Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

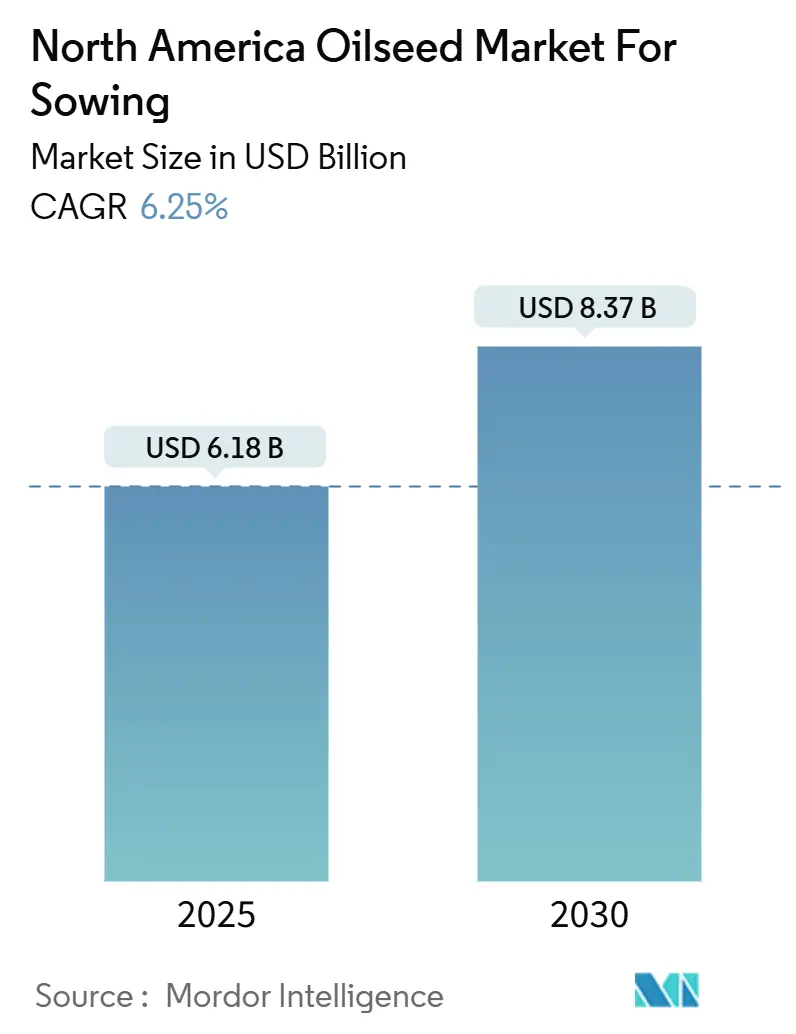

| Market Size (2025) | USD 6.18 Billion |

| Market Size (2030) | USD 8.37 Billion |

| Growth Rate (2025 - 2030) | 6.25% CAGR |

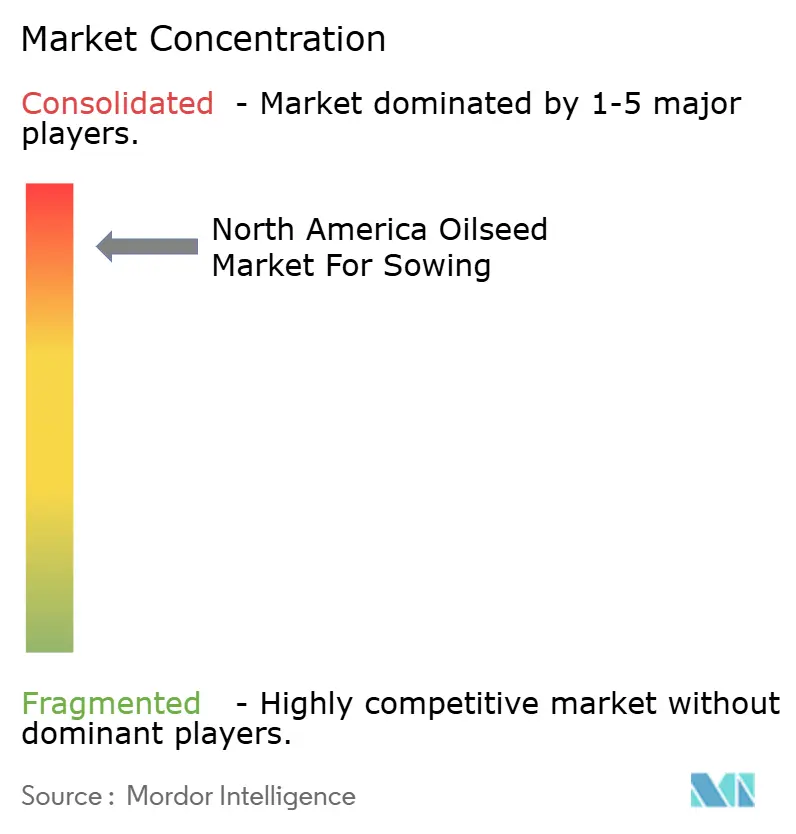

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Analysis of North America Oilseed Market For Sowing by Mordor Intelligence

The North America oilseed market for sowing size is valued at USD 6.18 billion in 2025 and is projected to reach USD 8.37 billion by 2030, advancing at a 6.25% CAGR. Rising renewable diesel mandates, record Canadian canola crushing, and almost universal adoption of herbicide-tolerant genetics are expanding demand while elevating premium seed pricing. Processors are adding capacity to capture the vegetable-oil pull from low-carbon fuel standards, and growers are prioritizing hybrids that integrate multi-trait herbicide packages to protect yields in resistance-prone fields. Weather volatility across the Corn Belt and Prairie provinces continues to disrupt planting calendars, yet seed companies are accelerating gene-edited introductions to counter climate stress. Regulatory scrutiny of herbicide chemistries is shortening product life cycles, intensifying the race for next-generation weed-management traits. Moderate market concentration persists because regional breeders retain share through localized germplasm and carbon-credit-aligned cover-crop offerings that complement multinational portfolios.

Key Report Takeaways

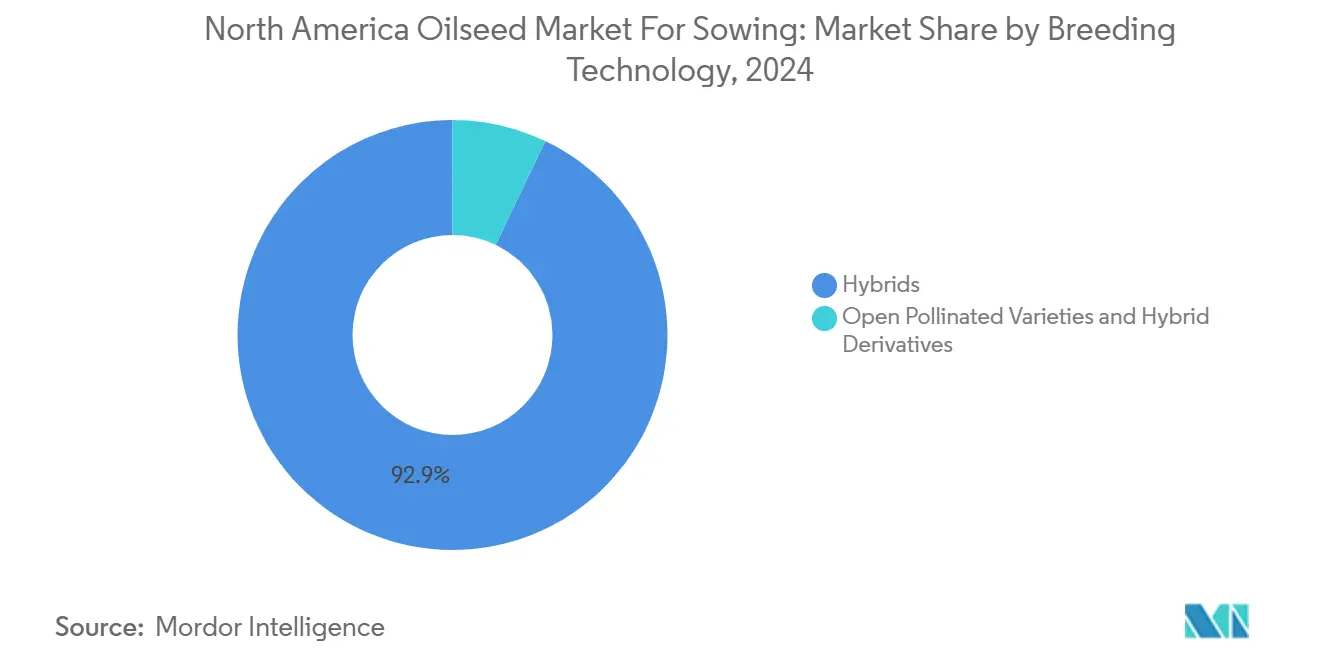

- By breeding technology, hybrids led with 92.9% market share of the North America oilseed market for sowing in 2024, and hybrids are forecast to expand at a 6.30% CAGR through 2030.

- By crop type, soybean accounted for a 77.9% market share of the North America oilseed market for sowing size in 2024 and is advancing at a 6.77% CAGR through 2030.

- By geography, the United States held 74.9% market share of the North America oilseed market for sowing in 2024, and is projected to grow at a 6.72% CAGR to 2030.

Insights and Trends of North America Oilseed Market For Sowing

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renewable diesel-driven demand surge for vegetable oils | +1.8% | United States and Canada, with spillover to Mexico | Medium term (2-4 years) |

| Rapid on-farm adoption of herbicide-tolerant GM traits | +1.2% | The United States and Canada primarily | Short term (≤ 2 years) |

| Record Canadian canola acreage expansion | +0.9% | Canada, with export implications for North America | Medium term (2-4 years) |

| Dicamba exit accelerates 2,4-D-based trait replacement cycle | +0.7% | United States Midwest and Plains states | Short term (≤ 2 years) |

| Carbon-credit programs stimulate sunflower and flax cover-crop seed demand | +0.5% | The United States and Canada, concentrated in the Prairie provinces | Long term (≥ 4 years) |

| High-oleic soybean contract premiums reshape seed mix | +0.4% | United States Midwest, expanding to Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Renewable-Diesel Driven Demand Surge for Vegetable Oils

United States renewable diesel capacity is on track to hit 5.9 billion gallons in 2025, more than doubling 2023 output and requiring heavy volumes of soybean and canola oil feedstocks[1]Source: U.S. Energy Information Administration, “U.S. renewable diesel production capacity continues to grow,” eia.gov. Each gallon of fuel consumes roughly 7.6 pounds of vegetable oil, so processors such as Cargill and ADM are racing to expand crush facilities designed for fuel-grade oils. The premium offered by fuel blenders over food markets is widening basis levels for high-oil varieties, steering planting decisions toward genetics that maximize oil yield per acre. Federal and state low-carbon mandates provide a multi-year demand signal that underpins processor investments and encourages growers to pivot acreage from feed grains into oilseeds.

Rapid On-Farm Adoption of Herbicide-Tolerant GM Traits

Herbicide-tolerant soybeans now cover 96% of United States acres, but grower focus has shifted from single glyphosate tolerance to triple-stacked platforms that layer glyphosate, glufosinate, and either dicamba or 2,4-D resistance. This rotation is a direct response to herbicide-resistant weeds that blanket more than 70 million acres in the United States. Trait cycling forces annual seed replacement, lifting royalty collections but also exposing farmers to steeper input costs as trait fees can represent 40% of seed invoices. Health Canada approvals keep pace, clearing transgenic soybeans and canola within months of United States authorizations and allowing simultaneous North American launches. As resistance intensifies, stacked traits become a management necessity rather than a premium option, sustaining growth in the North America oilseed market.

Record Canadian Canola Acreage Expansion

Canadian growers harvested record canola volumes in 2024 as Prairie acreage climbed and crushers operated at 11.4 million metric tons, with exports forecast at 12.5 million metric tons[2]Source: Statistics Canada, “Crushing statistics,” statcan.gc.ca. Canola oil secures a USD 0.05-0.10 per-pound premium over soybean oil because of its favorable cold-flow properties for renewable diesel blends. Virtually all Canadian hectares are planted to hybrid cultivars that deliver 15-20% yield lifts and higher oil profiles. Bayer reinforced its integrated value chain by purchasing a Lethbridge processing site for CAD 127 million (USD 94 million) in November 2024. Land availability is finite, so genetic gain through stress-tolerant hybrids remains the prime lever for output growth, supported by a streamlined Canadian variety-registration process that approved more than 20 new canola lines in 2024.

Dicamba Exit Accelerates 2,4-D-Based Trait Replacement Cycle

EPA restrictions on post-emergence dicamba after the 2024 season have pushed Midwest and Plains growers toward 2,4-D systems to protect soybean yields. Corteva’s Enlist platform is projected to extend soybean acres by 40% in 2025 as farmers seek flexible over-the-top options. The forced trait migration fuels near-term seed demand but also escalates licensing costs because growers must adopt entirely new germplasm to access the chemistry. Early field data already confirm 2,4-D-resistant weed biotypes in 12 states, indicating that the resistance treadmill is shortening and that multi-mode stacks will become standard packages. Seed companies are collaborating on next-generation constructs that combine multiple herbicide sites of action with disease and oil-content traits to sustain efficacy.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory uncertainty on GM traits and herbicide bans | -0.8% | United States and Canada, with Mexico restrictions | Long term (≥ 4 years) |

| Yield volatility from extreme weather events | -0.6% | North America-wide, concentrated in the Plains states | Short term (≤ 2 years) |

| Herbicide-resistant weed proliferation eroding trait value | -0.5% | United States Midwest and Plains, expanding to Canada | Medium term (2-4 years) |

| Rising seed prices from IP concentration hitting small growers | -0.4% | United States and Canada, affecting mid-scale operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Uncertainty on GM Traits and Herbicide Bans

Average regulatory review for new GM traits now exceeds five years in North America, inflating R&D budgets that ultimately filter into seed invoices. The EPA’s drifting stance on chemistries such as glyphosate and glufosinate raises doubts over trait longevity, complicating product-cycle planning for breeders[3]Source: U.S. Environmental Protection Agency, “EPA Announces Final Decision on Dicamba,” epa.gov. Mexico’s proposed GM corn ban underscores global policy risk and signals possible spillover into oilseed approvals. Although the Canadian Food Inspection Agency remains supportive, synchronized launches with the United States mean any delay stalls Canadian market access. Litigation from environmental groups layers added unpredictability, nudging companies to prioritize traits with clearer regulatory paths over cutting-edge gene-edited solutions that lack precedent.

Yield Volatility from Extreme Weather Events

The 2024 season combined delayed Midwest planting from excessive rain with Prairie drought that trimmed Saskatchewan canola yields by 15%. Weather shocks undermine the economics of premium hybrid seeds when yields fail to offset higher costs. Insurance offsets only partial losses, and policy premiums rise as climate volatility intensifies. Specialty crops like flax and sunflower endure tighter planting windows, magnifying exposure to spring moisture swings. Breeders are investing in abiotic-stress traits, yet payback remains uncertain without long-run weather predictability.

Segment Analysis

By Breeding Technology: Hybrids Drive Innovation Pipeline

Hybrid cultivars held 92.9% of the North America oilseed market for sowing share in 2024, and this sub-segment is set to advance at a 6.30% CAGR through 2030. Non-transgenic hybrids carve a premium niche among growers serving identity-preserved export channels that restrict GM content, yet their footprint remains small compared with transgenic stacks. Trait developers are pairing hybrid vigor with CRISPR-enabled oil-quality edits that fetch food and fuel premiums, reinforcing the North America oilseed market growth trajectory.

Open-pollinated varieties continue to shrink, sustained mainly by organic rotations where GM traits are prohibited. Hybrid derivatives built on public germplasm offer a transitional step for regional breeders lacking proprietary parents, but royalty terms often mirror full hybrids, limiting uptake. Commercial pipeline data show more than 150 fresh oilseed varieties, almost all hybrid, cleared North American registration in 2024. The intellectual property framework ensures breeders can recoup R&D investment, sustaining innovation momentum.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Crop: Soybean Dominate Renewable Fuel Transition

Soybean represented 77.9% of the North America oilseed market for sowing size in 2024 and are forecast to climb at a 6.77% CAGR to 2030. Renewable diesel demand is redirecting soybean oil away from food channels, lifting crush margins and encouraging growers to favor high-oil genetics. Premiums for high-oleic beans spur acreage migration, and stacked herbicide traits ease weed-control logistics during planting delays. Canola ranks second and benefits from record Canadian output, while rapeseed and mustard leverage shared genetics for disease resilience and cold-flow suitability in fuel blends.

Sunflower acreage is rebounding on the strength of carbon-credit programs and drought tolerance that hedges rainfall risk in marginal soils. Flax, safflower, and camelina remain niche contributors but attract R&D dollars for specialized fatty-acid profiles targeting industrial lubricants and aquaculture feed. Gene-editing tools shorten development cycles, positioning these minor crops for demand surges as new bio-based product markets mature.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The United States captured 74.9% of the North America oilseed market for sowing in 2024 and is projected to grow at a 6.72% CAGR, anchored by an unmatched renewable diesel build-out and a robust extension network that speeds trait diffusion. Crop insurance and commodity-loan programs buffer price risk, supporting higher-cost hybrid adoption even in volatile seasons. Canada follows, propelled by record canola crush and export channels that supply premium vegetable oil to global fuel refiners. Mexican production remains small, constrained by limited irrigated acreage and regulatory caution on GM traits, yet safflower and sunflower fill distinct regional niches.

Canada’s share derives from canola leadership, with 11.4 million metric tons crush in 2024 reflecting vertical integration from hybrid seed to processing. Export orientation positions Canadian growers to capture premiums in European and Asian vegetable-oil markets that value low-temperature flowability. Investments such as Bayer’s Lethbridge plant acquisition consolidate processing close to production to lower freight spreads and retain local value. CFIA’s streamlined approvals accelerate the roll-out of hybrids with higher oil or clubroot resistance that further support yield targets.

Mexico and the rest of North America remain minor contributors due to smaller land tracts and competing high-value crops. Nonetheless, sunflowers and safflowers play strategic roles in arid zones, and emerging water-saving agronomy could edge up acreage. Infrastructure gaps hamper large-scale crush development, but cross-border trade links allow domestic deficits to be covered by the United States and Canadian supply.

Competitive Landscape

Market concentration remains high, with Bayer AG, Corteva Inc., Land O’Lakes Inc., BASF SE, and Syngenta Group utilizing integrated germplasm and trait platforms to maintain scale advantages. However, regional breeders continue to succeed by developing hybrids tailored to specific soil and weather conditions. The exit from dicamba and pivot toward 2,4-D creates white space for trait innovators with differentiated herbicide modes, heightening competition. KWS and Limagrain divesting AgReliant Genetics to GDM for USD 2.1 billion in June 2025 highlights portfolio realignment among multinationals to sharpen focus on core crops and geographies.

Intellectual property strength underpins pricing power. Patent filings on stress tolerance and oil-profile edits jumped in 2024, signaling intensified R&D investment cycles. Independent firms capture niche segments by licensing traits on flexible acreage fees, but rising royalty costs limit competitiveness. Carbon-credit demand elevates sunflower and flax genetics, enabling local breeders to carve a share where multinationals lack dedicated programs. Gene-editing start-ups target camelina omega-3 and canola high-protein meal, yet regulatory clarity will dictate commercialization pace.

Multinationals invest heavily in data-driven breeding and precision phenotyping to shorten product cycles and outpace resistance development. Corteva’s USD 100 million facility upgrade in Iowa accelerates gene-edited trait screening, while Bayer integrates processing to capture downstream margins. Competitive intensity will continue to scale as renewable diesel, carbon markets, and regulatory shifts co-evolve and reshape seed profitability.

Leaders of North America Oilseed Market For Sowing

-

BASF SE

-

Bayer AG

-

Land O’Lakes Inc.

-

Syngenta Group

-

Corteva Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2025: KWS SAAT SE and Groupe Limagrain completed the divestiture of AgReliant Genetics to GDM for USD 2.1 billion. The transaction enables KWS and Limagrain to focus resources on their core European and international markets while providing GDM with enhanced North American market presence and access to established corn and soybean breeding programs.

- March 2025: Beck's Superior Hybrids acquired select assets from Gro Alliance, expanding its seed production and distribution capabilities across key Midwest markets. The acquisition includes processing facilities, germplasm assets, and dealer networks that strengthen Beck's position in premium oilseed markets.

- October 2024: Bayer AG acquired a canola processing facility in Lethbridge, Alberta for CAD 127 million (USD 94 million), expanding its integrated canola value chain capabilities. The facility enhances Bayer's ability to capture value from its InVigor canola genetics while supporting growing renewable diesel feedstock demand.

Scope of Report on North America Oilseed Market For Sowing

Hybrids, Open Pollinated Varieties & Hybrid Derivatives are covered as segments by Breeding Technology. Canola, Rapeseed & Mustard, Soybean, Sunflower are covered as segments by Crop. Canada, Mexico, United States are covered as segments by Country.

Breeding Technology

| Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide Tolerant Hybrids | |

| Insect Resistant Hybrids | ||

| Other Traits | ||

| Open Pollinated Varieties & Hybrid Derivatives | ||

Crop

| Canola, Rapeseed & Mustard |

| Soybean |

| Sunflower |

| Other Oilseeds |

Geography

| Canada |

| Mexico |

| United States |

| Rest of North America |

| Breeding Technology | Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide Tolerant Hybrids | ||

| Insect Resistant Hybrids | |||

| Other Traits | |||

| Open Pollinated Varieties & Hybrid Derivatives | |||

| Crop | Canola, Rapeseed & Mustard | ||

| Soybean | |||

| Sunflower | |||

| Other Oilseeds | |||

| Geography | Canada | ||

| Mexico | |||

| United States | |||

| Rest of North America | |||

Need A Different Region or Segment?

Customize Now

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms

Get More Details On Research Methodology

Download PDF