North America Polycarbonate (PC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

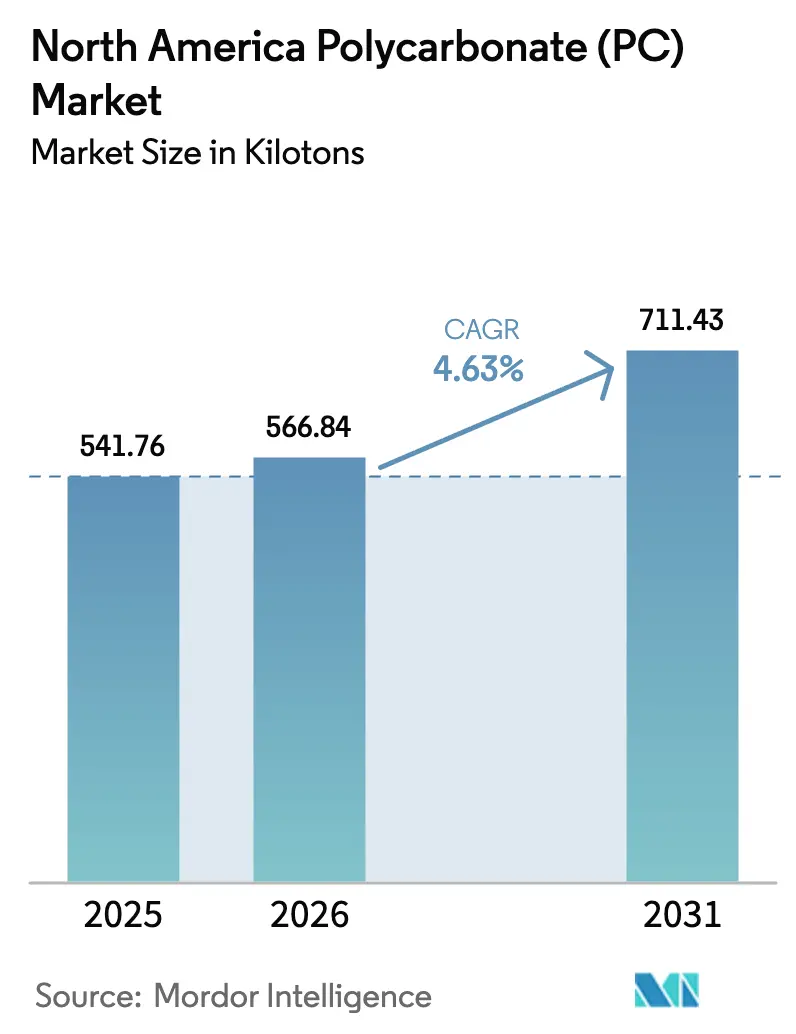

| Base Year Market Size (2025) | 541.76 kilotons |

| Market Volume (2026) | 566.84 kilotons |

| Market Volume (2031) | 711.43 kilotons |

| Growth Rate (2026 - 2031) | 4.63% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Polycarbonate (PC) Market Analysis by Mordor Intelligence

The North America Polycarbonate Market size in 2026 is estimated at 566.84 kilotons, growing from 2025 value of 541.76 kilotons with 2031 projections showing 711.43 kilotons, growing at 4.63% CAGR over 2026-2031. This trajectory indicates that the North America polycarbonate market size is benefiting from a structural pivot toward lightweighting in electric vehicles (EVs), accelerating 5G infrastructure roll-outs, and onshoring of advanced manufacturing. Suppliers that master specialty grades able to withstand higher temperatures, deliver optical clarity, and incorporate recycled feedstock are capturing outsized demand. Rapid commercialization of chemically recycled resins along the U.S. Gulf Coast illustrates how circular feedstock can offset bisphenol-A (BPA) price swings while improving sustainability profiles. The United States remains the anchor of consumption thanks to entrenched automotive OEMs, while Mexico’s expanding EV assembly base is reshaping regional supply chains. Growing preference for PFAS-free flame-retardant formulations further differentiates suppliers able to meet emerging regulatory benchmarks.

Key Report Takeaways

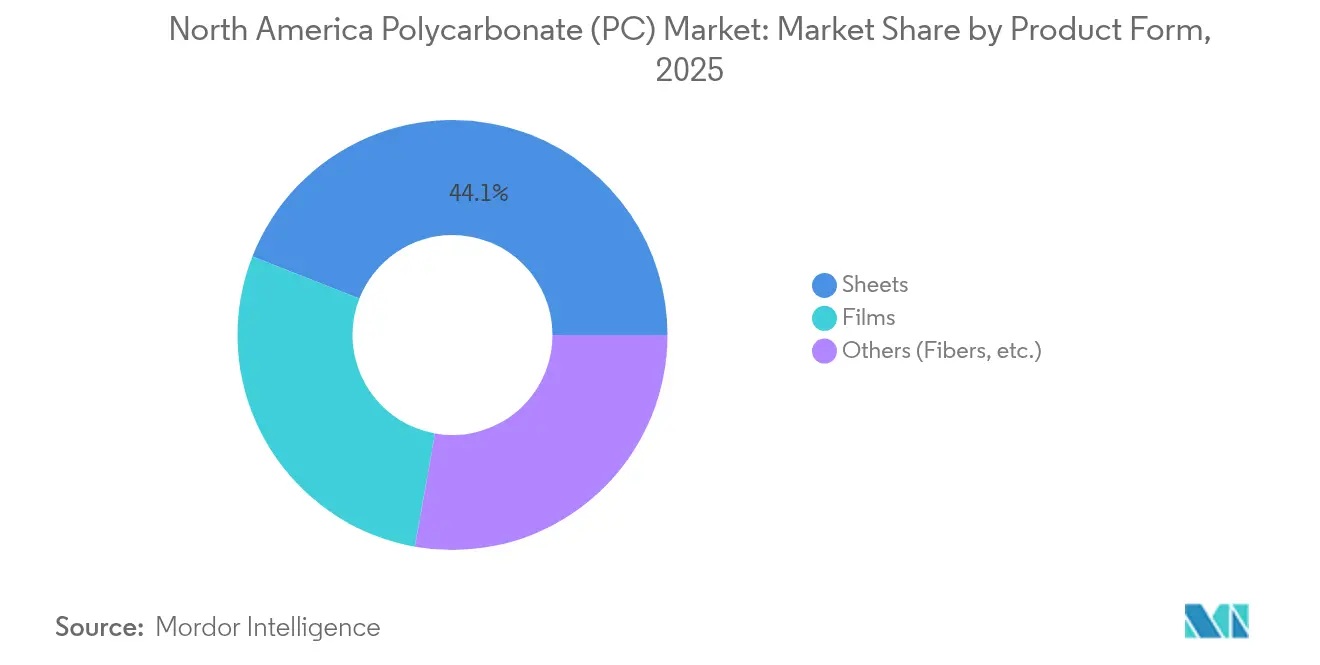

- By product form, sheets accounted for 44.05% of the North America polycarbonate market share in 2025. Films are projected to record the fastest 5.52% CAGR through 2031.

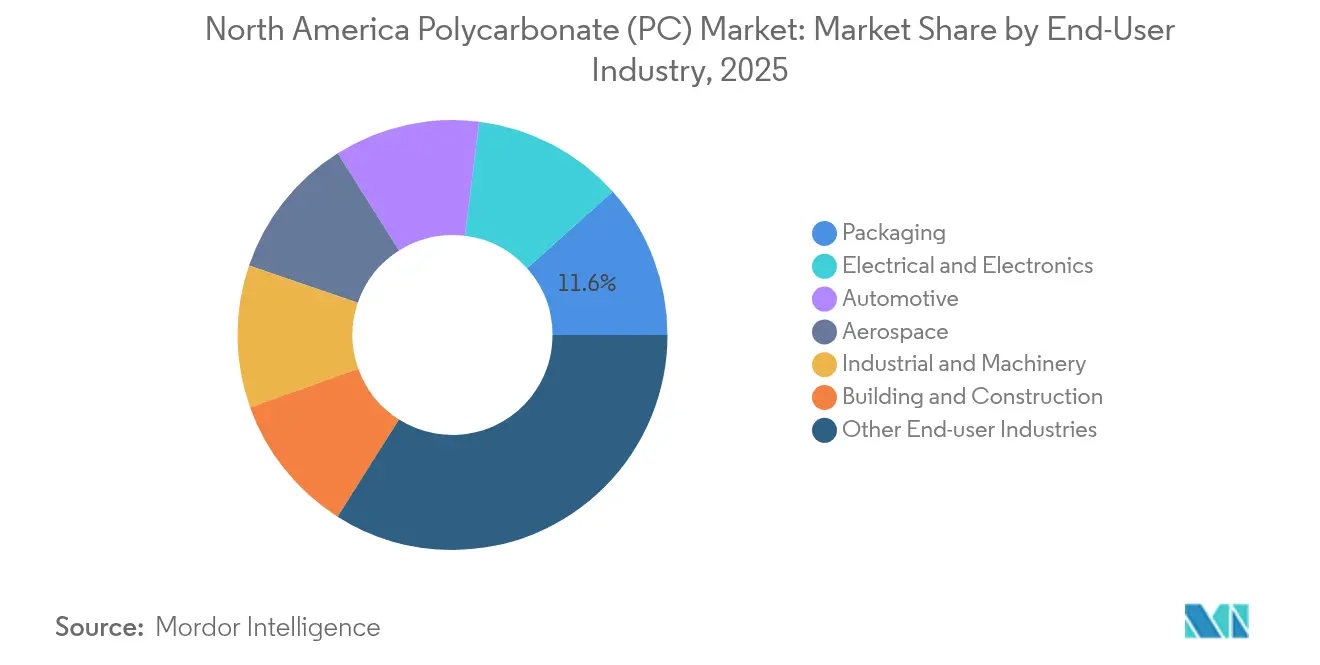

- By end-user industry, other end-user Industries accounted for 33.98% of the North America polycarbonate market share in 2025, while electrical and electronics applications are expected to register the highest 6.35% CAGR to 2031.

- By geography, the United States led with 69.55% volume share in 2025, whereas Mexico is forecast to post the fastest-growth CAGR of 6.12% between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Polycarbonate (PC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweighting demand in EV & autonomous vehicles | +1.20% | United States and Mexico | Medium term (2-4 years) |

| Proliferation of high-speed 5G & IoT electronics | +1.10% | Region-wide | Short term (≤ 2 years) |

| Expansion of greenhouse & smart-construction glazing | +0.80% | United States and Canada | Long term (≥ 4 years) |

| Rapid adoption of food-grade & BPA-free PC in packaging | +0.60% | Region-wide | Medium term (2-4 years) |

| Commercialisation of chemical-recycled PC resins (US Gulf Coast) | +0.70% | United States Gulf Coast region, spill-over to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lightweighting Demand in EV & Autonomous Vehicles

Each battery-electric car built in North America contains almost 22 pounds of polycarbonate, 15% more than a typical internal-combustion counterpart, because the material now appears in battery housings, charging-port covers, and lidar sensor modules. Weight reduction improves driving range, while optical-grade PC keeps sensor lenses clear in harsh weather. Planned facilities such as BMW’s high-voltage battery plant in San Luis Potosí expand demand corridors south of the U.S. border. Suppliers offering low-warpage, UV-stable resins stand to secure multi-year sourcing agreements with both legacy and start-up EV makers. The long design-in times typical of automotive platforms lock in volumes and support stable pricing. As autonomy levels rise, tier-one suppliers are specifying higher-clarity grades that resist yellowing under continuous lidar exposure, reinforcing the competitive edge of fully integrated producers that can tailor optical properties at the polymer-chain level.

Proliferation of High-Speed 5G & IoT Electronics

Roll-out of 5G base stations and edge-computing nodes accelerates demand for polycarbonate housings able to dissipate heat and block electromagnetic interference while meeting UL94 V-0 requirements at thin walls. Miniaturized IoT devices add incremental volume through watch casings, smart-home hubs, and medical wearables that need chemical-resistant, precision-moldable enclosures. Server racks used in mobile-edge data centers now feature PC panels that combine structural rigidity and weight savings, enabling easier maintenance in constrained urban sites. Suppliers that embed conductive fillers without compromising translucency unlock premium pricing in high-frequency antenna covers. Given the rapid obsolescence of telecom hardware, compounding lines that promise shorter lead times and lot-to-lot consistency achieve preferred-supplier status, particularly for contract manufacturers in Texas and Ontario.

Expansion of Greenhouse & Smart-Construction Glazing

Greenhouse operators adopting double-wall polycarbonate panels reduce heating energy by up to 30% compared with single-pane glass, freeing operating budgets for automation upgrades. Builders of smart offices and vertical farms choose PC skylights that integrate photovoltaic strips, blending daylighting with on-site power generation. Impact resistance superior to tempered glass improves safety in high-wind zones along the Gulf Coast. Sensor-embedded PC sheets monitor UV transmittance and trigger ventilation or shading automatically. In Canada, architects specify infrared-absorbing PC laminates to meet net-zero building codes without compromising natural light. These emerging functions push demand away from commodity sheets toward multilayer co-extrusions, lifting average selling prices and margins across the North America polycarbonate market.

Rapid Adoption of Food-Grade & BPA-Free PC in Packaging

The Food and Drug Administration has expanded its scrutiny of BPA exposure in reusable containers, prompting brand owners to insist on alternative-monomer polycarbonate that delivers equivalent clarity and toughness[1]Food and Drug Administration, “Bisphenol A (BPA): Use in Food Contact Application,” fda.gov . Chemical recycling breakthroughs enable closed-loop supply of food-contact grades, curbing reliance on virgin BPA and slashing lifecycle emissions. Sports-drink makers now prefer drop-in BPA-free resins to avoid switching to less-durable copolyesters. Refill-station pilot programs across California have raised demand for dishwasher-stable PC bottles that survive 100 wash cycles without stress-cracking. Producers with internal hydrolysis-stabilizer formulations differentiate themselves in this high-visibility segment, which influences consumer perception of polymer safety.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory scrutiny on bisphenol-A exposure | -0.90% | Region-wide | Short term (≤ 2 years) |

| Feedstock (BPA) price volatility | -0.70% | Region-wide | Medium term (2-4 years) |

| PFAS phase-out forcing re-qualification of flame-retardant grades | -1.00% | North America regulatory driven, global implications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Scrutiny on Bisphenol-A Exposure

Safety agencies on both sides of the Atlantic now question BPA migration limits, raising the prospect of tighter U.S. thresholds that could compel costly reformulations[2]European Food Safety Authority, “Bisphenol A: EFSA Updates Risk Assessment,” efsa.europa.eu. Packagers of infant-care products face reputational risks that encourage switching to alternative polymers, shaving baseline volume growth. Producers investing in non-BPA routes must validate mechanical parity and secure regulatory approval, a process that stretches development cycles. Mid-sized converters lacking in-house testing capabilities may defer capital upgrades, temporarily slowing downstream uptake. Even where bans are unlikely, retailers are adopting precautionary sourcing policies that favor BPA-free grades, reshaping demand patterns toward premium offerings but also compressing legacy product volumes.

Feedstock (BPA) Price Volatility

Limited North American BPA capacity and dependence on cumene feedstocks expose polycarbonate makers to sharp cost swings whenever phenol or acetone supply tightens. Hurricanes along the Gulf Coast periodically disrupt upstream operations, forcing spot-market purchases that erode margins. Contract customers in automotive and construction segments require stable pricing to commit to multi-year programs, so volatility risks bid withdrawals. Integrated producers cushion shocks with captive BPA units, whereas toll compounders rely on index-based pass-throughs that lag real-time fluctuations. These dynamics intensify competition for secure feedstock positions and could deter new entrants lacking backward integration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Sheets Remain the Volume Anchor While Films Accelerate

Sheets retained a 44.05% share of the North America polycarbonate market in 2025 on the strength of construction glazing, machine guards, and security barriers that demand large-format impact resistance. The segment’s entrenched scale secures baseline throughput for extrusion lines, while specification in building codes sustains replacement demand. Nonetheless, films are advancing at a 5.52% CAGR through 2031 as flexible electronics and high-barrier packaging gain ground. Multilayer co-extruded films just 25 microns thick enable foldable screens and medical blister packs, channels where value per kilogram outpaces sheets. Manufacturers that retrofit lines for optical-grade cleanliness capture orders from display assemblers in Ohio and Baja California. In contrast, the others category, encompassing powders and filaments, remains niche but benefits from additive-manufacturing adoption in aerospace interiors where flame-retardant powders slash part weight by 60%.

The North America polycarbonate market size tied to sheet volumes will still rise as infrastructure dollars stream into retrofitting public facilities with blast-resistant panels. Yet films provide strategic upside because each successive mobile-device generation specifies tighter tolerances and thinner gauges. As a result, suppliers that balance high-throughput sheet lines with solvent-cast or tenter-frame film assets diversify revenue without over-exposure to cyclical construction cycles. Price premiums on anti-fog, anti-scratch coated films improve margins and partially offset BPA cost swings.

By End-User Industry: Electronics Leads Future Growth, Diversified Demand Temper Risks

Electrical and electronics recorded the fastest 6.35% CAGR outlook as 5G small-cell deployments and edge servers multiply component counts that require flame-retardant, dimensionally stable housings. The North America polycarbonate market share linked to this segment is expected to climb steadily because each antenna unit incorporates up to 2.5 kilograms of specialty PC. Meanwhile, the other end-user industries bucket held the single-largest 33.98% slice in 2025, highlighting the material’s adaptability in medical devices, sports helmets, and industrial sight-glasses. Automotive demand is rebounding as EV volumes cross 2 million units region-wide, driving interior lighting lenses and battery module covers.

Packaging users are shifting toward dishwasher-stable, reusable containers that cut single-use waste, a trend aligning with chemical-recycling feedstock commitments from large resin producers. Building and construction customers value polycarbonate roofing that survives hailstorms better than fiberglass while admitting natural light that cuts daytime electricity needs. Aerospace adoption benefits from smoke-density compliant grades that shave 1 pound per passenger on wide-body jet interiors, translating into substantial fuel savings over an aircraft’s 25-year life. This diversified demand profile reduces cyclicality across the North America polycarbonate industry and positions integrated suppliers to balance order books during downturns in any single vertical.

Geography Analysis

The United States commanded 69.55% of regional consumption in 2025, anchored by a mature automotive supply web in the Midwest and expanding electronics clusters in the Southeast. Covestro’s Ohio capacity upgrade, scheduled to come online by 2026, reinforces domestic self-sufficiency and supports advanced recycling pilots along the Gulf Coast that reclaim post-consumer PC water-cooler bottles into food-contact resin. Federal investment incentives for semiconductor fabrication further lift film and compound demand as cleanroom equipment specifies static-dissipative PC panels.

Canada benefits from harmonized safety standards and leverages renewable-energy mandates that spur demand for building-integrated photovoltaic glazing using light-transmitting PC layers. Mining equipment OEMs in Ontario order impact-resistant hoppers and protective guards, applications where metal substitution cuts downtime caused by denting or corrosion. Cross-border rail logistics enable efficient shipment of bulk pellets from U.S. plants to Canadian converters, minimizing inventory costs.

Mexico, though smaller in absolute volume, is emerging as an indispensable node of the North America polycarbonate market. Greenfield EV assembly lines in Nuevo León and Coahuila are pulling component suppliers into adjacent industrial parks, creating localized demand for specialty grades used in battery enclosures and lidar housings. Free-trade provisions under USMCA ensure duty-free resin flows, while wage differentials preserve cost competitiveness. As global OEMs localize supply chains to buffer geopolitical shocks, Mexican converters gain share of high-value applications once imported from Asia. Government commitments to renewable energy and smart-agriculture programs also encourage use of polycarbonate films in drip-irrigation sensors and greenhouse panels, buttressing non-automotive demand.

Competitive Landscape

The North America polycarbonate market exhibits highly consolidated concentration. Covestro prioritizes specialty medical and optical-grade polymers and is doubling down on chemical-recycling alliances to secure post-consumer feedstock. SABIC has rolled out copolymer resins that deliver 20× higher chemical resistance, targeting battery-electric vehicle coolant manifolds. Trinseo launched PFAS-free formulations ahead of regulatory deadlines, giving appliance makers a drop-in option that eliminates fluorinated additives without tooling changes.

Integrated producers enjoy feedstock advantage through captive BPA units that buffer spot-market shocks, whereas compounders rely on formulation agility to win niche orders that require custom colors, anti-static functions, or bio-content certification. Collaborations with 3D-printing OEMs allow resin companies to position new powder grades for aerospace and medical prototypes, creating avenues for high-margin growth outside traditional extrusion and injection molding. Players lacking sustainability credentials risk deselection by OEMs pursuing science-based emission targets.

Competitive dynamics thus pivot toward R&D intensity and supply-chain resilience over sheer production tonnage. Early movers in closed-loop collection schemes secure post-consumer streams essential for premium recycled-content grades that command mark-ups exceeding 30%. Partnerships with toolmakers and automation firms shorten qualification cycles, tacking on service revenue and deepening customer lock-in. Collectively, these shifts favor incumbents with both financial muscle and technical breadth, raising barriers for new entrants.

North America Polycarbonate (PC) Industry Leaders

Covestro AG

LG Chem

Mitsubishi Chemical Group Corporation

SABIC

Trinseo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Covestro has announced the expansion of its polycarbonate production lines in Ohio, United States. This development enables the company to address the increasing demand for specialized polycarbonate materials while reinforcing its position as a leading provider in North America. The expanded facilities are expected to become fully operational by the end of 2026.

- January 2024: SABIC has introduced its new LNP ELCRES CXL polycarbonate (PC) copolymer resins, which offer exceptional chemical resistance. These advanced materials are designed to serve customers in the mobility, electronics, industrial, and infrastructure sectors.

North America Polycarbonate (PC) Market Report Scope

Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging are covered as segments by End User Industry. Canada, Mexico, United States are covered as segments by Country.| Sheets |

| Films |

| Others (Fibers, etc.) |

| Aerospace |

| Automotive |

| Building and Construction |

| Electrical and Electronics |

| Industrial and Machinery |

| Packaging |

| Other End-user Industries |

| United States |

| Canada |

| Mexico |

| By Product Form | Sheets |

| Films | |

| Others (Fibers, etc.) | |

| By End User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Electrical and Electronics | |

| Industrial and Machinery | |

| Packaging | |

| Other End-user Industries | |

| By Geography | United States |

| Canada | |

| Mexico |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Industrial Machinery, Electrical & Electronics, and Others are the end-user industries considered under the polycarbonate market.

- Resin - Under the scope of the study, virgin polycarbonate resin in its primary forms such as powder, granule, etc. are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms