North America Non-dairy Cheese Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

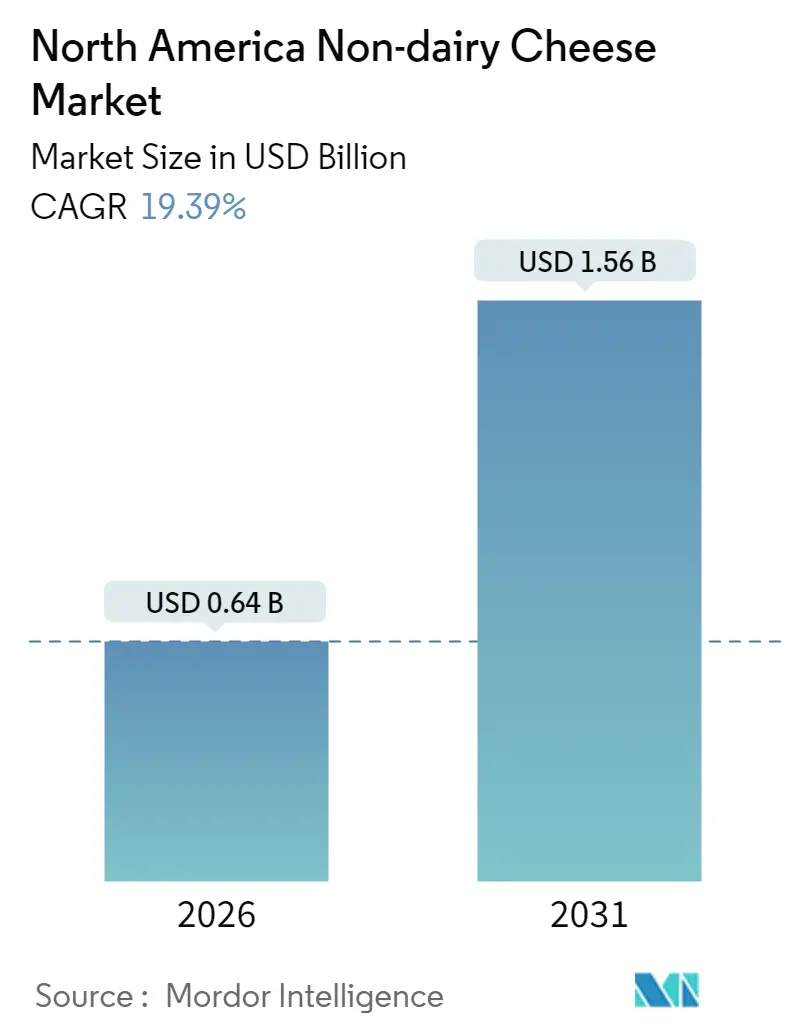

| Market Size (2026) | USD 0.64 Billion |

| Market Size (2031) | USD 1.56 Billion |

| Growth Rate (2026 - 2031) | 19.39% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Non-dairy Cheese Market Analysis by Mordor Intelligence

The North America non-dairy cheese market is expected to grow from USD 0.54 billion in 2025 to USD 0.64 billion in 2026 and is forecast to reach USD 1.56 billion by 2031 at 19.39% CAGR over 2026-2031. This growth represents a strong CAGR of 19.71% during the forecast period. The market's expansion is primarily attributed to several key factors. The increasing prevalence of lactose intolerance in diverse urban populations has heightened the demand for dairy alternatives. Additionally, the rising popularity of flexitarian diets, particularly among millennials and Generation Z consumers, has further fueled the adoption of non-dairy cheese products. Rapid advancements in product formulations, particularly those enhancing meltability, have also played a crucial role in driving demand. Technological innovations, such as precision-fermentation casein, are narrowing the performance gap between non-dairy and traditional dairy cheese. These advancements enable pizza and sandwich chains to experiment with plant-based options without compromising on texture or quality. Retailers are also adapting to this growing demand. Supermarkets are allocating more refrigerated shelf space to plant-based offerings, while online retailers are leveraging targeted promotions to attract and convert curious shoppers. The competitive landscape is evolving as well. Pure-play startups are focusing on artisan niches, offering unique and high-quality products to cater to specific consumer preferences. Meanwhile, established dairy processors are utilizing their extensive distribution networks to expand their reach and capture a larger market share. This dynamic has created an environment of intense competition, with players vying to establish dominance in the rapidly growing non-dairy cheese market.

Key Report Takeaways

- By product type, cashew-based cheese led with 36.24% of the North America non-dairy cheese market share in 2025; almond-based variants are projected to expand at a 20.02% CAGR through 2031.

- By form, shredded cheese commanded 32.84% of 2025 revenue, whereas sliced cheese is forecast to post the fastest 20.51% CAGR to 2031.

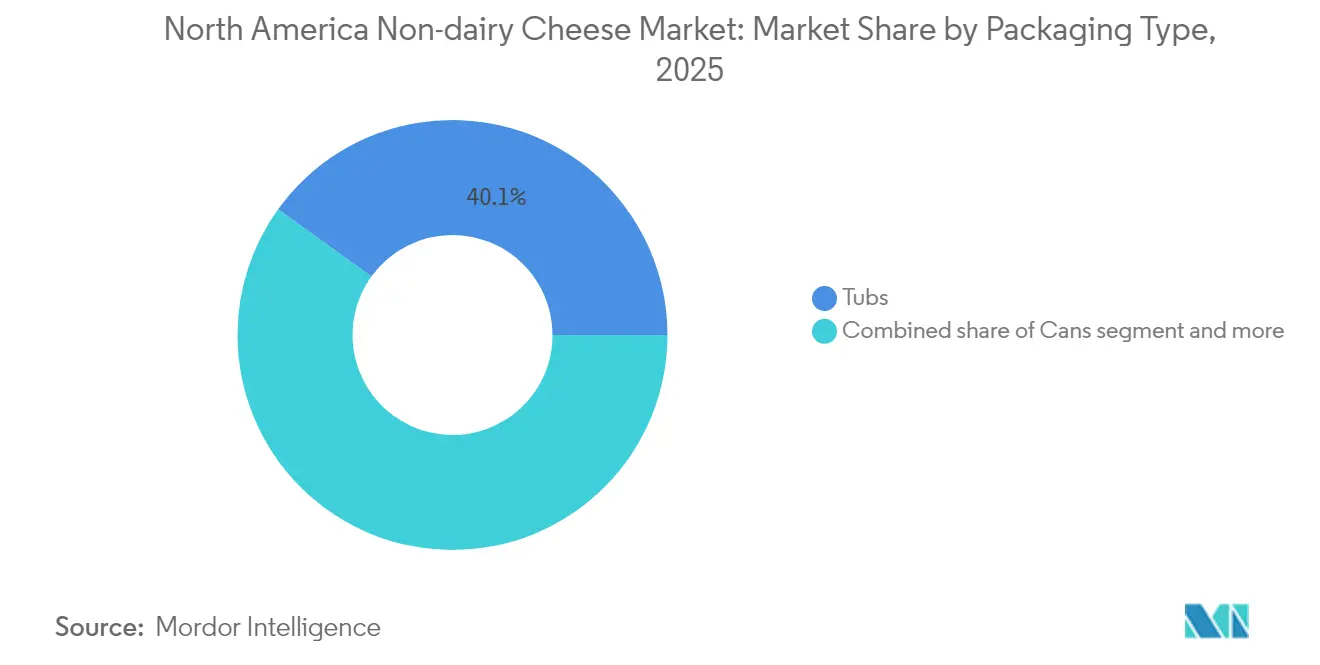

- By packaging, tubs captured 40.06% of 2025 sales, yet cans are set to rise at a 20.62% CAGR on the back of shelf-stable innovations.

- By distribution, off-trade channels secured 94.21% of value in 2025; on-trade is expected to climb at a 19.92% CAGR through 2031.

- By geography, the United States accounted for 79.02% of 2025 revenue, while Canada is poised for a 20.23% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Non-dairy Cheese Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising lactose intolerance prevalence pushes consumers toward dairy-free options | +3.2% | United States (Hispanic, African American, Asian American communities), Canada (urban centers) | Medium term (2-4 years) |

| Expanding vegan and flexitarian populations, especially millennials and Gen Z | +3.8% | United States (coastal metros), Canada (Toronto, Vancouver), Mexico (Mexico City, Monterrey) | Short term (≤ 2 years) |

| Health consciousness favors non-dairy cheese for its perceived benefits | +2.9% | United States, Canada (health-focused demographics) | Medium term (2-4 years) |

| Foodservice demand from pizza/QSR chains upgrading meltability | +2.4% | United States (national QSR chains), Canada (regional pizza operators) | Long term (≥ 4 years) |

| Product innovations improve meltability, texture, and flavor | +3.5% | North America | Medium term (2-4 years) |

| Sustainability concerns over dairy farming's environmental impact | +2.6% | United States (California, Pacific Northwest), Canada (British Columbia) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising lactose intolerance prevalence pushes consumers toward dairy-free options

In 2024, Medline Plus stated that approximately 30 million American adults experience some degree of lactose intolerance by the age of 20 [1]Source: Medline Plus, "Lactose intolerance", medlineplus.gov. This condition is particularly common among African American, Hispanic, Asian American, and Native American communities. Consequently, grocers in diverse metropolitan areas are allocating more shelf space to non-dairy alternatives. The FDA's 2024 guidance has further supported this shift. By permitting "plant-based cheese" labeling, provided products are clearly differentiated from dairy, the FDA has reduced regulatory barriers. This change allows brands to emphasize product functionality without risking enforcement actions. Enzyme-deficiency testing is also becoming a standard practice in pediatric care, fostering early awareness that leads to a lifelong preference for lactose-free products. Retailers have noted that non-dairy cheese sales in regions with higher Hispanic and Asian populations exceed those in predominantly white neighborhoods by 40 to 60 percentage points. This trend indicates that targeted distribution strategies can enhance market penetration. As demographic changes continue and lactose intolerance screenings become more common in healthcare, this growth is expected to sustain in the medium term.

Expanding vegan and flexitarian populations, especially millennials and gen Z

Health-conscious consumers are increasingly adopting plant-based diets, fueling the market's growth. The Good Food Institute reported that in 2024, 59% of U.S. households purchased plant-based foods [2]Source: Good Food Institute, "U.S retail market insight for plant-based industry", gfi.org. These consumers are notably reducing their consumption of animal products without fully eliminating them. Millennials and Generation Z, who collectively hold over half of the grocery purchasing power in urban areas, demonstrate significantly higher trial rates for plant-based cheese compared to older generations. The popularity of plant-based eating has been amplified by social media, with celebrity endorsements and influencer marketing playing key roles in shifting these products from niche to mainstream. In 2025, PETA recognized Chicago as the most vegan-friendly city in the U.S., citing its extensive range of plant-based options [3]Source: PETA, " PETA's Top 10 Vegan Friendly Cities of 2025", peta.org. Quick-service restaurants like Chipotle and Panera Bread, which target younger demographics, have introduced non-dairy cheese options to address unmet demand. Brands are rapidly adapting by utilizing digital marketing strategies to capture the attention of this demographic and convert initial interest into repeat purchases.

Health consciousness favors non-dairy cheese for its perceived benefits

Consumers increasingly perceive plant-based cheese as having lower saturated fat, being cholesterol-free, and containing fewer calories compared to dairy cheese, even when nutritional labels indicate similar fat content in cashew- and coconut-based formulations. This perception, documented in peer-reviewed nutrition journals, encourages health-conscious shoppers aiming to reduce cardiovascular risks to try these alternatives. The American Heart Association's dietary guidelines, which recommend limiting saturated fat intake, indirectly support plant-based options, as many consumers associate "plant-based" with "heart-healthy." Retailers are leveraging this perception by positioning non-dairy cheese near organic produce and functional foods, reinforcing the health-focused narrative. However, concerns about protein content persist, as most plant-based cheeses provide 1 to 3 grams per serving compared to 6 to 8 grams in dairy cheese. To address this, brands are fortifying their products with pea protein isolates and nutritional yeast. Medium-term growth depends on narrowing this nutritional gap while maintaining the clean-label appeal that resonates with ingredient-conscious consumers.

Foodservice demand from pizza and QSR chains upgrading meltability

Pizza chains and quick-service restaurants have traditionally avoided non-dairy cheese due to its poor melting, stretching, and browning properties, which negatively impacted visual appeal and consumer satisfaction. However, companies like New Culture and Perfect Day are addressing these issues through precision fermentation technologies that produce animal-free casein proteins. These proteins replicate the molecular structure responsible for dairy cheese's thermal behavior, eliminating functional shortcomings. Domino's and Papa John's have conducted limited-market trials of vegan cheese pizzas, with customer feedback showing that improved meltability has reduced the sensory gap to a level acceptable for mainstream consumers. Although non-dairy cheese costs 2 to 3 times more than mozzarella, foodservice operators are willing to absorb the higher costs to meet flexitarian demand and differentiate their menu offerings. The long-term success of this trend depends on scaling fermentation capacity to lower ingredient costs and achieving GRAS (Generally Recognized as Safe) status from the FDA for novel casein proteins, a regulatory milestone that multiple startups aim to reach before 2027.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing versus dairy cheese persists | -1.8% | United States (price-sensitive rural markets), Mexico (mass-market segments) | Short term (≤ 2 years) |

| Taste-texture skepticism among omnivores | -1.5% | United States (Midwest, South), Canada (rural provinces) | Medium term (2-4 years) |

| Lack of awareness among older demographics | -0.9% | United States (Baby Boomer cohorts), Canada (older suburban populations) | Long term (≥ 4 years) |

| Nut supply price volatility and climate risks | -1.2% | United States (California almond belt), Global (cashew sourcing from Vietnam, India) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Taste-texture skepticism among omnivores

Research on consumer perception indicates that taste is the primary obstacle to the adoption of non-dairy cheese. Omnivores frequently describe the texture as "plasticky," the aftertaste as "sour," and note a "lack of creaminess," which leads them to dismiss plant-based alternatives after initial trials. Blind taste tests conducted by food science researchers show that even formulations preferred by vegans receive lukewarm responses from omnivores accustomed to the complex flavors and mouthfeel of dairy cheese. This skepticism is particularly prevalent in the Midwest and Southern U.S., where dairy consumption is deeply rooted in culture, and plant-based diets are often viewed as a coastal trend. Quick-service restaurants testing non-dairy cheese report that customer satisfaction scores trail dairy options by 15 to 20 percentage points, discouraging broader menu inclusion. Medium-term improvements rely on narrowing the sensory gap through precision fermentation casein and advanced flavor-masking technologies. However, consumer education campaigns are equally essential to reset expectations and highlight that plant-based cheese offers unique attributes rather than replicating dairy exactly.

Lack of awareness among older demographics

Demographic purchasing data indicates that Baby Boomers and the Silent Generation have limited awareness of non-dairy cheese and are reluctant to try unfamiliar products. These older adults, accustomed to consuming dairy throughout their lives without significant health concerns, favor familiar options and often see plant-based alternatives as unnecessary. Retailers catering to this demographic allocate minimal shelf space to non-dairy cheese, which reduces visibility and widens the awareness gap. Marketing strategies that focus on lactose intolerance management and cholesterol reduction are more effective with older audiences compared to environmental or ethical messaging. This suggests that targeted communication can gradually increase product penetration. However, the long-term impact is limited by cohort replacement dynamics. As younger consumers grow older and gain higher spending power, they naturally drive category growth, reducing the need for significant awareness-building initiatives.

Segment Analysis

By Product Type: Cashew Dominance Faces Almond Disruption

In 2025, cashew-based cheese accounted for a 36.24% market share, attributed to its neutral flavor, creamy texture, and versatility in shredded, sliced, and block forms. These qualities appeal to both committed vegans and flexitarians exploring plant-based options. Almond-based cheeses are expected to grow at a 20.02% CAGR through 2031, driven by California processors diversifying crops due to water scarcity and a saturated almond butter market, while seeking higher-margin opportunities. Soy-based cheese has lost market share to nut-based alternatives, as consumers associate soy with genetic modification and hormonal disruption, despite scientific evidence affirming its safety. Other bases, such as oat, coconut, and pea protein, collectively hold the remaining market share and are attracting investments as brands develop allergen-free formulations that avoid tree nuts and soy. Precision fermentation technologies, which produce animal-free casein, are anticipated to disrupt this segmentation. Patent filings from New Culture and Perfect Day indicate that casein-fortified formulations can incorporate any plant base while delivering dairy-like functionality.

Cashew sourcing, concentrated in Vietnam and India, presents geopolitical and climate-related risks. In contrast, almond-based brands mitigate these risks by relying on California's domestic supply, highlighting supply chain resilience as a competitive advantage. Brands like Miyoko's Creamery and Kite Hill have established strong market positions by emphasizing artisan-crafted cashew formulations and adopting premium pricing strategies, even as mass-market consumers remain price-sensitive. Soy-based cheese continues to appeal to budget-conscious vegans and institutional foodservice operators prioritizing cost over taste, but its growth is limited by flavor challenges and its inability to command premium pricing. Oat-based cheese, introduced to North America by European brands, is gaining popularity among consumers seeking nut-free options due to allergy concerns, although texture issues persist. The FDA's GRAS approval process for novel proteins, including those derived from precision fermentation, will play a critical role. If casein-fortified formulations achieve commercial scalability before 2027, the focus may shift from base ingredients to functional performance.

Note: Segment shares of all individual segments available upon report purchase

By Form: Slices Surge as Sandwiches Go Plant-Based

In 2025, shredded cheese captured a dominant 32.84% market share, bolstered by strong demand from foodservice sectors, particularly pizzerias and taco chains. Here, meltability and portion control play pivotal roles in format preference. Meanwhile, cheese slices are on track to witness a robust growth rate of 20.51% CAGR through 2031. This surge is largely attributed to quick-service restaurants, such as Subway and Panera Bread, reshaping their menus to cater to the rising flexitarian demand for previously overlooked dairy-free options. Blocks and cubes, often linked to charcuterie boards and snacking, are experiencing sluggish growth. This is primarily due to texture challenges, making plant-based cheese less favorable for standalone consumption, in contrast to its melted counterparts. Other variations, like spreads and cream cheese substitutes, cater to niche breakfast and appetizer markets. However, they grapple with fierce competition from well-established dairy brands that dominate the refrigerated deli sections.

The growth of sliced cheese underscores its operational benefits for quick-service restaurants. Pre-portioned slices not only cut down labor costs but also reduce food waste, a challenge often faced with shredded cheese that requires precise measuring and is prone to clumping during storage. While pizza chains are open to experimenting with plant-based toppings, the premium pricing of shredded formats confines their use to limited-time offers, rather than a permanent fixture on the menu. Blocks of cheese encounter the most significant hurdles in adoption. Consumers anticipate cheese blocks to provide a rich flavor profile and a firm texture ideal for slicing. These are qualities that plant-based versions find challenging to emulate without costly and time-consuming aging processes. On the other hand, cream cheese alternatives, spearheaded by brands like Kite Hill and Miyoko's, have seamlessly integrated into the mainstream. Their simpler flavor profiles and spreadable textures effectively mask any functional shortcomings. This indicates that targeted innovation strategies in specific forms could pave the way for growth in segments that remain relatively untapped.

By Packaging Type: Tubs Lead, Cans Climb

In 2025, tubs secured a 40.06% market share, underscoring their appeal for shredded and spreadable formats. These products, often found in specialty retailers and natural food stores, cater to consumers who value resealability and portion flexibility. Meanwhile, cans are projected to experience a robust growth rate of 20.62% CAGR through 2031. This surge is attributed to their shelf-stable formulations, which sidestep cold-chain dependencies. As a result, these cans are increasingly distributed through convenience stores and gas stations, venues where refrigerated space is at a premium. Tins, on the other hand, are predominantly associated with imported European brands. However, they command only a minor market share and are being edged out by flexible pouches. These pouches not only lighten the packaging but also bolster sustainability credentials.

For brands eyeing rural markets and communities with food insecurity, canned non-dairy cheese emerges as a golden opportunity. In these areas, refrigeration access can be sporadic, and shelf-stable protein sources often fetch a premium. While tubs are the go-to for premium segments, thanks to their fresh and minimally processed image, brands are venturing into modified atmosphere packaging. This innovation doubles the refrigerated shelf life from 30 to 60 days, curbing retail waste and enhancing distribution economics. Tins are on the brink of obsolescence. As consumers become more sustainability-minded, there's a clear shift away from metal packaging. Instead, there's a growing preference for recyclable plastics and compostable materials. This shift compels European exporters to rethink and reformulate their packaging strategies for the North American audience. Navigating the FDA's stringent food contact substance regulations poses another challenge. These regulations oversee the migration of packaging materials into cheese products. Brands must ensure that any novel packaging doesn't leach compounds that could alter taste or introduce health risks. This compliance requirement, while crucial, can decelerate innovation cycles.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Off-Trade Dominates, On-Trade Accelerates

In 2025, off-trade channels accounted for 94.21% of the market share, highlighting consumers' preference for purchasing non-dairy cheese for home consumption through supermarkets, hypermarkets, and online platforms rather than dining out. On-trade distribution is projected to grow at a strong 19.92% CAGR through 2031, driven by casual dining chains and independent restaurants addressing customer demand for dairy-free options, which were previously unmet due to limited supplier availability and high prices. Within the off-trade segment, supermarkets and hypermarkets dominate sales by strategically utilizing refrigerated dairy case shelf space to encourage impulse purchases and attract conventional cheese buyers. Online retail is expanding rapidly, with direct-to-consumer subscriptions and third-party platforms like Amazon Fresh enabling brands to bypass traditional retail barriers and leverage consumer data for product development.

Convenience stores and specialist retailers, such as Whole Foods and Sprouts Farmers Market, play distinct roles in the distribution network. Convenience stores focus on shelf-stable formats, while specialist retailers emphasize artisan brands that command premium prices. Warehouse clubs, led by Costco, are testing bulk formats of non-dairy cheese to reduce per-unit costs, appealing to large households and small foodservice operators seeking cost-effective plant-based options. The on-trade segment is gaining traction as pizza chains like Domino's and Papa John's test vegan cheese as limited-time offers, evaluating consumer acceptance before committing to national rollouts. Although restaurant operators face margin pressures due to non-dairy cheese being 2 to 3 times more expensive than mozzarella, they are willing to absorb these costs to cater to flexitarian demand and differentiate their menus. According to a 2024 survey by the National Restaurant Association, 60% of operators plan to expand their plant-based menu offerings within the next two years, indicating sustained growth in the on-trade sector.

Geography Analysis

In 2025, the United States led the regional revenue landscape, capturing a significant 79.02% share. This leadership is driven by several factors: dense vegan populations in coastal metropolitan areas, aggressive shelf-space expansions by retailers like Whole Foods and Kroger, and foodservice trials by national pizza chains aiming to attract flexitarian consumers. California plays a pivotal role, contributing a substantial portion of US non-dairy cheese sales. This growth is supported by the state's large Hispanic and Asian American populations, who often experience higher rates of lactose intolerance. Additionally, California's focus on environmental sustainability encourages low-carbon food choices, further supported by state climate action plans promoting plant-based agriculture. In 2024, the FDA clarified regulations by allowing "plant-based cheese" labels, provided products are clearly distinguished from dairy. This regulatory update reduced compliance challenges and enabled brands to highlight product functionality without risking enforcement actions. Following California, New York and Texas rank as the second and third largest state markets. New York benefits from its dense urban population, while Texas sees rising interest among younger Hispanic consumers who are blending traditional dairy consumption with plant-based alternatives. However, rural areas in the Midwest and Southern states, where dairy farming traditions are deeply rooted, remain challenging markets. Plant-based eating is often perceived as a coastal trend in these regions, creating a cultural divide that national marketing campaigns struggle to address.

Canada is poised for significant growth, with a projected CAGR of 20.23% through 2031. This expansion is driven by federal support under the Plant-Based Food and Ingredients Sector Strategy, export promotion efforts, and consumer education campaigns aimed at normalizing plant-based diets. Demand in Canada is concentrated in cities like Toronto and Vancouver, where vegan populations are prominent, and retailers prioritize plant-based assortments, mirroring trends seen in California. Health Canada's strict labeling requirements, which mandate clear non-dairy descriptors, help reduce consumer confusion. These regulations allow brands to emphasize product functionality without implying dairy equivalence, which could lead to regulatory issues. Quebec presents a unique sub-market due to its French-language labeling requirements and cultural preference for artisan cheese. However, Montreal's diverse demographics are driving early adoption of plant-based products, particularly among younger consumers. In contrast, the Prairie provinces, including Alberta and Saskatchewan, face slower adoption rates. Strong dairy farming traditions and lower population densities, which hinder retail distribution, contribute to this lag.

Mexico's plant-based market is still emerging, but urban centers are showing early signs of growth. Imported brands are testing distribution partnerships with premium grocery chains like Chedraui and Soriana. Mexico City and Monterrey dominate sales, driven by affluent consumers seeking plant-based options for health and environmental benefits. Interestingly, despite high lactose intolerance rates among indigenous populations, this issue is less culturally acknowledged. Local production remains limited, with no major Mexican brands investing in non-dairy cheese manufacturing. However, ingredient suppliers are exploring partnerships with US brands to establish maquiladora facilities, which could lower import duties and logistics costs. Meanwhile, the broader North American region, including the Caribbean and Central America, shows sporadic interest in plant-based products. However, this interest is constrained by challenges such as limited cold-chain logistics, price sensitivity among consumers accustomed to low-cost dairy cheese, and underdeveloped retail infrastructure for specialty plant-based assortments.

Competitive Landscape

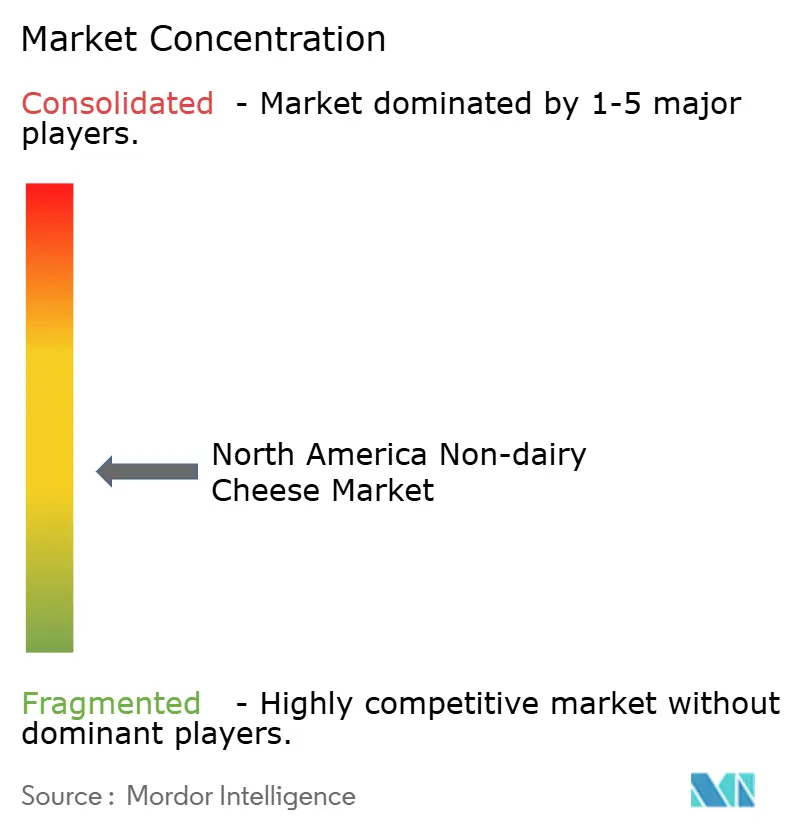

The North America non-dairy cheese market remains fragmented, with no single player commanding double-digit share, reflecting the category's nascent stage and the proliferation of startups targeting distinct consumer segments through differentiated formulations and positioning strategies. Established dairy companies like Danone SA and Saputo Inc. have entered the market through acquisitions or in-house product development. They have effectively leveraged their robust distribution networks and retailer relationships to secure shelf space, which remains a challenge for newer, pure-play startups. Upfield Group, the owner of Violife, has positioned itself as a market leader by focusing on foodservice partnerships and introducing innovative products such as Epic Mature Cheddar. This product replicates the flavor profile of aged dairy cheese, enabling premium pricing and fostering brand loyalty, particularly among omnivores hesitant about plant-based alternatives.

The non-dairy cheese market in North America is marked by ongoing product innovation and strategic expansion by leading players. Companies are introducing new flavors, textures, and formats while enhancing nutritional profiles to cater to evolving consumer preferences. They are demonstrating operational agility by investing in research and development and manufacturing capabilities to support rapid product development and market responsiveness. Strategic initiatives largely involve partnerships with retail chains and foodservice operators to strengthen distribution networks. Market leaders are pursuing growth through both organic means and acquisitions, particularly targeting companies with established plant-based cheese portfolios or specialized manufacturing expertise. The focus on sustainable and clean-label products has become a significant differentiator, with companies investing in eco-friendly packaging and transparent sourcing practices. Major players in the market include Danone SA, Good Planet Foods Private Ltd., Maple Leaf Foods, Miyoko's Creamery, and Saputo Inc.

Significant opportunities exist in underserved segments, such as allergen-free formulations that exclude tree nuts and soy, precision fermentation products fortified with casein for dairy-like meltability, and shelf-stable formats designed for convenience stores and rural areas with limited refrigeration. Emerging disruptors like New Culture and Perfect Day are utilizing precision fermentation to create animal-free casein proteins. This technological advancement could eliminate traditional ingredient segmentation by enabling any plant base to achieve dairy-equivalent functionality. Patent filings related to microbial transglutaminase enzyme applications and protein-blending techniques are creating competitive advantages for innovators while raising entry barriers for new entrants. This highlights the importance of intellectual property strategies in shaping the market's future. Smaller players such as Parmela Creamery and Treeline Cheese are challenging established companies by focusing on ultra-premium artisan segments. Their strategy of pricing above USD 15 for an 8-ounce package, justified by superior taste and texture, helps build brand equity and fund research and developmen without relying on mass-market distribution. The FDA's GRAS approval process for novel proteins will influence competitive dynamics, as brands that secure early regulatory approval for precision fermentation ingredients can gain first-mover advantages in foodservice channels where meltability is critical.

North America Non-dairy Cheese Industry Leaders

-

Danone SA

-

Maple Leaf Food

-

Miyoko's Creamery

-

Saputo Inc.

-

Good Planet Foods Private Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: RIND has introduced ALPINE SVVISS, a new addition to its range of cashew-based vegan cheeses. Staying true to RIND's artisanal standards, ALPINE SVVISS is gluten-free, cholesterol-free, and certified Kosher Pareve.

- August 2024: Plonts, a new entrant in the plant-based cheese market, has introduced its first product in the US after raising USD 12 million in a seed funding round and has established a pilot plant in Oakland, California.

- June 2023: Oatly Introduced Dairy-Free Cream Cheese in the U.S. The latest product from Oatly, offered in Plain and Chive and Onion flavors, perfectly replicates the savory and tangy profile of traditional cream cheese, entirely free of dairy.

North America Non-dairy Cheese Market Report Scope

| Cashew-Based Cheese |

| Soy-Based Cheese |

| Almond-Based Cheese |

| Others |

| Shredded |

| Blocks |

| Cubes |

| Slices |

| Others |

| Tubs |

| Tins |

| Cans |

| On-trade | |

| Off-trade | Convenience Stores |

| Specialist Retailers | |

| Supermarkets and Hypermarkets | |

| On-line Retail | |

| Others (Warehouse clubs, gas stations, etc.) |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| Product Type | Cashew-Based Cheese | |

| Soy-Based Cheese | ||

| Almond-Based Cheese | ||

| Others | ||

| Form | Shredded | |

| Blocks | ||

| Cubes | ||

| Slices | ||

| Others | ||

| Packaging Type | Tubs | |

| Tins | ||

| Cans | ||

| Distribution Channel | On-trade | |

| Off-trade | Convenience Stores | |

| Specialist Retailers | ||

| Supermarkets and Hypermarkets | ||

| On-line Retail | ||

| Others (Warehouse clubs, gas stations, etc.) | ||

| Conutry | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Market Definition

- Dairy Alternatives - Dairy alternatives are foods that are made from plant-based milk/oils instead of their usual animal products, such as cheese, butter, milk, ice cream, yogurt, etc. Plant-based or non-dairy milk alternative is the fast-growing segment in the newer food product development category of functional and specialty beverage across the globe.

- Non-Dairy Butter - Non dairy butter is a vegan butter alternative that is made from a mixture of plant oils. With an increase in alternative diets like vegetarianism, veganism, and gluten intolerance, plant butter is a healthy non-dairy substitute for normal butter.

- Non-Dairy Ice Cream - Plant based ice cream is a growing category. Non-dairy ice cream is a type of dessert made without any animal ingredients. This is typically considered a substitute for regular ice cream for those who cannot or do not eat animal or animal-derived products, including eggs, milk, cream, or honey.

- Plant-Based Milk - Plant based milks are milk substitutes that are made from nuts (e.g., hazelnuts, hemp seeds), seeds (e.g., sesame, walnuts, coconuts, cashews, almonds, rice, oats, etc.) or legumes (e.g., soy). Plant-based milk such as soy milk and almond milk have been popular in East Asia and the Middle East for centuries.

| Keyword | Definition |

|---|---|

| Cultured Butter | Cultured butter is prepared by having the raw butter go through chemical processing and has been added with certain emulsifiers and foreign ingredients. |

| Uncultured Butter | This type of butter is one which has not been processed in any way |

| Natural Cheese | The type of cheese in its most natural form. It is made from natural and simple products and ingredients, including fresh and natural salts, natural colors, enzymes, and high-quality milk. |

| Processed Cheese | Processed cheese undergoes the same processes as natural cheese; however, it requires more steps and many different forms of ingredients. Making processed cheese involves melting natural cheese, emulsifying it, and adding preservatives and other artificial ingredients or colorings. |

| Single Cream | Single cream contains around 18% fat. It’s a single layer of cream that appears over boiled milk. |

| Double Cream | Double cream contains 48% fat, more than double the amount of fat of single cream. It’s heavier and thicker than single cream |

| Whipping Cream | This has a much higher fat percentage than single cream (36%). Used to top cakes, pies, and puddings and as a thickener for sauces, soups, and fillings. |

| Frozen Desserts | Desserts that are meant to be eaten in frozen condition. E.g., sherbets, sorbets, frozen yogurts |

| UHT Milk (Ultra-high temperature milk) | Milk heated at a very high temperature. Ultra-high-temperature processing (UHT) of milk involves heating for 1–8 sec at 135–154°C. which kills the spore-forming pathogenic microorganism, resulting in a product with a shelf-life of several months. |

| Non-dairy butter/Plant-based butter | Butter made from plant-derived oil such as coconut, palm, etc. |

| Non-dairy Yogurt | Yogurt made from typically made from nuts, like almonds, cashews, coconuts, and even other foods like soybeans, plantains, oats, and peas |

| On-trade | It refers to restaurants, QSRs, and bars. |

| Off-trade | It refers to supermarkets, hypermarkets, on-line channels, etc. |

| Neufchatel cheese | One of the oldest kinds of cheese in France. It is a soft, slightly crumbly, mold-ripened, bloomy-rind cheese made in the Neufchâtel-en-Bray region of Normandy. |

| Flexitarian | It refers to a consumer preferring a semi-vegetarian diet, that is centered on plant foods with limited or occasional inclusion of meat. |

| Lactose Intolerance | Lactose intolerance is a reaction in digestive system to lactose, the sugar in milk. It causes uncomfortable symptoms in response to the consumption of dairy products. |

| Cream Cheese | Cream cheese is a soft and creamy fresh cheese with a tangy taste made from milk and cream. |

| Sorbets | Sorbet is a frozen dessert made using ice combined with fruit juice, fruit purée, or other ingredients, such as wine, liqueur, or honey. |

| Sherbet | Sherbet is a sweetened frozen dessert made with fruit and some sort of dairy product such as milk or cream. |

| Shelf stable | Foods that can be safely stored at room temperature, or "on the shelf," for at least one year and do not have to be cooked or refrigerated to eat safely. |

| DSD | Direct Store Delivery is the process in supply chain management wherein the product is delivered from manufacturing plant directly to the retailer. |

| OU Kosher | Orthodox Union Kosher is a kosher certification agency based in New York City. |

| Gelato | Gelato is a frozen creamy dessert made with milk, heavy cream and sugar. |

| Grass-fed Cows | Grass-fed cows are allowed to graze in pastures, where they eat a variety of grasses and clover. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms