| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 73.57 Billion |

| Market Size (2030) | USD 119.18 Billion |

| CAGR (2025 - 2030) | 10.13 % |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

North America Managed Services Market Analysis

The North America Managed Services Market size is estimated at USD 73.57 billion in 2025, and is expected to reach USD 119.18 billion by 2030, at a CAGR of 10.13% during the forecast period (2025-2030).

The North American managed services landscape is experiencing a fundamental shift driven by the rapid evolution of IT infrastructure and digital transformation initiatives. Organizations across industries are increasingly integrating sophisticated IT managed services tailored to their specific business needs, focusing on comprehensive technology assessments and customized roadmaps. This transformation is particularly evident in the financial services sector, where, according to Varonis, the average financial service employee now has access to approximately 11 million files, highlighting the growing complexity of data management and security requirements. Companies are responding by partnering with managed service providers who can deliver end-to-end solutions that address these complexities while ensuring compliance and operational efficiency.

The market is witnessing a significant trend toward specialized industry-specific solutions, particularly in sectors such as healthcare, financial services, and retail. Managed service providers are developing vertical-specific expertise and solutions that address unique industry challenges and regulatory requirements. For instance, in the United States, the Consumer Technology Association reports that connected devices have reached a record-breaking value of USD 487 billion, demonstrating the massive scale of technology adoption across industries. This proliferation of connected devices has created new opportunities for managed service providers to offer specialized device management, security, and optimization services.

Security and compliance have emerged as critical focus areas in the managed services landscape, with organizations seeking comprehensive protection against evolving cyber threats. Service providers are responding by expanding their security offerings beyond traditional endpoint protection to include advanced threat detection, compliance monitoring, and incident response capabilities. This trend is particularly pronounced in the financial sector, where regulatory requirements and the need for robust data protection have led to increased adoption of managed security services. Companies are increasingly looking for providers who can offer integrated security solutions that protect both on-premise and cloud-based assets while ensuring regulatory compliance.

The market is also characterized by strategic partnerships and consolidation activities aimed at expanding service capabilities and geographic reach. Managed service providers are actively pursuing acquisitions and partnerships to enhance their technical capabilities, particularly in areas such as cloud managed services, artificial intelligence, and automation. For example, KPaul Properties LLC's partnership with Fujitsu resulted in a 15% reduction in costs and achieved 95% uptime through virtualization, demonstrating the tangible benefits of strategic managed services partnerships. This trend toward consolidation is enabling providers to offer more comprehensive service portfolios while improving their ability to serve clients across multiple regions and industries.

North America Managed Services Market Trends

Increasing Shift to Hybrid IT

The adoption of IoT solutions, which connect hardware devices, embedded software, communication services, and managed services, has become vital to business success in North America. According to Vodafone's recent industry analysis, the Internet of Things (IoT) is considered crucial by 92% of US businesses for their operational success. This increasing IoT adoption has pushed organizations toward hybrid IT environments, as cloud-based solutions are being leveraged primarily to derive value from the data generated by IoT devices. The legacy IT infrastructure of enterprises often relies on the cloud for establishing connections with IoT devices, driving the need for hybrid IT solutions that can effectively manage both on-premises and cloud environments.

The enterprise mobility trend has emerged as another significant factor driving hybrid IT adoption, with companies focusing on business strategies and core competencies that fuel the utilization of bring-your-own-device (BYOD) policies. According to Cisco's analysis, enterprises with BYOD policies in place save approximately $350 per employee annually, with reactive programs potentially boosting these savings to as much as $1,300 per employee annually. This transition toward hybrid environments is further supported by organizations realizing the drawbacks of purely public or private cloud services, leading them to seek hybrid approaches that provide advantages of both architectures while minimizing their respective limitations. The hybrid model enables businesses to leverage the best of public and private cloud features, offering a more consistent, secure, and faster experience for data processing while maintaining the governance and compliance requirements of on-premises systems.

Understand The Key Trends Shaping This Market

Download PDF

Improved Cost and Operational Efficiency

Managed services have demonstrated significant improvements in operational efficiency and cost reduction for organizations across North America. According to industry analysis by Cisco Systems, managed services reduce recurring in-house costs by 30-40% while increasing operational efficiency by 50-60%. This substantial improvement in efficiency enables organizations to take advantage of emerging technologies without the burden of high capital expenditure or operational costs. The relentless focus on continuous improvement of operational and business processes stands as the most significant benefit, allowing organizations to optimize their resources while maintaining high-quality service delivery.

The adoption of managed network services and managed security services has particularly benefited organizations in areas such as network management and security operations. Industry data indicates that 95% of network changes are traditionally performed manually, resulting in operational costs being 2-3 times higher than the network's value. Managed service providers address this challenge by automating and streamlining these processes, significantly reducing both costs and potential errors. Furthermore, managed services enable organizations to access scalable third-party delivery infrastructure on a pay-per-use basis, allowing them to increase their service coverage and handle higher volumes without substantial capital investments. This model has proven particularly effective for risk and compliance management, where organizations can leverage expert services while maintaining cost predictability and operational efficiency.

Segment Analysis: By Deployment

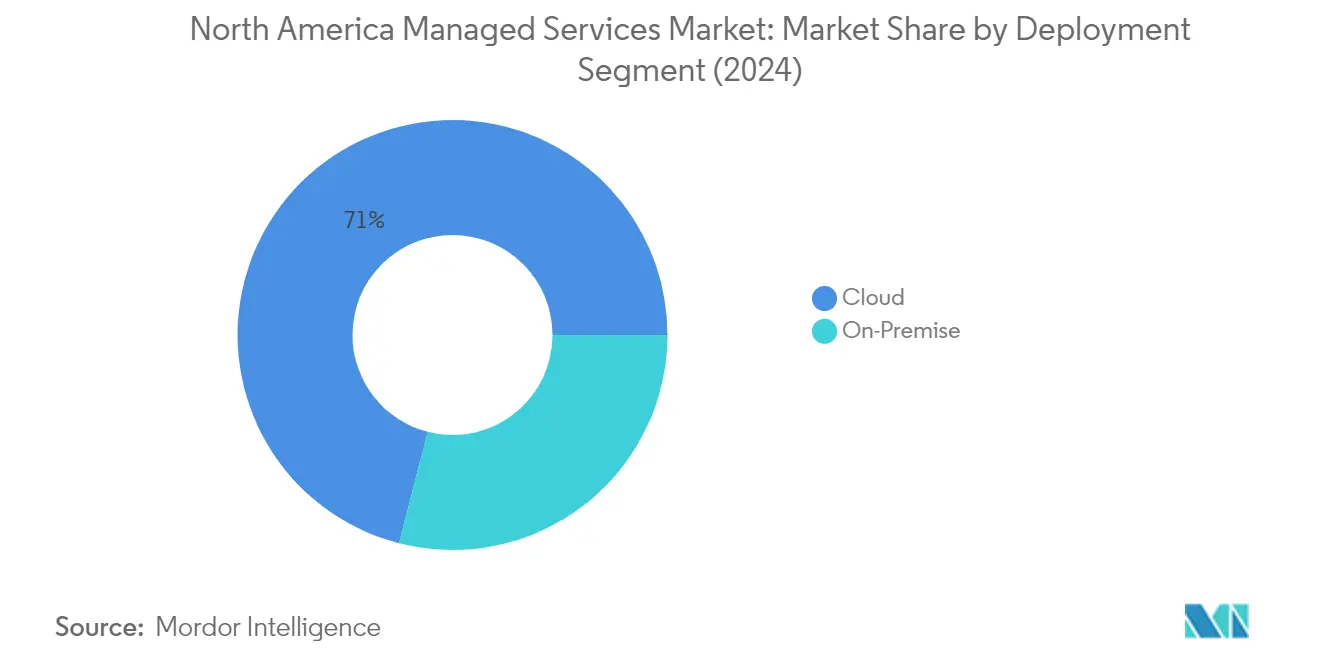

Cloud Segment in North America Managed Services Market

The cloud segment has emerged as the dominant force in the North America Managed Services Market, commanding approximately 71% of the total market share in 2024, equivalent to around USD 46.10 billion. This substantial market presence is driven by the increasing adoption of managed network services and managed security services across various industries, as organizations seek to leverage the benefits of scalability, flexibility, and cost-effectiveness offered by cloud deployments. The segment's growth is further accelerated by the rising demand for cloud-based managed security services, data analytics, and infrastructure management solutions. Cloud-based managed services are particularly attractive to businesses looking to reduce capital expenditure while maintaining access to cutting-edge technology and expertise. The segment's prominence is reinforced by the growing trend of hybrid IT environments and the increasing need for seamless integration between various cloud platforms. Additionally, the shift towards remote work models and digital transformation initiatives has further catalyzed the adoption of cloud-based managed services across North America.

On-Premise Segment in North America Managed Services Market

The on-premise segment continues to maintain its significance in the North America Managed Services Market, particularly among organizations with specific regulatory compliance requirements or those requiring complete control over their IT infrastructure. This segment is characterized by traditional IT service delivery models where infrastructure and applications are managed within the organization's physical premises. On-premise solutions remain crucial for industries such as healthcare, financial services, and government sectors, where data sovereignty and security concerns necessitate local infrastructure management. The segment's resilience is supported by organizations that require customized solutions, have legacy systems integration needs, or operate in environments where cloud adoption faces technical or regulatory constraints. Despite the growing cloud adoption trend, on-premise managed services continue to evolve, incorporating advanced monitoring tools, automation capabilities, and enhanced security features to meet modern business requirements.

