Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

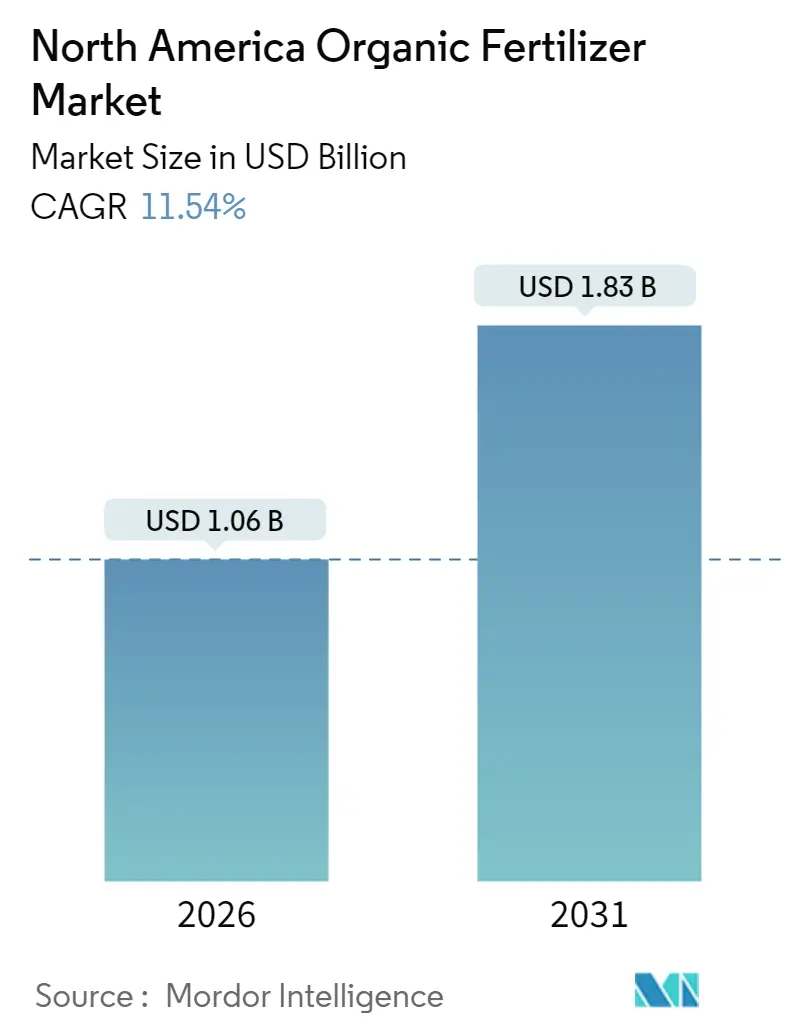

| Market Size (2026) | USD 1.06 Billion |

| Market Size (2031) | USD 1.83 Billion |

| Growth Rate (2026 - 2031) | 11.54% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Organic Fertilizer Market Analysis by Mordor Intelligence

The North America organic fertilizer market is expected to grow from USD 0.95 billion in 2025 to USD 1.06 billion in 2026 and is forecast to reach USD 1.83 billion by 2031 at 11.54% CAGR over 2026-2031. Growth is fueled by expanding certified organic acreage, wider use of precision-ag liquid applicators, and federal carbon-credit programs that reward manure conversion projects. Rapid scale-up of controlled-environment farms, local food-waste digestate mandates, and the launch of biopolymer-coated granules that pair humic acids with algae extracts are further improving nutrient-use efficiency and driving uptake. Investments from both government grants and private capital shorten payback periods for new composting and bio-processing facilities, which strengthens regional supply chains and keeps freight costs contained. These converging factors sustain a robust demand outlook for the North America organic fertilizer market through the decade.

Key Report Takeaways

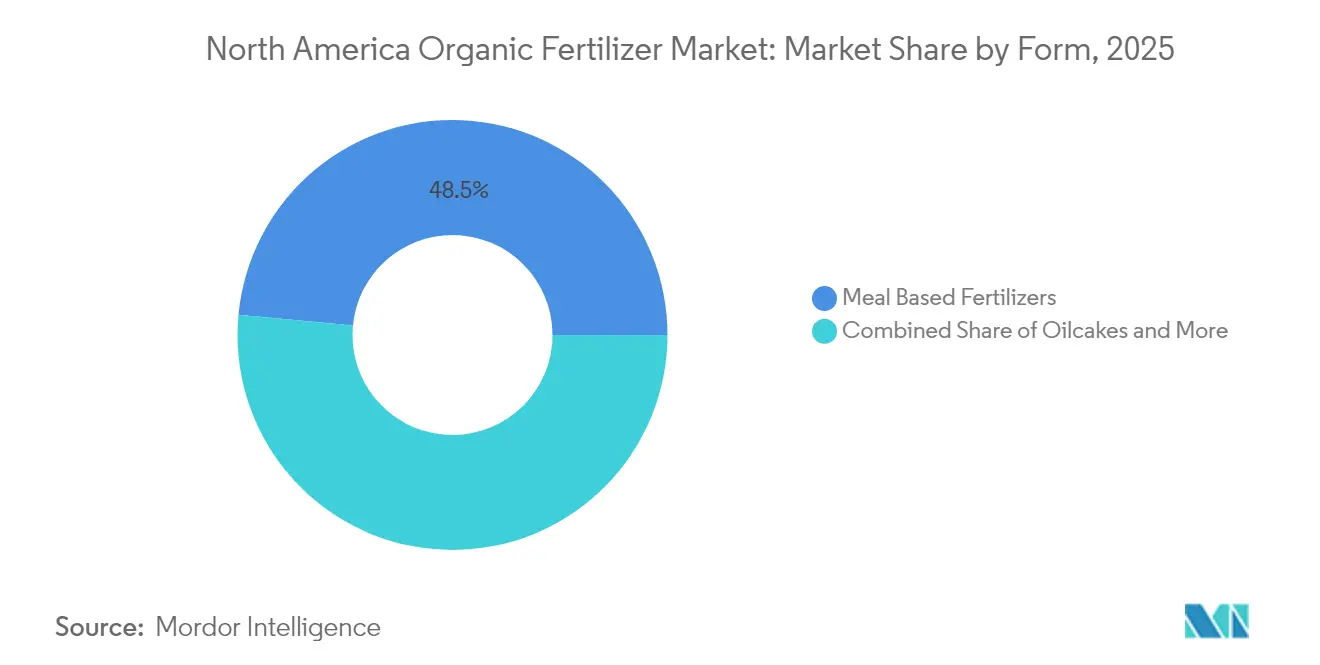

- By Form, meal-based products held 48.50% of the North America organic fertilizer market share in 2025, while manure-based fertilizers are projected to expand at a 11.76% CAGR through 2031, the fastest among all forms.

- By Crop Type, row crops accounted for a 52.10% share of the North America organic fertilizer market size in 2025 and are advancing at an 11.62% CAGR to 2031.

- By Geography, the United States captured 40.85% revenue share of the North America organic fertilizer market in 2025 while registering a 12.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Organic Fertilizer Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding certified organic acreage | +2.1% | United States, Canada, and Mexico | Medium term (2-4 years) |

| Precision-ag liquid application systems boost adoption of low-viscosity organics | +1.8% | United States, Canada | Short term (≤ 2 years) |

| USDA carbon-credit pilots rewarding manure-to-fertilizer projects | +1.5% | United States | Medium term (2-4 years) |

| Rapid scale-up of controlled-environment agriculture (CEA) in the U.S. and Canada | +1.3% | United States, Canada | Long term (≥ 4 years) |

| Municipal food-waste digestate mandates create local supply pools | +1.2% | United States, select Canadian provinces | Short term (≤ 2 years) |

| Biopolymer-coated granules integrating humic acids with algae extracts boost nutrient uptake efficiency | +2.0% | North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Certified Organic Acreage

Certified organic farmland keeps growing as farmers switch from synthetics to inputs approved under the United States Department of Agriculture National Organic Program. California leads with more than 2.13 million certified acres that generated USD 14.0 billion in organic sales during 2024. Mexico now counts 48,874 certified operators spanning all 32 states and benefits from an equivalence agreement with Canada that remains in force until 2027. Every new acre needs Organic Materials Review Institute-listed nutrients, and that requirement funnels predictable demand toward North America organic fertilizer market suppliers. Structured standards also shield compliant producers from lower-grade imports, supporting premium pricing.

Precision-ag Liquid Application Systems Boost Adoption of Low-viscosity Organics

Variable-rate sprayers, satellite guidance, and cloud-based decision tools are used on more than 60% of North American row-crop acres. These platforms work best with low-viscosity organic liquids that move through nozzles without clogging. Real-time soil testing data guide exact placement, which raises nutrient-use efficiency and lowers cost per harvested acre. Because the equipment is already on farms, growers can switch to compatible organics without large capital outlays, accelerating usage within the North America organic fertilizer market.

USDA Carbon-credit Pilots Rewarding Manure-to-fertilizer Projects

The Climate-Smart Commodities program grants carbon credits to anaerobic digestion and vermicomposting projects that prove methane capture and reduced synthetic displacement. Central Coast Worm Farm, for example, is scaling capacity to 158,000 metric tons per year after securing USD 4.2 million in grant funding. Credits and fertilizer sales create two revenue channels that improve project returns, prompting new builds in dairy and poultry regions. As more facilities come online, local supply pools deepen, and logistics costs fall, reinforcing the growth of the North America organic fertilizer market.

Biopolymer-Coated Granules Integrating Humic Acids with Algae Extracts Boost Nutrient Uptake Efficiency

New granulated fertilizers encapsulate mineral nutrients inside biodegradable polymers that bond humic acids with cold-water algae extracts. The humic fraction chelates micronutrients, keeping them in plant-available form, while algae metabolites supply natural growth stimulants that improve root architecture. Field trials across Midwestern corn and Canadian canola acres show higher early-season chlorophyll readings and a 10-15% reduction in total applied nitrogen compared with legacy organic meals. Because the coating controls moisture release, the granules flow smoothly through both pneumatic spreaders and precision planter boxes, aligning with variable-rate prescriptions already in use on large farms. Manufacturers position the product as a drop-in replacement for traditional pellets, which lowers switching costs and accelerates adoption across the North America organic fertilizer market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inconsistent nutrient analysis across batches | -1.4% | North America | Short term (≤ 2 years) |

| Short shelf-life for high-moisture liquids in warmer states | -1.1% | Southern United States, Mexico | Short term (≤ 2 years) |

| Slow-release profile mismatched to short-season row crops | -0.9% | Northern United States, Canada | Medium term (2-4 years) |

| Persistent heavy-metal limits in some recycled waste streams | -1.3% | North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Inconsistent Nutrient Analysis Across Batches

Organic fertilizers often show variable nitrogen, phosphorus, and potassium content because feedstock composition changes with season and processing method. This inconsistency complicates precision application, slows regulatory approvals, and forces extra laboratory tests that small producers cannot always afford. Without harmonized quality metrics across federal and state lines, manufacturers face fragmented compliance requirements that delay product launches and limit scalable growth for the North America organic fertilizer market.[1]Source: U.S. Environmental Protection Agency, “Sewage Sludge Standards,” EPA, epa.gov

Short Shelf-life for High-moisture Liquids in Warmer States

High-moisture formulations deteriorate quickly at temperatures common in southern U.S. states and Mexico. Microbial spoilage reduces nutrient content and clogs distribution lines, pushing dealers toward dry meal or pellet products. Maintaining a cold chain adds cost that erodes the pricing advantage of liquid organic fertilizers. Until stabilization chemistries become mainstream, this factor will hold back volume gains in the warmest sub-regions of the North America organic fertilizer market.

Segment Analysis

By Form: Meal-Based Dominance Anchored by Consistent Quality

Meal-based products captured 48.50% of total sales in 2025, the largest slice of the North America organic fertilizer market share, because steam-sterilized ingredients yield predictable nutrient profiles that pass regulatory audits. Processing removes pathogens and extends shelf life, giving distributors confidence in inventory planning. Manufacturers blend soybean meal, bone meal, and feather meal to customize nitrogen release curves that align with precision agriculture prescriptions. Manure-based fertilizers are growing fastest at a 11.76% CAGR as municipal digestate rules and on-farm composting projects deliver steady feedstock streams. Technology investments such as forced-air static piles and biochar inoculation minimize odor and speed maturation, closing the quality gap with meals. Emerging sub-categories like biochar-enhanced pellets and micro-algae powders find niche demand among high-value horticulture operators looking for carbon-rich amendments. Innovations across the form segment make it a central battleground for suppliers aiming to raise share in the North America organic fertilizer market.

The North America organic fertilizer market value for meal-based products is expected to grow steadily through 2031, highlighting the segment's increasing importance in row-crop rotations, where reliability and consistency are prioritized over nutrient density. Producers highlight audit-ready formulations that lower documentation burdens under organic certification. In parallel, manure-based lines ride cost advantages where local livestock waste offers negative feedstock costs and carbon-credit upside. Oilcakes, led by neem and castor seed products, maintain niche status for specialty fruit and nut crops because slow nitrogen release matches long growing cycles. Processors continue to expand capacity as CalRecycle grants unlock USD 130 million for feedstock-to-fertilizer infrastructure in California, adding to total supply available to the North America organic fertilizer market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Crop Type: Row Crops Provide Scale and Momentum

Row crops, chiefly corn, soybeans, and wheat, consumed 52.10% of value in 2025 and will preserve leadership with an 11.62% CAGR through 2031, supported by improved biological nitrogen fixation technologies. Federal crop insurance now recognizes organic practices, reducing risk and encouraging acreage shifts. Precision equipment owned by commodity producers spreads fixed costs over thousands of acres, making organic inputs cost-competitive on a per-bushel basis.

Horticultural crops contribute lower tonnage yet command premium pricing because growers seek residue-free inputs that satisfy export and retail standards. Certified organic blueberries, lettuce, and greenhouse tomatoes fetch price premiums that justify organic fertilizer adoption despite higher unit costs. Cash crops such as specialty grains and pulses post moderate growth as contract buyers stipulate organic credentials for value-added processing. Each crop group presents unique nutrient timing needs, prompting manufacturers to widen portfolios. Tailored offerings help firms win share in the North America organic fertilizer market, where one-size-fits-all formulas no longer suffice.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The United States generated 40.85% of regional revenue in 2025 and is on track for a 12.11% CAGR through 2031, the quickest among country markets. New domestic production grants worth USD 32 million have lowered entry barriers for small composters, while high-density organic clusters in California, Washington, and New York guarantee local demand. The state of California alone maintains more than 2.13 million certified acres, underpinning robust offtake for premium inputs across fresh produce supply chains. Canada ranks second in value, aided by continued mutual recognition of standards with Mexico and the United States, which cuts testing redundancy and speeds cross-border shipments.

Ongoing investment in controlled-environment agriculture also drives uptake of water-soluble organics that can circulate in hydroponic systems without clogging pumps. Government financing through Fideicomisos Instituidos en Relación con la Agricultura (FIRA) covers up to 80% of biofertilizer costs, lowering barriers for smallholders.

Certified acreage spans coffee, avocado, and maize zones, ensuring broad-based demand. Certification body Certimex’s ongoing approval by the European Union secures export channels and reinforces adherence to stringent nutrient standards. The Rest of North America comprises island economies and U.S. territories where specialty crops dominate. Limited arable area concentrates demand on high-value formulations, yet import logistics inflate landed costs, giving domestic composters an edge if they can secure waste streams. While small in absolute terms, these markets serve as test beds for innovative formulations that later scale into the wider North America organic fertilizer market.

Competitive Landscape

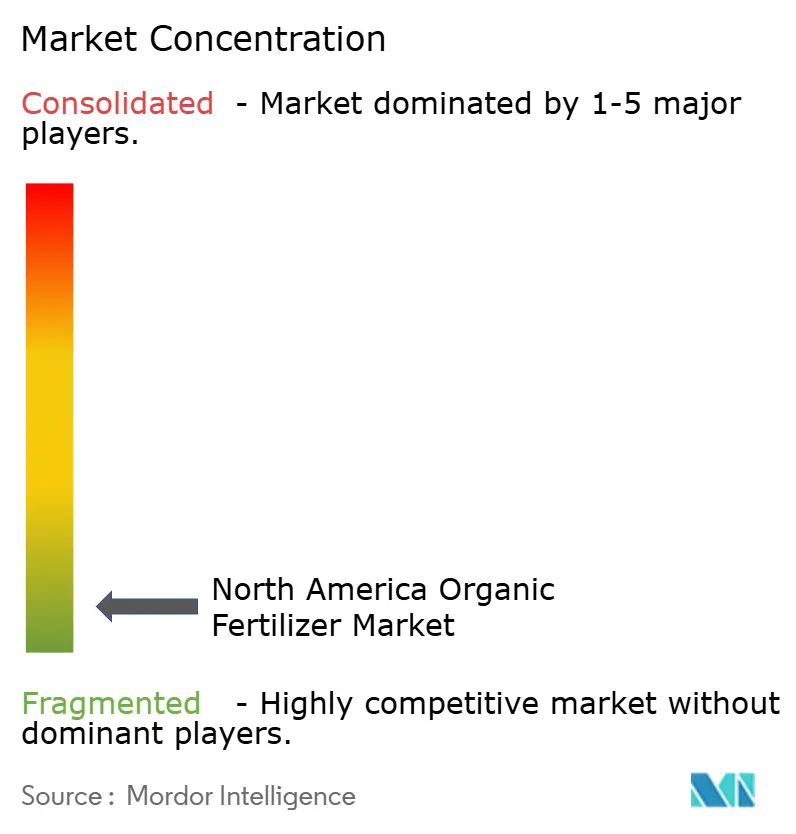

The North America organic fertilizer market remains highly fragmented. Cedar Grove Composting Inc., E.B. Stone and Sons Inc., Sustane Natural Fertilizer, The Espoma Company, and California Organic Fertilizers Inc. together accounted for a limited revenue share of 2024, underscoring the absence of dominant national brands. Each operates with a distinct raw-material focus: green-waste compost, specialty soil blends, municipal biosolids, consumer packaged meals, and organic liquids, so direct head-to-head overlap remains limited.

Cedar Grove Composting Inc. runs large in-vessel tunnels near Seattle and has adopted hybrid electric collection trucks that trim fuel use by 25% while lowering feedstock haul-in costs. E.B. Stone and Sons Inc. finished a new organic potting-mix line in Dixon, California, to support West Coast garden-center demand and shorten delivery lead times. Sustane Natural Fertilizer expanded its Cannon Falls, Minnesota, plant in 2024, lifting dried biosolid pellet capacity to 80,000 metric tons per year and adding a dedicated line for 8-2-4 granules aimed at row-crop applicators. These capacity moves anchor localized scale advantages yet keep overall regional share diluted.

The Espoma Company invested in an online soil-test kit and recommendation portal in 2025 so retail buyers can match Bio-tone fertilizers to crop-specific nutrient gaps, improving brand stickiness. California Organic Fertilizers Inc. introduced an Organic Materials Review Institute-listed 5-1-5 liquid fish hydrolysate in early 2024 that flows through variable-rate sprayers, addressing precision-ag compatibility needs. Across the board, players ally with equipment makers and digital agronomy platforms to prove return on investment, a key purchase trigger for large-acreage growers. The competitive field, therefore, rewards innovation in processing, product formulation, and data-supported application rather than sheer production volume.

North America Organic Fertilizer Industry Leaders

California Organic Fertilizers Inc.

Cedar Grove Composting Inc.

E.B.Stone & Sons Inc.

Suståne Natural Fertilizer Inc.

The Espoma Company

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2025: Nitricity, a U.S.-based agri-tech company, has raised USD 50 million to expand its technology that transforms almond waste into organic fertilizer. This funding will facilitate its growth across North America and internationally to deliver sustainable, locally sourced fertilizer solutions. The initiative aligns with the increasing demand for organic and regenerative agriculture in the region.

- August 2024: Solugen Global has developed Azogen 5-0-0, a liquid organic-friendly nitrogen fertilizer made from pig manure. The product targets fruit and vegetable growers in the U.S. and will be showcased at the Organic Grower Summit 2024.

North America Organic Fertilizer Market Report Scope

The North America Organic Fertilizer Market Report is Segmented by Form (Manure, Meal-Based Fertilizers, and Oilcakes), Crop Type (Cash Crops, Horticultural Crops, and Row Crops), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Form

| Manure |

| Meal Based Fertilizers |

| Oilcakes |

| Other Organic Fertilizer |

Crop Type

| Cash Crops |

| Horticultural Crops |

| Row Crops |

Country

| Canada |

| Mexico |

| United States |

| Rest of North America |

| Form | Manure |

| Meal Based Fertilizers | |

| Oilcakes | |

| Other Organic Fertilizer | |

| Crop Type | Cash Crops |

| Horticultural Crops | |

| Row Crops | |

| Country | Canada |

| Mexico | |

| United States | |

| Rest of North America |

Need A Different Region or Segment?

Customize Now

Market Definition

- AVERAGE DOSAGE RATE - The average application rate is the average volume of organic fertilizers applied per hectare of farmland in the respective region/country.

- CROP TYPE - Crop type includes Row crops (Cereals, Pulses, Oilseeds), Horticultural Crops (Fruits and vegetables) and Cash Crops (Plantation Crops, Fibre Crops and Other Industrial Crops)

- FUNCTION - The crop nutrition function of agricultural biological consists of various products that provide essential plant nutrients and enhance soil quality.

- TYPE - Organic fertilizers are applied to provide essential crop nutrients and enhance the soil quality.

| Keyword | Definition |

|---|---|

| Cash Crops | Cash crops are non-consumable crops sold as a whole or part of the crop to manufacture end-products to make a profit. |

| Integrated Pest Management (IPM) | IPM is an environment-friendly and sustainable approach to control pests in various crops. It involves a combination of methods, including biological controls, cultural practices, and selective use of pesticides. |

| Bacterial biocontrol agents | Bacteria used to control pests and diseases in crops. They work by producing toxins harmful to the target pests or competing with them for nutrients and space in the growing environment. Some examples of commonly used bacterial biocontrol agents include Bacillus thuringiensis (Bt), Pseudomonas fluorescens, and Streptomyces spp. |

| Plant Protection Product (PPP) | A plant protection product is a formulation applied to crops to protect from pests, such as weeds, diseases, or insects. They contain one or more active substances with other co-formulants such as solvents, carriers, inert material, wetting agents or adjuvants formulated to give optimum product efficacy. |

| Pathogen | A pathogen is an organism causing disease to its host, with the severity of the disease symptoms. |

| Parasitoids | Parasitoids are insects that lay their eggs on or within the host insect, with their larvae feeding on the host insect. In agriculture, parasitoids can be used as a form of biological pest control, as they help to control pest damage to crops and decrease the need for chemical pesticides. |

| Entomopathogenic Nematodes (EPN) | Entomopathogenic nematodes are parasitic roundworms that infect and kill pests by releasing bacteria from their gut. Entomopathogenic nematodes are a form of biocontrol agents used in agriculture. |

| Vesicular-arbuscular mycorrhiza (VAM) | VAM fungi are mycorrhizal species of fungus. They live in the roots of different higher-order plants. They develop a symbiotic relationship with the plants in the roots of these plants. |

| Fungal biocontrol agents | Fungal biocontrol agents are the beneficial fungi that control plant pests and diseases. They are an alternative to chemical pesticides. They infect and kill the pests or compete with pathogenic fungi for nutrients and space. |

| Biofertilizers | Biofertilizers contain beneficial microorganisms that enhance soil fertility and promote plant growth. |

| Biopesticides | Biopesticides are natural/bio-based compounds used to manage agricultural pests using specific biological effects. |

| Predators | Predators in agriculture are the organisms that feed on pests and help control pest damage to the crops. Some common predator species used in agriculture include ladybugs, lacewings, and predatory mites. |

| Biocontrol agents | Biocontrol agents are living organisms used to control pests and diseases in agriculture. They are alternatives to chemical pesticides and are known for their lesser impact on the environment and human health. |

| Organic Fertilizers | Organic fertilizer is composed of animal or vegetable matter used alone or in combination with one or more non-synthetically derived elements or compounds used for soil fertility and plant growth. |

| Protein hydrolysates (PHs) | Protein hydrolysate-based biostimulants contain free amino acids, oligopeptides, and polypeptides produced by enzymatic or chemical hydrolysis of proteins, primarily from vegetal or animal sources. |

| Biostimulants/Plant Growth Regulators (PGR) | Biostimulants/Plant Growth Regulators (PGR) are substances derived from natural resources to enhance plant growth and health by stimulating plant processes (metabolism). |

| Soil Amendments | Soil Amendments are substances applied to soil that improve soil health, such as soil fertility and soil structure. |

| Seaweed Extract | Seaweed extracts are rich in micro and macronutrients, proteins, polysaccharides, polyphenols, phytohormones, and osmolytes. These substances boost seed germination and crop establishment, total plant growth and productivity. |

| Compounds related to biocontrol and/or promoting growth (CRBPG) | Compounds related to biocontrol or promoting growth (CRBPG) are the ability of a bacteria to produce compounds for phytopathogen biocontrol and plant growth promotion. |

| Symbiotic Nitrogen-Fixing Bacteria | Symbiotic nitrogen-fixing bacteria such as Rhizobium obtain food and shelter from the host, and in return, they help by providing fixed nitrogen to the plants. |

| Nitrogen Fixation | Nitrogen fixation is a chemical process in soil which converts molecular nitrogen into ammonia or related nitrogenous compounds. |

| ARS (Agricultural Research Service) | ARS is the U.S. Department of Agriculture's chief scientific in-house research agency. It aims to find solutions to agricultural problems faced by the farmers in the country. |

| Phytosanitary Regulations | Phytosanitary regulations imposed by the respective government bodies check or prohibit the importation and marketing of certain insects, plant species, or products of these plants to prevent the introduction or spread of new plant pests or pathogens. |

| Ectomycorrhizae (ECM) | Ectomycorrhiza (ECM) is a symbiotic interaction of fungi with the feeder roots of higher plants in which both the plant and the fungi benefit through the association for survival. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.

Get More Details On Research Methodology

Download PDF