Market Size of north america pet food Industry

| Icons | Lable | Value |

|---|---|---|

|

|

Study Period | 2017 - 2029 |

|

|

Market Size (2024) | USD 85.00 Billion |

|

|

Market Size (2029) | USD 125.85 Billion |

|

|

Largest Share by Pets | Dogs |

|

|

CAGR (2024 - 2029) | 8.17 % |

|

|

Largest Share by Country | United States |

|

|

Market Concentration | Medium |

Major Players |

||

|

|

||

|

*Disclaimer: Major Players sorted in no particular order |

North America Pet Food Market Analysis

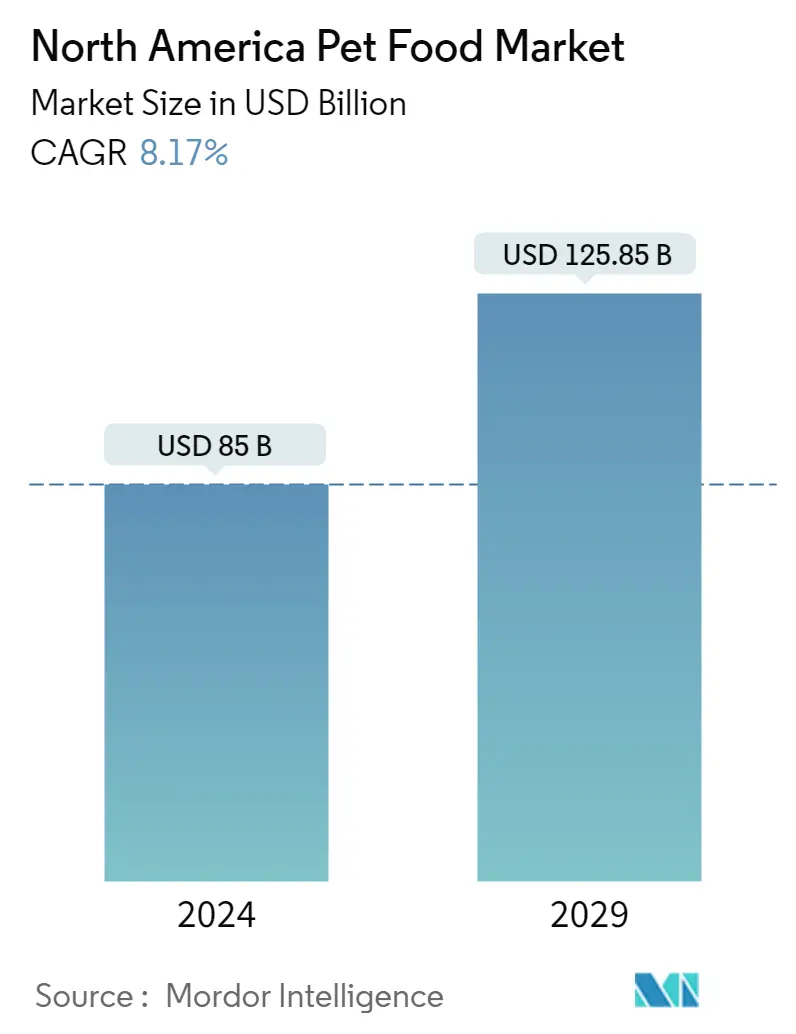

The North America Pet Food Market size is estimated at USD 85 billion in 2024, and is expected to reach USD 125.85 billion by 2029, growing at a CAGR of 8.17% during the forecast period (2024-2029).

85.00 Billion

Market Size in 2024 (USD)

125.85 Billion

Market Size in 2029 (USD)

10.60 %

CAGR (2017-2023)

8.17 %

CAGR (2024-2029)

Largest Market by Product

71.46 %

value share, Food, 2022

The rising pet population and the availability of a wide variety of pet food options, including custom-made pet foods with specialized diets, have contributed to the market's growth.

Largest Market by Country

88.55 %

value share, United States, 2022

The rising pet population, strong distribution networks, wide presence of major companies, and high consumer spending have contributed to its leading position in the region.

Fastest-growing Market by Product

10.47 %

Projected CAGR, Pet Veterinary Diets, 2023-2029

The rising prevalence of health issues in pets, particularly pet obesity and dental issues, and increased awareness of pet health are driving the market's growth.

Fastest-growing Market by Country

8.66 %

Projected CAGR, United States, 2023-2029

Rising pet ownership rates, increasing product innovations, and well-established pet retail chains and online platforms are some of the major factors driving the US market.

Leading Market Player

18.21 %

market share, Mars Incorporated, 2022

Mars, Incorporated is the market leader as it invests heavily in R&D and focuses on product innovations and expansions. It has also acquired major companies such as Champion Pet Foods.

Dogs exhibit a wider range of pet food preferences, which has led to an increased usage of commercial pet foods for dogs compared to cats

- The pet food industry in North America is experiencing rapid growth, particularly in the market for pet food. Dogs and cats held a significant share in both the volume and value of the North American pet food market. This can be attributed to the increased awareness about health and wellness among pet owners. Dogs typically have a more varied diet compared to cats, with many owners choosing to feed them a combination of dry and wet food.

- Pet food and treats are the primary types of food given to animals in the region, accounting for 85.5% of the market share in 2022. In the past, pet food mainly consisted of dry and wet products made from meat and grains. However, due to changing consumer preferences and a greater focus on pet health and wellness, the pet food industry has evolved to offer a wider range of products that cater to specific dietary needs and preferences.

- The main channels for distributing pet food in North America are supermarkets, pet stores, and online retailers, which collectively accounted for a 77.4% market share in 2022. These channels are preferred by consumers due to their accessibility, convenience, and the popularity of online shopping.

- In terms of consumption, the United States and Canada are the major countries in North America, representing a combined market share of 94.8% for pet food in 2022. This can be attributed to factors such as high pet ownership rates, increasing disposable incomes, and changing consumer preferences toward premium and organic pet food.

- Therefore, the growth of the pet food market is being driven by the rise of e-commerce and changing consumer preferences toward pet health and wellness. It is anticipated to record a CAGR of 8.4% during the forecast period.

Higher adoption of commercial pet food products in the United States is projected to grow faster than other countries

- The North American pet food market is one of the largest in the global pet food market. In 2022, North America accounted for USD 72.71 billion of the global market due to the large pet population, the high adoption rate of pets over the past five years, and growing awareness about the specialized pet food products in the region.

- The United States held the largest share of the North American pet food market. It accounted for 88.5% of the market in 2022 due to the highest pet population in the region and the growing pet humanization and premiumization. For instance, the pet population in the United States increased from 215.4 million heads in 2017 to 239.1 million heads in 2022, and 40% of the pet parents purchased premium pet food in 2022.

- Canada held the second-largest share of the market and accounted for USD 4.53 billion in 2022 due to the lower adoption of pets compared to the United States. The country is expected to register a CAGR of 4.4% during the forecast period due to the rising awareness about pet health and the growing pet expenditure.

- Mexico is one of the fastest-growing countries in the region. It is anticipated to register a CAGR of 7.1% during the forecast period due to Mexican pet parents increasingly purchasing high-quality and nutritious pet food products for their pets. There is a rise in the pets' ages, which is expected to help increase the demand for veterinary diets in the country.

- The rising pet population, growing demand for premium foods, and rising awareness about the health concerns in pets are anticipated to boost the growth of the North American pet food market during the forecast period.

North America Pet Food Industry Segmentation

Food, Pet Nutraceuticals/Supplements, Pet Treats, Pet Veterinary Diets are covered as segments by Pet Food Product. Cats, Dogs are covered as segments by Pets. Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets are covered as segments by Distribution Channel. Canada, Mexico, United States are covered as segments by Country.

- The pet food industry in North America is experiencing rapid growth, particularly in the market for pet food. Dogs and cats held a significant share in both the volume and value of the North American pet food market. This can be attributed to the increased awareness about health and wellness among pet owners. Dogs typically have a more varied diet compared to cats, with many owners choosing to feed them a combination of dry and wet food.

- Pet food and treats are the primary types of food given to animals in the region, accounting for 85.5% of the market share in 2022. In the past, pet food mainly consisted of dry and wet products made from meat and grains. However, due to changing consumer preferences and a greater focus on pet health and wellness, the pet food industry has evolved to offer a wider range of products that cater to specific dietary needs and preferences.

- The main channels for distributing pet food in North America are supermarkets, pet stores, and online retailers, which collectively accounted for a 77.4% market share in 2022. These channels are preferred by consumers due to their accessibility, convenience, and the popularity of online shopping.

- In terms of consumption, the United States and Canada are the major countries in North America, representing a combined market share of 94.8% for pet food in 2022. This can be attributed to factors such as high pet ownership rates, increasing disposable incomes, and changing consumer preferences toward premium and organic pet food.

- Therefore, the growth of the pet food market is being driven by the rise of e-commerce and changing consumer preferences toward pet health and wellness. It is anticipated to record a CAGR of 8.4% during the forecast period.

| Pet Food Product | |||||||||||

| |||||||||||

| |||||||||||

| |||||||||||

|

| Pets | |

| Cats | |

| Dogs | |

| Other Pets |

| Distribution Channel | |

| Convenience Stores | |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels |

| Country | |

| Canada | |

| Mexico | |

| United States | |

| Rest of North America |

North America Pet Food Market Size Summary

The North American pet food market is experiencing significant expansion, driven by a growing awareness of pet health and wellness among owners. This market is characterized by a diverse range of products catering to the dietary needs of pets, particularly dogs and cats, which dominate both the volume and value segments. The shift from traditional dry and wet food to more specialized and premium offerings reflects changing consumer preferences. Supermarkets, pet stores, and online retailers are the primary distribution channels, with the latter gaining popularity due to the convenience and variety they offer. The United States and Canada are the leading countries in this market, supported by high pet ownership rates and increasing disposable incomes, which encourage spending on premium and organic pet food products.

The market's growth is further fueled by the rise in pet adoption, particularly cats, and the trend of pet humanization, where pets are treated as family members. This has led to increased expenditure on pet food, with a notable shift towards premium segments such as customized, natural, and organic options. The pandemic has also accelerated the adoption of online shopping for pet food, contributing to higher sales through e-commerce platforms. The market is moderately consolidated, with major players like Colgate-Palmolive Company, General Mills Inc., Mars Incorporated, Nestle (Purina), and The J. M. Smucker Company leading the industry. Innovations and new product launches continue to shape the market, catering to the evolving needs and preferences of pet owners in the region.

North America Pet Food Market Size - Table of Contents

-

1. MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

-

1.1 Pet Food Product

-

1.1.1 Food

-

1.1.1.1 By Sub Product

-

1.1.1.1.1 Dry Pet Food

-

1.1.1.1.1.1 By Sub Dry Pet Food

-

1.1.1.1.1.1.1 Kibbles

-

1.1.1.1.1.1.2 Other Dry Pet Food

-

-

-

1.1.1.1.2 Wet Pet Food

-

-

-

1.1.2 Pet Nutraceuticals/Supplements

-

1.1.2.1 By Sub Product

-

1.1.2.1.1 Milk Bioactives

-

1.1.2.1.2 Omega-3 Fatty Acids

-

1.1.2.1.3 Probiotics

-

1.1.2.1.4 Proteins and Peptides

-

1.1.2.1.5 Vitamins and Minerals

-

1.1.2.1.6 Other Nutraceuticals

-

-

-

1.1.3 Pet Treats

-

1.1.3.1 By Sub Product

-

1.1.3.1.1 Crunchy Treats

-

1.1.3.1.2 Dental Treats

-

1.1.3.1.3 Freeze-dried and Jerky Treats

-

1.1.3.1.4 Soft & Chewy Treats

-

1.1.3.1.5 Other Treats

-

-

-

1.1.4 Pet Veterinary Diets

-

1.1.4.1 By Sub Product

-

1.1.4.1.1 Diabetes

-

1.1.4.1.2 Digestive Sensitivity

-

1.1.4.1.3 Oral Care Diets

-

1.1.4.1.4 Renal

-

1.1.4.1.5 Urinary tract disease

-

1.1.4.1.6 Other Veterinary Diets

-

-

-

-

1.2 Pets

-

1.2.1 Cats

-

1.2.2 Dogs

-

1.2.3 Other Pets

-

-

1.3 Distribution Channel

-

1.3.1 Convenience Stores

-

1.3.2 Online Channel

-

1.3.3 Specialty Stores

-

1.3.4 Supermarkets/Hypermarkets

-

1.3.5 Other Channels

-

-

1.4 Country

-

1.4.1 Canada

-

1.4.2 Mexico

-

1.4.3 United States

-

1.4.4 Rest of North America

-

-

North America Pet Food Market Size FAQs

How big is the North America Pet Food Market?

The North America Pet Food Market size is expected to reach USD 85.00 billion in 2024 and grow at a CAGR of 8.17% to reach USD 125.85 billion by 2029.

What is the current North America Pet Food Market size?

In 2024, the North America Pet Food Market size is expected to reach USD 85.00 billion.