Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

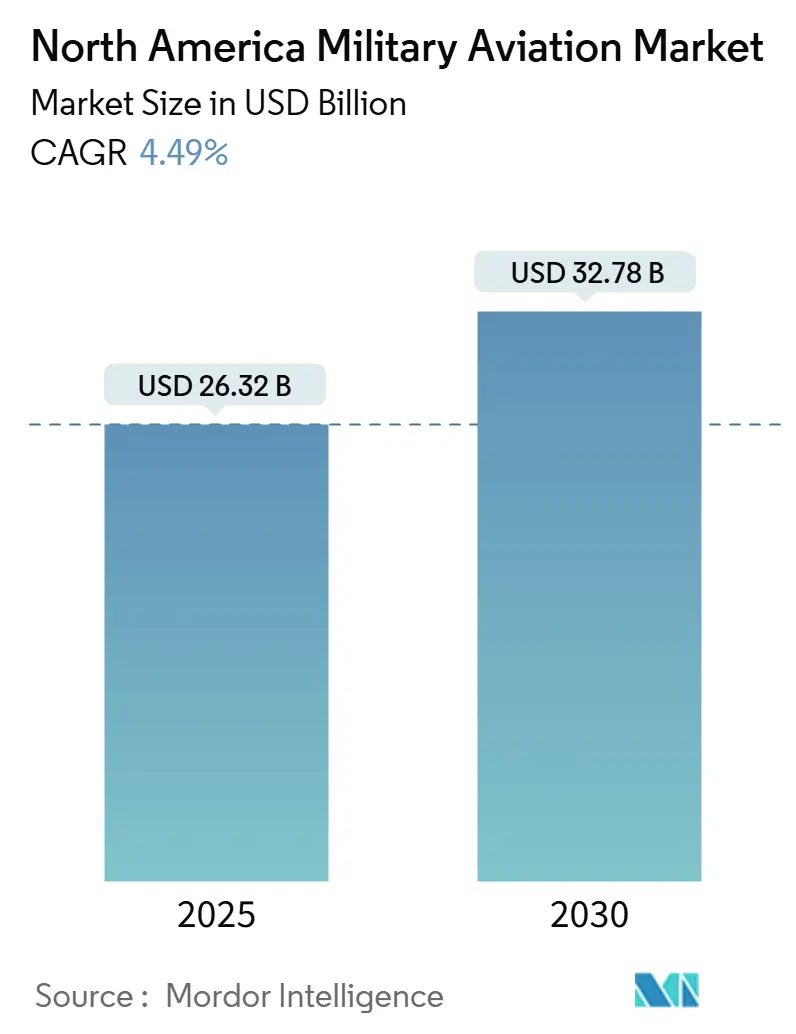

| Market Size (2025) | USD 26.32 Billion |

| Market Size (2030) | USD 32.78 Billion |

| Growth Rate (2025 - 2030) | 4.49% CAGR |

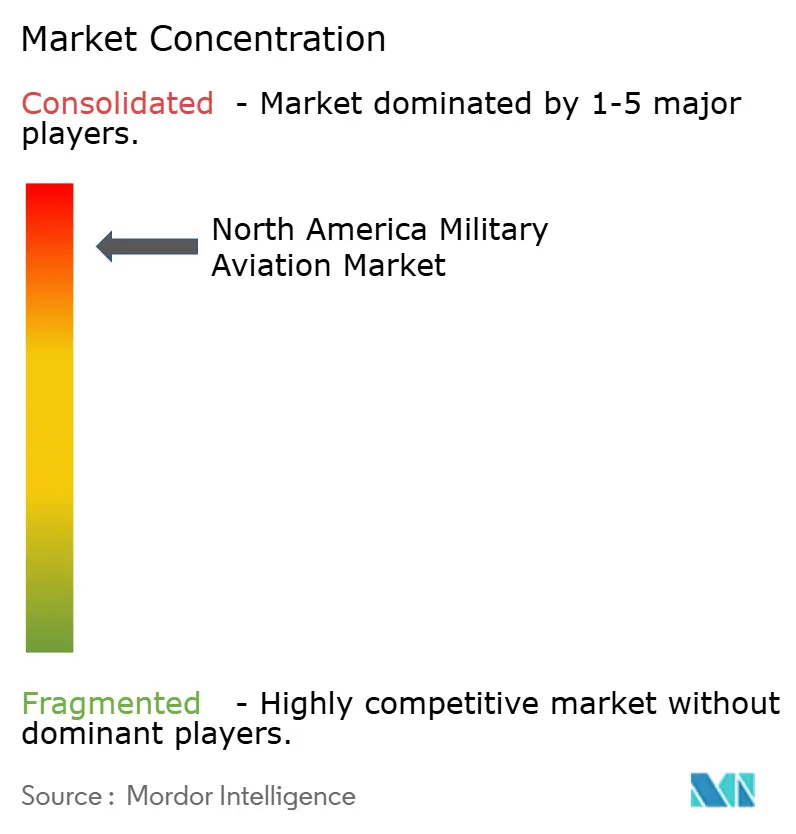

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Military Aviation Market Analysis by Mordor Intelligence

The North American military aviation market reached USD 26.32 billion in 2025 and is forecasted to climb to USD 32.78 billion by 2030, advancing at a 4.49% CAGR. Growth tracks the shift from procurement-heavy cycles toward sustainment-centric operations as the F-35 Lightning II fleet matures, next-generation bomber and tanker programs move into production, and additive manufacturing cuts maintenance turnaround times. Elevated funding for stealth technologies, modular open-systems avionics, and optionally-manned combat aircraft underpins long-term demand certainty, while recurring aftermarket contracts smooth revenue volatility relative to historical acquisition spikes. Supply-chain constraints around titanium and composites, and periodic congressional funding delays, temper the expansion trajectory. Still, they are offset by multi-year fleet support agreements, rising depot-level workloads, and cross-border industrial cooperation between the US and Canada. Competitive dynamics increasingly reward incumbents that couple digital sustainment platforms with vertical integration, a trend that amplifies margin stability even as platform sales plateau.

Key Report Takeaways

- By aircraft type, fixed-wing platforms led with 87.17% revenue share in 2024 and are projected to post the fastest 5.43% CAGR through 2030 as F-35 operations dominate fleet activity.

- By end-user service, the Air Force commanded 65.32% of 2024 spending while also recording the highest forecast growth at a 7.15% CAGR, driven by B-21 Raider and KC-46 Pegasus procurement momentum.

- By propulsion type, turbofan engines captured 69.37% of the market in 2024, while fully electric/hybrid‑electric systems are projected to grow at a 6.72% CAGR through 2030.

- By geography, the United States is expected to account for 94.64% of the regional market share in 2024. Furthermore, the United States market is projected to grow at a CAGR of 4.79%.

North America Military Aviation Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainment-heavy F-35 program drives aftermarket demand | +1.2% | United States and Canada | Long term (≥ 4 years) |

| The US National Defense Strategy boosts next-gen bomber and tanker budgets | +0.8% | United States | Medium term (2-4 years) |

| Canada’s Future Fighter Capability Project (FFCP) procurement | +0.3% | Canada | Short term (≤ 2 years) |

| Shift toward optionally-manned combat aircraft (loyal wingmen) | +0.7% | United States | Long term (≥ 4 years) |

| Additive manufacturing of legacy parts cuts AOG time | +0.4% | North America | Medium term (2-4 years) |

| Modular open-systems avionics mandate accelerates retrofit cycles | +0.5% | United States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

F-35 Sustainment Operations Transform Aftermarket Economics

Lockheed Martin’s F-35 fleet has entered a sustainment-intensive phase that materially reshapes revenue distribution across the North American military aviation market. The contractor booked USD 7.3 billion in F-35 sustainment revenue for 2024, reflecting a 43% year-over-year growth, as predictive maintenance algorithms within the Autonomic Logistics Information System (ALIS) increased spare parts consumption and depot visitation rates.[1]Lockheed Martin, “2024 Annual Report,” lockheedmartin.com Tier-2 and Tier-3 suppliers with repair certifications now secure multi-decade contracts that ensure volume visibility, favoring firms with composite airframe and low-observable coating capabilities. Fleet mission-capable-rate targets encourage the stockpiling of long-lead items, and the resulting working-capital stability supports continued investment in digital twin tooling, which further compresses turnaround times. Consequently, aftermarket gross margins outpace historical platform-sale levels, and operators receive data-driven cost-per-flight-hour pricing that aligns supplier incentives with readiness outcomes.

US National Defense Strategy Drives Next-Generation Platform Investment

The 2022 National Defense Strategy prioritizes strategic deterrence assets, allocating USD 5.1 billion to the B-21 Raider for fiscal 2024 and sustaining the KC-46 Pegasus ramp-up despite earlier technical headwinds.[2]U.S. Department of Defense, “Defense Budget Materials FY 2024,” defense.gov Composite-rich airframes and radar-absorbing structures elevate supplier qualification thresholds, consolidating awards within incumbents that maintain certified stealth-manufacturing lines. Congressional support remains resilient, insulating program baselines from short-term budget turbulence. Downstream, second-tier avionics and propulsion vendors benefit from modular open-architecture mandates that allow incremental capability insertion. The bomber-tanker recapitalization wave, therefore, anchors a predictable demand backbone for the North American military aviation market well into the 2030s, even as procurement phase-outs of legacy bombers offset a portion of the topline uplift.

Canada’s FFCP Procurement Catalyzes Regional Supply-Chain Integration

Canada’s CAD 19 billion (USD 14.2 billion) FFCP unlocks incremental volume. It deepens cross-border industrial ties via 100% Industrial and Technological Benefits offsets, compelling prime contractors to reinvest contract value domestically.[3]Government of Canada, “Future Fighter Capability Project,” canada.ca Canadian aerospace firms secure a predictable workshare in F-35 composite structures, electronic warfare modules, and pilot training services, enabling them to scale their production lines alongside their US counterparts. The harmonized fleet architecture simplifies logistics, allowing for common spares pooling and joint depot utilization, which lowers lifecycle costs for both nations. Additionally, Canadian suppliers leverage participation credentials to capture export opportunities in NATO modernization campaigns, reinforcing the project’s strategic significance beyond its headline aircraft tally.

Shift Toward Optionally-Manned Combat Aircraft

The US Air Force’s USD 6 billion Collaborative Combat Aircraft (CCA) initiative pivots tactical aviation doctrine toward loyal-wingman concepts, promising step-change force-multiplication effects by 2028.[4]U.S. Air Force, “Collaborative Combat Aircraft Program,” af.mil Early contracts awarded to Anduril and General Atomics validate software-defined airframes that accept rapid sensor and weapon plug-ins under an open-systems backbone. Unit acquisition prices projected at one-quarter of manned fifth-generation fighters enable larger sortie densities and attritable mission sets. Integration roadmaps pair CCAs with F-35 and F-22 formations, extending sensor reach and weapons standoff while reducing risk to high-value manned assets. Over time, CCA fleet sustainment will add a recurring revenue layer that diversifies the North America military aviation market beyond traditional fighter refresh cycles, reinforcing demand even as major manned programs plateau post-2030.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain titanium and composite shortages constrain ramp-ups | -0.6% | North America (global inputs) | Medium term (2-4 years) |

| Congressional CRs delay long-lead funding releases | -0.4% | United States | Short term (≤ 2 years) |

| Skilled military aviation technician shortage | -0.3% | North America | Long term (≥ 4 years) |

| Noise and emissions caps near bases restrict flight-hour allocations | -0.2% | United States and Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Material Constraints Limit Production Scaling

Boeing experienced a 15% decline in KC-46 deliveries during 2024 due to titanium forging bottlenecks, while Lockheed Martin flagged composite prepreg shortages as the primary headwind to expanding F-35 production.[5]Boeing, “2024 Quarterly Report,” boeing.com The titanium market remains tightly linked to a handful of global producers, and geopolitical frictions have curtailed spot availability, compelling primes to forward-buy at elevated prices. Composite capacity is similarly constrained given autoclave capital intensity and labor-skill requirements. Contractors counteract by dual-sourcing and increasing inventory buffers, which inflate working capital and lengthen program cash-conversion cycles.

Congressional Funding Mechanisms Create Procurement Uncertainty

The fiscal year 2024 budget cycle operated under a six-month continuing resolution that deferred USD 2.3 billion in planned aircraft contracts, forcing primes and mid-tier suppliers to self-fund critical long-lead materials. Smaller machine shops face an acute liquidity strain, accelerating consolidation that narrows the supplier base and heightens the risk of single-source dependency. Once appropriations are cleared, compressed timelines lead to surge hiring and overtime premiums, introducing inefficiencies that increase per-unit costs. Operators subsequently contend with staggered delivery profiles that complicate training pipelines and spares forecasting.

Segment Analysis

By Aircraft Type: Fixed-Wing Spending Remains the Core Growth Engine

Fixed-wing platforms commanded 87.17% of 2024 revenue, and their 5.43% CAGR keeps the North America military aviation market firmly oriented toward fighter, bomber, and tanker operations. The North American military aviation market size for fixed-wing systems is projected to reach USD 28.4 billion by 2030, as the expansion of the F-35 fleet combines with the production cycles of the B-21 and KC-46. Multi-role fighters contribute the most significant dollar value, buoyed by rising mission-capable-rate targets that expand spare-parts budgets and software upgrade contracts. Strategic transport and tanker aircraft add steady modernization demand, including cockpit digitization and connectivity retrofits that align with Joint All-Domain Command and Control (JADC2) objectives.

Rotorcraft retains12.83% share, supported by UH-60 Black Hawk and AH-64 Apache service-life extensions plus CH-47F Block II upgrades. Although their forecast growth trails fixed-wing expansion, continued emphasis on distributed operations and humanitarian response capabilities provides a stable baseline. Advanced vertical-lift research feeds incremental spending on drivetrain improvements and composite rotor-blade replacements, partially offsetting mature fleet profiles. Future unmanned resupply concepts integrate with manned rotorcraft to form hybrid formations, opening new sustainment touchpoints for avionics, data links, and sensor packages that drive additional value within the North American military aviation market.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Service: Air Force Programs Anchor Investment Momentum

The Air Force accounted for 65.32% of 2024 spending and is expected to post a 7.15% CAGR through 2030, reflecting concentrated investment in next-generation bomber, tanker, and fighter sustainment programs. The North American military aviation market share for Air Force platforms is expected to remain above 60% across the forecast horizon as B-21 production accelerates and F-35A deployments proliferate. The Space Force's realignment marginally reallocates budgets, yet core tactical-air and strategic-lift missions continue to drive upgrades in avionics, communications, and electronic warfare.

Army Aviation ranks second, driven by the UH-60 recapitalization and the Future Long-Range Assault Aircraft (FLRAA) development path, which integrates open-systems sensors and mission-planning suites. Naval and Marine Corps aviation expands through the acquisition of F-35B/C, with carrier-based operations generating higher-than-average maintenance cost intensity. Special operations elements consume disproportionate sustainment dollars given elevated flight hours and mission-unique sensor packages, highlighting recurring upgrade cycles as a durable feature within the North American military aviation market.

By Propulsion Type: Turbofan engines are integral to multi-role fighters and strategic airlift programs

Turbofan engines accounted for 69.37% of the 2024 market value and are expected to grow at a compound annual growth rate (CAGR) of 6.72%. Advancements in next-generation fighter programs and modernization efforts in heavy-lift transport drive this growth. In North America, the turbofan segment is projected to exceed USD 22 billion by 2030, supported by adaptive-cycle engine retrofits that offer a 25% increase in range and a 10% reduction in fuel consumption. Additionally, sustainment revenues are bolstered by digital-threaded health monitoring systems and hot-section life-limit resets, which enhance time-on-wing performance.

Turbojet propulsion remains significant for high-speed platforms, with growth linked to F135 engine overhaul cycles and spares provisioning for the B-21 Raider. Turboshaft engines are critical for rotary-wing fleets, where the Improved Turbine Engine Program incorporates additive-manufactured components to enhance power density for Apache and Black Hawk helicopters. Turboprop engine demand is concentrated in training and light-lift aircraft, with incremental efficiency improvements in legacy engine families such as the T56 and PT6. Meanwhile, fully electric and hybrid-electric propulsion systems, though still in the developmental phase, are attracting research and development (R&D) investments and prototype funding. These systems indicate a potential shift in propulsion spending beyond 2030, driven by sustainability goals and low-emission mandates.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The US represented nearly 85% of the 2024 value and maintains mid-single-digit growth driven by stable congressional support for the B-21 Raider, KC-46 Pegasus, and F-35 sustainment lines. Major contractor hubs in Texas, California, Georgia, and Missouri form dense supplier corridors that optimize logistics and workforce pooling. Depot-level overhaul centers in Oklahoma City and Warner Robins anchor regional employment, enabling the rapid incorporation of additive-manufactured spares. The US initiatives around modular open systems and digital engineering export technical standards that permeate the broader North American military aviation market, reinforcing the country's technology leadership position.

Canada contributed roughly 12% of regional spending in 2024, with the CAD 19 billion (USD 14.2 billion) FFCP contract driving its forecast growth ahead of the regional average. Industrial offset requirements channel workshare into composite aerostructures, mission-system software, and pilot-training solutions, seeding long-term capabilities at firms clustered around Quebec and Ontario's aerospace corridors. The North American military aviation market gains resiliency through this bilateral supply-chain diversification. Canadian sustainment hubs are slated to service joint F-35 fleet demands, enhancing readiness while broadening MRO revenue pools.

Mexico accounts for the remaining 3% of demand, concentrated on border-surveillance aircraft, disaster-response helicopters, and limited fixed-wing modernization. Budget ceilings restrict the adoption of high-end stealth assets, yet fleet-life extension programs create tactical ISR upgrade opportunities. Regional MRO agreements enable Mexican operators to utilize US and Canadian depot capacity, ensuring compliance with airworthiness directives and fostering cross-border technical cooperation that promotes overall stability in the North American military aviation market.

Competitive Landscape

The marketplace remains highly concentrated, with Lockheed Martin, Boeing, and Northrop Grumman controlling the bulk of prime contracts across fighter, bomber, and tanker lines. Certified stealth-manufacturing facilities, long-cycle intellectual property, and extensive digital sustainment ecosystems reinforce their entrenched positions. Lockheed Martin leverages the F-35’s global footprint to secure multi-year performance-based logistics agreements, while Boeing capitalizes on composite-repair hubs to strengthen KC-46 aftermarket streams. Northrop Grumman’s B-21 low-rate-initial-production award cements its stealth-bomber franchise through the 2040s, guaranteeing workload visibility.

Second-tier primes such as Raytheon Technologies and Spirit AeroSystems expand via avionics modernization kits and structural-component subcontracts that align with MOSA standards. Emerging entrants, such as Anduril Industries, pursue rapid prototyping and software-centric architectures under the CCA program, exploiting compressed development cycles to challenge legacy cost structures. Additive-manufacturing service providers, including small-business innovators, secure footholds by supplying legacy fleet spares that sidestep tooling obsolescence costs, adding competitive nuance to the North America military aviation industry.

Government policy also shapes rivalry. Defense Production Act allocations prioritize critical material and micro-electronics capacity, effectively subsidizing qualified suppliers. Cybersecurity Maturity Model Certification compliance introduces a barrier that disproportionately affects small firms without dedicated security staff, nudging them toward teaming agreements with large primes. Collectively, these dynamics reinforce high entry thresholds, supporting consolidated market power inside the North America military aviation market

North America Military Aviation Industry Leaders

-

Airbus SE

-

Lockheed Martin Corporation

-

Northrop Grumman Corporation

-

Textron Inc.

-

The Boeing Company

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2025: In a deal worth more than USD 173 million, the US Air Force awarded Boeing a contract to produce eight more MH-139A Grey Wolf helicopters and provide training and sustainment support services.

- September 2025: Lockheed Martin and the F-35 Joint Program Office (JPO) finalized an agreement for lots 18-19, covering the production and delivery of up to 296 F-35 aircraft to expand the global fleet.

- March 2025: The US Air Force awarded Boeing a contract to design, build, and deliver its next-generation fighter aircraft.

- January 2024: The Northrop Grumman B-21 Raider, the US Air Force's next-generation stealth bomber, entered the low-rate initial production (LRIP) phase. This milestone marks a significant advancement in the aircraft's development program, as it transitions from design and testing to manufacturing.

North America Military Aviation Market Report Scope

By Aircraft Type

| Fixed-Wing Aircraft | Multi-role Aircraft |

| Training Aircraft | |

| Transport Aircraft | |

| Other Aircraft | |

| Rotorcraft | Multi-Mission Helicopter |

| Transport Helicopter | |

| Other Helicopter |

By End-User Service

| Air Force |

| Army Aviation |

| Naval/Marine Corps Aviation |

| Joint/Special Operations |

| Paramilitary and Coast Guard |

By Propulsion Type

| Turbofan |

| Turbojet |

| Turboprop |

| Turboshaft |

| Fully Electric/Hybrid-Electric |

By Geography

| United States |

| Canada |

| Mexico |

| By Aircraft Type | Fixed-Wing Aircraft | Multi-role Aircraft |

| Training Aircraft | ||

| Transport Aircraft | ||

| Other Aircraft | ||

| Rotorcraft | Multi-Mission Helicopter | |

| Transport Helicopter | ||

| Other Helicopter | ||

| By End-User Service | Air Force | |

| Army Aviation | ||

| Naval/Marine Corps Aviation | ||

| Joint/Special Operations | ||

| Paramilitary and Coast Guard | ||

| By Propulsion Type | Turbofan | |

| Turbojet | ||

| Turboprop | ||

| Turboshaft | ||

| Fully Electric/Hybrid-Electric | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

Need A Different Region or Segment?

Customize Now

Market Definition

- Aircraft Type - All the military aircraft and rotorcraft which are used for various applications are included in this study.

- Sub-Aircraft Type - For this study, sub-aircraft types such as fixed-wing aircraft and rotorcraft based on their application are considered.

- Body Type - Multi-Role Aircraft, Transport, Training Aircraft, Bombers, Reconnaissance Aircraft, Multi-Mission Helicopters, Transport Helicopters and various other aircraft and rotorcraft are considered in this study.

| Keyword | Definition |

|---|---|

| IATA | IATA stands for the International Air Transport Association, a trade organization composed of airlines around the world that has an influence over the commercial aspects of flight. |

| ICAO | ICAO stands for International Civil Aviation Organization, a specialized agency of the United Nations that supports aviation and navigation around the globe. |

| Air Operator Certificate (AOC) | A certificate granted by a National Aviation Authority permitting the conduct of commercial flying activities. |

| Certificate Of Airworthiness (CoA) | A Certificate Of Airworthiness (CoA) is issued for an aircraft by the civil aviation authority in the state in which the aircraft is registered. |

| Gross Domestic Product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| RPK (Revenue Passenger Kilometres) | The RPK of an airline is the sum of the products obtained by multiplying the number of revenue passengers carried on each flight stage by the stage distance - it is the total number of kilometers traveled by all revenue passengers. |

| Load Factor | The load factor is a metric used in the airline industry that measures the percentage of available seating capacity that has been filled with passengers. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| International Transportation Safety Association (ITSA) | International Transportation Safety Association (ITSA) is an international network of heads of independent safety investigation authorities (SIA). |

| Available Seats Kilometre (ASK) | This metric is calculated by multiplying Available Seats (AS) in one flight, defined above, multiplied by the distance flown. |

| Gross Weight | The fully-loaded weight of an aircraft, also known as “takeoff weight,” which includes the combined weight of passengers, cargo, and fuel. |

| Airworthiness | The ability of an aircraft, or other airborne equipment or system, to operate in flight and on the ground without significant hazard to aircrew, ground crew, passengers or to other third parties. |

| Airworthiness Standards | Detailed and comprehensive design and safety criteria applicable to the category of aeronautical product (aircraft, engine or propeller). |

| Fixed Base Operator (FBO) | A business or organization that operates at an airport. An FBO provides aircraft operating services like maintenance, fueling, flight training, charter services, hangaring, and parking. |

| High Net worth Individuals (HNWIs) | High Net worth Individuals (HNWIs) are individuals with over USD 1 million in liquid financial assets. |

| Ultra High Net worth Individuals (UHNWIs) | Ultra High Net worth Individuals (UHNWIs) are individuals with over USD 30 million in liquid financial assets. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| EASA (European Aviation Safety Agency) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| Airborne Warning and Control System (AW&C) aircraft | Airborne Warning and Control System (AEW&C) aircraft is equipped with a powerful radar and on-board command and control center to direct the armed forces. |

| The North Atlantic Treaty Organization (NATO) | The North Atlantic Treaty Organization (NATO), also called the North Atlantic Alliance, is an intergovernmental military alliance between 30 member states – 28 European and two North American. |

| Joint Strike Fighter (JSF) | Joint Strike Fighter (JSF) is a development and acquisition program intended to replace a wide range of existing fighter, strike, and ground attack aircraft for the United States, the United Kingdom, Italy, Canada, Australia, the Netherlands, Denmark, Norway, and formerly Turkey. |

| Light Combat Aircraft (LCA) | A light combat aircraft (LCA) is a light, multirole jet/turboprop military aircraft, commonly derived from advanced trainer designs, designed for engaging in light combat. |

| Stockholm International Peace Research Institute (SIPRI) | Stockholm International Peace Research Institute (SIPRI) is an international institute that provides data, analysis, and recommendations for armed conflict, military expenditure, and arms trade as well as disarmament and arms control. |

| Maritime Patrol Aircraft (MPA) | A maritime patrol aircraft (MPA), also known as maritime reconnaissance aircraft is a fixed-wing aircraft designed to operate for long durations over water in maritime patrol roles, in particular, anti-submarine warfare (ASW), anti-ship warfare (AShW), and search and rescue (SAR). |

| Mach Number | The Mach number is defined as the ratio of true airspeed to the speed of sound at the altitude of a given aircraft. |

| Stealth Aircraft | Stealth is a Common term applied to low observable (LO) technology and doctrine, that makes an aircraft near invisible to radar, infrared or visual detection. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF