| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 15.04 Billion |

| Market Size (2030) | USD 17.38 Billion |

| CAGR (2025 - 2030) | 2.94 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

North America Plastic Caps And Closures Market Analysis

The North America Plastic Caps And Closures Market size is worth USD 15.04 Billion in 2025, growing at an 2.94% CAGR and is forecast to hit USD 17.38 Billion by 2030.

The North American plastic caps and closures industry is experiencing a significant transformation driven by sustainability initiatives and technological advancements in manufacturing processes. According to the American Chemistry Council, the United States produced 22,618 million pounds of HDPE in 2022, highlighting the substantial scale of plastic production capacity in the region. Major industry players are increasingly focusing on developing eco-friendly solutions, with companies like Origin Materials launching biodegradable plastic closure bottle caps made from polyhydroxyalkanoate (PHA) in March 2024. The industry is witnessing a surge in research and development activities aimed at creating innovative, sustainable packaging closures solutions that maintain product integrity while reducing environmental impact.

The market is significantly influenced by evolving consumer preferences and changing regulatory landscapes across North America. According to the US Census Bureau, construction spending in March 2024 was 9.6% above the March 2023 estimate, indicating robust growth in related industries that utilize plastic packaging components. Manufacturers are responding to these changes by developing advanced closure systems that offer enhanced functionality while meeting stringent regulatory requirements. The industry has seen notable innovations in child-resistant packaging, tamper-evident solutions, and dispensing systems, particularly in the pharmaceutical and personal care sectors.

The healthcare sector continues to be a crucial driver of innovation in the plastic caps and closures market. According to the American Society of Clinical Oncology (ASCO), there are estimated to be about 44,020 new cases of thyroid cancer in the United States in 2024, highlighting the growing demand for pharmaceutical packaging solutions. This has led to increased development of specialized container closure systems that ensure product safety and compliance with regulatory standards. Companies are investing in advanced manufacturing technologies to produce high-precision closures that meet the stringent requirements of medical and pharmaceutical applications.

Raw material dynamics and production efficiency remain critical factors shaping the industry landscape. The Beverage Marketing Corporation reports that the bottled water market reached USD 46 billion in 2022, with 15.9 billion gallons sold, demonstrating the substantial demand for plastic closure solutions. Manufacturers are increasingly adopting automated production systems and implementing quality control measures to enhance operational efficiency. The industry is witnessing a trend toward the integration of smart manufacturing technologies, including IoT sensors and automated quality control systems, to optimize production processes and maintain consistent product quality.

North America Plastic Caps And Closures Market Trends

Demand for Bottled Beverages Drives the Demand for Plastic Caps and Closures

The increasing consumption of bottled beverages, particularly bottled water, continues to be a primary driver for bottle caps and closures in North America. According to the International Bottled Water Association (IBWA) and the Beverage Marketing Corporation (BMC), bottled water has emerged as the most consumed beverage among Americans, reflecting growing health consciousness and a preference for convenient, portable hydration solutions. This trend is further evidenced by the significant retail sales growth in the food and beverage sector, with US retail food and beverage stores reaching approximately USD 985.3 billion in 2023, compared to USD 728.8 billion in 2017. In Canada, the average person consumes about 335 liters of water daily, equivalent to 670 standard water bottles (500 ml size), highlighting the substantial demand for bottled water and associated packaging components.

The industry is responding to this growing demand through innovative product developments and sustainable solutions. For instance, in May 2024, AlpekPolyester USA LLC introduced CAPETall, a new PET resin specifically designed for bottle caps that improves post-consumer PET bottle recycling and promotes circular economy principles. Similarly, in March 2024, Beyond Plastic launched one of the market's first biodegradable plastic bottle caps made from polyhydroxyalkanoate (PHA), offering recyclable, compostable, and biodegradable properties while maintaining the familiar look and functionality of traditional petroleum-based caps. These innovations demonstrate the industry's commitment to meeting increasing beverage packaging demands while addressing environmental concerns.

Understand The Key Trends Shaping This Market

Download PDF

Increased Demand for Innovative Solutions from Different End-Users

The growing sophistication of end-user requirements across various industries, particularly in cosmetics, personal care, and beverages, is driving innovation in plastic closure solutions. In the United States, closures for cosmetics are gaining significant traction due to their hygienic qualities, ease of use, and enhanced dispensing characteristics, while simultaneously providing a cohesive look to products such as fragrances and face creams. This trend is supported by the robust growth of the US cosmetics and personal care industry, which reached USD 90 billion in 2023, according to Common Thread Co., reflecting increasing consumer focus on personal appearance and hygiene maintenance.

The demand for innovative solutions is further amplified by changing consumer preferences and sustainability requirements across different end-user segments. Packaging companies are increasingly emphasizing the development of caps and closures that meet sustainable packaging criteria, incorporating new materials and lightweight designs while maintaining functionality. This innovation drive is particularly evident in the beverage sector, where manufacturers are developing specialized beverage closures for various applications, from sports caps for sports drinks to premium beverages, each requiring unique dispensing and sealing properties. The industry's response includes the development of tamper-evident features, child-resistant designs, and enhanced user-friendly functionalities, demonstrating the sector's ability to adapt to evolving end-user requirements while maintaining product integrity and consumer safety.

Segment Analysis: Raw Material

Polyethylene (PE) Segment in North America Plastic Caps and Closures Market

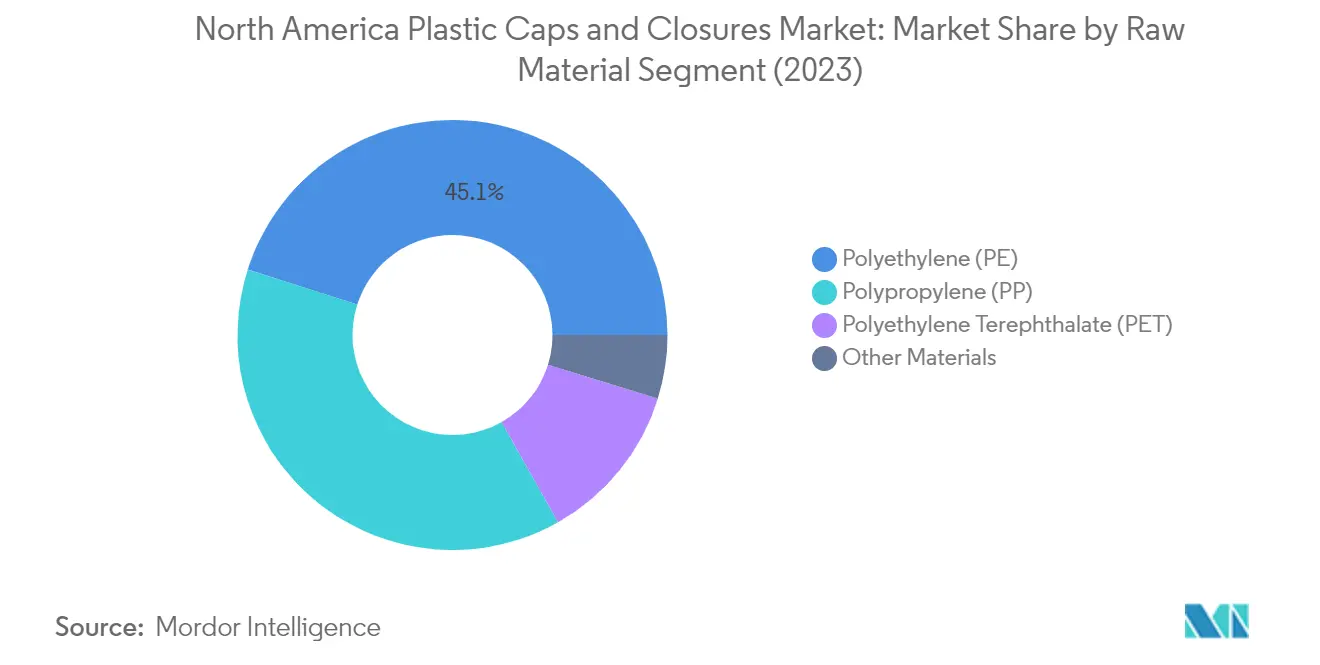

Polyethylene (PE) maintains its dominant position in the North American plastic caps and closures market, commanding approximately 45% market share in 2024. This substantial market presence is attributed to PE's superior durability, chemical resistance, and cost-effectiveness compared to other materials. PE, particularly HDPE and LDPE variants, has become the preferred choice for water bottle closures due to its exceptional organoleptic properties, ensuring optimal taste and odor characteristics. The material's versatility allows manufacturers to produce both rigid and flexible closures, making it ideal for various applications across beverage, food, and personal care industries. Major manufacturers are increasingly focusing on developing recyclable PE closures to meet growing sustainability demands, while maintaining the material's core benefits of strength and cost-effectiveness.

Polyethylene Terephthalate (PET) Segment in North America Plastic Caps and Closures Market

The Polyethylene Terephthalate (PET) segment is experiencing the most rapid growth in the North American plastic caps and closures market, with a projected growth rate of approximately 4% from 2024 to 2029. This accelerated growth is driven by PET's exceptional barrier properties against water vapor, gases, dilute acids, oils, and alcohol, making it particularly suitable for food and beverage packaging applications. The material's increasing adoption is further supported by its superior recyclability and potential for circularity in packaging solutions. Manufacturers are actively developing innovative PET closure designs that enhance product protection while meeting sustainability requirements. The segment's growth is also bolstered by its compliance with FDA regulations and its recognition as a safe material for food contact applications, particularly in recycled forms.

Remaining Segments in Raw Material Segmentation

The remaining segments in the market include Polypropylene (PP) and other materials such as Polystyrene and Polyvinyl Chloride (PVC). Polypropylene holds significant importance due to its superior rigidity and resistance to heat, water, and chemicals, making it particularly suitable for caps and closures in high-temperature applications. The other materials segment, while smaller in market share, continues to serve specific niche applications where unique material properties are required. These materials contribute to the market's diversity by offering specialized solutions for specific end-use applications, particularly in the pharmaceutical and chemical packaging sectors where material compatibility and chemical resistance are crucial factors.

Segment Analysis: By Type

Threaded Segment in North America Plastic Caps and Closures Market

The threaded segment dominates the North American plastic caps and closures market, commanding approximately 47% market share in 2024. Threaded plastic caps and closures are manufactured using various resin materials such as HDPE, LDPE, and polypropylene, available in continuous thread and non-continuous thread variants. These closures are particularly valued for their ease of installation and superior protection properties that prevent wear and tear over time. The segment's dominance is largely attributed to its widespread application across various industries, including pharmaceuticals, personal care, and food and beverages, where they provide premium packaging solutions and preserve product quality. Threaded caps are especially preferred for sealing bottles and jars used in aerospace, automotive, beverage, food, chemicals, paints, coatings, personal care, pet care, pharmaceuticals, and nutraceuticals, as these closures effectively pack containers to exclude carbon dioxide, oxygen, moisture, and microorganisms.

Child-Resistant Segment in North America Plastic Caps and Closures Market

The child-resistant segment is experiencing the fastest growth in the North American plastic caps and closures market, with a projected growth rate of approximately 4% from 2024 to 2029. This remarkable growth is driven by stringent legislation and increasing safety concerns, particularly in the United States market. The segment's expansion is supported by continuous innovations in child-resistant packaging solutions, such as multi-step mechanisms requiring two separate movements to open containers and oversized packaging designs. Major players are actively introducing new child resistance solutions, including no-torque plastic child-resistant caps with ergonomic designs featuring patented, sliding, two-step opening procedures. The integration of digital technology in child-resistant closures to enhance medication adherence represents another significant advancement, with features such as embedded microprocessors that track patient usage and store history within internal memory.

Remaining Segments in Type Segmentation

The dispensing and unthreaded segments complete the market segmentation by type in the North American plastic caps and closures industry. The dispensing closures segment serves various applications, including spice lids, flip-tops, disc tops, push-pulls, spouts, droppers, pumps, and sprayers, particularly important in personal care, health and beauty, food, and beverage sectors. Scientific advancements in dispensing closures seal technologies have led to enhanced closure systems that are especially effective in preserving product integrity. Meanwhile, the unthreaded segment caters to specific applications where threading action is not required, such as snap caps, sifter fitments, pour-out fitments, and tub lids, commonly used in paint packaging and food containers.

Segment Analysis: By End-User Industry

Beverages Segment in North America Plastic Caps and Closures Market

The beverages segment dominates the North American plastic caps and closures market, commanding approximately 38% market share in 2024. This significant market position is primarily driven by the rising consumption of bottled water, carbonated soft drinks, and other beverages across the United States and Canada. The segment's growth is further supported by increasing consumer preference for convenience packaging and on-the-go consumption formats. Major beverage manufacturers in the region are continuously innovating their packaging solutions, particularly focusing on sustainable and recyclable caps and closures. The segment's robust performance is also attributed to the growing demand for functional beverages, energy drinks, and premium beverage products that require specialized closure solutions for product protection and consumer convenience.

Cosmetics and Toiletries Segment in North America Plastic Caps and Closures Market

The cosmetics and toiletries segment is emerging as the fastest-growing segment in the North American plastic caps and closures market, projected to grow at approximately 4% CAGR from 2024 to 2029. This growth is primarily driven by increasing consumer spending on personal care products and the rising demand for premium beauty products across the region. The segment's expansion is further fueled by innovations in dispensing solutions, including airless pumps and specialized closures that enhance product preservation and user experience. Manufacturers are increasingly focusing on developing sustainable and recyclable closure solutions to meet the growing environmental consciousness among cosmetic consumers. The segment is also benefiting from the rising trend of clean beauty products and the increasing demand for travel-sized personal care items requiring specialized closure solutions.

Remaining Segments in End-User Industry

The pharmaceutical and healthcare segment plays a crucial role in the market, driven by stringent packaging requirements and the growing demand for tamper-evident closure solutions. The food segment continues to expand with innovative closure solutions for condiments, sauces, and other food products, including food packaging closures. The household chemicals segment maintains steady growth through the demand for cleaning products and detergents requiring secure closure solutions. Each of these segments contributes uniquely to the market's dynamics, with manufacturers developing specialized solutions to meet specific industry requirements, such as tamper-evident closure features for pharmaceuticals, dispensing solutions for food products, and child-resistant mechanisms for household chemicals.

North America Plastic Caps And Closures Market Geography Segment Analysis

North America Plastic Caps and Closures Market in the United States

The United States dominates the North American plastic caps and closures market, commanding approximately 83% of the total market share in 2024. The country's market leadership is driven by its robust beverage industry, particularly the bottled water segment, where consumer preferences continue to shift towards healthier alternatives to carbonated drinks. The presence of major beverage manufacturers and their continuous investment in innovative packaging closures solutions has significantly contributed to market growth. The country's emphasis on sustainable packaging solutions, evidenced by initiatives like the Draft National Strategy for Plastic Pollution Prevention, has prompted manufacturers to develop eco-friendly alternatives. The cosmetics and personal care sector has emerged as another significant driver, with a rising consumer focus on premium packaging and enhanced user experience. Additionally, the pharmaceutical sector's growth, coupled with stringent regulations on child-resistant pharmaceutical closures, has created sustained demand for specialized caps and closures.

North America Plastic Caps and Closures Market in Canada

Canada represents the fastest-growing market in the North American region, with a projected CAGR of approximately 3% from 2024 to 2029. The country's market growth is primarily fueled by its expanding pharmaceutical sector, where increasing investments in manufacturing capacity and continuous research and development activities are driving demand for specialized pharmaceutical closures. The presence of major pharmaceutical companies and their focus on new product development has created substantial opportunities for innovative plastic closure solutions. The Canadian beauty and personal care market has shown remarkable potential, particularly in natural and organic product segments, necessitating specialized packaging solutions. The country's strong emphasis on sustainable packaging practices and the growing adoption of recycled materials in manufacturing processes has positioned it as a progressive market for environmentally conscious packaging solutions. Furthermore, the beverage industry's shift towards premium packaging and the increasing demand for convenience features in bottle closure have contributed significantly to market expansion.

Get Analysis on Important Geographic Markets

Download PDF

North America Plastic Caps And Closures Industry Overview

Top Companies in North American Plastic Caps and Closures Market

The North American plastic caps and closures market is characterized by the strong presence of major players like Berry Global, Silgan Holdings, Amcor, Aptar Group, TriMas Corporation, and several other established manufacturers. These companies are driving market evolution through a sustained focus on sustainable packaging solutions and eco-friendly materials, particularly emphasizing recyclable and lightweight designs. Innovation trends center around developing tethered caps, tamper-evident solutions, and child-resistant closures while improving product functionality and user experience. Companies are investing heavily in research and development to create breakthrough solutions that combine sustainability goals with enhanced consumer experiences. Operational strategies focus on supply chain optimization, manufacturing footprint rationalization, and backward integration to ensure cost competitiveness and reliable material supply. Strategic expansion moves predominantly involve mergers and acquisitions to strengthen market presence, enhance technological capabilities, and access new customer segments across various end-user industries.

Fragmented Market with Strong Regional Players

The competitive landscape exhibits a highly fragmented structure with a mix of global conglomerates and specialized regional manufacturers. Global players like Berry Global and Amcor leverage their extensive manufacturing networks, technological capabilities, and broad product portfolios to serve diverse end-user industries across the region. These companies maintain their market positions through continuous innovation, strategic acquisitions, and strong customer relationships across food, beverage, pharmaceutical, and personal care sectors. Regional specialists like Pano Cap Canada and Erie Molded Plastics focus on specific market segments, offering customized solutions and maintaining a strong local presence through flexible manufacturing capabilities and responsive customer service.

The market demonstrates moderate consolidation tendencies, with larger players actively pursuing strategic acquisitions to expand their product offerings and geographical reach. Recent merger and acquisition activities highlight the industry's focus on technological advancement, sustainability capabilities, and market expansion. Companies are particularly interested in acquiring businesses that complement their existing product lines or provide access to new technologies and sustainable solutions. This consolidation trend is expected to continue as companies seek to strengthen their competitive positions and achieve economies of scale while meeting evolving customer demands for innovative and sustainable plastic packaging components.

Innovation and Sustainability Drive Future Success

For established players to maintain and expand their market share, a multi-faceted approach combining technological innovation, sustainability initiatives, and operational excellence is crucial. Companies must invest in developing eco-friendly solutions, including recyclable materials and lightweight designs, while maintaining product performance and safety standards. Building strong relationships with key end-users through collaborative product development and customization capabilities is essential for long-term success. Operational efficiency through advanced manufacturing processes and supply chain optimization remains critical for maintaining cost competitiveness in a market with moderate buyer bargaining power.

New entrants and smaller players can gain ground by focusing on niche markets and specialized applications where larger competitors may have limited presence. Success factors include developing innovative solutions for specific end-user requirements, establishing strong regional distribution networks, and maintaining flexibility in manufacturing operations. The relatively low threat of substitution products provides stability, but companies must navigate increasing regulatory pressures regarding plastic usage and recycling requirements. End-user concentration in key sectors like beverages and pharmaceuticals necessitates strong customer relationship management and consistent product quality to maintain market position. Future success will increasingly depend on companies' ability to align their strategies with sustainability goals while meeting evolving customer demands for innovative packaging closures solutions.

North America Plastic Caps And Closures Market Leaders

-

Silgan Holdings Inc.

-

Amcor PLC

-

Closure Systems International Inc.

-

AptarGroup Inc.

-

Trimas Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

North America Plastic Caps And Closures Market News

- April 2024: Aptar Closures launched Future Disc Top, a new closure designed to address the beauty and personal care industry’s evolving needs. This disc top closure prioritizes three key areas: recyclability, e-commerce compatibility, and consumer convenience.

- April 2024: The Kroger Co. announced that MCoBeauty Australia, one of the fastest-growing beauty brands, was making its United States debut at Kroger Family of Stores. The brand launched over 250 beauty and skincare products in stores. With affordability and practicality paramount to MCoBeauty's mission to provide accessible, innovative products, the luxe-for-less brand offers trend-focused makeup and skincare items under USD 30.

North America Plastic Caps & Closures Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

-

4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of Geopolitical Scenarios on the Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Demand for Bottled Beverages Drive the Demand for Plastic Caps and Closures

- 5.1.2 Increased Demand for Innovative Solutions from Different End Users

-

5.2 Market Restraints

- 5.2.1 Stringent Regulations on Manufacturers Pertaining to Environmental Degradation

- 5.2.2 Lightweight and Cost-effective Stand-up Pouch Packaging Alternatives

6. MARKET SEGMENTATION

-

6.1 By Material

- 6.1.1 Polyethylene (PE)

- 6.1.2 Polyethylene Terephthalate (PET)

- 6.1.3 Polypropylene (PP)

- 6.1.4 Other Types of Materials

-

6.2 By Type

- 6.2.1 Threaded

- 6.2.2 Dispensing

- 6.2.3 Unthreaded

- 6.2.4 Child-resistant

-

6.3 By End-user Industry

- 6.3.1 Beverage

- 6.3.1.1 Bottled Water

- 6.3.1.2 Soft Drinks

- 6.3.1.3 Spirits

- 6.3.1.4 Other Beverages

- 6.3.2 Food

- 6.3.3 Pharmaceutical and Healthcare

- 6.3.4 Cosmetics and Toiletries

- 6.3.5 Household Chemicals (Detergents, Cleaners, Soaps, and Polishes)

- 6.3.6 Other End-user Industries

-

6.4 By Country

- 6.4.1 United States

- 6.4.2 Canada

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles*

- 7.1.1 Silgan Holdings Inc.

- 7.1.2 Amcor PLC

- 7.1.3 Closure Systems International Inc.

- 7.1.4 AptarGroup Inc.

- 7.1.5 TriMas Corporation

- 7.1.6 Guala Closures SpA

- 7.1.7 Berry Global Inc.

- 7.1.8 Tetra Pak Group

- 7.1.9 O.Berk Company LLC

- 7.1.10 BERICAP Holding GmbH

- 7.1.11 Pano Cap Canada Ltd

- 7.1.12 Erie Molded Plastics Inc.

8. INVESTMENT ANALYSIS

9. FUTURE OUTLOOK OF THE MARKET

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

North America Plastic Caps And Closures Industry Segmentation

Plastic caps and closures are crucial in the packaging business. They are used to seal many containers, such as bottles, jars, and tubes. These closures serve various purposes, including keeping products fresh, avoiding leaking, ensuring tamper evidence, and making it easier for consumers to use the product. The study tracks the consumption trends of plastic-based caps and closures in North America. The study also considers the impact of various geopolitical scenarios on the market, key themes, and end-user industries-related demand cycles.

The scope of the study excludes caps and closures that are an important part of the container (e.g., aerosol can valve assemblies), closures for industrial bulk containers, home canning and bottling closures, caps and closures used in nonpackaging applications (e.g., pen caps, valve covers, distributor caps, food storage containers lids, liquor decanter closures), and flexible closures such as twist ties or foil lidding.

The North American plastic caps and closures market is segmented by material (polyethylene (PE), polyethylene terephthalate (PET), and polypropylene (PP), other types of materials), type (threaded, dispensing, unthreaded, and child-resistant), end-user industry (beverage [bottled water, soft drinks, and spirits], food, pharmaceutical and healthcare, cosmetics and toiletries, household chemicals [detergents, cleaners, soaps, and polishes], other end-user industries), and country (United States, Canada). The report offers the market forecasts and size in volume (units) and value (USD) for all the above segments.

| By Material | Polyethylene (PE) | ||

| Polyethylene Terephthalate (PET) | |||

| Polypropylene (PP) | |||

| Other Types of Materials | |||

| By Type | Threaded | ||

| Dispensing | |||

| Unthreaded | |||

| Child-resistant | |||

| By End-user Industry | Beverage | Bottled Water | |

| Soft Drinks | |||

| Spirits | |||

| Other Beverages | |||

| Food | |||

| Pharmaceutical and Healthcare | |||

| Cosmetics and Toiletries | |||

| Household Chemicals (Detergents, Cleaners, Soaps, and Polishes) | |||

| Other End-user Industries | |||

| By Country | United States | ||

| Canada | |||

Need A Different Region or Segment?

Customize Now

North America Plastic Caps & Closures Market Research FAQs

How big is the North America Plastic Caps And Closures Market?

The North America Plastic Caps And Closures Market size is worth USD 15.04 billion in 2025, growing at an 2.94% CAGR and is forecast to hit USD 17.38 billion by 2030.

What is the current North America Plastic Caps And Closures Market size?

In 2025, the North America Plastic Caps And Closures Market size is expected to reach USD 15.04 billion.

What years does this North America Plastic Caps And Closures Market cover, and what was the market size in 2024?

In 2024, the North America Plastic Caps And Closures Market size was estimated at USD 14.60 billion. The report covers the North America Plastic Caps And Closures Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the North America Plastic Caps And Closures Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

North America Plastic Caps And Closures Market Research

Mordor Intelligence offers a comprehensive analysis of the plastic caps and closures industry. We leverage extensive expertise in container closure systems research. Our detailed examination covers the complete spectrum of products. This includes bottle caps, screw caps, specialized sports caps, and twist caps. The report encompasses various segments such as pharmaceutical closures, beverage closures, and food packaging closures. It provides crucial insights into plastic closure technologies and innovations in tamper evident closure systems.

Stakeholders across the value chain can access our detailed report PDF, available for download. It examines trends in plastic packaging components and dispensing closures. The analysis offers valuable information about jar closure developments and packaging closures advancements. Particular attention is given to bottle closure technologies. Our research methodology ensures thorough coverage of all aspects. From basic plastic cap designs to sophisticated container closure systems, our report enables businesses to make informed decisions based on reliable market intelligence.