Segment Analysis: By Type

Managed Network Segment in North America Managed Services Market

The managed network services segment dominates the North America Managed Services Market, holding approximately 45% market share in 2024. This significant market position is driven by the increasing complexity of IT environments and the growing need for greater network accessibility and enhanced business processes at minimum cost. Organizations are increasingly becoming interested in advanced management tools and new network architectures that leverage machine learning and artificial intelligence to create self-driving or autonomous networks. The segment's growth is further supported by the rapid adoption of cloud-based solutions, the proliferation of IoT devices, and the increasing demand for secure and reliable network infrastructure across various industries.

Managed Mobility Segment in North America Managed Services Market

The managed mobility services segment is experiencing the fastest growth in the North America Managed Services Market, with an expected growth rate of approximately 22% during 2024-2029. This remarkable growth is primarily driven by the increasing adoption of BYOD (Bring-Your-Own-Device) policies across multiple industries and the growing need for enterprise mobility management solutions. Organizations are increasingly focusing on mobile-first strategies to enhance productivity without compromising security and privacy in the workplace. The segment's growth is further accelerated by the rising integration of IoT devices, the need for secure mobile device management, and the increasing demand for seamless mobile application deployment and management services.

Remaining Segments in North America Managed Services Market

The other significant segments in the market include managed data services, managed security services, Managed Communications, and managed infrastructure services. The Managed Data Center segment plays a crucial role in helping organizations manage their growing data storage and computing needs, while Managed Security services focus on providing comprehensive cybersecurity solutions and threat management. Managed Communications services facilitate unified communications and collaboration solutions across enterprises, and Managed Infrastructure services help organizations optimize their IT infrastructure operations. Each of these segments contributes uniquely to the overall market dynamics, addressing specific technological needs and challenges faced by organizations in their digital transformation journey.

Segment Analysis: By Enterprise Size

Large Enterprises Segment in North America Managed Services Market

Large enterprises dominate the North America managed services market, accounting for approximately 63% of the total market value in 2024. These enterprises are increasingly adopting managed services to handle their complex IT infrastructure needs while focusing on their core business operations. The segment's prominence is driven by enterprises' substantial IT budgets, complex technological requirements, and the need for comprehensive end-to-end managed services solutions. Large enterprises typically opt for managed services from integrated service providers and large MSPs as these providers offer superior technology support, minimal downtime, robust security measures, and cutting-edge network solutions that are crucial for maintaining uninterrupted business processes. The adoption of cloud services, BYOD policies, big data analytics, AI, and machine learning environments are major factors driving large enterprises to rely on managed service providers as they focus on accelerating their digital transformation initiatives.

Small Enterprises Segment in North America Managed Services Market

The small enterprises segment is projected to experience the fastest growth in the North America managed services market from 2024 to 2029, with an expected growth rate of approximately 14%. This rapid growth is primarily driven by the increasing recognition among small enterprises of the cost-effectiveness and operational benefits offered by managed services. Small enterprises are finding managed IT services particularly attractive as they often lack the financial resources or human capital to maintain large internal IT teams. The segment's growth is further fueled by the rising need for multi-device operations, data management practices, and comprehensive IT support. These enterprises benefit significantly from MSPs' access to trained IT professionals, specialized expertise, and the ability to provide focused assistance for multiple challenges. The trend toward remote monitoring, updating, and managing organizations' document management infrastructure is also contributing to the segment's rapid expansion.

Remaining Segments in Enterprise Size Segmentation

Medium enterprises represent a significant portion of the North America managed services market, positioning themselves between small and large enterprises in terms of service requirements and adoption patterns. This segment demonstrates unique characteristics as these organizations typically have more complex needs than small enterprises but operate with more limited resources compared to large enterprises. Medium enterprises are increasingly turning to managed service providers to help them scale effectively while maintaining operational efficiency. They particularly value managed services for their ability to provide enterprise-level reporting, analytics, collaboration tools, and security solutions without requiring substantial upfront investments. The segment's adoption of managed services is driven by the need to focus on core business activities while leveraging external expertise for IT operations and infrastructure management.

Segment Analysis: By End-User Vertical

IT and Telecom Segment in North America Managed Services Market

The IT and Telecom sector has emerged as the dominant force in the North America Managed Services Market, commanding approximately 30% of the total market share in 2024. This segment's leadership position is driven by the high rate of technological adoption, increased implementation of BYOD policies, and growing need for enhanced security due to rapidly expanding data volumes among organizations. The sector is experiencing robust growth as telecommunication companies face constant pressure to deliver innovative services at lower costs while maintaining their competitive edge. The adoption of software-defined networking (SDN) and network function virtualization (NFV) technologies is reshaping how enterprises architect their wide area networks to meet growing network requirements. Additionally, the shift toward remote working has accelerated the adoption of SD-WAN solutions, while the increasing demand for cloud-based managed services has been fueled by government regulations and business transformation initiatives. The segment's growth is further supported by the rising need for secured networks and the integration of emerging technologies like 5G, artificial intelligence, and edge computing.

Remaining Segments in End-User Vertical

The North America Managed Services Market encompasses several other significant segments including BFSI, Healthcare, Entertainment and Media, Retail, Manufacturing, and Government sectors. The BFSI sector has shown strong adoption driven by the need for enhanced data security and regulatory compliance requirements. Healthcare organizations are increasingly leveraging managed services for electronic health records management and ensuring HIPAA compliance. The Entertainment and Media segment is focusing on content management and streaming services infrastructure, while the Retail sector is embracing managed services for POS systems and e-commerce platforms. The Manufacturing sector is utilizing these services for industrial automation and IoT integration, while the Government sector is implementing managed services to modernize public infrastructure and enhance cybersecurity measures. Each of these segments contributes uniquely to the market's dynamics, with varying requirements for network security, data management, and operational efficiency improvements.

North America Managed Services Market Geography Segment Analysis

North America Managed Services Market in the United States

The United States dominates the North American managed services landscape, commanding approximately 86% of the total market share in 2024. The country's market leadership is driven by significant efforts in IoT adoption, automation implementation, and cloud-based service integration. The presence of major technology giants and their continuous investments in data center expansions has created a robust infrastructure backbone. The market is witnessing increased adoption of AI-enabled managed services, with enterprises leveraging these solutions for network traffic control, automated issue resolution, and enhanced customer service through AI-powered chatbots. The US government's renewed focus on technological advancement, particularly in areas like cybersecurity and cloud computing, has created additional growth opportunities for managed service providers (MSPs). The market is also seeing a transformation in delivery models, with an increasing number of providers offering consumption-based and pay-as-you-go options to meet diverse client needs.

North America Managed Services Market in Canada

Canada represents a dynamic growth market in the North American managed services landscape, projected to expand at approximately 13% CAGR from 2024 to 2029. The country's market is characterized by a strong emphasis on cloud adoption and digital transformation initiatives across various industries. Canadian businesses are increasingly embracing multi-cloud environments and automation technologies, driving demand for sophisticated IT managed services solutions. The market is particularly active in unified communications as a service (UCaaS) and contact center as a service (CCaaS) segments, with emerging players offering innovative cloud-based solutions. The government's "cloud-first" strategy has been instrumental in driving adoption, particularly among public sector organizations. Canadian managed service providers (MSPs) are differentiating themselves through specialized offerings in areas such as data sovereignty compliance, managed security services, and hybrid cloud management, addressing the unique regulatory and business requirements of the Canadian market.

North America Managed Services Market in Other Regions

The North American managed services market demonstrates a concentrated structure primarily focused on the United States and Canada, with these two nations driving the majority of market developments and innovations. The market dynamics are shaped by the unique regulatory environments, technological infrastructures, and business requirements specific to each country. While the United States leads in terms of market size and technological adoption, Canada shows promising growth potential with its progressive policies and increasing digital transformation initiatives. The integration of emerging technologies, such as artificial intelligence, machine learning, and edge computing, is reshaping the managed services landscape across both nations. The market continues to evolve with increasing emphasis on managed cloud services, managed communication services, and digital transformation solutions, reflecting the broader technological trends in the North American region.

Get Analysis on Important Geographic Markets

Download PDF

North America Managed Services Industry Overview

Top Companies in North America Managed Services Market

The North American managed services market features prominent players like IBM, Microsoft, Cisco, AT&T, HP, Dell Technologies, and Verizon leading the competitive landscape. These companies are actively pursuing product innovation through enhanced managed cloud services capabilities, advanced security solutions, and integrated service offerings that combine traditional infrastructure management with emerging technologies like AI, IoT, and edge computing. Strategic partnerships and collaborations, particularly in cloud services and managed security services, have become increasingly common as companies seek to expand their service portfolios and technical capabilities. Market leaders are demonstrating operational agility by rapidly adapting to remote work demands, implementing automation solutions, and developing specialized vertical-specific offerings. Geographic expansion strategies, particularly targeting underserved mid-market segments and regional markets, are being complemented by investments in emerging technologies and service delivery platforms to maintain competitive advantages.

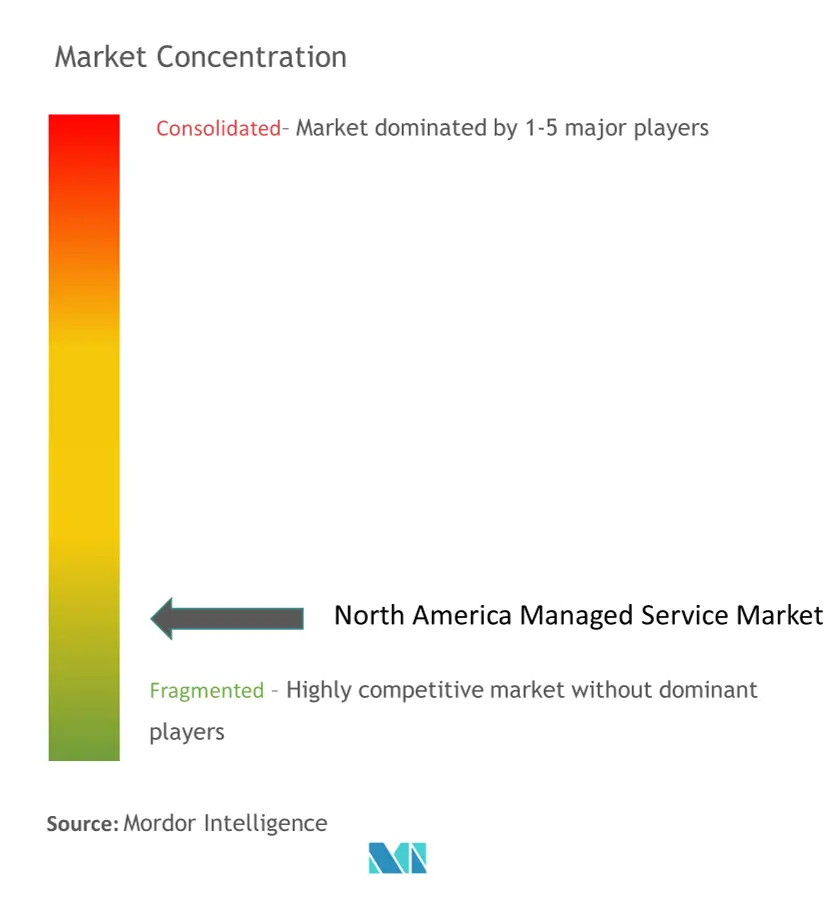

High Market Consolidation Drives Strategic Growth

The managed services market in North America is characterized by a mix of global technology conglomerates and specialized regional providers, with large enterprises dominating the high-end market segment while regional players focus on small and medium businesses. The market structure shows significant consolidation among top-tier providers who leverage their extensive infrastructure, established client relationships, and comprehensive service portfolios to maintain market leadership. These dominant players are increasingly expanding their capabilities through strategic acquisitions of specialized providers, particularly in areas like cloud services, managed security services, and vertical-specific solutions.

The market is witnessing accelerated merger and acquisition activity, with larger providers acquiring smaller, specialized firms to enhance their technical capabilities and geographic reach. This consolidation trend is particularly evident in the cloud services and security segments, where established players are seeking to strengthen their market positions through strategic acquisitions. Independent MSPs are increasingly forming strategic alliances and partnerships to compete with larger competitors, while also focusing on developing niche expertise in specific industries or technologies to maintain their market relevance.

Innovation and Specialization Drive Future Success

Success in the managed services market increasingly depends on providers' ability to deliver comprehensive, integrated solutions while maintaining specialization in high-demand areas like cybersecurity, cloud services, and industry-specific solutions. Market leaders are investing heavily in developing proprietary technologies and platforms, while also maintaining strong partnerships with major cloud and technology providers. The ability to offer flexible, scalable solutions that address specific industry requirements while providing comprehensive security and compliance capabilities has become crucial for maintaining competitive advantage.

Future market success will require providers to balance standardization with customization, offering modular service packages that can be tailored to specific client needs while maintaining operational efficiency. Companies must also navigate evolving regulatory requirements, particularly in areas like data privacy and security, while maintaining service quality and cost competitiveness. The increasing adoption of multi-cloud and hybrid environments presents both opportunities and challenges, requiring providers to develop sophisticated orchestration capabilities and maintain expertise across multiple platforms. Success will also depend on providers' ability to demonstrate clear value propositions and return on investment to increasingly sophisticated buyers while managing the risk of substitution from in-house IT operations. Additionally, managed support services and managed operations are becoming critical components of service offerings, enabling providers to deliver end-to-end solutions that meet diverse client needs.

North America Managed Services Market Leaders

-

Fujitsu Ltd

-

Cisco Systems Inc.

-

IBM Corporation

-

AT&T Inc.

-

HP Development Company LP

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

North America Managed Services Market News

- January 2024: AVI-SPL introduced its Enterprise Managed Services solution, which mainly includes audio-visual (AV), digital signage, and unified communications (UC) solutions for the workplace, in rooms, and on the cloud. The key features of AVI-SPL’s Enterprise Managed Services are its extensive coverage, simple deployment, worldwide reach, and comprehensive support.

- October 2023: IBM launched a managed cybersecurity service that leverages AI and automation to help organizations detect and respond to threats across cloud and on-premise environments. Managed cybersecurity services provide ongoing management and monitoring of a company’s security operations by a team of experts.

North America Managed Services Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

-

4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Increasing Shift to Hybrid IT

- 5.1.2 Improved Cost and Operational Efficiency

-

5.2 Market Challenges

- 5.2.1 Integration, Regulatory Issues, and Reliability Concerns

6. MARKET SEGMENTATION

-

6.1 By Deployment

- 6.1.1 On-premise

- 6.1.2 Cloud

-

6.2 By Type

- 6.2.1 Managed Data Center

- 6.2.2 Managed Security

- 6.2.3 Managed Communications

- 6.2.4 Managed Network

- 6.2.5 Managed Infrastructure

- 6.2.6 Managed Mobility

-

6.3 By Enterprise Size

- 6.3.1 Small Enterprises

- 6.3.2 Medium Enterprises

- 6.3.3 Large Enterprises

-

6.4 By End-user Vertical

- 6.4.1 BFSI

- 6.4.2 IT and Telecom

- 6.4.3 Healthcare

- 6.4.4 Entertainment and Media

- 6.4.5 Retail

- 6.4.6 Manufacturing

- 6.4.7 Government

- 6.4.8 Other End-user Verticals

-

6.5 By Country

- 6.5.1 United States

- 6.5.2 Canada

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 Fujitsu Ltd

- 7.1.2 Cisco Systems Inc.

- 7.1.3 IBM Corporation

- 7.1.4 AT&T Inc.

- 7.1.5 HP Development Company LP

- 7.1.6 Microsoft Corporation

- 7.1.7 Verizon Communications Inc.

- 7.1.8 Dell Technologies Inc.

- 7.1.9 Citrix Systems Inc.

- 7.1.10 Rackspace Inc.

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

North America Managed Services Industry Segmentation

Managed service is the practice of outsourcing, on a proactive basis, certain processes and functions intended to improve operations and cut expenses. It simplifies IT operations, increases user satisfaction, and improves service quality while reducing operating costs. Managed services options range from short-term post-go-live assistance to long-term application operations.

The North American managed services market is segmented by deployment (on-premise and cloud), type (managed data center, managed security, managed communications, managed network, managed infrastructure, and managed mobility), enterprise size (small enterprises, medium enterprises, and large enterprises), end-user vertical (BFSI, IT and telecom, healthcare, entertainment and media, retail, manufacturing, government, and other end-user verticals), and country (United States and Canada). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Deployment | On-premise |

| Cloud | |

| By Type | Managed Data Center |

| Managed Security | |

| Managed Communications | |

| Managed Network | |

| Managed Infrastructure | |

| Managed Mobility | |

| By Enterprise Size | Small Enterprises |

| Medium Enterprises | |

| Large Enterprises | |

| By End-user Vertical | BFSI |

| IT and Telecom | |

| Healthcare | |

| Entertainment and Media | |

| Retail | |

| Manufacturing | |

| Government | |

| Other End-user Verticals | |

| By Country | United States |

| Canada |

Need A Different Region or Segment?

Customize Now

North America Managed Services Market Research Faqs

How big is the North America Managed Services Market?

The North America Managed Services Market size is expected to reach USD 73.57 billion in 2025 and grow at a CAGR of 10.13% to reach USD 119.18 billion by 2030.

What is the current North America Managed Services Market size?

In 2025, the North America Managed Services Market size is expected to reach USD 73.57 billion.

Who are the key players in North America Managed Services Market?

Fujitsu Ltd, Cisco Systems Inc., IBM Corporation, AT&T Inc. and HP Development Company LP are the major companies operating in the North America Managed Services Market.

What years does this North America Managed Services Market cover, and what was the market size in 2024?

In 2024, the North America Managed Services Market size was estimated at USD 66.12 billion. The report covers the North America Managed Services Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the North America Managed Services Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

North America Managed Services Market Research

Mordor Intelligence offers a comprehensive analysis of the managed services industry. We specialize in IT managed services and managed operations research. Our extensive coverage includes crucial sectors such as cloud managed services, managed security services, and managed print services. The report provides detailed insights into MSP operations, managed cybersecurity services, and managed network services. It is available in an easy-to-read report PDF format for download. Our analysis also covers managed hosting services, managed data services, and emerging managed IoT services.

Stakeholders gain from our in-depth analysis of managed infrastructure services, managed mobility services, and managed support services. The report examines managed backup services and managed application services, while also exploring trends in technology management services. Our comprehensive coverage includes managed storage services, managed connectivity, and managed business services. Additionally, it covers managed workplace services and managed communication services. The analysis also encompasses IT outsourcing services and managed telecommunications, providing stakeholders with actionable insights for strategic decision-making.