Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

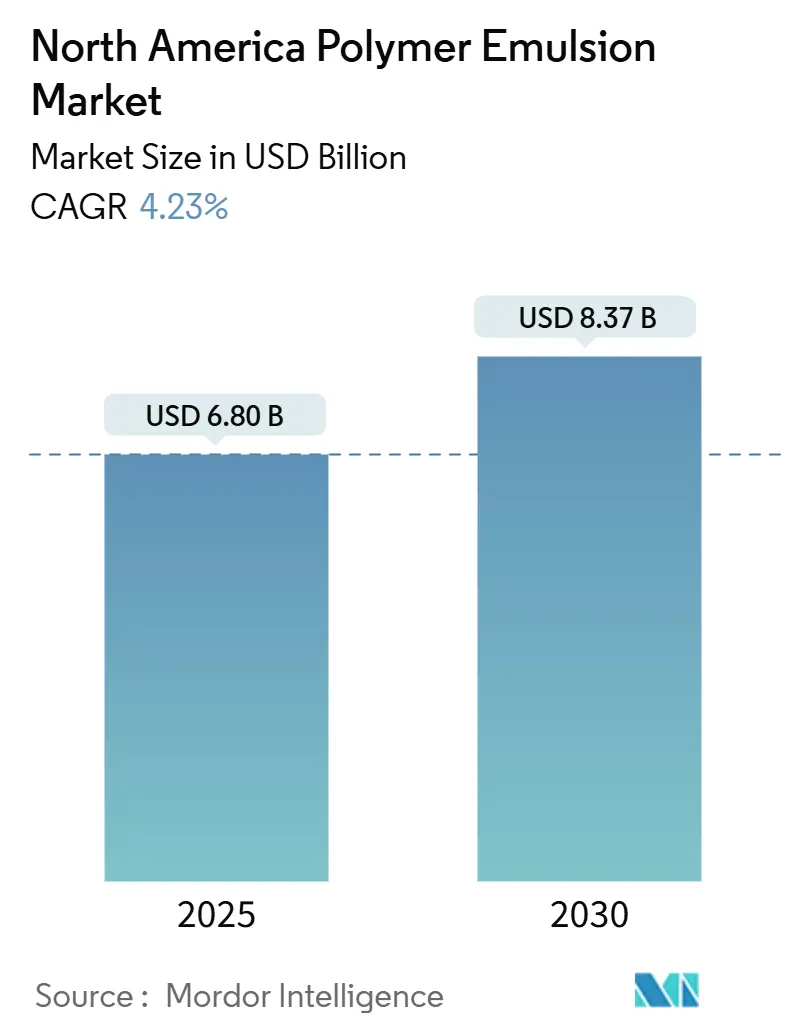

| Market Size (2025) | USD 6.80 Billion |

| Market Size (2030) | USD 8.37 Billion |

| Growth Rate (2025 - 2030) | 4.23% CAGR |

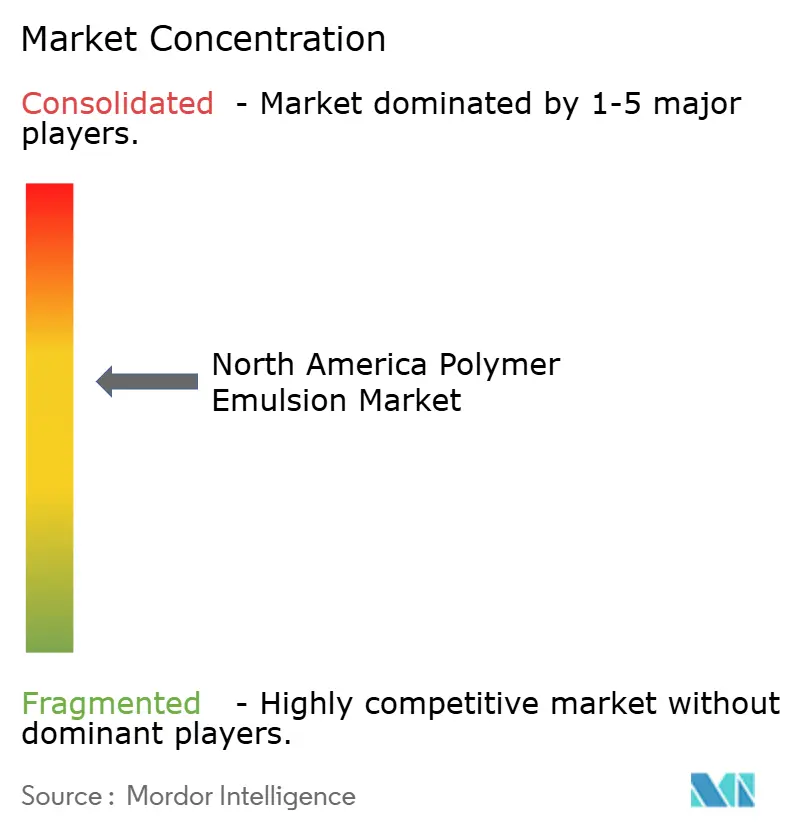

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Polymer Emulsion Market Analysis by Mordor Intelligence

The North America Polymer Emulsion Market size is estimated at USD 6.80 billion in 2025, and is expected to reach USD 8.37 billion by 2030, at a CAGR of 4.23% during the forecast period (2025-2030). Heightened sustainability mandates, infrastructure-related outlays, and steady residential maintenance cycles provide enduring volume support while pushing formulators toward water-borne systems. Tightening VOC thresholds, most notably California’s 50 g/l limit for select architectural coatings, accelerate the shift away from solvent-borne chemistries. Raw-material volatility and PFAS phase-outs create margin pressure but simultaneously trigger rapid innovation in bio-based acrylics and silicone-enabled additives. Against this backdrop, multinational producers scale up specialty dispersions, and mid-tier suppliers pursue capacity debottlenecking to serve premium packaging, automotive interiors, and infrastructure-grade admixture niches.

Key Report Takeaways

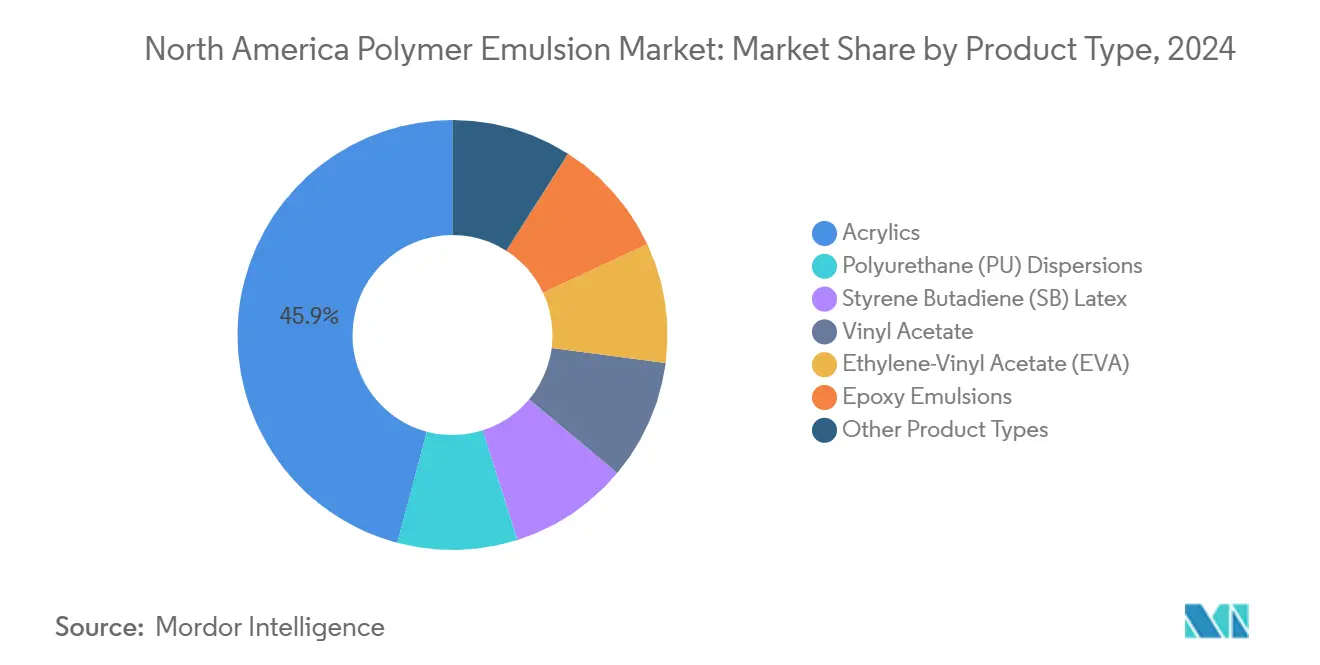

- By product type, acrylics led with 45.84% of the North America polymer emulsion market share in 2024, whereas polyurethane (PU) dispersions are projected to post the fastest 4.81% CAGR through 2030.

