Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

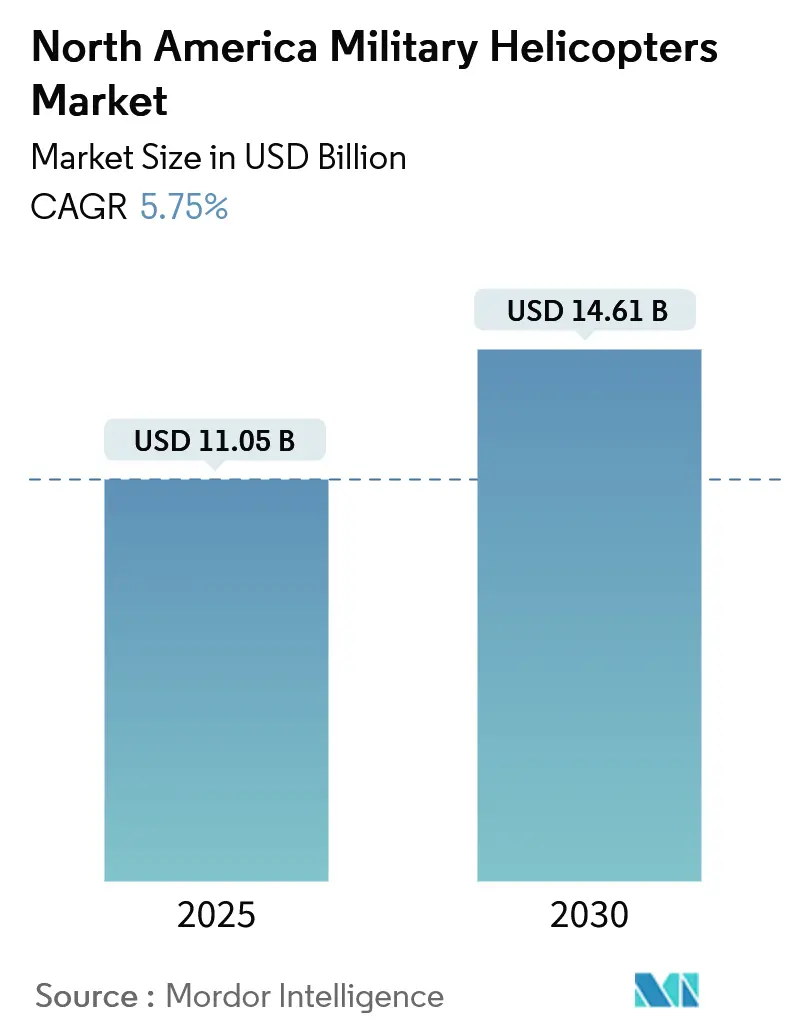

| Market Size (2025) | USD 11.05 Billion |

| Market Size (2030) | USD 14.61 Billion |

| Growth Rate (2025 - 2030) | 5.75% CAGR |

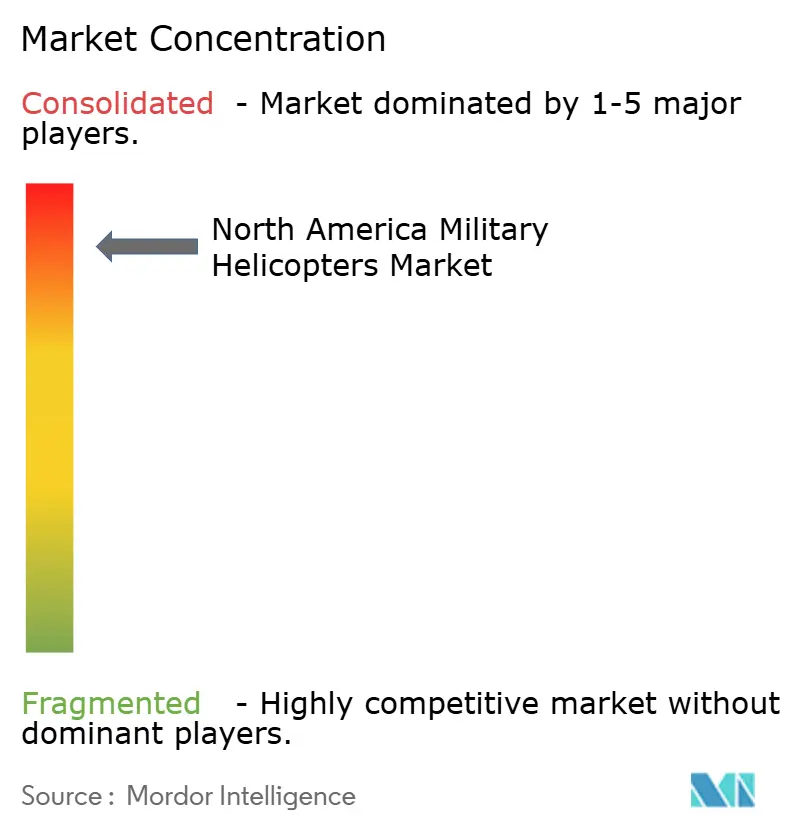

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Military Helicopters Market Analysis by Mordor Intelligence

The North America military helicopters market reached USD 11.05 billion in 2025 and is projected to climb to USD 14.61 billion by 2030, advancing at a 5.75% CAGR. The primary growth engines are the sustained rotorcraft modernization programs, Future Vertical Lift (FVL) prototyping, and growing demand for multi-mission modular platforms. Procurement priorities now favor airframes that can shift seamlessly between combat, transport, and reconnaissance roles without requiring dedicated variants. In parallel, the rapid maturation of manned-unmanned teaming architectures is reshaping mission concepts and creating new pathways for avionics and software upgrades. Expanded defense budgets across the US, Canada, and Mexico ensure steady near-term funding. At the sa for each purposeme time, Arctic performance requirements and digital-twin-enabled sustainment models open longer-term opportunities for specialized subsystems.

Key Report Takeaways

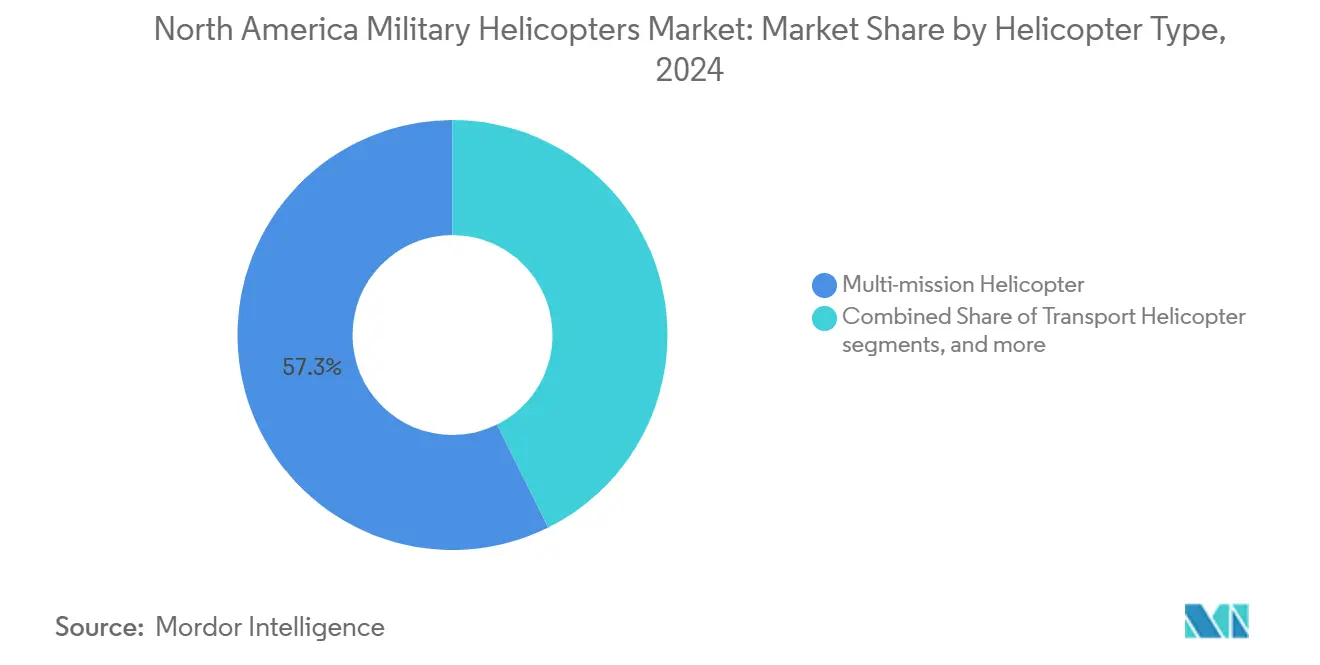

By helicopter type, multi-mission models led the North American military helicopter market, accounting for 57.34% of the market share in 2024.

By end-user service, Army Aviation accounted for a 44.11% revenue share in 2024; Joint/Special Operations is forecast to post the fastest growth of 6.45% CAGR through 2030.

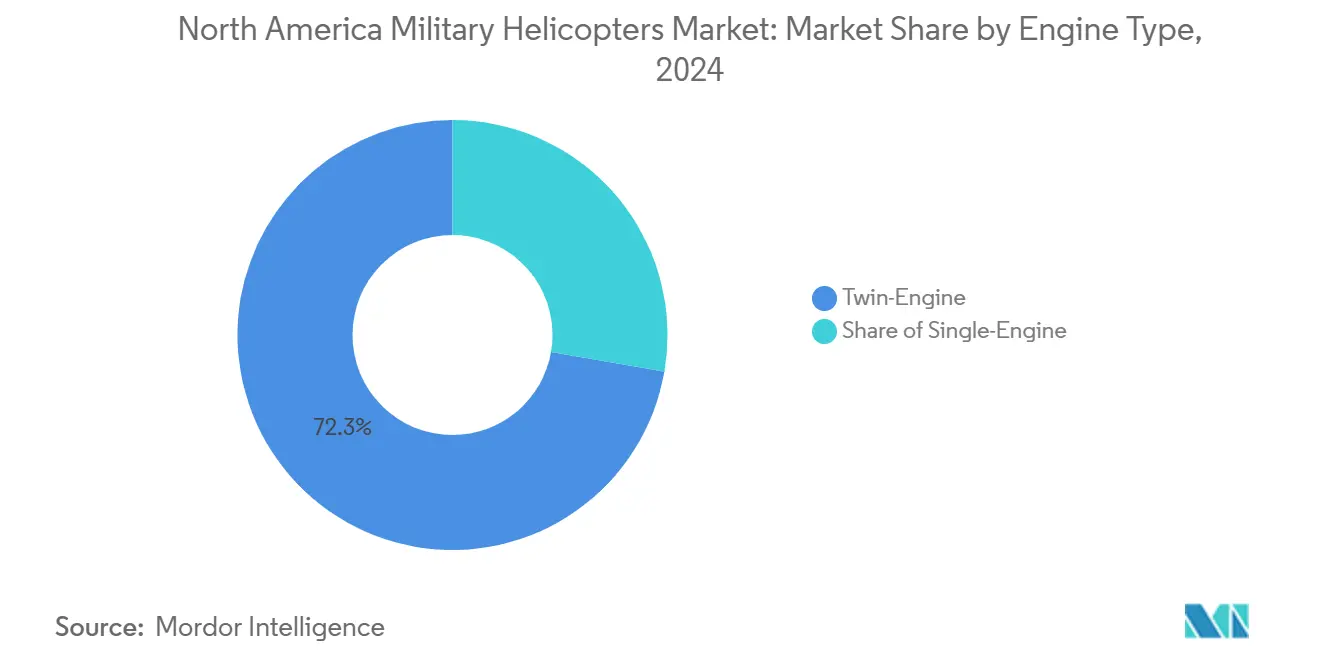

By engine type, twin-engine platforms accounted for 72.29% of the North American military helicopters market size in 2024 and are expected to expand at a 6.12% CAGR over the forecast period.

By application, combat and close air support dominated with a 40.61% value share in 2024, whereas humanitarian and disaster relief is expected to register a 6.87% CAGR from 2024 to 2030.

By country, the United States contributed 84.55% of the 2024 spending; Mexico is poised to record the highest 7.55% CAGR from 2024 to 2030.

North America Military Helicopters Market Trends and Insights

Driver Impact Analysis

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated rotorcraft modernization programs | +1.20% | United States, Canada | Medium term (2-4 years) |

| Shift toward multi-mission modular platforms | +1.90% | North America | Long term (≥ 4 years) |

| Future Vertical Lift and similar next-gen initiatives | +1.40% | United States | Long term (≥ 4 years) |

| Rapid adoption of manned-unmanned teaming (MUM-T) | +1.50% | United States, Canada | Medium term (2-4 years) |

| Digital-twin-driven predictive maintenance demand | +0.60% | North America | Short term (≤ 2 years) |

| Arctic/heavy-weather capable configuration demand | +0.70% | United States, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Rotorcraft Modernization Programs

The US Army’s Future Long-Range Assault Aircraft (FLRAA) contract highlights how rapidly modernization schedules are compressing, with initial low-rate production funding already included in the 2025 budget cycle.[1]Assistant Secretary of the Army (Acquisition, Logistics & Technology), “FLRAA Contract Award Announcement,” army.mil The Bell V-280 tiltrotor, selected for FLRAA, promises cruise speeds nearly 50% higher than those of legacy utility helicopters, while doubling effective range. These performance specifications require parallel investments in airframe materials, drivetrains, and mission-system cooling. Canada’s CAD 18.4 billion tactical helicopter roadmap reflects that urgency; its phased approach encompasses the life extension of CH-146 Griffons, the introduction of Arctic-optimized platforms, and the integration of NATO-interoperable datalinks.[2]Department of National Defence Canada, “Future Tactical Aviation Capability Roadmap,” canada.ca Together, these programs create a predictable baseline of retrofit and new-build orders that ripple across the entire North America military helicopters market.

Shift Toward Multi-Mission Modular Platforms

Service planners increasingly require helicopters that can accept sensor, weapons, or cabin-fit modules in under ten minutes without specialized ground support equipment. The US Coast Guard’s all-MH-60T strategy demonstrates downstream efficiencies, achieving a 13% reduction in total airframes while maintaining sortie capacity and lowering long-term sustainment costs.[3]United States Coast Guard, “All MH-60T Transition Strategy,” dcms.uscg.mil Airframers are re-engineering cabins with standardized hard points, quick-disconnect power buses, and open-systems software architectures that simplify field upgrades. Training pipelines also benefit; aircrew transition courses now emphasize mission-package familiarization rather than type-specific flight characteristics, shortening conversion timelines and building operational flexibility across the North America military helicopters market.

Future Vertical Lift and Similar Next-Gen Initiatives

FVL sets the benchmark for digital fly-by-wire controls, adaptive rotor technologies, and open-architecture avionics that can host third-party algorithms at the pace of software. Canada’s participation in NATO’s long-range rotorcraft concept, which shares FVL’s goal of 2× range and a 30% lower acoustic signature, ensures that a standard technology stack will dominate continental procurement from the late 2020s onward.[4]NATO Standardization Office, “Next-Generation Rotorcraft Capability Factsheet,” nato.int Early demonstrations of autonomy frameworks show single pilots task-managing multiple unmanned escorts, establishing the operational logic underpinning most combat helicopter doctrines by 2030. The resulting electronics, cybersecurity, and propulsion upgrade cycles generate a robust aftermarket revenue stream within the North American military helicopters market.

Rapid Adoption of Manned–Unmanned Teaming (MUM-T)

Apache battalions already field Level-4 MUM-T capability, giving cockpit crews complete control over onboard sensor payloads of RQ-7 Shadow and newer FTUAS drones. This operational reality accelerates demand for low-latency datalinks, edge-compute mission processors, and secure waveform modems. Legacy airframes, such as the CH-146 Griffon, are being retrofitted with new control stations and helmet-mounted displays, validating the retrofit potential across in-service fleets. MUM-T also influences weapons carriage; lightweight, precision-guided munitions designed for unmanned platforms now qualify for use on manned pylons, broadening the munitions ecosystem that rides on top of the North American military helicopters market.

Digital-Twin-Driven Predictive Maintenance Demand

Military logisticians are transitioning from calendar-based depot visits to flight-hour-driven predictive models, which reduce unscheduled downtime by 20–30%. Digital twins blend onboard sensor data with historical parts-failure curves to forecast component fatigue, enabling condition-based part replacement rather than blanket overhauls. Early MH-60T technology pilots have already reported a four percentage-point improvement in mission-capable rates, which justifies deeper investments in cloud-native maintenance information systems. Suppliers of engine health-monitoring modules, vibration sensors, and analytics software benefit directly, reinforcing ecosystem stickiness inside the North America military helicopters market.

Arctic/Heavy-Weather Capable Configuration Demand

Polar over-water patrols and high-latitude search-and-rescue missions require rotorcraft that can start unassisted at –40 °C, fly in icing conditions, and sustain autonomous navigation in geomagnetic-disturbed zones. Canada’s Arctic and Northern Policy Framework lists aviation survivability as a core pillar, prompting ice-protection retrofits on existing maritime helicopters and new requirements for de-icing system redundancy in upcoming competitions. US Northern Command has similarly prioritized cold-soak testing for National Guard Black Hawks assigned to Alaska. These specifications draw specialized gearbox heaters, engine bleed-air systems, and composite rotor blades with heated leading edges into the procurement spotlight, broadening the supplier field within the North America military helicopters market.

Restraints Impact Analysis

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total life-cycle cost and stretched defense budgets | -1.40% | North America | Long term (≥ 4 years) |

| Stringent export-control and tech-transfer constraints | -0.90% | United States, Canada, Mexico | Medium term (2-4 years) |

| Growing lethality of A2/AD threats | -0.60% | North America | Medium term (2-4 years) |

| Skilled-pilot shortages and composite-material bottlenecks | -0.70% | North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Total Life-Cycle Cost and Stretched Defense Budgets

Military helicopter life-cycle costs are becoming a growing concern as defense budgets are stretched thin across various modernization programs. Over their operational lifespans, these costs can be three to four times higher than the initial purchase price. For example, the US Coast Guard addresses this issue by consolidating its helicopter fleet to standardized MH-60T platforms. While this move involves higher upfront costs, it aims to reduce long-term sustainment expenses, as noted by FlightGlobal. Modern helicopters require specialized maintenance, certified technicians, and proprietary spare parts, resulting in ongoing financial commitments over their 20-to 30-year service lives. The complexity of their advanced systems, such as avionics and integrated mission systems, increases maintenance costs and reduces aircraft availability. Military planners are left balancing capability needs with budget constraints. Canada's CAD 2.28 billion (USD 1.73 billion) contract for CH-146 Griffon sustainment through the 2030s highlights how in-service support costs can rival initial procurement expenses, as reported by Public Services and Procurement Canada.

Stringent Export-Control and Tech-Transfer Constraints

Export control regulations, such as the International Traffic in Arms Regulations (ITAR), create significant hurdles for military helicopter manufacturers. These rules make it more challenging to share technology and collaborate on development, which limits market opportunities and increases costs. Advanced technologies, such as manned-unmanned teaming systems and electronic warfare capabilities, are particularly affected, even though they are critical for modern military helicopters. The lengthy export licensing process can delay international sales by 12-24 months, making US suppliers less competitive in time-sensitive procurement situations. Additionally, restrictions on technology transfer prevent North American manufacturers from forming international production partnerships, leading to higher domestic production costs and fewer economies of scale. Canada's helicopter modernization programs face these challenges when integrating US-developed systems with local requirements, potentially limiting their technology options, as noted by National Defence.

Growing Lethality of A2/AD Threats

Anti-access/area-denial (A2/AD) threats make helicopter operations more dangerous. Advanced surface-to-air missile systems, electronic warfare capabilities, and cyber attacks target helicopters' vulnerabilities in contested areas. Modern A2/AD systems can hit helicopters over 50 kilometers away using radar-guided missiles and infrared seekers that bypass traditional countermeasures. This forces changes in how helicopters are used and designed, as highlighted by Airbus. The spread of man-portable air defense systems (MANPADS) and directed-energy weapons adds to the risks, even in secure areas. As a result, helicopters must fly at higher altitudes and greater distances, which can reduce their effectiveness. Electronic warfare systems further complicate operations by disrupting GPS navigation, communication, and sensors that helicopters rely on for their navigation and communication.

Skilled-Pilot Shortages and Composite-Material Bottlenecks

The military helicopter market faces two significant challenges: a shortage of skilled pilots and supply chain issues with composite materials. The US military is short about 1,800 helicopter pilots, and training new ones takes time. Basic training alone takes 18-24 months, and mission-specific certifications add even more time, making it challenging to meet the growing demand for pilots. On the production side, shortages of composite materials are causing delays. These materials, such as specialized carbon fiber, require precise manufacturing and quality control, which limits the rate at which production can scale up. The COVID-19 pandemic disrupted supply chains for aerospace-grade materials, and the effects are still felt in 2024-2025. These challenges force military organizations to carefully balance helicopter purchases with the availability of pilots and maintenance resources.

Segment Analysis

By Helicopter Type: Multi-Mission Dominance Drives Procurement

Multi-mission helicopters captured 57.34% of 2024 spending, confirming their central role in force-structure calculus across all services. This share translates to USD 6.3 billion in the base year in the North America military helicopters market. Budget managers are increasingly prioritizing platform versatility over mission-specific optimization, and cabin reconfiguration kits that enable hoist rescue one day and troop insertion the next have become standard line-item requirements. The North America military helicopters market benefits from this trend as upgradeable software baselines and modular weapons racks open recurring revenue opportunities.

Though less numerous, transport helicopters remain indispensable for outsized-cargo moves and disaster logistics, keeping a floor under heavy-lift demand. Conversely, specialized attack and reconnaissance airframes, propelled by autonomy-ready designs, are projected to register a 6.12% CAGR through 2030. The anticipated service entry of FVL-derived armed variants underscores how new-build demand is tilting toward platforms that merge high speed, reduced acoustic signature, and plug-and-play sensor masts.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Service: Army Aviation Leads Rotorcraft Requirements

Army Aviation accounted for 44.11% of 2024 shipments, or roughly USD 4.9 billion of North America's military helicopter market share. Fleet recapitalization strategies prioritize long-range assault, Armed Aerial Scout replacements, and expanded National Guard lift, funneling procurement toward the twin-engine utility class. The 6.45% CAGR forecast for Joint/Special Operations is driven by rapid deployment mandates that require low-observable coatings, aerial refueling probes, and expanded cabin fuel cells.

Air Force helicopter buying centers on combat search-and-rescue and special operations infiltration, maintaining a small but technically sophisticated requirement set. Naval/Marine Corps Aviation offsets the cost of shipboard certification through standardization on common cockpits and maintenance tooling, enabling cross-deck interoperability. Paramilitary and Coast Guard operators expand slowly yet steadily, driven by domestic disaster-relief missions emphasizing endurance and hoist performance.

By Engine Type: Twin-Engine Reliability Drives Market Preference

Twin-engine models accounted for 72.29% of the contracted value in 2024, representing USD 8.0 billion of the North American military helicopters market size. Redundancy remains the decisive criterion for over-water flight, urban casualty evacuation, and Arctic patrol. The FAA Military Rotorcraft Certification Roadmap requires twin-compressor shutdown survivability, which is pushing even traditionally single-engine mission sets toward twin-engine layouts. With a 6.12% CAGR projected through 2030, suppliers of dual-channel Full Authority Digital Engine Controls (FADEC) and advanced single-engine-inoperative flight laws are expected to experience consistent demand.

Single-engine helicopters remain relevant in pilot training pipelines and light reconnaissance, where acquisition cost advantages offset survivability trade-offs. Several services are exploring hybrid-electric supplemental power units that could blur the line between single and twin classes by providing short-duration redundancy without doubling prime-mover count.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Combat Missions Lead While Humanitarian Roles Expand

Combat and close-air-support tasks accounted for 40.61% of 2024 contract obligations, continuing to hold doctrinal importance. The North America military helicopters market relies on this baseline demand for weapons integration kits, ballistic protection, and threat-warning receivers. Looking forward, humanitarian and disaster-relief flights are set to post the highest 6.87% CAGR, reflecting the climate-driven uptick in hurricanes, wildfires, and flooding that require vertical-lift response assets.

Troop transport remains a perennial mission set, although the rising adoption of unmanned cargo pods may gradually shift intra-theater resupply away from manned cabins. Pilot-training allocations increase with the overall fleet size; rotary-wing accession programs now incorporate unmanned-system control modules, indicating how operator skill sets evolve in tandem with platform technology.

Geography Analysis

The US continues to anchor regional demand, driven by FLRAA, Future Attack Reconnaissance Aircraft (FARA), and sustained MH-60T buys for the Coast Guard. Each program pushes high-speed rotor, adaptive engine, and open-architecture avionics technologies into serial production, creating scale advantages for domestic suppliers. The industrial base benefits from government-furnished equipment strategies that de-risk avionics swaps and foster plug-and-play upgrade paths.

Canada’s CAD 18.4 billion (USD 13.21 billion) tactical helicopter roadmap places heavy weight on Arctic survivability, fuel-efficient engines, and standardized cockpits. The Griffon Limited Life Extension project flew its first upgraded airframe in mid-2024 and will roll into fleet-wide retrofit through 2032. Simultaneously, the CH-148 Cyclone program, with deliveries set to conclude in 2025, ensures maritime anti-submarine and surface surveillance capabilities well into the 2030s.

Mexico’s helicopter recapitalization emphasizes multi-mission utility models that are adaptable to counter-narcotics operations, border security, and disaster relief. Airframes procured under Light Utility Helicopter initiatives are fitted with modular rescue hoists, fast-rope kits, and high-lift rotor blades to match varied mission profiles. Training cooperation with the US Army Security Assistance Command accelerates proficiency gains, while planned maintenance depots in Puebla aim to shorten turnaround times and develop local skilled labor.

Across the region, harsh weather remains a unifying concern—from Gulf hurricanes to Arctic blizzards. Consequently, cold-start reliability, rotor-blade de-icing, and all-weather navigation suites now appear as standard line items in nearly every request for proposal, structurally supporting technology investment across the North America military helicopters market.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The market is highly concentrated, with Lockheed Martin Corporation (Sikorsky), The Boeing Company, Airbus SE, Leonardo S.p.A., and Bell Textron Inc. being are top helicopter deliverables. These prime contractors possess entrenched intellectual property, classified production processes, and cleared labor pools, which create formidable entry barriers. Lockheed Martin's ownership of Sikorsky further consolidates its systems integration acumen, as evidenced by the digital twin applied to the Coast Guard's MH-60T service life extension.

Airbus SE and Leonardo S.p.A. maintain smaller yet strategically important footprints through targeted programs—Airbus via H145 variants for US Special Operations, Leonardo through TH-73 trainer production in Philadelphia. Tier-1 engine suppliers General Electric and Pratt & Whitney (RTX Corporation) continue to battle for next-generation turboshaft awards, offering all-new cores that tout 25% fuel-burn reductions.

Competitive differentiation centers on software-centric attributes: open-system mission computers, cyber-resilient data buses, and autonomy-ready sensor stacks. Suppliers who demonstrate government-validated cybersecurity credentials and proven modular software upgrades command premium evaluation scores. Export-control strictures tilt the advantage toward domestic integrators for classified payloads. However, niche suppliers of ice protection, crash-worthy seating, and lightweight ballistic panels still find room to compete within the North American military helicopters market.

North America Military Helicopters Industry Leaders

Airbus SE

Leonardo S.p.A

The Boeing Company

Lockheed Martin Corporation (Sikorsky)

Bell Textron Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2025: In a strategic move to enhance its capabilities, the US Coast Guard has placed a USD 14.3 million order for 13 General Electric T700 engines, integral to its MH-60 medium-range recovery helicopters. These T700 engines are crucial long-lead components, facilitating the expansion of the Coast Guard's MH-60 fleet and accelerating the transition of several air stations from the MH-65E to the more advanced MH-60. With its superior range, speed, payload capacity, and advanced avionics, the MH-60 stands out as a versatile platform, adeptly serving all 11 missions of the Coast Guard. The aircraft's prowess in locating, identifying, and tracking surface targets, regardless of the time of day, underscores its significance in search and rescue operations and law enforcement activities.

- January 2024: With an investment of USD 1.7 billion (CAD 2.28 billion), the Canadian government is set to extend the operational life of its CH-146 Griffon helicopters. Bell Textron Canada Limited (BTCL) has been chosen for this endeavor, which prioritizes safety enhancements and promises job creation nationwide. In collaboration with Bell Textron Canada Limited, the Canadian government is ensuring vital in-service support for the CH-146 Griffon helicopters, integral to the Royal Canadian Air Force. This move, focused on preserving the operational readiness of 82 CH-146 Griffon helicopters stationed at 11 sites across Canada, underscores a strong commitment to bolstering the nation's air fleet.

North America Military Helicopters Market Report Scope

By Helicopter Type

| Multi-mission Helicopter |

| Transport Helicopter |

| Other Helicopter |

By End-User Service

| Air Force |

| Army Aviation |

| Naval/Marine Corps Aviation |

| Joint/Special Operations |

| Paramilitary and Coast Guard |

By Engine Type

| Single-Engine |

| Twin-Engine |

By Application

| Combat and Close Air Support |

| Troop Transport |

| Humanitarian and Disaster Relief |

| Pilot Training |

By Country

| United States |

| Canada |

| Mexico |

| By Helicopter Type | Multi-mission Helicopter |

| Transport Helicopter | |

| Other Helicopter | |

| By End-User Service | Air Force |

| Army Aviation | |

| Naval/Marine Corps Aviation | |

| Joint/Special Operations | |

| Paramilitary and Coast Guard | |

| By Engine Type | Single-Engine |

| Twin-Engine | |

| By Application | Combat and Close Air Support |

| Troop Transport | |

| Humanitarian and Disaster Relief | |

| Pilot Training | |

| By Country | United States |

| Canada | |

| Mexico |

Need A Different Region or Segment?

Customize Now

Market Definition

- Aircraft Type - All the military rotorcraft which are used for various applications are included in this study.

- Sub-Aircraft Type - For this study, all the military helicopters based on their application are considered.

- Body Type - Multi-Mission Helicopters, Transport Helicopters, Training Helicopters and various other rotorcraft are considered in this study.

| Keyword | Definition |

|---|---|

| IATA | IATA stands for the International Air Transport Association, a trade organization composed of airlines around the world that has an influence over the commercial aspects of flight. |

| ICAO | ICAO stands for International Civil Aviation Organization, a specialized agency of the United Nations that supports aviation and navigation around the globe. |

| Air Operator Certificate (AOC) | A certificate granted by a National Aviation Authority permitting the conduct of commercial flying activities. |

| Certificate Of Airworthiness (CoA) | A Certificate Of Airworthiness (CoA) is issued for an aircraft by the civil aviation authority in the state in which the aircraft is registered. |

| Gross Domestic Product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| RPK (Revenue Passenger Kilometres) | The RPK of an airline is the sum of the products obtained by multiplying the number of revenue passengers carried on each flight stage by the stage distance - it is the total number of kilometers traveled by all revenue passengers. |

| Load Factor | The load factor is a metric used in the airline industry that measures the percentage of available seating capacity that has been filled with passengers. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| International Transportation Safety Association (ITSA) | International Transportation Safety Association (ITSA) is an international network of heads of independent safety investigation authorities (SIA). |

| Available Seats Kilometre (ASK) | This metric is calculated by multiplying Available Seats (AS) in one flight, defined above, multiplied by the distance flown. |

| Gross Weight | The fully-loaded weight of an aircraft, also known as “takeoff weight,” which includes the combined weight of passengers, cargo, and fuel. |

| Airworthiness | The ability of an aircraft, or other airborne equipment or system, to operate in flight and on the ground without significant hazard to aircrew, ground crew, passengers or to other third parties. |

| Airworthiness Standards | Detailed and comprehensive design and safety criteria applicable to the category of aeronautical product (aircraft, engine or propeller). |

| Fixed Base Operator (FBO) | A business or organization that operates at an airport. An FBO provides aircraft operating services like maintenance, fueling, flight training, charter services, hangaring, and parking. |

| High Net worth Individuals (HNWIs) | High Net worth Individuals (HNWIs) are individuals with over USD 1 million in liquid financial assets. |

| Ultra High Net worth Individuals (UHNWIs) | Ultra High Net worth Individuals (UHNWIs) are individuals with over USD 30 million in liquid financial assets. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| EASA (European Aviation Safety Agency) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| Airborne Warning and Control System (AW&C) aircraft | Airborne Warning and Control System (AEW&C) aircraft is equipped with a powerful radar and on-board command and control center to direct the armed forces. |

| The North Atlantic Treaty Organization (NATO) | The North Atlantic Treaty Organization (NATO), also called the North Atlantic Alliance, is an intergovernmental military alliance between 30 member states – 28 European and two North American. |

| Joint Strike Fighter (JSF) | Joint Strike Fighter (JSF) is a development and acquisition program intended to replace a wide range of existing fighter, strike, and ground attack aircraft for the United States, the United Kingdom, Italy, Canada, Australia, the Netherlands, Denmark, Norway, and formerly Turkey. |

| Light Combat Aircraft (LCA) | A light combat aircraft (LCA) is a light, multirole jet/turboprop military aircraft, commonly derived from advanced trainer designs, designed for engaging in light combat. |

| Stockholm International Peace Research Institute (SIPRI) | Stockholm International Peace Research Institute (SIPRI) is an international institute that provides data, analysis, and recommendations for armed conflict, military expenditure, and arms trade as well as disarmament and arms control. |

| Maritime Patrol Aircraft (MPA) | A maritime patrol aircraft (MPA), also known as maritime reconnaissance aircraft is a fixed-wing aircraft designed to operate for long durations over water in maritime patrol roles, in particular, anti-submarine warfare (ASW), anti-ship warfare (AShW), and search and rescue (SAR). |

| Mach Number | The Mach number is defined as the ratio of true airspeed to the speed of sound at the altitude of a given aircraft. |

| Stealth Aircraft | Stealth is a Common term applied to low observable (LO) technology and doctrine, that makes an aircraft near invisible to radar, infrared or visual detection. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF