Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

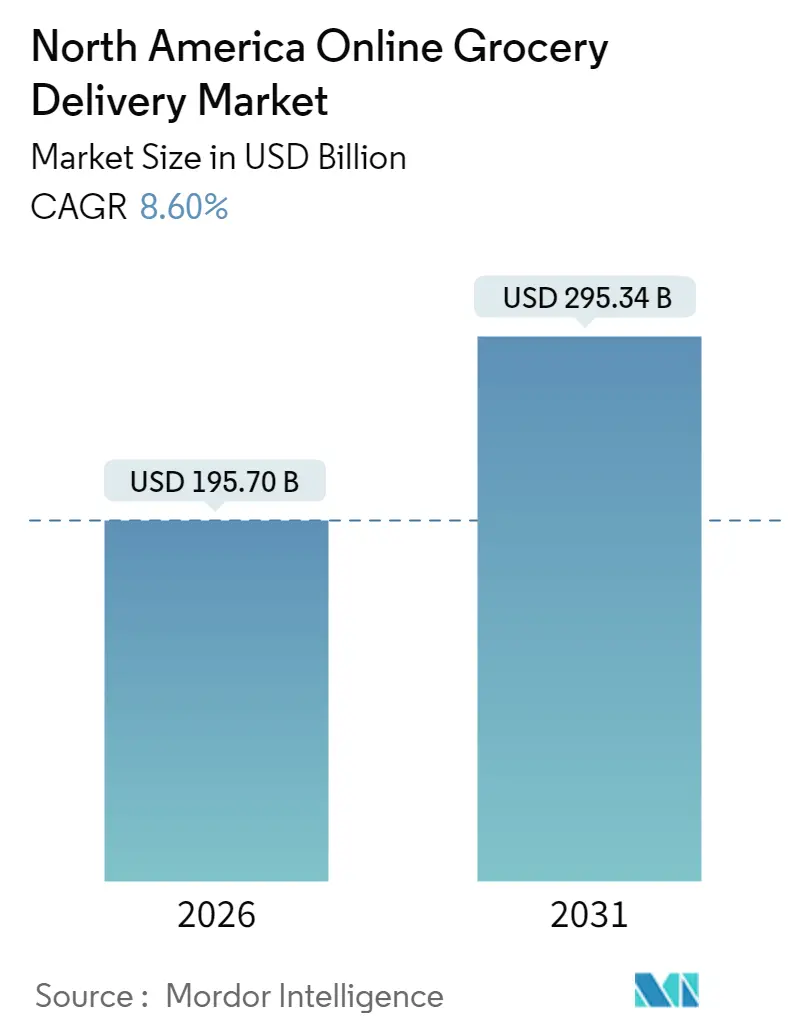

| Market Size (2026) | USD 195.7 Billion |

| Market Size (2031) | USD 295.34 Billion |

| Growth Rate (2026 - 2031) | 8.60% CAGR |

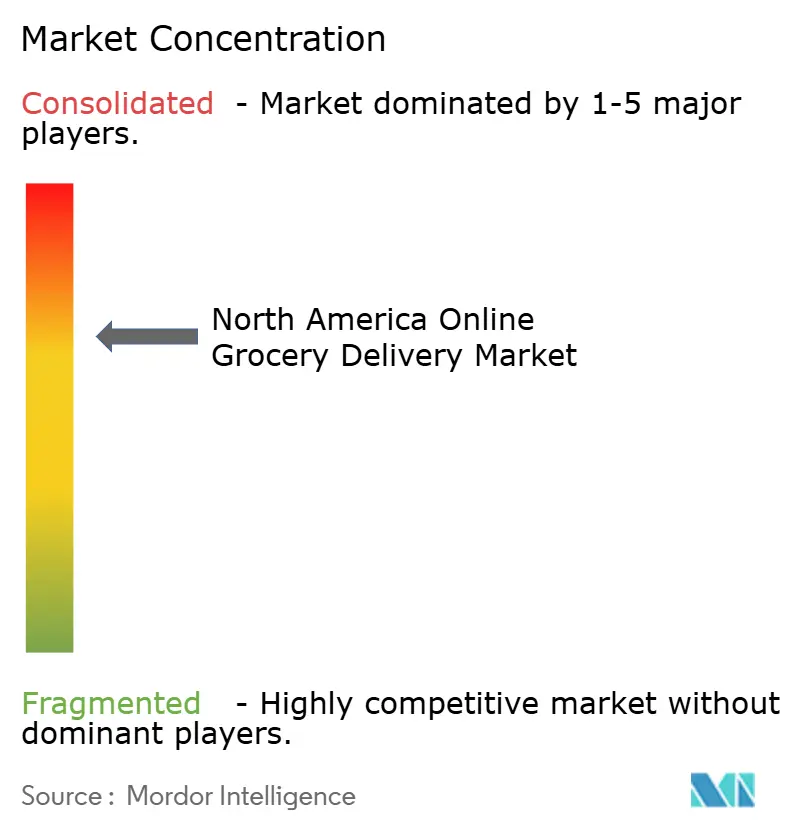

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Online Grocery Delivery Market Analysis by Mordor Intelligence

North America online grocery delivery market size in 2026 is estimated at USD 195.7 billion, growing from 2025 value of USD 180.2 billion with 2031 projections showing USD 295.34 billion, growing at 8.60% CAGR over 2026-2031. Structural shifts such as subscription programs, the digitization of SNAP benefits, and record-high infrastructure investment have made digital grocery a permanent habit rather than a pandemic spike. Established omnichannel retailers leverage their store footprints as last-mile nodes, while pure-play platforms double down on data-driven personalization to protect share. Same-day fulfilment networks, AI-assisted demand planning, and low-emission vehicle rollouts lower unit costs and raise service quality. Together, these forces set a clear path for sustained volume gains in the North America online grocery delivery market. [1]Walmart Investor Relations, “May 15, 2025 – Form 8-K Current Report,” stock.walmart.com

Key Report Takeaways

- By product type, retail delivery led with 62.38% of the North America online grocery delivery market share in 2025, whereas quick commerce is forecast to grow at 20.3% CAGR through 2031.

- By delivery speed, same-day services captured 45.35% of the North America online grocery delivery market size in 2025, while instant delivery under two hours is expected to advance at 25.9% CAGR to 2031.

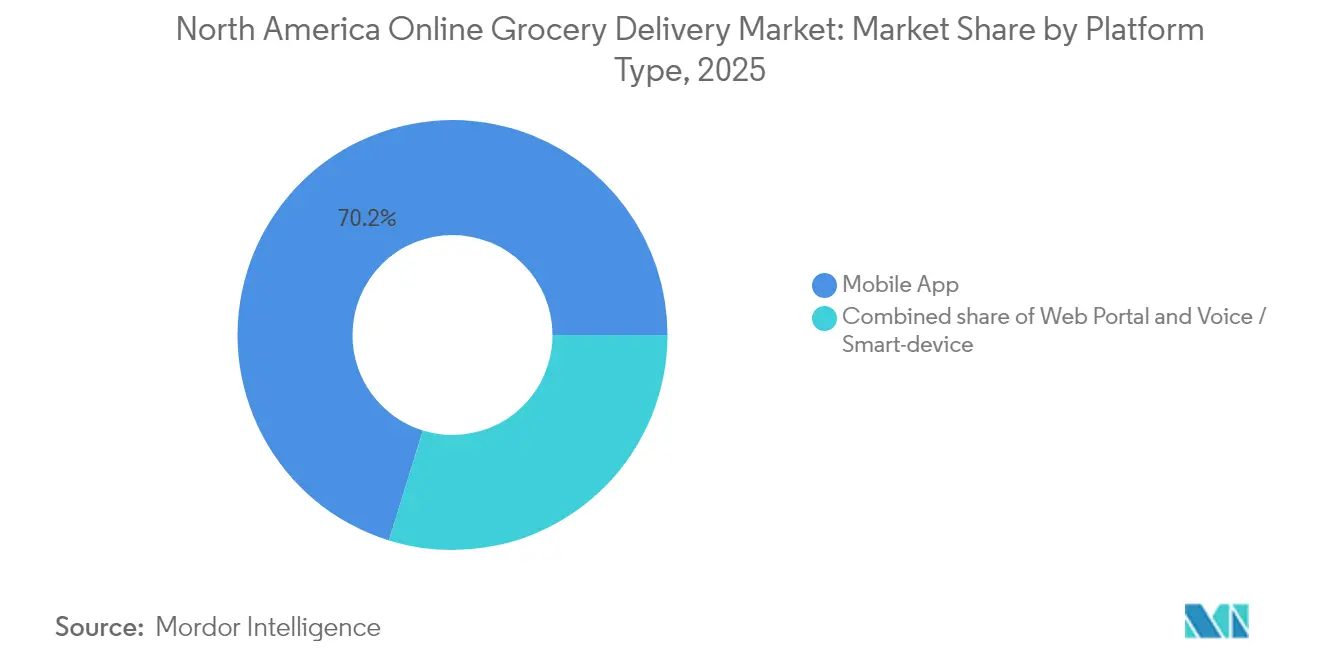

- By platform type, mobile apps dominated with 70.22% revenue share in 2025; voice and smart-device interfaces show the fastest projected CAGR at 17.2% through 2031.

- By customer type, household consumers accounted for 90.35% share of the North America online grocery delivery market size in 2025, but corporate and institutional demand is set to grow 13.6% annually through 2031.

- By country, the United States retained 85.60% of the North America online grocery delivery market share in 2025, whereas Mexico is on track for a 15.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Online Grocery Delivery Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subscription services' recurring-revenue flywheel | 1.80% | North America, with strongest adoption in US urban markets | Medium term (2-4 years) |

| SNAP Online expansion & EBT digitisation | 1.20% | US nationwide, with concentrated impact in food desert regions | Short term (≤ 2 years) |

| Same-day fulfilment infrastructure roll-out | 2.10% | US metropolitan areas, expanding to Canada secondary markets | Medium term (2-4 years) |

| AI-powered demand-forecasting for perishables | 0.90% | Global, with early deployment in US and Canadian operations | Long term (≥ 4 years) |

| Dark-store micro-fulfilment economics | 1.40% | US urban cores, pilot expansion to Mexico City | Medium term (2-4 years) |

| ESG-led switch to low-emission last-mile fleets | 0.70% | California leading, spreading to Northeast US and Canadian provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Subscription Services’ Recurring-Revenue Flywheel

Paid memberships such as Walmart+ convert one-off shoppers into predictable, high-frequency customers. Bundled perks—free delivery, fuel discounts, streaming content—reduce churn and lift average order frequency, letting retailers subsidize shipping without eroding margin. Amazon, Safeway and regional grocers alike exploit first-party data from subscriptions to personalize offers and optimize inventory, deepening competitive moats around scale.

SNAP Online Expansion & EBT Digitization

Forty-one million SNAP participants now enjoy digital purchase capability, after the USDA expanded the program to every state in 2024. Kroger, DoorDash and Shipt quickly integrated EBT check-out, unlocking incremental demand from food-insecure households and cutting fraud through chip-enabled cards. California’s statewide chip-and-tap rollout beginning January 2025 accelerates the shift, widening the addressable base for the North America online grocery delivery market. [2]U.S. Department of Agriculture, “USDA Continues Expanding SNAP Online Shopping,” fns.usda.gov

Same-Day Fulfilment Infrastructure Roll-Out

Amazon serves 40 million U.S. shoppers with same-day delivery, while Walmart lifted <3-hour deliveries by 91% in 2025 through store-based micro-fulfilment. Regional chains such as Save Mart deploy automated dark stores to cut pick times, proving that robotics can level the playing field against national giants. Speed now trumps price once networks hit scale, evidenced by 30% of Walmart customers opting to pay extra for accelerated service.

AI-Powered Demand Forecasting for Perishables

Algorithms ingest sales trends, weather data and promotions to predict fresh-item demand, lowering waste by up to 25% and reducing stockouts. Albertsons’ DC Forecasts tool already automates purchasing across 17 U.S. distribution centers. Independent grocers adopt cloud-based AI suites to remain competitive on availability despite lower volumes, reinforcing data scale as a barrier to entry.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Last-mile cost inflation outpacing basket value | -2.30% | North America, particularly US metropolitan areas | Short term (≤ 2 years) |

| Driver & warehouse labour shortages | -1.70% | US and Canada, acute in urban centers | Medium term (2-4 years) |

| Cold-chain capacity bottlenecks | -1.10% | North America, concentrated in secondary markets | Medium term (2-4 years) |

| Municipal fee caps & Proposition-22 style rules | -0.80% | California leading, potential spread to other states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Last-Mile Cost Inflation Outpacing Basket Value

Urban minimum-wage ordinances for gig workers lift delivery costs faster than basket values grow. Platforms must choose between absorbing losses or raising fees, pressuring unit economics in the North America online grocery delivery market. Regulatory scrutiny of fee structures, such as the CFPB’s probe into Walmart, compounds compliance expense.

Driver & Warehouse Labor Shortages

The trucking sector may face a 160,000-driver shortfall by 2030, intensifying wage competition for last-mile couriers and fulfilment staff. Walmart has automated 45% of U.S. eCommerce operations to offset labour scarcity, highlighting automation’s role as both cost lever and strategic hedge.

Segment Analysis

By Product Type: Retail Delivery Retains Leadership

Retail delivery held 62.38% of the North America online grocery delivery market share in 2025. Consumers favour full-basket shopping that mirrors in-store experiences, driving sustained volume through omnichannel retailers. Quick commerce, though only a minority today, is the fastest-growing slice at a 20.3% CAGR thanks to urban demand for immediacy. Meal-kit providers face margin pressure as HelloFresh anticipates double-digit revenue decline, while supermarkets roll out in-house kits to win back share.

Quick commerce startups like Gopuff launch convenience hubs across major metros, but unit profitability hinges on dense order pools and premium fees. Specialty ethnic and wellness categories gain traction as demographic diversity rises. Pharmacy integration boosts basket size, reinforcing the revenue potential embedded within the North America online grocery delivery market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Delivery Speed: Same-Day Becomes Table Stakes

Same-day options commanded 45.35% of the North America online grocery delivery market size in 2025 and continue to expand as retailers retrofit stores into micro-fulfilment nodes. Instant services promise sub-2-hour turnaround and are projected to grow at 25.9% CAGR. Yet sustainability of ultra-rapid delivery remains in question outside dense cores, where order density fails to absorb high fixed costs.

Next-day delivery survives for bulk pantry staples and value-oriented customers. Platforms now segment service levels, charging premiums for speed while keeping standard tiers price-competitive, allowing refined revenue management across the North America online grocery delivery market.

By Platform Type: Mobile Apps Dominate, Voice Rises

Mobile apps captured 70.22% share in 2025, benefiting from mature UX design and in-app loyalty features. Voice assistants recorded the highest growth trajectory at 17.2% CAGR, with Amazon Alexa enabling hands-free reorders and predictive replenishment that blurs shopping into an ambient experience. Web portals remain indispensable for corporate buyers who need bulk uploads and invoice management.

Augmented-reality shelf browsing and smart-fridge sensors inch closer to mainstream, underscoring how digital interfaces widen the funnel for the North America online grocery delivery industry.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Customer Type: Households Anchor Volume; Corporates Accelerate

Households accounted for 90.35% of 2025 revenues, validating grocery’s historic consumer focus. Corporate and institutional customers, however, are expanding at 13.6% annually. Offices, hospitals and universities increasingly outsource pantry management for employee retention and operational simplicity. Larger baskets and predictable cycles enhance margin, turning B2B an attractive growth avenue inside the North America online grocery delivery market.

Geography Analysis

The United States drives the lion’s share of demand, with the North America online grocery delivery market size in the country mirroring overall regional growth. Robust SNAP participation, same-day networks serving 40 million addresses, and omnichannel leaders such as Walmart (37% eGrocery share) create a high barrier to new entrants. Californian zero-emission mandates push fleets toward electric vans, while the Northeast prioritizes dense-city logistics and the Southeast focuses on suburban pickup models.

Canada contributes a smaller but stable slice, leveraging a CAD 6.5 billion investment by Walmart to expand Supercentres and modernize supply chains. Domestic chains like Loblaw counter U.S. brands through locally tailored assortments and loyalty ecosystems. Click-and-collect remains prominent, reflecting lower urban density outside Toronto and Vancouver.

Mexico offers the steepest curve, propelled by Walmex’s plan to add 1,500 stores and two robotics-equipped DCs by 2030. eCommerce sales rose 25% to USD 34 billion in 2024, yet online penetration in grocery sits in single digits, indicating ample runway. Local sourcing (83% of goods made in Mexico) bolsters supplier networks and keeps pricing competitive, positioning Mexico as a breakout contributor to the North America online grocery delivery market.

Competitive Landscape

Competition intensifies as physical retailers weaponize store networks to match pure-play speed. Walmart’s omnichannel model, Instacart’s platform economics, and Amazon’s robotics-driven fulfilment illustrate diverging strategies converging on scale and data mastery. Patent filings for autonomous delivery, such as DoorDash’s vehicle-to-third-party communication system, underscore a race toward capital-heavy logistics innovation.

Retail media networks emerge as lucrative adjacencies—Instacart’s 2024 ad revenue topped USD 1 billion, while Walmart Connect grew 26%—monetizing supplier budgets and insulating margins. Quick commerce remains a contested niche; players experiment with 20-minute promises yet grapple with profitability outside dense urban pockets. Smaller grocers pursue differentiation via sustainable packaging and local provenance rather than speed, carving defensible micro-segments inside the vast North America online grocery delivery market.

Scale economics and automation widen the gap between leaders and followers. Capital requirements for robotics, AI and EV fleets deter new entrants, suggesting the market is trending toward oligopoly with periodic niche insurgents. [4]U.S. Patent Office, “Systems for Autonomous and Automated Delivery Vehicles to Communicate with Third Parties,” uspto.report

North America Online Grocery Delivery Industry Leaders

Walmart Inc.

Amazon.com Inc.

Instacart

Costco Wholesale Corp.

The Kroger Co.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: Misfits Market acquired reuse-centric startup The Rounds, adding circular packaging capabilities and issuing USD 30 credits plus free Misfits+ to new members.

- May 2025: Instacart posted 10% GTD growth and USD 244 million adjusted EBITDA, introducing a USD 10 minimum basket for Instacart+ to push order frequency.

- April 2025: Walmart Mexico unveiled a USD 6 billion 2025 budget, targeting 1,500 new stores and two AI-powered DCs by 2030.

- March 2025: DoorDash beat EPS forecasts, grew grocery volumes and scaled drone pilots, aiming for category share leadership within 12 months.

North America Online Grocery Delivery Market Report Scope

Online grocery shopping is a way to buy food and other necessities using a web-based shopping service. People can use online shopping methods to purchase these items online.

North America's online grocery delivery market is segmented by product type (retail delivery, quick commerce, meal kit delivery) and country (United States, Canada).

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Product Type

| Retail Delivery |

| Quick Commerce (?30-min) |

| Meal-kit Delivery |

| Specialty and Ethnic Grocery |

| Pharmacy and Health Items |

By Delivery Speed

| Standard (next-day +) |

| Same-day |

| Instant (<2 hours) |

By Platform Type

| Mobile App |

| Web Portal |

| Voice / Smart-device |

By Customer Type

| Household Consumers |

| Corporate / Institutional |

By Country

| United States |

| Canada |

| Mexico |

| By Product Type | Retail Delivery |

| Quick Commerce (?30-min) | |

| Meal-kit Delivery | |

| Specialty and Ethnic Grocery | |

| Pharmacy and Health Items | |

| By Delivery Speed | Standard (next-day +) |

| Same-day | |

| Instant (<2 hours) | |

| By Platform Type | Mobile App |

| Web Portal | |

| Voice / Smart-device | |

| By Customer Type | Household Consumers |

| Corporate / Institutional | |

| By Country | United States |

| Canada | |

| Mexico |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the North America online grocery delivery market?

The market reached USD 195.7 billion in 2026 and is forecast to hit USD 295.34 billion by 2031.

Which delivery speed segment is growing fastest?

Instant services that arrive in under two hours are projected to expand at a 25.9% CAGR through 2031.

How important are subscription programs to market growth?

Subscriptions add +1.8% to the overall CAGR by boosting order frequency and lowering churn.

Which country shows the highest growth potential?

Mexico leads with a 15.95% forecast CAGR thanks to large-scale investment and rising smartphone adoption.

What technologies most reduce operating costs?

AI demand forecasting and automated micro-fulfilment cut waste and labour needs, directly improving unit economics.

Are corporate customers a meaningful opportunity?

Yes, corporate and institutional buyers are the fastest-growing customer group at 13.6% CAGR, offering larger baskets and predictable demand.