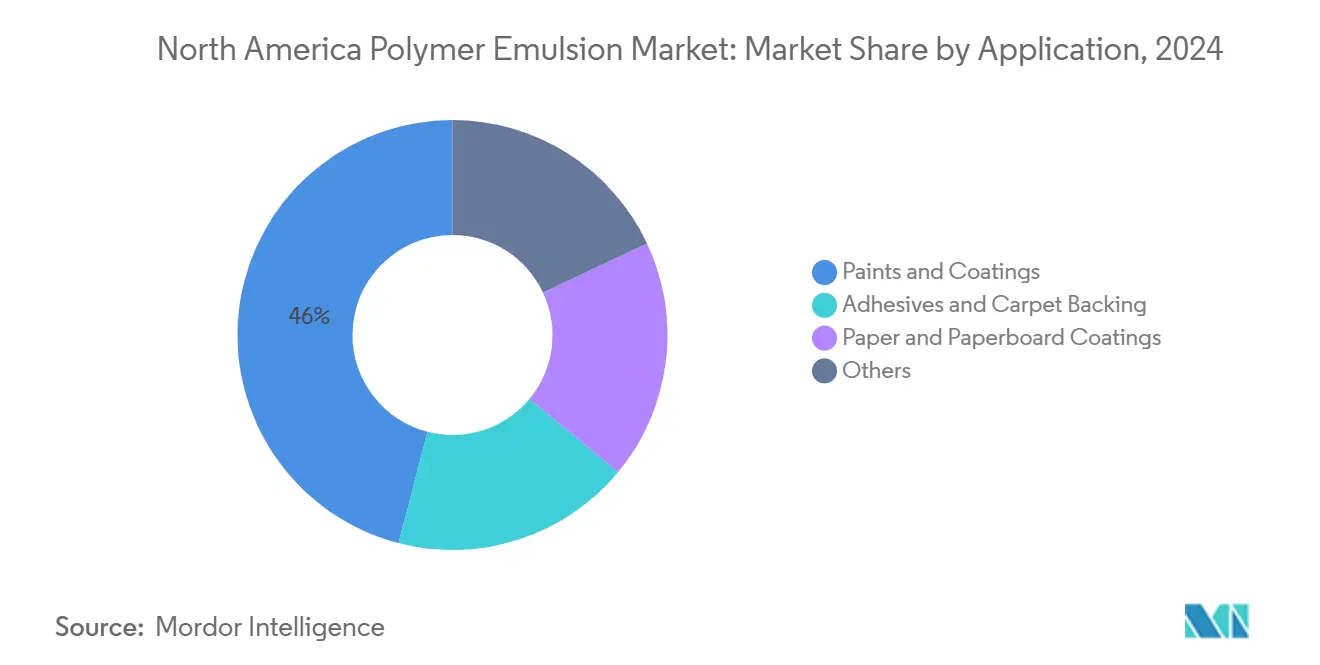

- By application, paints and coatings accounted for 45.95% of demand in 2024, while adhesives and carpet backing are set to expand at a 4.60% CAGR to 2030.

- By geography, the United States held 83.06% revenue stake in 2024 and is poised to grow at a 4.26% CAGR through 2030.

North America Polymer Emulsion Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward low-VOC water-borne systems | +1.2% | California, Northeast U.S. | Medium term (2-4 years) |

| Housing-led repaint demand | +0.8% | U.S. Sunbelt, Canadian urban cores | Short term (≤ 2 years) |

| Infrastructure-grade latex admixtures uptake | +0.7% | United States; spillover to Canada, Mexico | Long term (≥ 4 years) |

| E-commerce packaging adhesives boom | +0.6% | Logistics corridors across North America | Medium term (2-4 years) |

| Bio-based latex in premium architectural work | +0.4% | United States and Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Low-VOC Water-Borne Systems

Stringent emission limits give water-borne dispersions a structural cost-of-compliance advantage over legacy solvent technologies. California’s 50 g/l VOC cap and parallel Canadian rules constrain formulators, pushing demand toward acrylic lattices and next-generation bio-acrylates with 40% certified renewable content that also cut cradle-to-gate carbon footprints by 30%[1]California Air Resources Board, “VOC Limits,” arb.ca.gov. Industrial coaters cite easier cleanup and safer indoor application as further incentives, ensuring the driver’s impact persists through at least mid-decade.

Housing-Led Repaint Demand in U.S. and Canada

Aging housing stock creates a maintenance cycle unlinked to new-build volatility. Sherwin-Williams raised domestic architectural coating prices by 5% in 2024 and still logged volume gains, underscoring end-market elasticity. North American single-family starts are set to rise another 5% in 2025, but repaint jobs—where higher-performance emulsions command premium pricing—drive the bulk of incremental gallons, especially in cold-climate provinces where freeze-thaw durability is prized.

Infrastructure-Grade Latex Admixtures Uptake

Federal stimulus channeled through the Infrastructure Investment and Jobs Act funded more than 56,000 transportation projects, lifting U.S. highway construction spending to USD 126 billion in 2024. Polymer-modified admixtures enhance asphalt crack resistance and concrete flexural strength, positioning latex suppliers for multi-year volume visibility. Sika’s construction chemicals unit already posted 12.8% sales growth on the back of these specifications.

Bio-Based Latex in Premium Architectural Coatings

Green-building certifications such as LEED reward lower-carbon materials, spurring demand for soy-based or CO₂-utilizing dispersions that emulate alkyd gloss while offering water cleanup. Celanese and partner mortar brands now integrate captured carbon into polymer backbones, creating marketable environmental product declarations and opening margin-rich specification channels in high-profile commercial builds.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile butadiene feedstock pricing | -0.9% | U.S. Gulf Coast; styrene-butadiene users | Short term (≤ 2 years) |

| Competition from powder and high-solids resins | -0.6% | U.S. Midwest, Canadian Prairies | Medium term (2-4 years) |

| Impending PFAS-linked additive restrictions | -0.4% | California, New York, New England | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from Powder and High-Solids Resins

In appliance and metal-furniture lines, powder coatings offer zero-VOC quick-cure benefits, siphoning share from water-borne enamels. Wacker Chemie’s polymer division logged a 7% sales dip in 2024 despite higher volumes, underscoring price pressure as customers weigh total applied cost savings from powder and high-solids alternatives.

Impending PFAS-Linked Additive Restrictions

California’s finalized rulemaking eliminates key PFAS surfactants by 2026, compelling formulators to re-optimize stability packages. Leading producers have already pledged total PFAS exit by 2025, but smaller toll manufacturers may lack research and development bandwidth, limiting near-term supply flexibility.

Segment Analysis

By Product Type: Acrylic Scale Meets PU Agility

Acrylics captured 45.84% of the North America polymer emulsion market share in 2024, reflecting balanced cost-performance and broad formulation latitude across decorative and light-industrial categories. Although pricing remains sensitive to acrylate monomer swings, scale economies and abundant supplier competition stabilize margins for top-tier producers. The segment’s mid-single-digit growth benefits from VOC compliance tailwinds and continuous tint base innovations that improve hide at lower film thickness.

Polyurethane dispersions represent the fastest-growing slice at a 4.81% CAGR, supported by rising demand for abrasion-resistant automotive interiors and flexible food wraps. High elongation and chemical-resistance profiles enable formulators to displace PVC plastisols in premium seat-cover substrates, while low-temperature heat-seal grades meet e-commerce packaging throughput targets. As capacity additions in North Carolina and the U.S. Midwest come online, the PU segment’s contribution to the North America polymer emulsion market size is forecast to widen steadily.

Note: Segment shares of all individual segments available upon report purchase

By Application: Coatings Anchor, Adhesives Accelerate

Paints and coatings consumed 45.95% of total polymer emulsions in 2024, securing a resilient demand floor for bulk acrylic and vinyl acetate grades. Repaint cycles, weather-resistant topcoats for infrastructure, and OEM refinish channels render coatings a dependable cash-flow engine, allowing suppliers to fund specialty dispersion research and development. Architectural brands emphasize washability and early-rain resistance, elevating opportunity for higher-solids binder platforms that preserve open time without cosolvent addition.

Adhesives and carpet backing form the fastest-moving application cohort, expanding at a projected 4.60% CAGR through 2030. Corrugators prefer water-borne lattices over starch to meet moisture-resistance test protocols of digitally printed boxes destined for grocery and meal-kit fulfilment. Carpet mills upgrade to low-odor SBR-acrylic hybrids capable of hot-water extraction stability, a requisite for premium hospitality specifications. Paper and paperboard coatings leverage latex to close porosity gaps, and the starch-to-latex ratio in blade coaters continues to inch upward, underpinning steady binder lifts even in flat publication-paper tonnage environments.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

The United States accounted for 83.06% of the North America polymer emulsion market size in 2024, underpinned by a USD 126 billion highway spend and 5% price hikes that paint manufacturers successfully passed through without demand erosion. Lubrizol’s USD 20 million acrylic expansion in North Carolina and BASF’s Louisiana MDI upgrade attest to the country’s ongoing reinvestment cycle in downstream water-borne technologies.

Canada presents a smaller yet stable market, benefiting from regulations mirroring U.S. VOC limits and consistent renovation activity in Ontario and British Columbia. Federal retrofit incentives stimulate uptake of weather-capable exterior latexes, supporting mid-single-digit dispersion growth. While Dow postponed its Path2Zero ethylene project, local paint makers rely on cross-border feedstock flows, highlighting the integrative nature of the regional supply chain[2]Chemical & Engineering News, “Dow Plans Deep Cuts Amid Poor Economy,” cen.acs.org.

Mexico contributes incremental momentum as industrial coating, appliance, and automotive plants seek locally sourced coil-coating resins. AkzoNobel’s 35% capacity uplift in García underscores the near-shoring trend that positions Mexico as a manufacturing bridge between U.S. consumers and Latin American growth corridors.

Competitive Landscape

The North America polymer emulsion market is moderately fragmented. BASF, Dow, and Arkema exploit backward integration into monomers, enabling rapid formulation pivots when raw-material spreads widen. Scale allows these leaders to absorb compliance costs tied to PFAS exit and renewable feedstock adoption, then cascade learnings across global sites. Raw-material volatility and sustainability premiums spur deal activity. Arkema divested non-core solvent assets to bankroll bio-acrylate scale-up, while propylene tightness may accelerate alliances between monomer suppliers and downstream dispersers.

North America Polymer Emulsion Industry Leaders

Arkema

BASF

Celanese Corporation

Wacker Chemie AG

Dow

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Trinseo instituted a USD 0.04/dry lb price increase for styrene-butadiene latex supplied to North American carpet markets, citing higher feedstock and freight costs.

- January 2025: Lubrizol completed a USD 20 million upgrade at its Gastonia, North Carolina site to expand acrylic emulsion capacity and advance next-generation resin technologies for coatings applications.

North America Polymer Emulsion Market Report Scope

The North America polymer emulsion market report includes:

By Product Type

| Acrylics |

| Polyurethane (PU) Dispersions |

| Styrene Butadiene (SB) Latex |

| Vinyl Acetate |

| Ethylene-Vinyl Acetate (EVA) |

| Epoxy Emulsions |

| Other Product Types |

By Application

| Adhesives and Carpet Backing |

| Paper and Paperboard Coatings |

| Paints and Coatings |

| Others |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Acrylics |

| Polyurethane (PU) Dispersions | |

| Styrene Butadiene (SB) Latex | |

| Vinyl Acetate | |

| Ethylene-Vinyl Acetate (EVA) | |

| Epoxy Emulsions | |

| Other Product Types | |

| By Application | Adhesives and Carpet Backing |

| Paper and Paperboard Coatings | |

| Paints and Coatings | |

| Others | |

| By Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

How large is the North America polymer emulsion market in 2025?

It stands at USD 6.80 billion, with a forecast to reach USD 8.37 billion by 2030.

Which product category holds the biggest slice of regional demand?

Acrylic emulsions lead, capturing 45.84% of 2024 sales thanks to broad architectural and industrial use.

What is the main growth driver through 2030?

Stricter VOC regulations, especially in California, accelerate migration toward low-emission water-borne systems.

Which application is expanding fastest?

Adhesives and carpet backing are projected to rise at a 4.60% CAGR as e-commerce packaging volumes surge.

Why is the United States so dominant?

It holds 83.06% share due to large-scale infrastructure spending, stringent environmental rules, and sizable housing stock.

How will PFAS restrictions influence suppliers?

Firms that commercialize PFAS-free surfactant packages and silicone-based alternatives are positioned to win share as bans tighten from 2026 onward.

Page last updated on: