Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

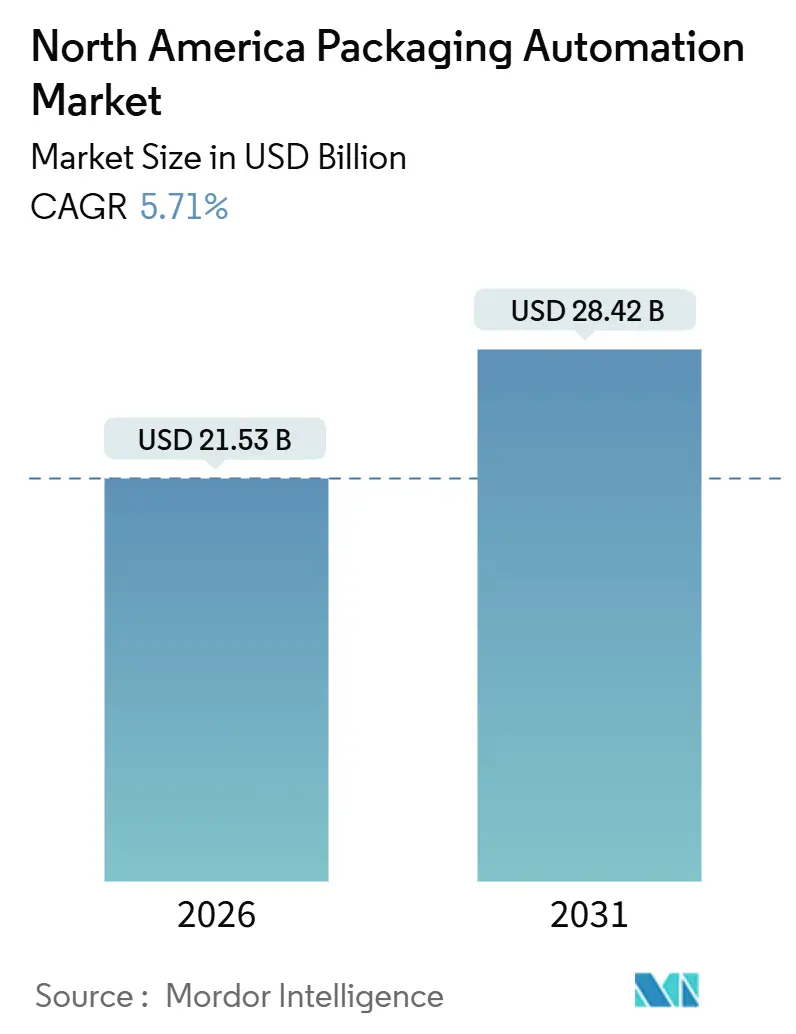

| Market Size (2026) | USD 21.53 Billion |

| Market Size (2031) | USD 28.42 Billion |

| Growth Rate (2026 - 2031) | 5.71% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Packaging Automation Market Analysis by Mordor Intelligence

The North America packaging automation market size is valued at USD 21.53 billion in 2026 and is projected to reach USD 28.42 billion by 2031, registering a 5.71% CAGR. Labor scarcity, rapidly rising wage bills, and regulatory mandates are shifting automation from a productivity booster to a business continuity requirement. Food, beverage, and pharmaceutical companies are retrofitting lines to safeguard throughput when shifts cannot be fully staffed. Higher throughput demands, mixed-SKU order profiles, and recyclable mono-material substrates are converging to favor modular, servo-driven platforms that store dozens of recipes and enable 10-minute tool changes. Palletizing robots, collaborative vision systems, and AI-enabled quality control modules are crossing cost thresholds that previously limited their adoption to high-volume applications. Federal and provincial incentive programs in Canada lower the effective payback periods, while tightened U.S. immigration policy keeps the labor market taut, sustaining demand for equipment. Declining costs for mid-payload collaborative robots and unified motion-vision software are widening the buyer base, supporting a resilient growth outlook despite high capital intensity.

Key Report Takeaways

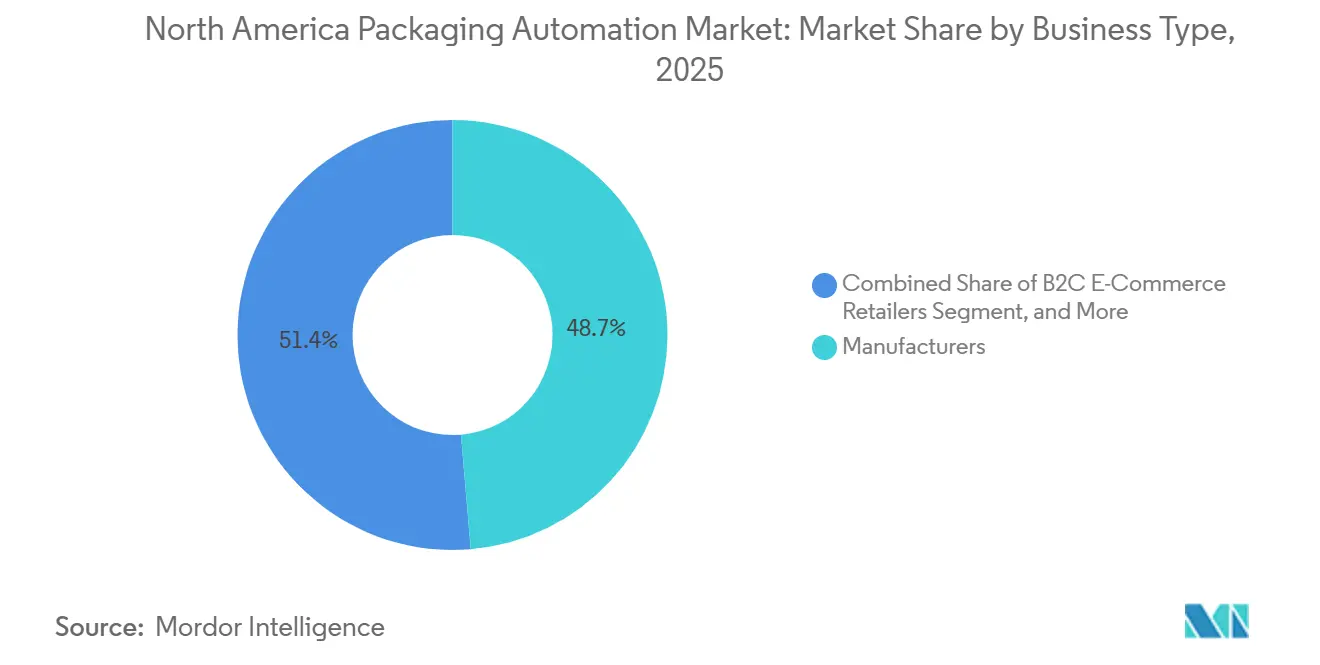

- By business type, manufacturers captured 48.65% of the North America packaging automation market share in 2025.

- By product type, the North America packaging automation market size for palletizing equipment is projected to grow at a 7.13% CAGR between 2026–2031.

- By automation level, fully automatic systems captured 63.31% of the North America packaging automation market share in 2025.

- By end-user, the North America packaging automation market size for pharmaceutical applications is projected to grow at a 6.89% CAGR between 2026–2031.

- By country, the United States captured 73.81% of the North America packaging automation market share in 2025.

North America Packaging Automation Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Manufacturing Labour Shortages | +1.2% | United States, Canada, Mexico | Medium term (2-4 years) |

| Need To Cut Operating Cost Per Packaged Unit | +0.9% | United States, Canada | Long term (≥ 4 years) |

| Surge In SKU Count from E-Commerce and Omnichannel | +1.4% | United States, Canada | Short term (≤ 2 years) |

| Regulatory Shift Toward Recyclable Mono-Materials | +0.7% | United States (California-led), Canada | Medium term (2-4 years) |

| AI-Enabled Quality-Control Reduces Giveaway and Recall Risk | +0.8% | United States, Canada | Medium term (2-4 years) |

| On-Machine Energy-Monitoring Cuts Utilities 5-15% | +0.5% | United States, Canada, Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Manufacturing Labour Shortages

Production job vacancies in U.S. plants remained near record levels through 2024, while rural processors contended with intensified wage competition from logistics hubs. A smaller pipeline of immigrant workers compounded the gap, steering producers toward robots and vision systems, which were viewed as a means of continuity insurance rather than a means of cost reduction. Automation vendors now market turnkey cells that replace two-shift crews yet require only one operator for supervision, tilting total-cost-of-ownership calculations in favor of capital expenditures. The scarcity is most acute in food clusters across the Midwest and Prairie provinces, anchoring demand for pick-and-place robots that withstand wash-down environments. As line downtimes attributable to absenteeism translate into lost retailer shelf slots, plant managers prioritize investments with the highest direct uptime payoff.

Surge in SKU Count from E-Commerce and Omnichannel

Between 2020 and 2024, omnichannel retailers increased the number of active SKUs by double digits, while order sizes per SKU shrank markedly, compressing the economic windows for manual setup. Changeovers that once occurred weekly now interrupt production several times per shift, underscoring the value of servo-driven, recipe-controlled machinery that can recall hundreds of parameters instantly. Mixed-case orders require palletizing robots with advanced vision to stage variable pack sizes without manual stacking. The 7.51% CAGR for B2C e-commerce retailers mirrors this need for agile equipment that can thrive in 10,000-square-foot micro-fulfillment centers.

AI-Enabled Quality-Control Reduces Giveaway and Recall Risk

Machine-vision platforms equipped with convolutional neural networks detect torn seals, misapplied labels, and fill-level deviations in real-time, minimizing scrap and shielding brands from costly recalls. The FDA guidance identifies packaging integrity failures as a leading recall trigger, with direct costs for a mid-sized producer exceeding USD 10 million.[1]“Guidance for Industry: Preventive Controls for Human Food,” U.S. Food and Drug Administration, fda.gov Vision attaches rates on new lines that surpassed 60% in 2024, driven by pharmaceutical and dairy applications, where thin margins magnify the impact of giveaway. Synthetic-image training techniques reduce data-collection cycles, enabling near-immediate deployment on low-volume SKUs and expanding adoption to a broader range of processors.

Regulatory Shift Toward Recyclable Mono-Materials

California’s SB 54 and the U.S. Plastics Pact force a pivot from multilayer laminates to mono-material films, each requiring distinct heat-seal temperatures and tension settings. Equipment makers now supply adaptive sealing jaws and inline thickness measurement to accommodate wider tolerances in recycled resins. Quick-change tooling becomes indispensable as brands experiment with fiber-based pouches and polyethylene films featuring 50% recycled content. Non-compliance risks a lockout of the California market, amplifying urgency across the continent.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront CAPEX For Fully Automated Lines | -0.6% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Integration Complexity with Legacy Controls | -0.4% | United States, Canada | Medium term (2-4 years) |

| Validation Overhead for Pharma and Food Safety | -0.3% | United States, Canada | Long term (≥ 4 years) |

| Cyber-Security Risk in Converged OT/IT Networks | -0.3% | United States, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX for Fully Automated Lines

Turnkey robotic cells can exceed USD 2 million before installation, a hurdle for mid-market processors that assess projects on three-year payback horizons. Extended 18-month lead times expose buyers to component price volatility, further dampening appetite. Leasing and automation-as-a-service contracts reduce the initial cash outlay but remain concentrated among enterprises with multiple sites, allowing them to amortize engineering fees across similar lines of business.

Integration Complexity with Legacy Controls

Lines commissioned in the 2000s often feature proprietary controllers that are incompatible with modern Ethernet-based protocols, necessitating full panel rewires during retrofits. NIST cybersecurity guidance highlights that legacy hardware lacks capacity for encrypted traffic, compelling managers to choose between connectivity and security. Edge gateways can translate protocols, but they add cost and latency, and do not address the looming obsolescence of spare parts. Integration complexity inflates downtime risk, steering some operators toward greenfield builds in regions such as Ontario or Nuevo León.

Segment Analysis

By Business Type: Direct-to-Consumer Fulfillment Accelerates Spend

Manufacturers captured 48.65% of 2025 revenue, yet the North America packaging automation market is witnessing the fastest growth among B2C e-commerce retailers at a 7.51% CAGR. Order-level variability and next-day delivery promises prompt fulfillment centers to adopt carton erection, bagging, and print-and-apply robots that can process mixed assortments without human intervention. Amazon revealed the deployment of more than 750,000 robotic drive units in 2024, illustrating the scale at which e-commerce is automating packaging tasks.

As urban wages exceed USD 20 per hour and parcel volumes continue to rise, automation becomes increasingly instrumental in controlling the cost per shipment, nudging this segment’s share steadily upward. Wholesale distributors and contract packagers remain sensitive to capital cost and favor modular upgrades that preserve line flexibility. However, recipe-driven software enabling 10-minute tool changeovers is eroding prior objections, suggesting an incremental shift toward higher automation levels even in smaller facilities.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Product Type: Palletizing Gains as Mixed-SKU Staging Intensifies

Conveying and handling equipment retained 27.49% of 2025 revenue, underscoring its indispensability to overall line speed. Nevertheless, robotic palletizers are on track for 7.13% annual growth as retailers demand floor-ready pallets comprising multiple SKUs. ABB’s FlexPalletizer 360 handles 15 case sizes within a single shift, marking a shift from fixed-gantry to vision-guided robots tailored to fragmented order profiles.[2]“Product Launch: FlexPalletizer 360,” ABB Ltd., abb.com

Filling and labeling systems grow closer to the overall North America packaging automation market rate, given their mature installed base. Serialization regulations are driving investment in high-speed labelers capable of printing and verifying 2D codes at rates of 300 units per minute; however, palletizing dominates incremental spending because it alleviates the end-of-line bottleneck.

By Automation Level: Fully Automatic Lines Extend Lead

Fully automatic equipment accounted for 63.31% of 2025 revenue and is forecast to outstrip semi-automatic alternatives with a 7.32% CAGR. Unified motion-vision environments and declining collaborative robot prices reduce commissioning time, enticing mid-tier processors previously priced out.

The North America packaging automation market share for fully automatic lines is likely to clear 70% by 2031 as operators phase out labor-intensive stations vulnerable to absenteeism. Semi-automatic solutions retain value in artisanal or seasonal runs; however, their relative share declines because integrated cells now offer modular layouts and smaller footprints.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Industry: Pharmaceuticals Outpace Food

Food processors hold 42.58% of revenue due to high-volume snack, meat, and beverage lines, but compliance requirements drive pharmaceuticals to a 6.89% CAGR. Unique identifier mandates necessitate vision-verified codes on every carton, driving the adoption of integrated inspection and rejection modules that enable speeds of up to 300 cartons per minute.

Cold-chain packaging complexity adds further impetus, as automated loading minimizes human contact with temperature-sensitive vials, thereby reducing the risk of contamination. Beverage, cosmetics, chemicals, and logistics applications are expanding at a rate similar to the overall market, with logistics providers investing in right-size boxing and ship-label automation to meet parcel-carrier dimensional-weight rules.

Geography Analysis

The United States generated 73.81% of 2025 revenue. Dense clusters of food and pharmaceutical producers in the Midwest, Southeast, and Mid-Atlantic sustain a large installed base that now receives incremental upgrades rather than full replacements. Compliance-driven modernization of California’s recycling rules and federal serialization mandates underpin steady growth, but legacy control complexity tempers the pace of growth.

Canada is forecast to grow at 6.65% through 2031 as Strategic Innovation Fund grants cover up to half of eligible automation costs. A smaller installed base enables greenfield deployment that sidesteps integration hurdles common south of the border.[3]“Strategic Innovation Fund,” Innovation, Science and Economic Development Canada, ic.gc.ca Labor vacancy rates in Canadian manufacturing mirror those in the U.S., reinforcing the business continuity appeal of automation. Mexico trails in absolute value yet benefits from nearshoring under the U.S.-Mexico-Canada Agreement.

Wage escalation in border regions and triple-digit annual labor turnover have spurred interest in automated packing cells that meet U.S. quality benchmarks. Infrastructure gaps in utilities and connectivity hinder adoption in certain industrial zones, but robotics suppliers are forming local integration partnerships that reduce execution risk. By 2030, cumulative investment will narrow the technology gap, positioning Mexican facilities as interchangeable nodes in North American supply chains.

Competitive Landscape

Global controls and robotics majors, including ABB, Rockwell Automation, Siemens, and Schneider Electric, anchor the market, leveraging their installed PLC bases to cross-sell motion and vision solutions. Their scale supports lifetime service agreements that smaller machine builders cannot match.

Specialized OEMs, such as Syntegon, ProMach, and JLS Automation, lead niche categories, from blister packing to case erecting, and frequently partner with the majors for control architecture. Technology differentiation centers on AI-infused vision, teach-by-demonstration robot programming, and cloud analytics. Cybersecurity readiness has become a bid criterion after highly publicized ransomware incidents exposed operational vulnerabilities.

Vendors offering segmented network architectures aligned with NIST guidelines gain favor among pharmaceutical and dairy buyers. Fragmentation persists within product silos, yet appetite for single-accountability turnkey projects is consolidating spend toward suppliers with deep integration capabilities.

North America Packaging Automation Industry Leaders

ABB Ltd.

Rockwell Automation, Inc.

Siemens AG

Schneider Electric SE

Mitsubishi Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2025: Siemens expanded its Alpharetta, Georgia, manufacturing site by USD 50 million, adding 200 jobs and raising servo-drive capacity by 30%.

- September 2025: ABB launched FlexPalletizer 360, a collaborative robotic palletizer handling 15 case sizes without manual changeover.

- August 2025: Rockwell Automation acquired Clearpath Robotics to integrate autonomous mobile robots into its packaging automation portfolio.

- July 2025: Syntegon opened a USD 25 million customer experience center in New Jersey for live demonstrations of serialized pharmaceutical lines.

North America Packaging Automation Market Report Scope

The North America packaging automation market refers to the regional industry segment focused on the design, manufacture, and deployment of automated machinery and systems that streamline packaging operations. These solutions include robotic case packers, palletizers, automated filling and sealing machines, and integrated control systems that reduce manual intervention and enhance productivity.

The North America Packaging Automation Market Report Is Segmented By Business Type (B2B E-Commerce Retailers, B2C E-Commerce Retailers, Omni-Channel Retailers, Wholesale Distributors, and Manufacturers), Product Type (Filling, Labelling, Horizontal/Vertical Pillow, Case Packaging, Bagging, Palletizing, Conveying/Handling, Capping, and Wrapping), Automation Level (Fully-Automatic, and Semi-Automatic), End-User Industry (Food, Pharmaceuticals, Cosmetics, Household, Beverages, Chemicals, Logistics, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

By Business Type

| B2B E-Commerce Retailers |

| B2C E-Commerce Retailers |

| Omni-Channel Retailers |

| Wholesale Distributors |

| Manufacturers |

By Product Type

| Filling |

| Labelling |

| Horizontal / Vertical Pillow |

| Case Packaging |

| Bagging |

| Palletising |

| Conveying / Handling |

| Capping |

| Wrapping |

By Automation Level

| Fully Automatic |

| Semi-Automatic |

By End-user Industry

| Food |

| Pharmaceuticals |

| Cosmetics |

| Household |

| Beverages |

| Chemicals |

| E-commerce and Logistics |

| Other End-user Industries |

By Country

| United States |

| Canada |

| Mexico |

| By Business Type | B2B E-Commerce Retailers |

| B2C E-Commerce Retailers | |

| Omni-Channel Retailers | |

| Wholesale Distributors | |

| Manufacturers | |

| By Product Type | Filling |

| Labelling | |

| Horizontal / Vertical Pillow | |

| Case Packaging | |

| Bagging | |

| Palletising | |

| Conveying / Handling | |

| Capping | |

| Wrapping | |

| By Automation Level | Fully Automatic |

| Semi-Automatic | |

| By End-user Industry | Food |

| Pharmaceuticals | |

| Cosmetics | |

| Household | |

| Beverages | |

| Chemicals | |

| E-commerce and Logistics | |

| Other End-user Industries | |

| By Country | United States |

| Canada | |

| Mexico |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What will the size of the North America packaging automation market be like by 2031?

Forecasts indicate the market will reach USD 28.42 billion by 2031, driven by a 5.71% CAGR.

Which segment shows the fastest growth potential?

B2C e-commerce retailers are projected to post a 7.51% CAGR, reflecting the need for flexible, small-order automation.

Why are palletizing systems gaining momentum?

Mixed-SKU orders and floor-ready pallet requirements are driving demand for vision-guided robotic palletizers, which are growing at a 7.13% annual rate.

What factors make Canada an attractive investment location?

Federal cost-sharing grants and a smaller installed base enable greenfield automation, supporting a 6.65% CAGR.

How does regulation influence adoption?

California's recycling mandates and FDA serialization rules compel upgrades, accelerating the purchase of adaptive sealing and vision inspection systems.