Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

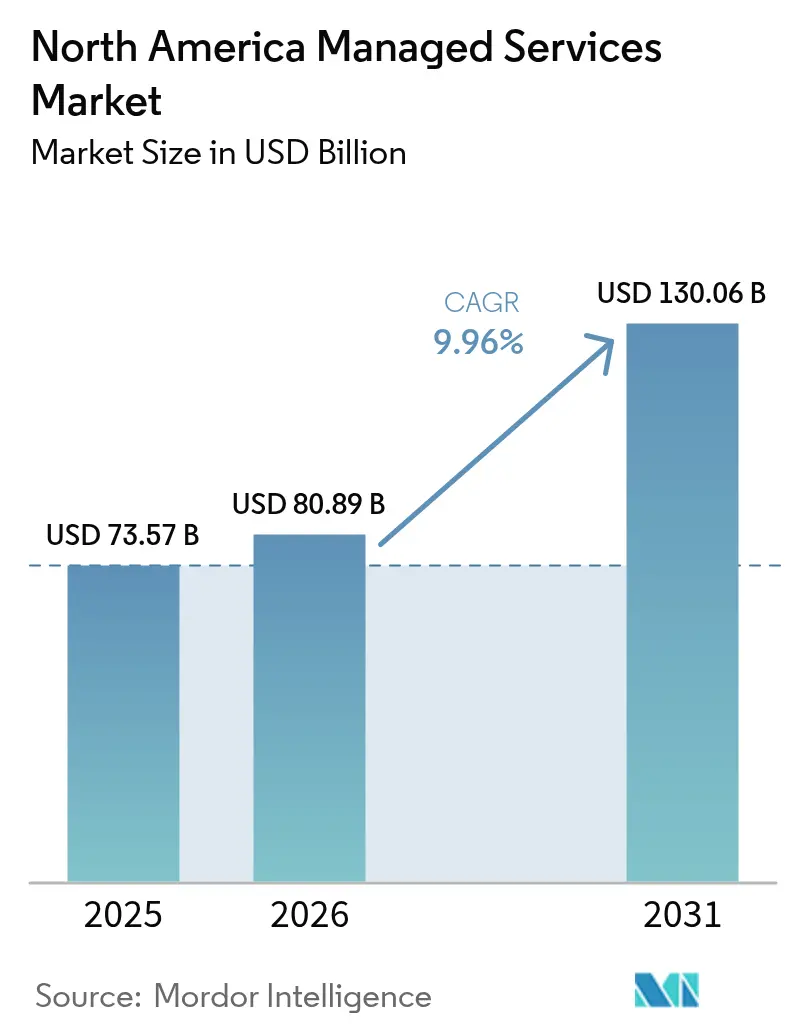

| Base Year Market Size (2025) | USD 73.57 Billion |

| Market Size (2026) | USD 80.89 Billion |

| Market Size (2031) | USD 130.06 Billion |

| Growth Rate (2026 - 2031) | 9.96% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Managed Services Market Analysis by Mordor Intelligence

The North America managed services market size is expected to grow from USD 73.57 billion in 2025 to USD 80.89 billion in 2026 and is forecast to reach USD 130.06 billion by 2031 at 9.96% CAGR over 2026-2031. Ongoing spending on cloud modernization, surging cyber-insurance premiums, and the proliferation of state privacy rules continue to push enterprises toward managed services partnerships that reduce compliance risk and deliver specialized expertise. Nearly three of every four regional enterprises now operate some mix of public and private clouds, making cross-platform management a top operational priority. Severe talent shortages in security, cloud architecture, and artificial intelligence amplify the need for external providers that can supply hard-to-hire skills at scale. Large deals increasingly link cost optimization commitments to service-level metrics, which strengthens the business case for AI-enabled automation inside service delivery platforms. Competitive intensity is rising as private-equity-backed consolidators buy regional specialists, broadening geographic reach and service breadth while maintaining the customer intimacy that mid-market buyers expect.

Key Report Takeaways

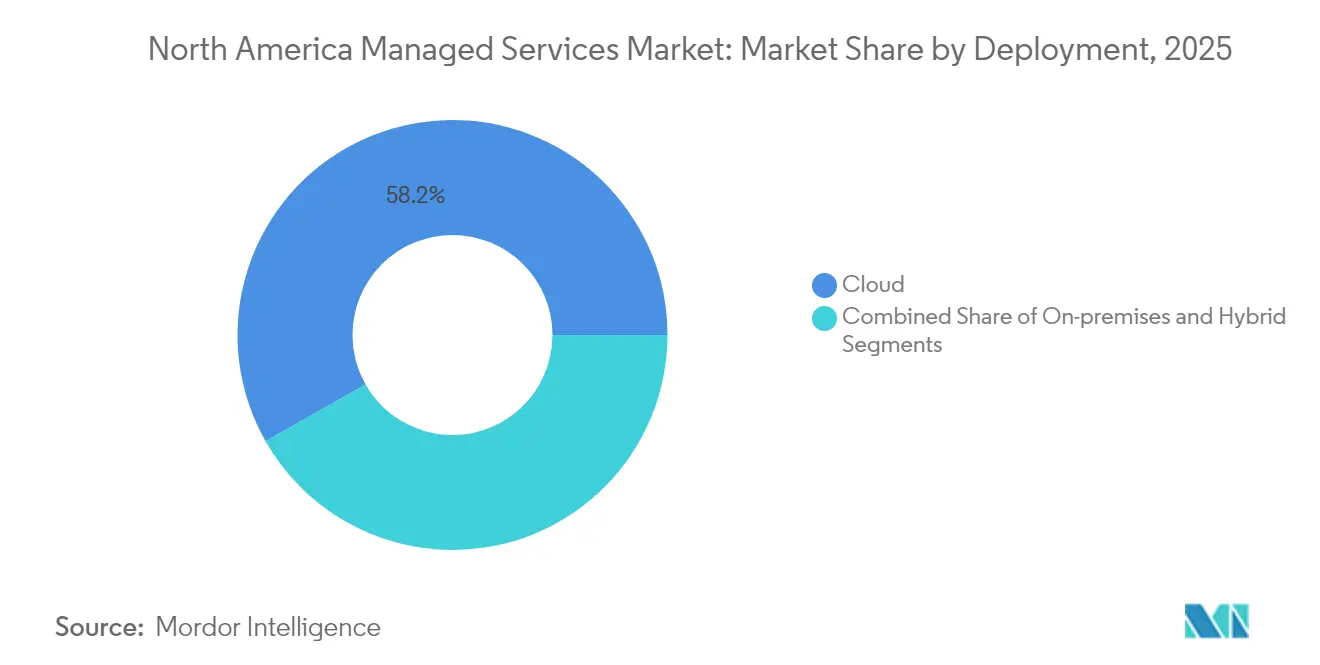

- By deployment, cloud-hosted solutions commanded 58.22% of North America managed services market share in 2025, while hybrid deployments are projected to expand at 11.03% CAGR through 2031.

- By service type, managed security services led with a 24.05% revenue share in 2025 in the North America managed services market; managed cloud and application services hold the fastest projected CAGR at 10.61% through 2031.

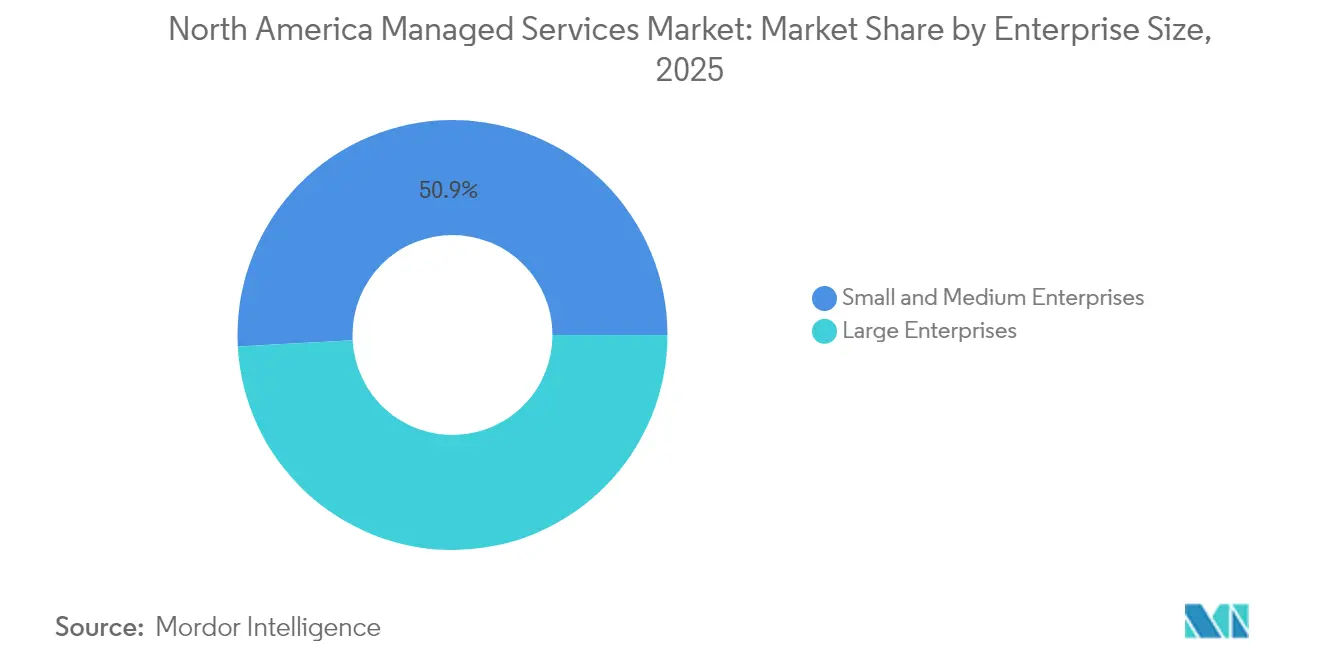

- By enterprise size, large enterprises accounted for 49.15% of the North America managed services market size in 2025, whereas small and medium enterprises are projected to record an 10.95% CAGR to 2031.

- By end user, the BFSI segment generated 24.21% of 2025 revenue in the North America managed services market, while healthcare and life sciences is on track for a 10.49% CAGR through 2031.

- By country, the United States represented 72.10% of regional spending in 2025 in the North America managed services market and is forecast to expand at an 11.26% CAGR over the next five years.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Managed Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enterprises shifting to hybrid and multi-cloud architectures | +2.8% | Global, with early gains in US West Coast, Northeast corridors | Medium term (2-4 years) |

| Rising cyber-threat landscape driving managed security adoption | +2.1% | North America and EU, spill-over to APAC | Short term (≤ 2 years) |

| IT skill shortages and need for cost optimisation | +1.9% | Global | Long term (≥ 4 years) |

| Accelerated digital transformation in SMEs | +1.7% | APAC core, spill-over to North America | Medium term (2-4 years) |

| State-level privacy laws spurring compliance-led outsourcing | +1.4% | National, with early gains in California, Texas, Florida | Short term (≤ 2 years) |

| Edge-compute managed services for 5G private networks and Industry 4.0 | +1.2% | North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Enterprises Shifting to Hybrid and Multi-Cloud Architectures

Roughly 75% of regional organizations now distribute workloads across multiple public clouds and on-premises infrastructure, which intensifies demand for managed orchestration and governance services. Vendor pricing actions that raise licensing costs are accelerating repatriation assessments and hybrid adoption strategies. Enterprises are standardizing on container platforms to limit lock-in and simplify portability, yet they still require outside expertise for policy enforcement, FinOps optimization, and workload migration. Managed service providers are capitalizing by bundling discovery, migration, and ongoing cost-control services into outcome-based contracts that tie fees to savings delivered. These factors collectively sustain the North America managed services market as a critical channel for multicloud operational excellence.

Rising Cyber-Threat Landscape Driving Managed Security Adoption

Threat actors now deploy artificial intelligence to automate reconnaissance and build polymorphic malware, which overwhelms internal security operations centers. New U.S. Securities and Exchange Commission incident-reporting rules obligate public companies to disclose material breaches within four business days, pushing boards to demand 24 × 7 detection and response coverage. Managed detection and response services fill the gap because enterprises often lack staff trained in threat hunting, forensics, and cloud-native security controls. Providers are investing in AI correlation engines that shrink dwell time and meet the stringent reporting windows. As cyber insurance underwriters impose higher premiums for organizations without third-party monitoring, managed security becomes both a technical requirement and a financial hedge.

IT Talent Shortages and Need for Cost Optimization

Nine in ten enterprises report difficulty hiring experts in cloud architecture, data science, and secure DevOps. Wage inflation adds further strain, raising the fully-loaded cost of experienced engineers and prompting financial officers to shift spending toward opex-based managed services contracts. Providers respond with talent-as-a-service models that embed specialized squads for cloud migrations, AI model operations, and zero-trust implementations. Continuous certification programs help MSPs retain scarce practitioners and pass skill depth on to clients. Because investors increasingly evaluate digital transformation projects on six-month return windows, the ability to deploy ready-made teams has become a critical advantage that sustains growth across the North America managed services market.

Accelerated Digital Transformation in SMEs

Small and medium enterprises once lagged digital pioneers, yet three in four now expect bigger technology budgets in 2025, and one in five plans to invest at least USD 10 million per initiative.[1]TEKsystems, “2025 State of Digital Transformation Report,” teksystems.com Many adopt platform-based managed services because they lack internal integration skills and cannot justify enterprise software licenses. Providers tailor packaged cloud migration, data analytics, and cybersecurity bundles that offer predictable monthly fees tied to usage. Pay-as-you-grow pricing helps SMEs scale without large capital outlays while gaining enterprise-grade resiliency and compliance. As a result, SME adoption adds a fresh layer of momentum to the North America managed services market by broadening the addressable base beyond Fortune 500 buyers.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-sovereignty and legacy-integration complexity | -1.8% | Global, with regulatory influence from GDPR, state privacy laws | Medium term (2-4 years) |

| Vendor lock-in and perceived loss of control | -1.2% | North America and EU | Long term (≥ 4 years) |

| Inflation-driven wage pressure eroding MSP margins | -0.9% | Global | Short term (≤ 2 years) |

| Sustainability-reporting costs for service providers | -0.6% | North America and EU, with early gains in California, New York | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Sovereignty and Legacy-Integration Complexity

Fourteen U.S. states now enforce comprehensive privacy statutes with varied residency and processing obligations, which complicates cross-border data architectures and lengthens implementation cycles. Many large enterprises retain decades-old proprietary systems that cannot move to public clouds without costly refactoring, forcing providers to blend on-premises support with cloud-native tooling. Compliance frameworks such as NIST SP 800-171 and sector-specific mandates in healthcare or finance require granular audit trails, adding overhead for managed service providers. These factors slow project kickoffs and in certain cases limit the revenue capture potential that otherwise fuels the North America managed services market.

Vendor Lock-in and Perceived Loss of Control

High-profile supplier consolidation and surprise price increases amplify customer fears of dependency. CIOs now draft exit clauses, data portability terms, and multi-provider structures into managed services contracts, which extends negotiation timelines. Technology leaders also worry that outsourcing strategic functions can diminish internal relevance, leading to organizational pushback. To address these concerns, providers increasingly propose hybrid engagement models that allow companies to retain governance over key workloads while outsourcing discrete tasks. Although such models support adoption, they narrow deal scope and temper revenue growth within the North America managed services industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Dominance Accelerates Hybrid Innovation

Cloud-hosted deployments generated 58.22% of North America managed services market revenue in 2025, while hybrid environments are forecast for an 11.03% CAGR through 2031. The surge reflects hyperscaler resilience, generous partner rebates, and marketplace procurement that simplify subscription terms. Hybrid adoption gains momentum as strict data-residency rules and edge-compute latency targets push certain workloads closer to users. Industrial firms use private 5G networks to link factories, then anchor data analytics in regional clouds managed by MSPs. As a result, providers rebound from purely lift-and-shift work to ongoing optimization engagements that balance cost, performance, and compliance across diverse infrastructures. The North America managed services market frequently embeds container management add-ons that deliver automated patching and policy enforcement for distributed clusters. Service catalogs now include FinOps dashboards that visualize chargeback and governance metrics, further cementing MSP involvement in cost stewardship.

By Service Type: Security Leadership Meets Cloud Acceleration

Managed security accounted for 24.05% of 2025 revenue, underscoring board-level urgency to harden defenses against AI-driven attacks. Managed cloud and application services claim the fastest forecast CAGR at 10.61%, propelled by enterprises that shift custom development into serverless and container environments yet still require external oversight. Legacy data-center services remain relevant for regulated workloads that must stay on-premises, but providers increasingly wrap them in automation and remote-management layers to improve margin profile. Unified communications, SD-WAN, and managed networks support hybrid work patterns that persist in 2025. Across categories, AI-based orchestration engines reduce manual effort, freeing engineers to move into consulting roles that drive higher bill rates. This pivot helps sustain profitability even as price competition intensifies across the North America managed services market.

By Enterprise Size: SME Momentum Challenges Large-Enterprise Dominance

Large enterprises represented 49.15% of North America managed services market share in 2025, leveraging multiyear budgets to negotiate broad outcome-based contracts covering infrastructure, applications, and cybersecurity. In contrast, SMEs demonstrate an 10.95% CAGR through 2031 as cloud-first strategies lower entry barriers. Providers package modular service blocks that align with SME cash-flow needs and regulatory thresholds. Many SMEs view MSPs as fractional CIOs who orchestrate vendor ecosystems and maintain compliance artifacts. The North America managed services industry therefore benefits from an expanding funnel of customers willing to consume standardized offerings, creating scale advantages for providers that specialize in specific verticals like dental practices, regional banks, or SaaS start-ups.

By End-user Vertical: BFSI Leadership Meets Healthcare Innovation

BFSI generated 24.21% of 2025 revenue, reinforced by interchange fee pressures that push banks to outsource non-core IT functions and focus spend on digital engagement. Robust regulatory frameworks such as FedLine compliance elevate the need for external audit support and real-time monitoring. Healthcare and life sciences exhibit the fastest 10.49% CAGR amid telehealth adoption, electronic health record modernization, and genomics workloads that demand high-performance compute with strict data privacy. Industrial settings use managed services to converge operational technology and IT under zero-trust frameworks, while retailers invest in omnichannel optimization that blends inventory analytics with customer-facing applications. The sector mix diversifies top-line growth across the North America managed services market, reducing dependence on any single vertical.

Geography Analysis

North American spending remains heavily concentrated in large metropolitan corridors, yet secondary cities in the Mountain West and Midwest post above-average growth as manufacturers deploy Industry 4.0 programs. The region is expected to grow, supported by deep cloud adoption and a patchwork of state privacy laws that incentivize outsourcing to compliance-ready providers. United States federal modernization initiatives drive multi-billion-dollar contract vehicles that often stipulate small-business participation, creating teaming opportunities for regional MSPs. In Canada, fintech regulation and public-sector cloud mandates sustain consistent contract flow despite softer macroeconomic indicators.

Mexico benefits from supply-chain realignment that encourages near-shore software development centers relying on managed cloud security to satisfy U.S. client compliance. State privacy rules in California, Texas, Florida, and Colorado add regional complexity that favors providers with embedded legal and audit experts. Cross-border data-flow negotiations under the new Canada-U.S. Data Bridge Agreement encourage harmonized controls that MSPs can standardize across multi-tenant platforms. The North America managed services market, therefore, grows not just in volume but in geographic nuance, demanding provider footprints that combine local delivery with centralized innovation hubs.

Competitive Landscape

The top 10 providers control roughly 49% of revenue, yet more than 5,000 regional and vertical specialists operate profitably within the long tail. Accenture closed 27 acquisitions in fiscal 2024 to deepen industry-specific capabilities, while IBM and Kyndryl expanded hyperscaler alliances to shift revenue toward higher-margin cloud services.[3]Accenture, “2024 Annual Report,” accenture.com Private equity funding exceeded USD 8 billion in completed transactions during 2024, fueling roll-ups that merge local MSPs into national platforms and accelerate the adoption of standardized AI-driven delivery tooling. Competitive differentiation now hinges on the ability to embed automation that compresses resolution time and surfaces predictive insights. Providers experiment with usage-based pricing that aligns incentives and mitigates perceived vendor lock-in. Partnerships with Amazon Web Services, Microsoft Azure, and Google Cloud unlock co-selling benefits that improve lead-generation economics across the North America managed services market. Vertical compliance accelerators, such as pre-mapped HIPAA controls, shorten sales cycles and shore up win rates against global integrators.

North America Managed Services Industry Leaders

AT&T Inc.

Fujitsu Limited

Cisco Systems, Inc.

Hewlett Packard Enterprise Company

International Business Machines Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Kyndryl posted USD 160 million in adjusted pretax income for Q3 FY 2025 and reported trailing-twelve-month signings of USD 16.3 billion, validating its pivot toward automation-led managed services.

- January 2025: Information Services Group recorded Q4 2024 Americas managed services ACV of USD 5.7 billion, including eight mega-deals that each topped USD 100 million.

- January 2025: IBM announced Q4 2024 revenue of USD 17.6 billion, with software up 10% year on year, reflecting client movement toward platform-driven managed services.

- December 2024: OMERS Private Equity acquired a majority stake in Integris, marking its first platform investment in the regional MSP space and signaling ongoing financial sponsor interest.

North America Managed Services Market Report Scope

Managed service is the practice of outsourcing, on a proactive basis, certain processes and functions intended to improve operations and cut expenses. It simplifies IT operations, increases user satisfaction, and improves service quality while reducing operating costs. Managed services options range from short-term post-go-live assistance to long-term application operations.

The North American managed services market is segmented by deployment (on-premise and cloud), type (managed data center, managed security, managed communications, managed network, managed infrastructure, and managed mobility), enterprise size (small enterprises, medium enterprises, and large enterprises), end-user vertical (BFSI, IT and telecom, healthcare, entertainment and media, retail, manufacturing, government, and other end-user verticals), and country (United States and Canada). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Deployment

| On-premises |

| Cloud-hosted |

| Hybrid |

By Service Type

| Managed Data Centre |

| Managed Security |

| Managed Communications (UCaaS) |

| Managed Network (LAN/WAN, SD-WAN) |

| Managed Infrastructure and Platform |

| Managed Mobility and Workplace |

| Managed Application and DevOps |

By Enterprise Size

| Small and Medium Enterprises |

| Large Enterprises |

By End-user Vertical

| BFSI |

| IT and Telecom |

| Healthcare and Life Sciences |

| Media and Entertainment |

| Retail and E-commerce |

| Manufacturing and Industrial |

| Government and Public Sector |

| Energy and Utilities |

| Other End-user Verticals |

By Country

| United States |

| Canada |

| Mexico |

| By Deployment | On-premises |

| Cloud-hosted | |

| Hybrid | |

| By Service Type | Managed Data Centre |

| Managed Security | |

| Managed Communications (UCaaS) | |

| Managed Network (LAN/WAN, SD-WAN) | |

| Managed Infrastructure and Platform | |

| Managed Mobility and Workplace | |

| Managed Application and DevOps | |

| By Enterprise Size | Small and Medium Enterprises |

| Large Enterprises | |

| By End-user Vertical | BFSI |

| IT and Telecom | |

| Healthcare and Life Sciences | |

| Media and Entertainment | |

| Retail and E-commerce | |

| Manufacturing and Industrial | |

| Government and Public Sector | |

| Energy and Utilities | |

| Other End-user Verticals | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the North America managed services market in 2026?

The market reached USD 80.89 billion in 2026 and is projected to hit USD 130.06 billion by 2031.

Which service category generates the greatest revenue?

Managed security services lead with 24.05% of 2025 revenue, propelled by rising threat complexity.

Why are hybrid deployments growing faster than fully cloud or on-premises models?

Hybrid designs help enterprises meet data-residency rules and control costs while leveraging public-cloud scalability, resulting in an 11.03% CAGR through 2031.

Which end-user vertical shows the fastest spending growth?

Healthcare and life sciences is expected to grow at a 10.49% CAGR as digital health adoption accelerates.

What is driving private equity interest in managed service providers?

Recurring revenue, scalable automation platforms, and cross-sell opportunities have pushed PE investments above USD 8 billion in recent transactions.

Page last updated on: