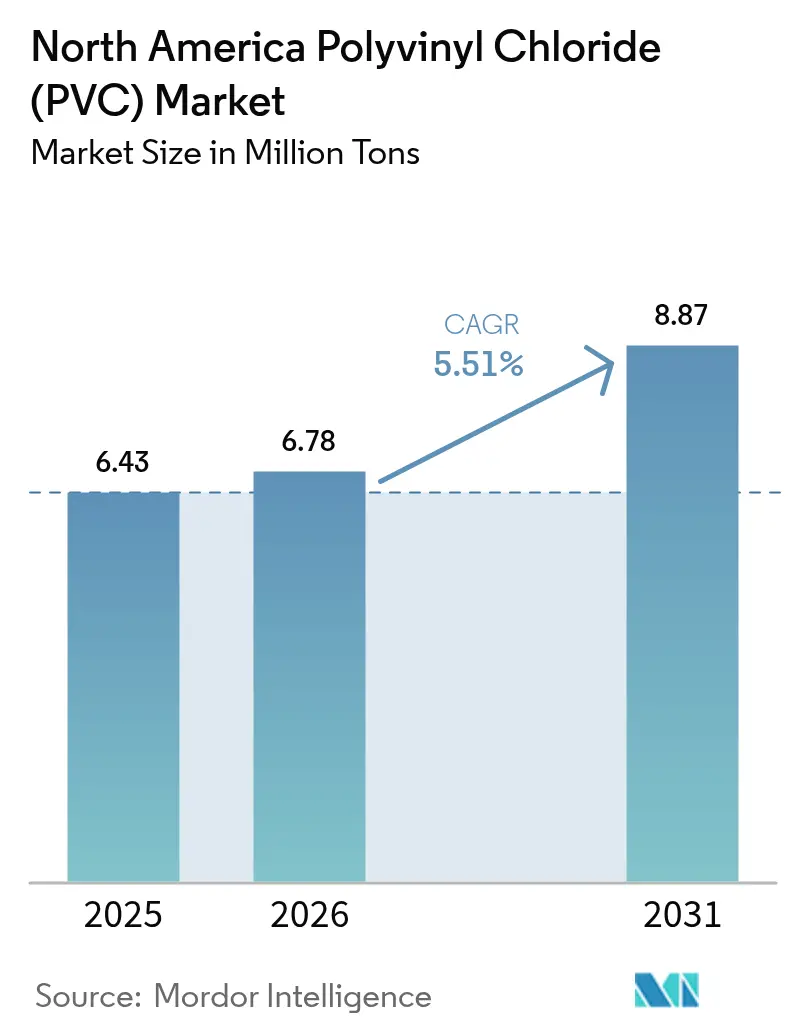

| Base Year Market Size (2025) | 6.43 Million tons |

| Market Volume (2026) | 6.78 Million tons |

| Market Volume (2031) | 8.87 Million tons |

| Growth Rate (2026 - 2031) | 5.51% CAGR |

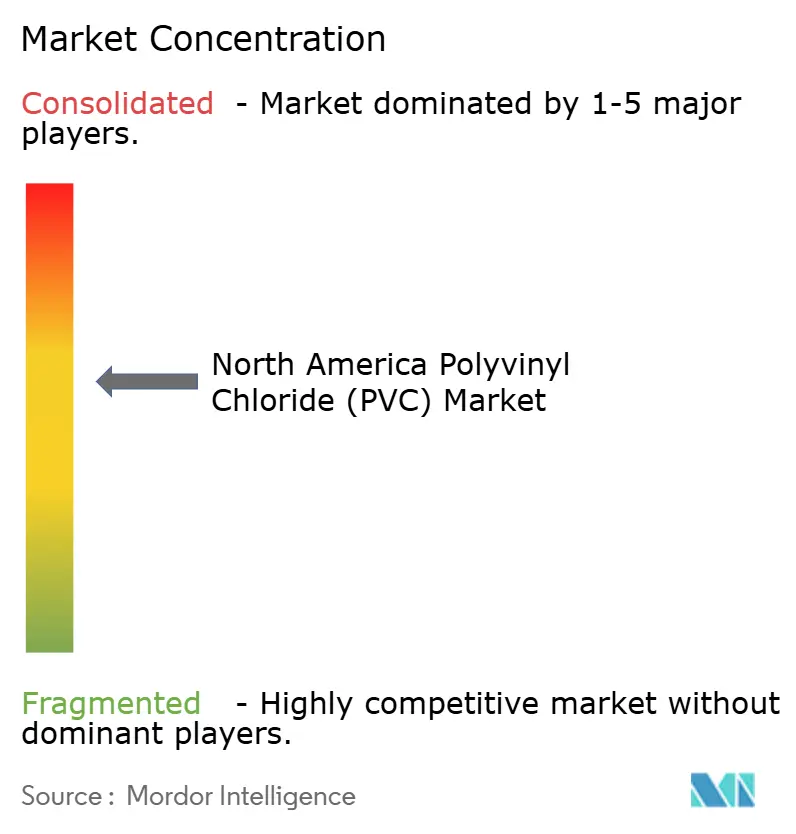

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Polyvinyl Chloride (PVC) Market Analysis by Mordor Intelligence

The North America Polyvinyl Chloride Market size is projected to expand from 6.43 Million tons in 2025 and 6.78 Million tons in 2026 to 8.87 Million tons by 2031, registering a CAGR of 5.51% between 2026 to 2031. Federal infrastructure funding, healthcare-related reshoring, and the adoption of bio-based plasticizers are jointly lifting demand even as environmental activism challenges chlorinated polymers. Government allocations for lead service-line replacement are pulling rigid pipe through procurement cycles that run at least until 2029, while FDA guidance on medical-grade polymers is unlocking premium tiers of flexible PVC. The United States' demand dominates because its municipal water networks and medical-device hubs dwarf regional peers. Producers with vertically integrated assets and AI-driven process control are trimming energy intensity, securing carbon-credit upside in California, and positioning for corporate sustainability mandates.

Key Report Takeaways

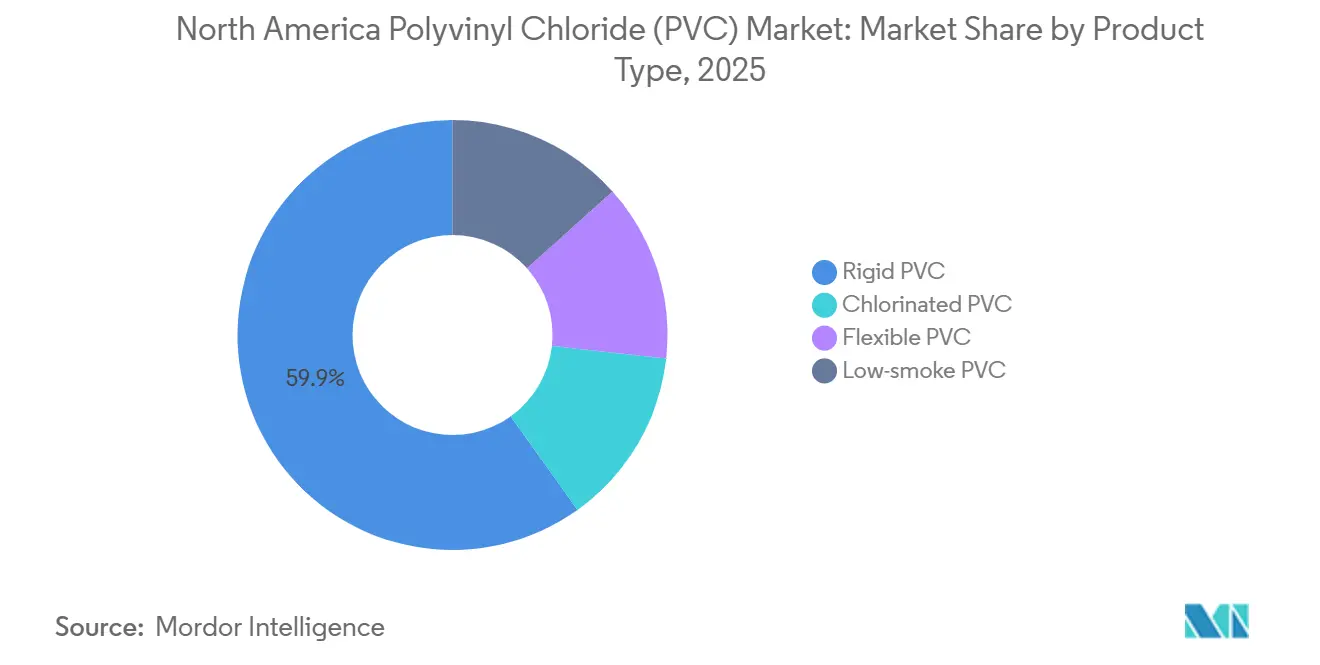

- By product type, rigid PVC led with 59.88% of the polyvinyl chloride market share in 2025, while flexible PVC is forecast to grow at a 5.82% CAGR through 2031.

- By application, Pipes and Fittings led with 45.71% of the polyvinyl chloride market share in 2025, while Profiles, Hoses, and Tubing are forecast to grow at a 5.63% CAGR through 2031.

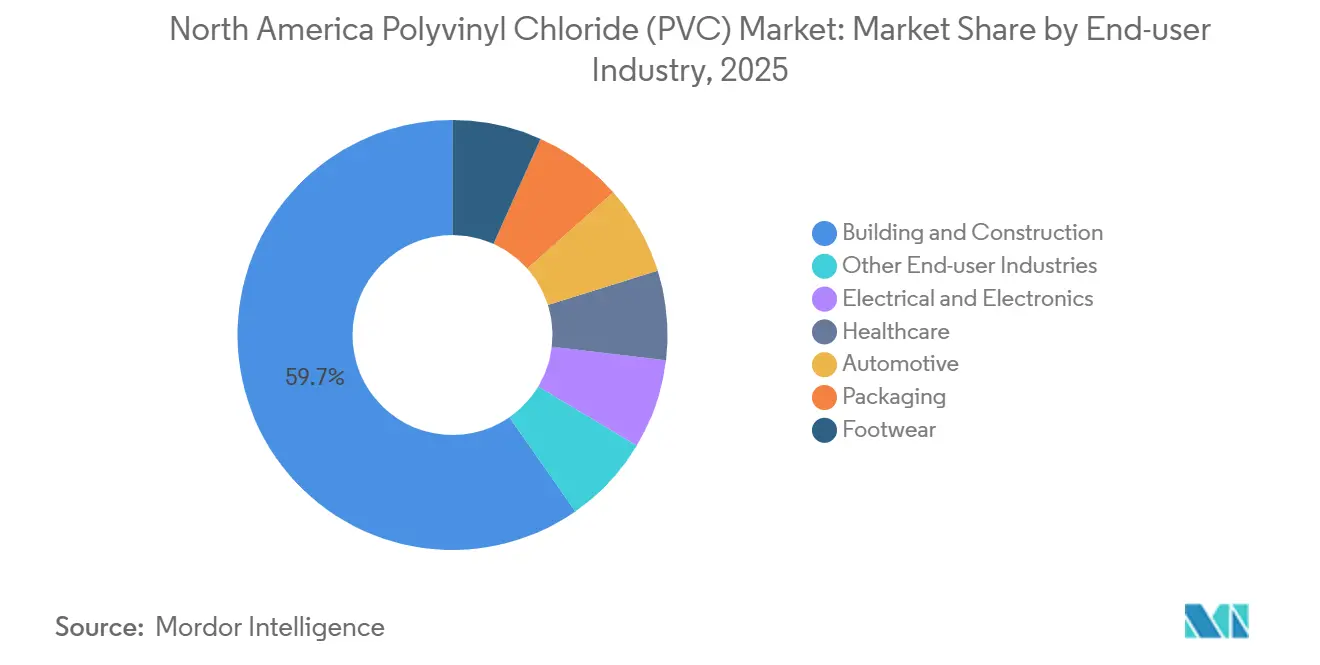

- By end-user industry, building and construction commanded 59.66% of the polyvinyl chloride market share in 2025, while healthcare is projected to advance at a 6.12% CAGR to 2031.

- By geography, the United States accounted for 77.92% of the polyvinyl chloride market share in 2025 and is poised for a 5.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Polyvinyl Chloride (PVC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging use in medical-grade devices and IV bags | +1.2% | United States, with concentration in Midwest and Southeast manufacturing hubs | Medium term (2-4 years) |

| Federal funding for replacement water infrastructure | +1.8% | United States, particularly states with aging municipal systems (Michigan, Pennsylvania, Ohio) | Long term (≥ 4 years) |

| Regulatory tailwinds for lead-free plumbing | +0.9% | United States and Canada, driven by EPA and Health Canada mandates | Medium term (2-4 years) |

| Bio-based plasticizers unlocking premium niches | +0.7% | North America, with early adoption in consumer-facing packaging and medical applications | Short term (≤ 2 years) |

| AI-optimized PVC production lowering carbon intensity | +0.5% | United States and Canada, concentrated in facilities with digital infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Use in Medical-Grade Devices and IV Bags

Healthcare’s pivot toward single-use disposables is reshoring flexible PVC that had migrated offshore during the 2010s. The medical plastics segment reached USD 577.66 billion in 2024 and will grow 10.2% annually to 2030, with PVC specified for IV units, tubing, blood bags, and syringes. FDA guidance issued in 2024 triggered investments in ultra-clean resin lines that meet ISO 10993, creating a domestic premium tier that commands 15-20% price uplifts[1]U.S. Food and Drug Administration, “Medical Device Supply Chain Resilience,” fda.gov. These volumes decouple healthcare PVC from housing cycles, sustaining demand even when residential starts dip. An aging population and chronic disease prevalence keep dialysis equipment and infusion sets on a steady growth curve. CPSC reaffirmation of phthalate limits in 2024 accelerated the switch to bio-based plasticizers in pediatric devices, reinforcing the segment’s premium positioning.

Federal Funding for Replacement Water Infrastructure

The EPA earmarked USD 15 billion under the Bipartisan Infrastructure Law for lead service-line replacement, with another USD 35 billion flowing through the Drinking Water State Revolving Fund. States with large inventories of lead pipe face statutory obligation windows, compressing procurement cycles and elevating suppliers holding NSF/ANSI 14 certifications. PVC pipe averages 30–40% lower cost per linear foot than ductile iron, making it the default choice for cash-constrained utilities. Regional demand spikes in Michigan, Ohio, and Pennsylvania favor producers with nearby capacity. While polyethylene advocates court regulators, PVC’s entrenched qualification base preserves share for the forecast horizon.

Regulatory Tailwinds for Lead-Free Plumbing

The EPA’s Lead and Copper Rule Improvements and Health Canada’s 2025 Plumbing Fittings Regulation cut allowable lead content in wetted surfaces to 0.25%. Because PVC is inherently lead-free, specifiers avoid the compliance risk present with metallic alternatives. LEED v4.1 and the WELL Building Standard now award points for lead-free plumbing, reinforcing uptake in commercial construction. In states like California and New York, where green-building incentives stack on federal mandates, PVC’s regulatory advantage widens. Municipalities pursuing accelerated replacement schedules further cement PVC’s positioning in potable-water systems.

Bio-Based Plasticizers Unlocking Premium Niches

Vegetable oil and citrate-derived plasticizers fetch 20–30% premiums but gain share wherever “phthalate-free” claims support brand positioning. The CPSC bans eight phthalates in children’s products, and the FDA is reevaluating DEHP in medical devices, guiding converters toward bio-based alternatives. Early adopters are resolving migration and low-temperature flexibility issues, opening avenues in medical tubing, food-contact films, and premium flooring. Long-term feedstock contracts with agricultural suppliers hedge volatility, allowing formulators to protect margins while marketing sustainability credentials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying environmental and health scrutiny | -0.8% | North America, with intensity in California, New York, and Canadian provinces | Medium term (2-4 years) |

| Tightening limits on phthalate plasticizers | -0.6% | United States and Canada, driven by CPSC and Health Canada regulations | Short term (≤ 2 years) |

| Upcoming PFAS-style scrutiny on chlorinated polymers | -0.5% | United States, with potential spill-over to Canada and Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying Environmental and Health Scrutiny

Activist campaigns have persuaded several California water districts to adopt “PVC-free” policies despite decades of safe service and NSF certification[2]National Sanitation Foundation, “NSF/ANSI 14: Plastics Piping System Components,” nsf.org . Media focus on microplastics in drinking water and “forever chemical” narratives blur distinctions between PVC and PFAS, swaying procurement in politically sensitive regions. Automotive OEMs in Europe are specifying halogen-free wire insulation to meet End-of-Life Vehicle mandates, and North American plants on global platforms are following suit. Reputational risk, rather than technical deficiency, is steering some bids toward polyethylene, forcing PVC advocates to amplify lifecycle-assessment data.

Tightening Limits on Phthalate Plasticizers

The CPSC’s 2024 prohibition of eight phthalates and the FDA’s ongoing DEHP risk review require costly reformulation of legacy flexible PVC. Smaller converters lacking R&D bandwidth face margin compression or market exit, consolidating share with vertically integrated majors. EPA TSCA evaluations flag unreasonable occupational exposure risks for DIDP and DINP, foreshadowing additional curbs. Investor caution surrounding potential phase-outs is delaying capital additions in flexible-PVC capacity, tempering near-term expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rigid Dominance Masks Flexible’s Healthcare Surge

Rigid PVC captured 59.88% of 2025 tonnage, anchoring the polyvinyl chloride market in water pipe, conduit, and window profiles. Flexible PVC, however, is poised for a 5.82% CAGR to 2031 on the strength of medical disposables and phthalate-compliant formulations. Within the polyvinyl chloride market size, clear rigid grades serve pressure pipe certified under NSF/ANSI 14, while non-clear rigid dominates DWV and conduit.

Flexible PVC’s higher growth rate reflects its compatibility with bio-based plasticizers and premium healthcare niches. Clear flexible grades are standard in IV bags and transparent tubing that require fluid-flow visibility. Non-clear flexible remains integral in wire jacketing and industrial hoses, and low-smoke PVC grades are mandated for tunnels and high-rise applications under NFPA 262. CPVC extends into hot-water distribution where 200 °F ratings eclipse standard PVC. Diversified producers spanning rigid and flexible variants are best placed to capture the polyvinyl chloride market’s bifurcating opportunity set.

By Application: Pipes Anchor Volume, Profiles Capture Growth

Pipes and fittings accounted for 45.71% of 2025 consumption, anchoring the polyvinyl chloride market share on infrastructure programs. Profiles, hoses, and tubing will grow at a 5.63% CAGR through 2031, paced by window-frame retrofits, industrial hoses, and medical tubing. Films and sheets retain relevance in medical drapes and geomembranes despite substitution to polyolefins in commodity packaging.

Wire and cable demand bifurcates between commodity building wire and specialty automotive harnesses. Bottles now occupy niche chemical-packaging slots after mainstream beverage migration to PET and HDPE. Short-cycle applications such as profiles and hoses deliver faster asset turns and margin potential than long-cycle pipe, yet they expose converters to economic swings.

By End-user Industry: Construction’s Scale, Healthcare’s Velocity

Building and construction used 59.66% of 2025 tonnage, leveraging PVC’s 30–40% cost advantage over copper and ductile iron. LEED v4.1 credits for lead-free systems and recycled content reinforce the specification. However, cyclical housing and interest-rate sensitivity cap upside. Healthcare volumes will grow at a 6.12% CAGR through 2031, making it the fastest-expanding end-user industry within the polyvinyl chloride market.

Medical-grade PVC earns 15–20% premiums, and FDA supply-chain guidance spurs investment in ISO 10993-compliant lines. Electrical and electronics rely on PVC conduit and junction boxes but face halogen-free substitution in data centers and EVs. Automotive volumes rise in wire harnesses yet risk displacement by cross-linked polyethylene. Packaging, footwear, and other outlets hold residual shares, with vinyl footwear thriving in abrasion-resistant niches.

Geography Analysis

The United States controlled 77.92% of 2025 volume and will grow at a 5.93% CAGR through 2031, underpinned by its vast municipal water networks and medical-device clusters. EPA infrastructure grants funnel disproportionately to Midwest states, rewarding producers with proximate assets. Vertical integration, from chlor-alkali to compounding, creates switching costs that insulate U.S. suppliers from low-priced imports.

Canada’s smaller population constrains absolute tonnage, yet regulatory alignment with U.S. standards eases cross-border trade. Health Canada’s 0.25% lead limit for plumbing fittings harmonizes with EPA rules, enabling producers to leverage common product listings. The country’s demand centers on renovation of older housing stock and municipal pipe replacements in Ontario and Quebec.

Mexico benefits from USMCA tariff-shift provisions that make cross-border supply chains attractive for commodity rigid pipe. Domestic capacity has inched upward, but the nation remains a net PVC importer serving local construction and automotive plants. Producers operating on both sides of the border can arbitrage labor and energy cost differentials while meeting U.S. compliance demands for medical-grade imports.

Competitive Landscape

Five producers, Westlake, Formosa Plastics, Orbia, Shin-Etsu, and Occidental, hold about 60–65% of regional capacity, indicating moderate concentration. Capacity expansions continue: Westlake’s Lake Charles build-out added 250,000 t/y in 2024, trimming freight for Gulf Coast converters. INEOS upgraded Chocolate Bayou with machine-learning controls that cut energy use 10%, lowering Scope 1 emissions by 25,000 t/y.

Formosa secured a 10-year, USD 300 million contract with a Midwestern water utility, reflecting the value of NSF-certified pipe and established distributor networks. Shin-Etsu partnered on bio-plasticizer compounds to penetrate phthalate-free healthcare niches. Orbia’s low-smoke PVC addresses data-center cable codes, while Braskem’s Brazilian expansion targets North American imports.

AI-driven process optimization is emerging as a quiet differentiator, improving yields and reducing off-spec volumes. Yet disclosures are scarce, suggesting strategic sensitivity. The Vinyl Institute’s lifecycle-assessment tools help counter environmental scrutiny, but adoption varies. Substitution threats, polyethylene in water pipe, halogen-free compounds in automotive, define the competitive frontier more than new PVC entrants.

North America Polyvinyl Chloride (PVC) Industry Leaders

Westlake Corporation

Shin-Etsu Chemical Co., Ltd.

Formosa Plastics Corporation

Occidental Petroleum Corporation

Orbia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The Vinyl Institute, representing U.S. manufacturers of polyvinyl chloride (PVC) resin, welcomed a new trade framework between the United States and India. The agreement aimed to reduce or eliminate tariffs and non-tariff barriers, promoting increased U.S. exports of PVC to one of the world's fastest-growing markets.

- December 2025: Westlake Corporation announced the closure of its polyvinyl chloride (PVC) plant in Aberdeen, Mississippi, which had an annual production capacity of approximately 1 billion pounds of suspension PVC resin. The company continued to supply PVC products from its seven other chlorovinyl facilities in North America.

North America Polyvinyl Chloride (PVC) Market Report Scope

Polyvinyl chloride (PVC or vinyl) is a widely used, versatile, and cost-effective thermoplastic polymer. It is primarily derived from salt and oil/gas and is known for its durability, lightweight nature, fire resistance, and chemical stability. These properties make it suitable for applications such as pipes, window frames, medical devices, and cable insulation.

The North America polyvinyl chloride (PVC) market is segmented by product type, application, and geography. By product type, the market is segmented into rigid PVC, flexible PVC, low-smoke PVC, and chlorinated PVC. The rigid PVC is further segmented into clear rigid PVC and non-clear rigid PVC. The flexible PVC is further segmented into clear flexible PVC and non-clear flexible PVC. By application, the market is segmented into pipes and fittings, films and sheets, wires and cables, bottles, profiles, hoses and tubing, and other applications. The report also covers the market size and forecasts for polyvinyl chloride (PVC) in 3 countries across the region. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

By Product Type

| Rigid PVC | Clear Rigid PVC |

| Non-clear Rigid PVC | |

| Flexible PVC | Clear Flexible PVC |

| Non-clear Flexible PVC | |

| Low-smoke PVC | |

| Chlorinated PVC |

By Application

| Pipes and Fittings |

| Films and Sheets |

| Wires and Cables |

| Bottles |

| Profiles, Hoses and Tubing |

| Other Applications |

By End-user Industry

| Building and Construction |

| Electrical and Electronics |

| Healthcare |

| Automotive |

| Packaging |

| Footwear |

| Other End-user Industries |

By Country

| United States |

| Canada |

| Mexico |

| By Product Type | Rigid PVC | Clear Rigid PVC |

| Non-clear Rigid PVC | ||

| Flexible PVC | Clear Flexible PVC | |

| Non-clear Flexible PVC | ||

| Low-smoke PVC | ||

| Chlorinated PVC | ||

| By Application | Pipes and Fittings | |

| Films and Sheets | ||

| Wires and Cables | ||

| Bottles | ||

| Profiles, Hoses and Tubing | ||

| Other Applications | ||

| By End-user Industry | Building and Construction | |

| Electrical and Electronics | ||

| Healthcare | ||

| Automotive | ||

| Packaging | ||

| Footwear | ||

| Other End-user Industries | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

What is the size of the North America Polyvinyl Chloride (PVC) market?

The North America Polyvinyl Chloride (PVC) market size stands at 6.78 million tons in 2026 and is forecast to reach 8.87 million tons by 2031, growing at a 5.51% CAGR from 2026.

Which PVC product type is expanding fastest through 2031?

Flexible PVC is projected to rise at a 5.82% CAGR through 2031, fueled by healthcare tubing and phthalate-free formulations.

What drives PVC pipe demand in the United States?

USD 15 billion in federal funds for lead service-line replacement and 30–40% cost savings over ductile iron keep rigid PVC pipe at the center of municipal procurement.

Why is healthcare a strategic segment for PVC suppliers?

Medical-grade PVC commands 15–20% price premiums and grows 6.12% through 2031due to an aging population and supply-chain reshoring incentives.

Page last updated on: