Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

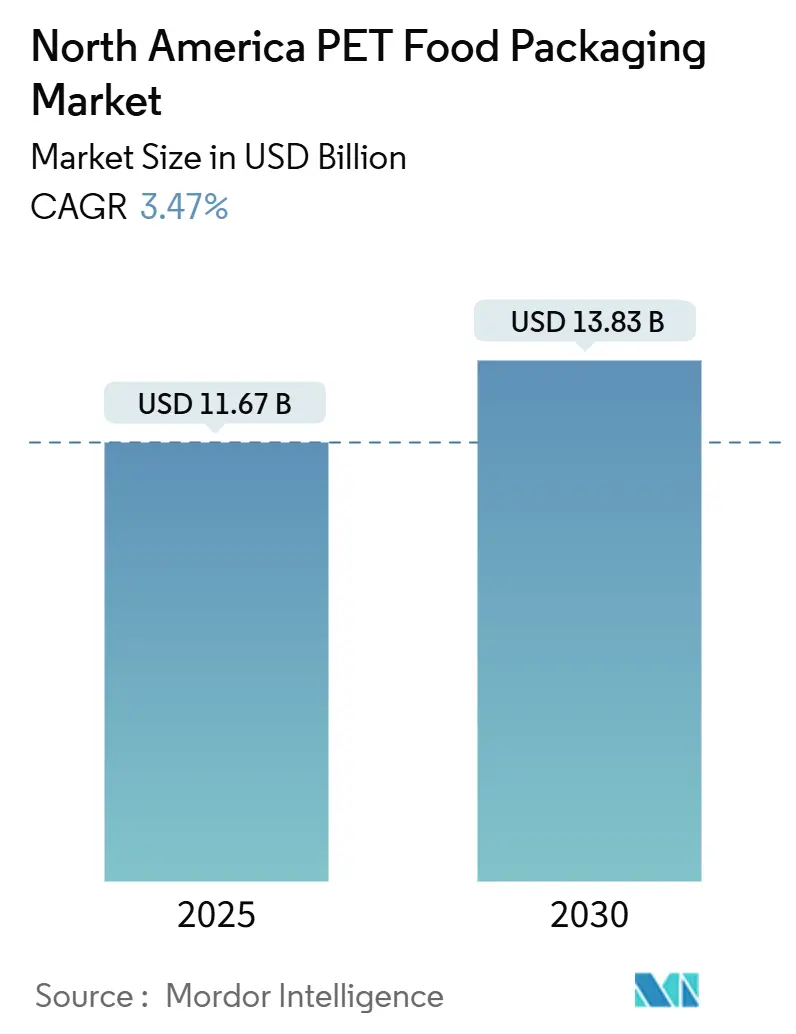

| Market Size (2025) | USD 11.67 Billion |

| Market Size (2030) | USD 13.83 Billion |

| Growth Rate (2025 - 2030) | 3.47% CAGR |

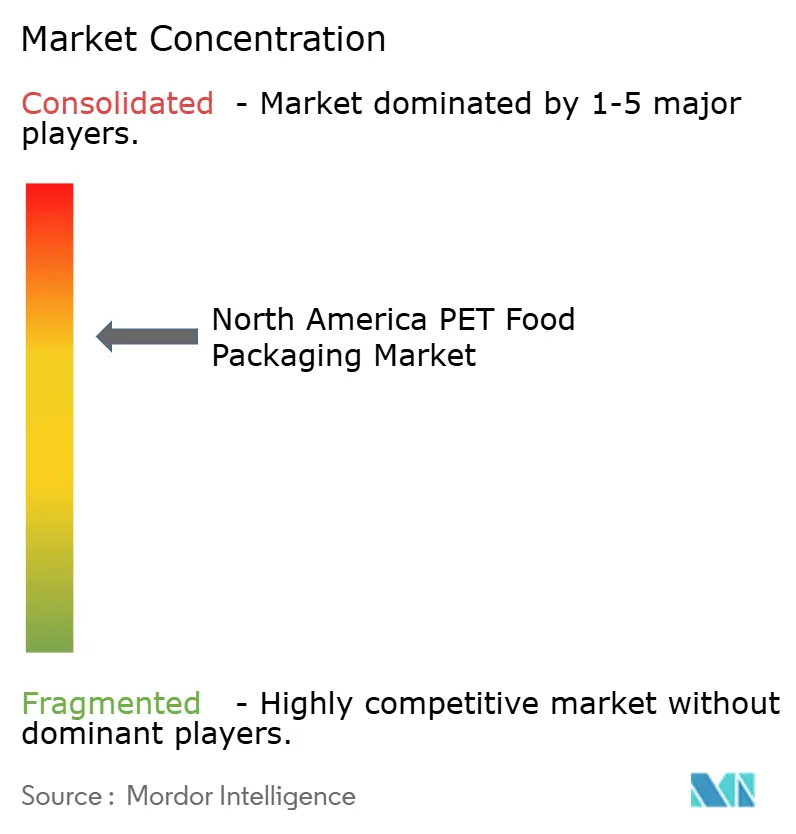

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America PET Food Packaging Market Analysis by Mordor Intelligence

The North America pet food packaging market size stood at USD 11.67 billion in 2025 and is projected to reach USD 13.83 billion by 2030, progressing at a 3.47% CAGR. An upswing in pet ownership, premium dietary preferences, and regulatory nudges toward recyclability are shifting demand from commodity containers to high-value formats that balance barrier performance with sustainability. Millennial consumers favor resealable closures, clear windows, and lightweight constructions that fit e-commerce parcel dimensions, prompting brand owners to redesign primary and secondary packs for omnichannel distribution.[1]Petfood Industry, “3 Future Trends in Pet Food Manufacturing,” petfoodindustry.com While plastic retains scale advantages, rapid material substitution toward paper, paperboard, and mono-material films reflects intensifying anti-plastics activism and emerging 30% recycled-content mandates. Concurrently, automation and smart sensors are raising throughput and traceability standards, enabling converters to offset labor constraints and meet retailer guidelines for in-line quality assurance.

Key Report Takeaways

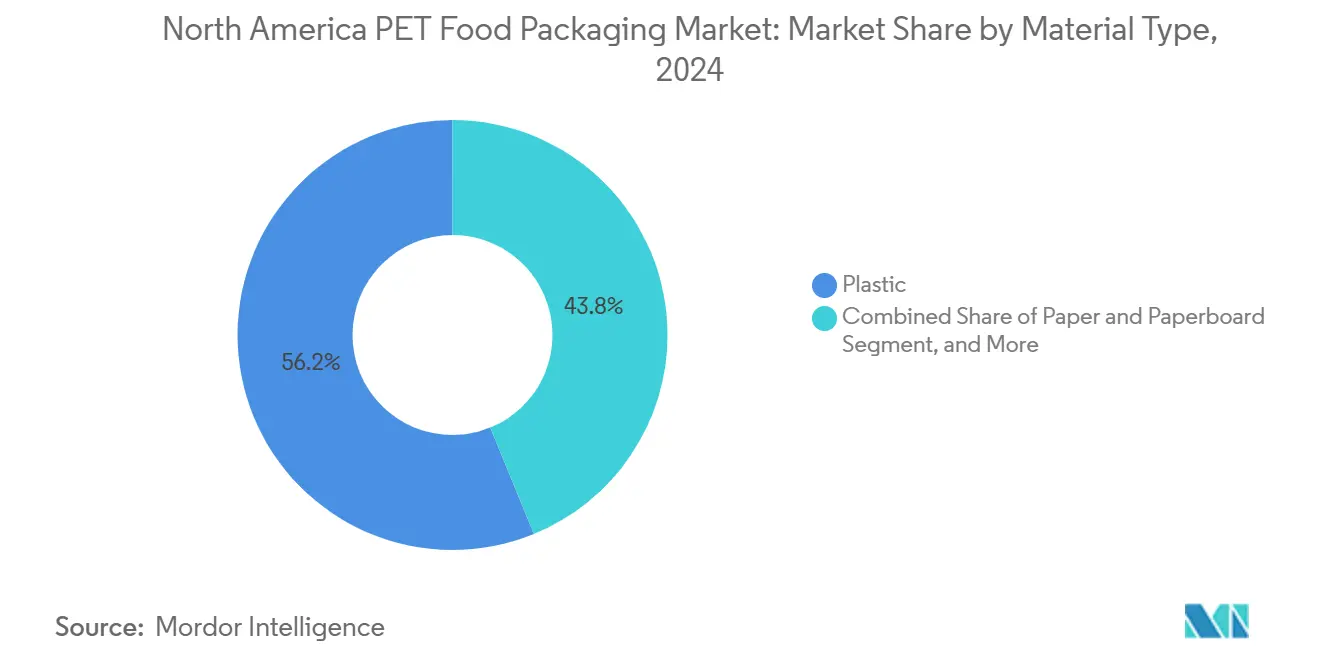

- By material, plastic captured 56.18% of the North America pet food packaging market share in 2024.

- By product type, the North America pet food packaging market size for the pouches segment is projected to grow at a 5.67% CAGR between 2025-2030.

- By food type, dry food captured 54.12% of the North America pet food packaging market share in 2024.

- By pet animal type, the North America pet food packaging market size for the feline segment is projected to grow at a 3.96% CAGR between 2025-2030.

- By geography, the United States captured 60.15% of the North America pet food packaging market share in 2024.

North America PET Food Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumisation of Grain-Free and High-Protein Formulae | +0.8% | United States and Canada metropolitan areas | Medium term (2-4 years) |

| Surge in E-Commerce Led Direct-to-Consumer Packaging Fulfilment | +0.9% | Core North America, spill-over to Mexico cities | Short term (≤ 2 years) |

| Lightweight Barrier Films Replacing Multilayer Metal Cans | +0.6% | United States and Canada premium segments | Long term (≥ 4 years) |

| Rising Disposable Incomes among Millennial Pet Parents | +0.7% | North American metropolitan areas | Medium term (2-4 years) |

| Deployment of Smart RFID-Enabled Freshness Sensors | +0.3% | United States and Canada premium channels | Long term (≥ 4 years) |

| Local Legislative Mandates on Post-Consumer Recycled Resin Content | +0.5% | United States state programs, Canadian provinces, emerging Mexico standards | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premiumisation of Grain-Free and High-Protein Formulae

Manufacturers marketing grain-free and protein-dense diets require ultra-low oxygen transmission rates to curb lipid oxidation, pushing demand for metallized polyethylene terephthalate and aluminum-oxide coated films that cost up to 20% more than standard laminations. Ingredient transparency surveys show 73% of pet parents under 35 read labels before purchase, encouraging clear windows, matte varnishes, and tactile elements that reinforce premium narratives. Resealable sliders and portion-control cups reduce feeding errors, supporting veterinary recommendations and minimizing waste. These enhancements lift average pack price but also elevate brand loyalty in a market where 42% of consumers switched labels after noticing packaging damage. The premiumisation driver therefore ties material science to lifestyle storytelling, boosting the North America pet food packaging market even in mature categories.

Surge in E-Commerce Led Direct-to-Consumer Packaging Fulfilment

Online penetration hit 23% of regional pet food sales in 2024, and parcel carriers now dictate drop-test and dimensional-weight thresholds that converge on sturdy, space-efficient designs.[2]Pet Food Processing, “Leveraging Automation and Robotics in Pet Food Processing,” petfoodprocessing.net Brands qualifying for Amazon’s Frustration-Free program remove outer cartons and shave 15-25% of total material, creating immediate cost-of-goods savings while slashing freight surcharges. Optimal cases of 12 x 9 x 6 inches for dry diets boost pallet fill to 88%, cutting transportation emissions and supporting corporate ESG targets. Subscription bundles embed tamper-evident pull tabs and scannable batch codes so automated inventory platforms can predict reorder cycles. These logistics-centric tweaks are central to the North America pet food packaging market, especially as last-mile economics shape pack geometry more than shelf presence.

Lightweight Barrier Films Replacing Multilayer Metal Cans

Retort-ready pouches employing aluminum-oxide coatings deliver water-vapor transmission rates under 0.1 g/m²/day, matching the shelf stability of cans while trimming pack weight by up to 60%. Flexible structures also cut warehouse footprint and reduce energy during sterilization because thinner walls accelerate heat penetration. Capital costs for retort lines, however, span USD 2-5 million, driving partnerships between brands and co-packers to de-risk investment. Early adopters positioned retort pouches as portion-friendly “spoon-free” meals, commanding 10-15% price premiums that consumers pay for convenience. As curbside recycling expands to accommodate mono-material high-barrier films, regulatory momentum will further tilt share away from metal, reshaping the North America pet food packaging market over the long term.

Rising Disposable Incomes among Millennial Pet Parents

Millennial households now account for 35% of regional pet ownership and spent USD 1,247 each on pet food in 2024, 40% above the Generation X average. This cohort values pack aesthetics, with 62% ranking resealability as a top attribute and 54% willing to pay more for recycled content. AAFCO’s Pet Food Label Modernization mandates larger nutrition panels, boosting primary pack real estate and indirectly favoring stand-up pouches over small cans because of the printable face area. High discretionary income supports rapid trial of novel formats such as freeze-dried toppers in rigid PET jars, each equipped with QR codes linking to farm-of-origin stories. These trends amplify premium pack-value capture and push converters to diversify machinery, sustaining the North America pet food packaging market growth during economic cycles.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Virgin Resin Prices | -0.4% | Global, acute in North America converters | Short term (≤ 2 years) |

| High Capital Outlay for Retort-Ready Pouch Lines | -0.3% | United States and Canada production hubs | Medium term (2-4 years) |

| Limited Curb-Side Recycling Infrastructure for Multi-Material Pouches | -0.2% | North America suburban and rural zones | Long term (≥ 4 years) |

| Growing Anti-Plastics Activism Targeting Pet Food Brands | -0.3% | United States and Canada consumer markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Virgin Resin Prices

Polyethylene and polypropylene quotes swung 25-40% during 2023-2024, compressing converter margins locked into fixed brand contracts.[3]Packaging Dive, “Packaging Laws Taking Effect in 2024,” packagingdive.com To hedge, large suppliers carry 60-90 days of inventory, tying up working capital and crowding out R&D budgets. Food-grade recycled pellets trade at 15-20% above virgin when supply is tight, limiting substitution that could cushion volatility. Small and mid-sized plants without multi-year resin agreements face spot-price exposure that erodes competitiveness, nudging them toward consolidation. The resulting supply-base shake-up tempers the otherwise steady expansion of the North America pet food packaging market.

High Capital Outlay for Retort-Ready Pouch Lines

Achieving commercial sterility in flexible retort packs requires specialized sealing heads, overpressure vessels, and in-line vision systems, pushing initial investment beyond USD 2 million per line. Validation tests dictated by FDA Low-Acid Canned Food rules can add USD 500,000 before first sale, extending payback horizons to five years for mid-tier brands. Operator training demands augment payroll expenses, while downtime during installation disrupts supply contracts. As a result, only converters with deep pockets or high-volume commitments can participate, slowing format migration despite consumer appeal. This restraint caps wet-food pouch penetration and slightly drags on the North America pet food packaging market CAGR.

Segment Analysis

By Material: Sustainability Pressures Recast the Plastic Core

Plastic accounted for 56.18% of North America pet food packaging market share in 2024, but its dominance is edging down as paper and paperboard climb at a 4.51% CAGR to 2030. The transition is driven by state-level recycled-content bills and producer-responsibility fees that penalize multi-material laminates. Despite cost advantages, conventional polyethylene structures struggle to reach the 30% post-consumer resin threshold without compromising seal integrity, pushing converters toward engineered mono-material films. EPR schemes in California, Oregon, and New Jersey already levy variable tariffs based on recyclability, steering brand owners to substrate redesign.

Developers of water-based dispersion coatings are piloting paper packs that withstand 50 drop cycles and sustain moisture barrier ratings suited for dry kibble. For wet formulas, bio-based coatings blended with polyvinyl alcohol extend shelf life up to 12 months, creating credible alternatives to metallized film. The continuous ebb and flow between barrier performance and recyclability will redefine material value pools, yet plastic remains indispensable for retort closures and high-stiffness zipper profiles. As a result, hybrid solutions such as “recycle-ready” PE-PE laminates will anchor near-term volume, while fiber innovations chip away at longer-term share in the North America pet food packaging market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Product Type: Pouches Leapfrog Legacy Bags

Bags held 34.25% North America pet food packaging market share in 2024 thanks to cost-efficient rollstock and high-speed form-fill-seal lines. However, stand-up pouches are accelerating at a 5.67% CAGR, reflecting their ship-ready geometry, billboard branding area, and portion-friendly reclosability. Barrier enhancements have raised oxygen protection to rival that of thick-wall bags, enabling smaller SKU sizes without sacrificing shelf life. For wet entrées, spouted retort pouches support “tear-pour-serve” rituals that resonate with busy pet parents and cut aluminum inputs by half.

Rigid bottles cater to niche liquid treats and probiotic toppers, leveraging HDPE’s compatibility with high-viscosity fills. Folding cartons primarily aggregate single-serve packs for club-store channels, adding gift-worthy cues. Though cans remain synonymous with traditional wet food, 76% of surveyed millennials indicated a preference for lighter packs that they can reseal after partial feeding. In this context, pouches are poised to surpass bags in perceived value, cementing their position as the innovation epicenter of the North America pet food packaging market.

By Food Type: Wet Formulas Gain Hydration-Driven Momentum

Dry diets continued to command 54.12% of the North America pet food packaging market size in 2024, yet wet recipes are advancing at a 4.02% CAGR as veterinarians highlight hydration and palatability benefits. Premium claim stacking human-grade meat, bone broth, and functional botanicals necessitate sterilization regimes that preserve nutrient integrity without retort-induced off-flavors. Thus, high-barrier pouches and aluminum trays are displacing steel cans, especially in urban markets where waste collection favors lightweight packs.

Hybrid freeze-dried and raw nuggets, though still below 5% share, call for nitrogen-flushed stand-up pouches with moisture scavengers that extend shelf life above 18 months. These cutting-edge formats capture double-digit price premiums while navigating complex cold-chain or ambient-shelf transitions. In parallel, dry kibble pack optimization targets higher fat diets, using EVOH layers to arrest rancidity. Collectively, format diversity tied to nutrition trends unlocks incremental value for converters across the North America pet food packaging market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Pet Animal Type: Cats Climb on Portion-Perfect Packs

Canine products delivered a 51.28% North America pet food packaging market share in 2024 because of larger feeding volumes. However, feline lines are rising at a 3.96% CAGR, propelled by smaller households adopting cats that demand high-protein single-serve portions. Cat owners gravitate to 70-gram pouches with tear-notch openings and easy-scrape interiors that curtail leftovers. Slim cans with foil-peel lids also cater to cats’ “fresh can every meal” rituals, but flexible packs now offer equivalent aroma retention with less metal.

Dog-food packaging innovations focus on reclosable sliders for 20-pound bags and measuring windows that guide portion control, supporting weight-management claims. Meanwhile, exotic species reptiles, birds, and small mammals drive micro-batch packaging with gas-barrier PET jars and child-safe caps. Each sub-segment challenges converters to balance run-length efficiency with SKU proliferation, sustaining overall momentum in the North America pet food packaging market.

Geography Analysis

The United States, representing 60.15% of North America pet food packaging market share in 2024, benefits from sophisticated e-commerce fulfillment, retailer recyclable-content scorecards, and per-capita spending that exceeds USD 250 annually. Federal Food Safety Modernization updates have introduced new current good manufacturing practice clauses that emphasize package integrity, nudging plants toward automated optical inspection. State-level recycled-content legislation adds cost but simultaneously rewards early adopters with shelf-tag recognition programs that attract eco-conscious buyers.

Canada’s adoption of extended producer responsibility widened in 2025, obligating brands to finance collection and sortation infrastructure. Provincial eco-fees vary by recyclability index; hence mono-material PE-PE laminates enjoy a 12% fee discount compared with foil-laminate stand-up pouches. Bilingual labeling statutes occupy up to 35% of printable area, favoring wider gusset or wrap-around formats. These dynamics encourage converters to maintain dedicated Canadian artwork teams and shorter press runs, slightly raising unit economics yet deepening strategic alignment with retailer packaging scorecards.

Mexico is the regional growth frontier, advancing at a 4.15% CAGR through 2030. Urbanization and disposable-income gains in Guadalajara and Monterrey spur premium pet food adoption, prompting local pack makers to install multi-lane pouch fillers that handle small grammage wet foods. ADM’s USD 33 million Guadalajara expansion triples output and integrates water-reuse systems that cut process effluent by 40%. Government moves to align with MERCOSUR food-contact protocols promote export agility, while pending recycled-content rules could accelerate film substitution, unlocking further upside for the North America pet food packaging market.

Competitive Landscape

Amcor, Berry Global, Crown Holdings, and Silgan Holdings anchor a moderately concentrated field where the five largest suppliers account for about 68% of regional sales. Their investment cadence centers on high-throughput machinery, in-line vision tech, and closed-loop scrap recovery that cushions resin price swings. Berry Global, for instance, fitted its Iowa plant with smart conveyors that boost line speed 18% and cut unscheduled downtime by 9%, driving cost leadership in co-extruded films.

Mid-tier converters pursue niche value bio-based coatings, digital printing for short runs, or subscription-specific pack assortments to evade direct commodity confrontation. Hill’s Pet Nutrition’s USD 450 million Kansas plant exemplifies integrated scale; the site processes more than 1,000 cans per minute under AI-enhanced defect detection, reinforcing vertical alignment between brand owner and converter. Meanwhile, Hillenbrand’s buyout of Schenck Process Food and Performance Materials adds weigh-belt feeders and bulk-handling systems to its pet-food portfolio, broadening equipment ecosystems that surround primary packaging.

Emerging entrants emphasize sustainability storytelling with compostable films or post-consumer resin rates above 50%. Yet anti-plastics activism risks customer backlash if end-of-life claims prove unverifiable, compelling alliances with recycling start-ups to guarantee traceability. Overall, competitive differentiation hinges on balancing regulatory foresight, material innovation, and operational excellence each essential for capturing share in the evolving North America pet food packaging market.

North America PET Food Packaging Industry Leaders

Amcor PLC

American Packaging Corporation

ProAmpac Intermediate Inc.

Coveris Holdings SA

Crown Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: ADM invested USD 33 million in a new pet-food line at its Guadalajara facility, tripling capacity and adding 65 jobs.

- December 2024: The European Commission enacted a full BPA ban in food-contact materials; North American suppliers started migrating to mono-material PET solutions.

- November 2024: PACK EXPO International 2024 drew 77,500 attendees and spotlighted automation and sustainable packaging for pet-food applications.

- October 2024: Hill’s Pet Nutrition commissioned its USD 450 million smart facility in Kansas, integrating RFID and AI-powered inspection.

- September 2024: A U.S. congressional bill proposed a 30% recycled-content requirement for plastic packaging, triggering regional supply-chain assessments.

North America PET Food Packaging Market Report Scope

Pet food packaging in North America helps keep the products fresh, long-lasting, clean, and free from contamination. Rising concerns over the nutritional intake of pets are leading to a rise in the manufacturing of a variety of pet food and boosting the demand for advanced materials for pet food packaging. The study tracks the key demand-side market dynamics based on a wide range of base indicators, such as pet food demand and local production. It analyzes the key material type, product type, and food type-based innovations witnessed across North America, which includes the United States and Canada. Further, The impact of the recent outbreak of COVID-19 on the spending on pet food products and vendor strategies is also analyzed as part of the final study.

By Material

| Plastic |

| Paper and Paperboard |

| Metal |

By Product Type

| Bags |

| Pouches |

| Plastic Bottles and Containers |

| Metal Cans |

| Folding Cartons |

| Other Product Types |

By Food Type

| Dry Food |

| Wet Food |

| Other Food Type |

By Pet Animal Type

| Canine (Dog) |

| Feline (Cat) |

| Other Pet Animal Types |

By Geography

| United States |

| Canada |

| Mexico |

| By Material | Plastic |

| Paper and Paperboard | |

| Metal | |

| By Product Type | Bags |

| Pouches | |

| Plastic Bottles and Containers | |

| Metal Cans | |

| Folding Cartons | |

| Other Product Types | |

| By Food Type | Dry Food |

| Wet Food | |

| Other Food Type | |

| By Pet Animal Type | Canine (Dog) |

| Feline (Cat) | |

| Other Pet Animal Types | |

| By Geography | United States |

| Canada | |

| Mexico |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the North America pet food packaging market in 2025?

The market is valued at USD 11.67 billion in 2025 and is projected to reach USD 13.83 billion by 2030, growing at a 3.47% CAGR.

Which package format is growing fastest in North America?

Stand-up pouches are the fastest, expanding at a 5.67% CAGR as brands pursue lightweight, resealable alternatives for both dry and wet foods.

Why is Mexico considered a high-growth region for pet food packaging?

Rising disposable incomes, urbanization, and investments like ADM’s new Guadalajara line support a 4.15% CAGR for Mexican demand.

What regulatory trends influence material choice in pet food packaging?

State recycled-content mandates, extended producer responsibility fees, and a pending 30% recycled-content federal bill are steering brands toward mono-material and PCR-rich substrates.

How are converters coping with volatile resin prices?

Large suppliers hedge via long-term contracts and scrap-recycling loops, while smaller firms explore post-consumer resin blends and joint purchasing cooperatives to cushion price swings.

What role does automation play in the competitive landscape?

High-speed vision systems, robotic palletizers, and RFID tracking like those in Hill’s Kansas plant elevate throughput and traceability, delivering cost and compliance advantages.