Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

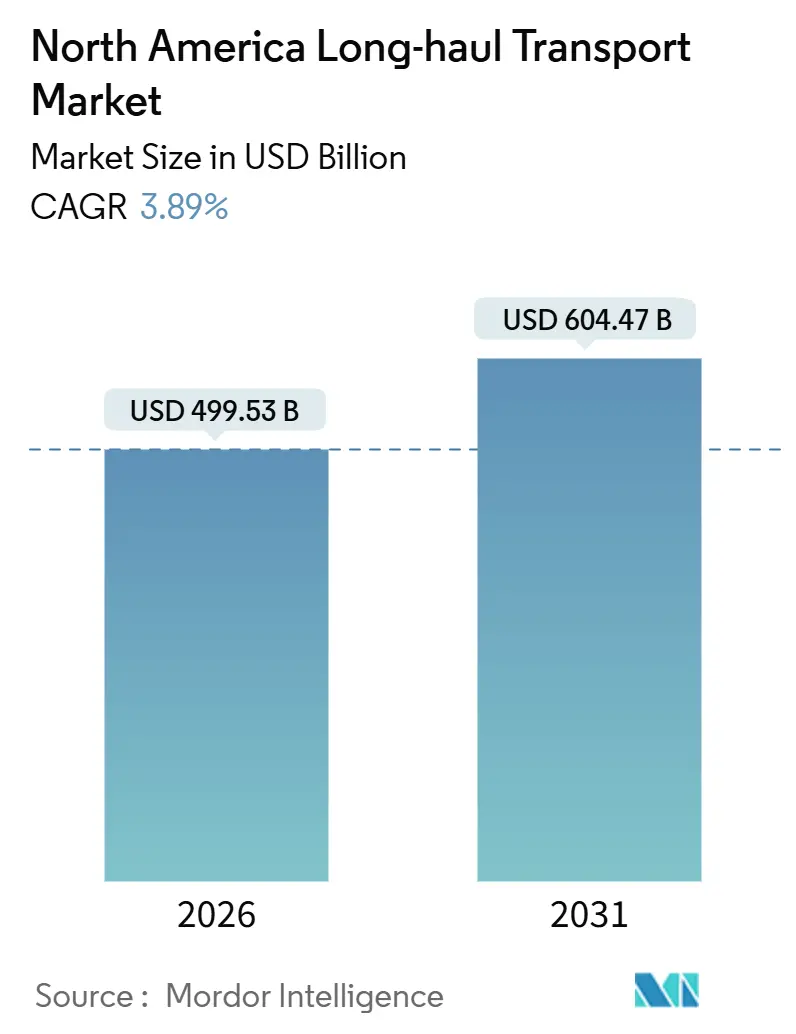

| Market Size (2026) | USD 499.53 Billion |

| Market Size (2031) | USD 604.47 Billion |

| Growth Rate (2026 - 2031) | 3.89% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Long-haul Transport Market Analysis by Mordor Intelligence

The North America long-haul transport market size is estimated at USD 499.53 billion in 2026, and is expected to reach USD 604.47 billion by 2031, at a CAGR of 3.89% during the forecast period (2026-2031). Intensifying cross-border freight flows under the United States-Mexico-Canada Agreement (USMCA), e-commerce fulfillment models that reward fast replenishment, and capacity constraints linked to electronic-logging-device enforcement continue to underpin steady growth in the North America long-haul transport market. Spot rates moderated in late 2025, yet disciplined fleet additions and persistent driver shortages kept contract pricing firmer than historical down-cycles. Omnichannel retailers pulled inventory closer to consumption zones, which broadened less-than-truckload (LTL) demand, while manufacturing reshoring from Asia to Mexico and the United States lifted north-south lane volumes. Carriers that deploy aerodynamic tractors and fuel-saving trailers gained a cost edge as Environmental Protection Agency (EPA) Phase 3 standards drew closer, and digital load-matching platforms compressed booking lead times from hours to minutes.

Key Report Takeaways

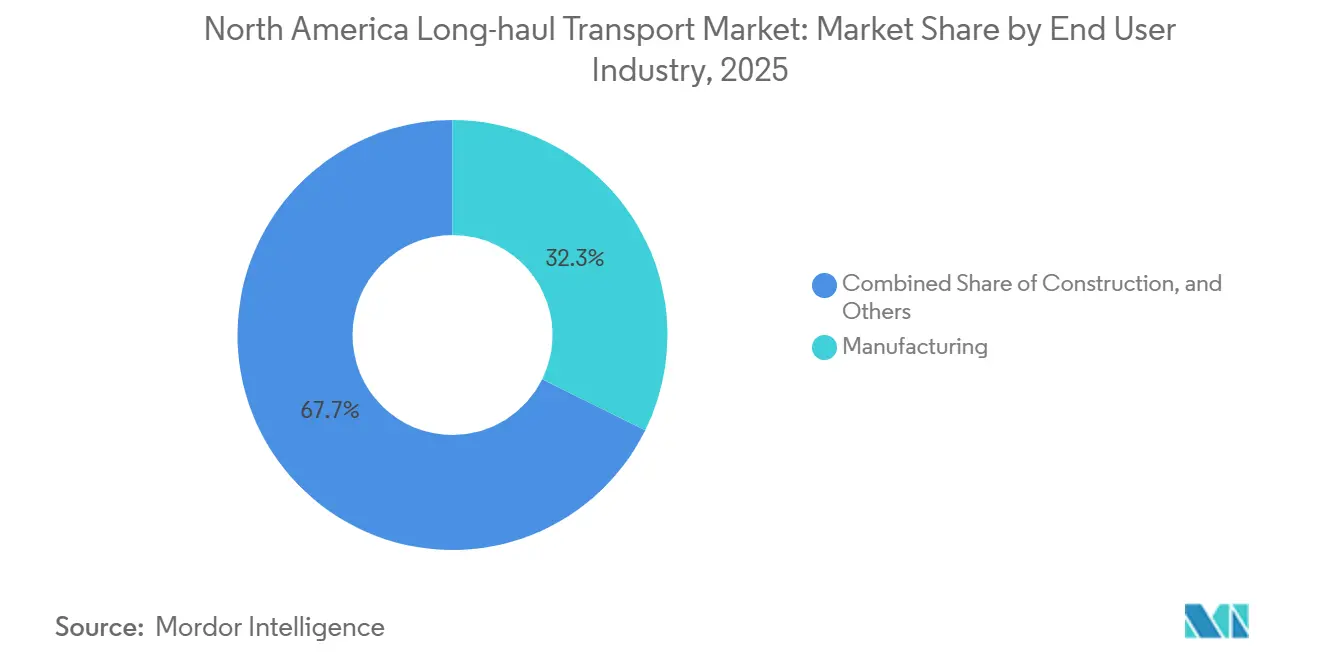

- By end user, manufacturing captured a 32.30% North America long-haul transport market share in 2025; Wholesale and Retail Trade is poised to expand at a 4.41% CAGR (2026-2031) and will be the fastest growing end-user segment through 2031.

- By destination type, domestic shipments accounted for 62.51% of the North America long-haul transport market size in 2025, while international movements are projected to register a 4.47% CAGR (2026-2031) as nearshoring accelerates.

- By truckload specification type, Full-Truck-Load (FTL) operations dominated with 79.88% revenue share in 2025; the LTL segment is forecast to grow at 4.30% CAGR (2026-2031), the quickest within truckload specifications.

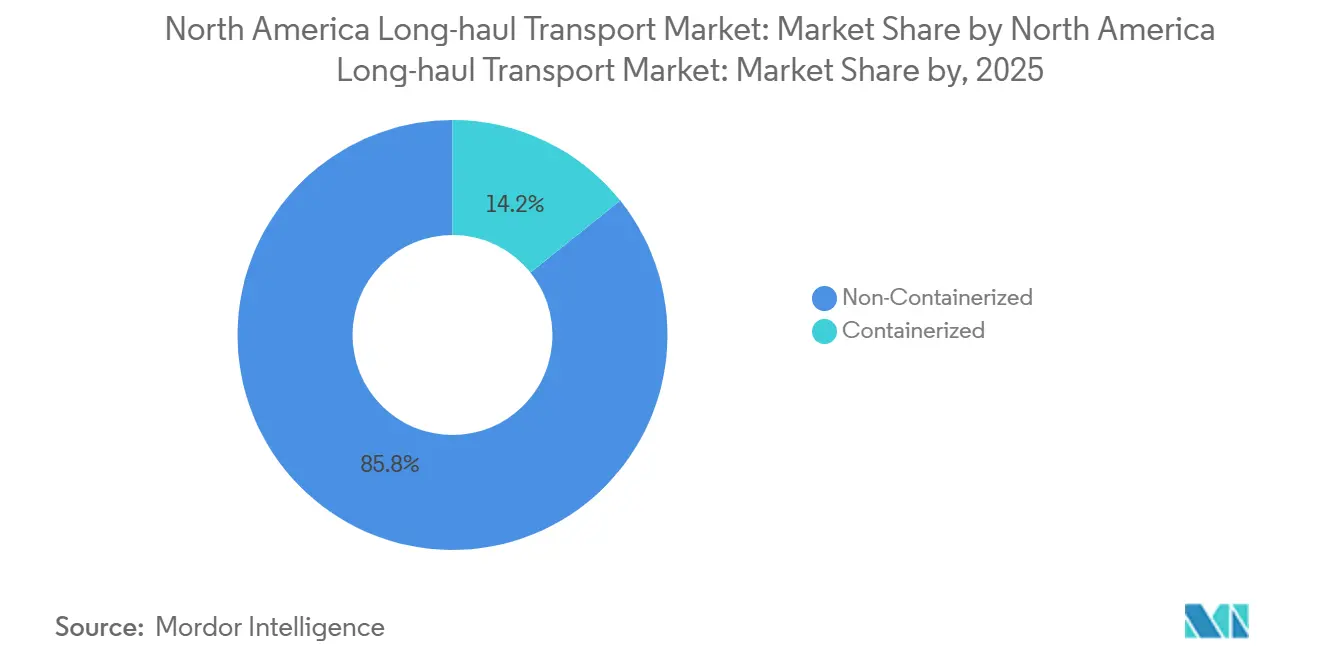

- By containerization type, non-containerized freight represented 85.75% of the 2025 value, yet containerized intermodal lanes are expected to advance at a 3.97% CAGR (2026-2031).

- By goods configuration type, solid goods held 72.43% of revenue share in 2025; fluid goods will pace ahead at a 4.21% CAGR (2026-2031) on refinery expansions and renewable-fuel mandates.

- By temperature control type, non-temperature-controlled comprised 94.70% of revenue in 2025, whereas temperature-controlled shipments will increase at a 4.25% CAGR (2026-2031), fueled by biologics distribution.

- By country, the United States maintained an 85.22% share of the North America long-haul transport market in 2025; Mexico is set to rise the fastest, posting a 5.41% CAGR (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Long-haul Transport Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce parcel volume surge | +0.6% | United States, with spillover to Canada and urban Mexico | Short term (≤ 2 years) |

| Manufacturing reshoring and near-shoring | +0.5% | United States and Mexico, concentrated in automotive and electronics corridors | Medium term (2-4 years) |

| Cross-border trade growth under USMCA | +0.4% | United States-Mexico border states, Ontario-Michigan gateway | Medium term (2-4 years) |

| Cold-chain pharma and biologics expansion | +0.3% | United States and Canada, clustered around biotech hubs | Long term (≥ 4 years) |

| Engine and aerodynamics fuel-efficiency gains | +0.2% | North America-wide, accelerated by EPA Phase 3 standards | Long term (≥ 4 years) |

| AI-enabled back-haul and load-matching platforms | +0.3% | United States and Canada, early adoption in high-density freight lanes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-commerce Parcel Volume Surge

United States online retail sales touched USD 1.14 trillion in 2024, driving parcel counts past 21 billion units and forcing carriers to restructure linehaul legs into relay runs that keep drivers closer to home. Integrated express players invested heavily in automated hubs capable of processing 1.2 million pieces per hour, raising service benchmarks for the broader North America long-haul transport market. Truckload fleets responded by embedding AI route-optimization tools that trimmed empty-mile ratios four points to 14% in early 2025. The mix shift toward smaller, more frequent shipments expanded LTL terminal traffic but added handling costs of USD 0.08 to USD 0.12 per pound. E-commerce share of total freight tonnage is projected to stabilize near 20% by 2028 as omnichannel models blend store pickups with home deliveries[1]“Quarterly Retail E-commerce Sales,” U.S. Census Bureau, census.gov .

Manufacturing Reshoring and Near-Shoring

United States manufacturing construction outlays doubled to USD 228 billion in 2024, largely for semiconductor, battery, and pharmaceutical projects that shorten supply chains from 30-day ocean legs to three-day truck hauls. Mexico attracted USD 36 billion in foreign direct investment the same year, with plants in Nuevo León and Guanajuato funneling wire harnesses and battery modules northbound under USMCA content rules. Cross-border truck freight hit a record USD 47.9 billion in March 2025, underscoring resilient lane demand. Reshoring lifts shipment frequency and complexity, rewarding carriers that operate bonded yards and offer bundled drayage, warehousing, and linehaul services. Smaller brokers struggle to match this integrated suite, spurring consolidation in the North America long-haul transport market[2]“Foreign Direct Investment Statistics,” Banco de México, banxico.org.mx.

Cross-Border Trade Growth under USMCA

USMCA governed USD 1.6 trillion in trilateral trade by 2024 and lifted automotive content rules to 75%, encouraging component sourcing within the bloc. Daily truck crossings at Laredo averaged 14,200 in 2024, a 9% year-over-year jump, while Canada–United States lanes carried USD 36.8 billion in March 2025. Labor-value provisions tightened wage differentials, anchoring freight inside the North America long-haul transport market lanes for another decade. Carriers with authority in all three nations leverage seamless documentation processes to capture higher-margin, door-to-door business. Investments in bilingual customer support and customs-brokerage partnerships are emerging differentiators.

Cold-Chain Pharma and Biologics Expansion

The Food and Drug Administration approved 14 biologics in 2024 that mandate an unbroken 2°C to 8°C chain, elevating the premium segment of the North America long-haul transport market. Logistics providers spent USD 1.8 billion retrofitting reefer trailers with IoT sensors broadcasting data every 15 minutes, safeguarding compliance and curbing recall risk. Each biologic launch requires 50 to 100 reefer loads per month during ramp-up, a volume that tightens specialized capacity and commands spot rates 20% higher than dry van equivalents. Cold-chain demand extends to Mexican produce exports, which advanced 8% in 2024 and depend on equipment meeting both USDA and FDA standards. Carriers holding ISO 9001 certifications and validated lanes lock in premium contracts but shoulder higher maintenance costs because reefer units consume 0.5 to 0.8 gallons of diesel per hour when idling.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute driver shortage and wage inflation | -0.4% | United States and Canada, most severe in long-haul over-the-road segments | Short term (≤ 2 years) |

| Volatile diesel prices | -0.3% | North America-wide, with greater impact on independent owner-operators | Short term (≤ 2 years) |

| Escalating bridge and highway tolls | -0.2% | Concentrated in Northeast U.S. and Ontario toll corridors | Medium term (2-4 years) |

| ESG-driven early fleet-electrification CAPEX | -0.2% | United States and Canada, led by large fleets with sustainability mandates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acute Driver Shortage and Wage Inflation

Retirements accelerated a shortfall that reached 60,000 to 80,000 drivers in 2025, keeping turnover above 90% at large truckload fleets and pushing median pay to USD 62,000. Federal clearinghouse disqualifications removed capacity equal to 2.5% of the commercial-license pool by year-end 2024. Recruiting costs soared to as high as USD 12,000 per new hire, which squeezed smaller carriers’ margins. Autonomous truck trials logged 2.5 million commercial miles in 2024 yet await rulemaking on liability frameworks before scaling beyond pilots. As the labor gap persists, contract rates remain sticky, underpinning the North America long-haul transport market even in periods of soft freight demand[3]“Driver Shortage Report 2025,” American Trucking Associations, trucking.org .

Volatile Diesel Prices

Diesel averaged USD 3.52 per gallon in 2024, swinging USD 0.65 between monthly peaks and troughs and adding USD 6,000 to USD 8,000 per tractor annually. Fuel constitutes roughly one-quarter of operating costs, so rapid price climbs erode margins when surcharges lag. Large carriers hedged exposure through bulk contracts that shaved up to 8% off retail pump levels, while 8,200 independent owner-operators exited in 2024 amid price spikes. The emergence of renewable diesel and biodiesel blends, which captured 4.2% of consumption in 2024, layered additional volatility owing to feedstock swings. Persistent variability keeps fleet modernization toward aerodynamic equipment a strategic priority[4]“Diesel Fuel Update,” U.S. Energy Information Administration, eia.gov.

Segment Analysis

By End User Industry: Manufacturing Volume Anchors, Wholesale Trade Accelerates

Manufacturing generated 32.30% of the North America long-haul transport market share in 2025, reflecting consistent automotive and machinery flows into integrated assembly corridors. Wholesale and Retail Trade leads growth at a 4.41% CAGR (2026-2031) as retailers redistribute inventory across regional fulfillment centers for faster final-mile execution. Agriculture continues to rely on bulk grain moves from Midwest elevators to Gulf export terminals, while construction traffic rose 6.8% on federally funded infrastructure work. Oil and Gas, Mining, and Quarrying softened 2.1% due to flat energy output and subdued natural-gas pricing, but fluid-grade tanker carriers partially offset weakness through chemical shipments tied to semiconductor fabrication. Other diversified verticals, including health care and consumer electronics, aligned with broader GDP expansions.

Reshoring has steadily increased intermediate-goods flows, prompting manufacturers to contract more frequent LTL runs that reduce in-process inventory. Safety audits under the Compliance, Safety, Accountability (CSA) program sharpen carrier selection criteria, elevating well-scored fleets above price-only competitors. E-commerce retail imports continue to reinforce the wholesale segment’s momentum, especially on west-to-east, port-to-inland corridors. As fiscal support cools post-2026, construction freight is likely to normalize, yet the diversified base built by the wholesale channel keeps the North America long-haul transport market insulated from sector-specific shocks.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Destination: Domestic Dominates, International Gains on Nearshoring

Domestic lanes comprised 62.51% of 2025 revenue, driven by dense manufacturing clusters and large consumption centers located within a 500-mile radius. International traffic is forecast to expand at a 4.47% CAGR (2026-2031) as USMCA compliance embeds more north-south component shipments. March 2025 cross-border freight tallied USD 47.9 billion, underlining sustained Mexico–United States flows that shorten lead times and cut inventory costs. Canadian traffic of USD 36.8 billion in the same month emphasized diversified bidirectional volumes of lumber, auto parts, and energy products.

Bonded warehousing near Laredo, El Paso, and Detroit allows integrated solutions that command premiums over plain linehaul. Currency-exchange exposure introduces complexity but offers margin plays for carriers with automated invoicing in multiple denominations. Domestic freight faces higher exposure to driver turnover, while customs bottlenecks remain the prime risk on international lanes. Harmonized electronic-logging-device standards across Mexico and Canada reduce border dwell times and improve asset turns, strengthening the North America long-haul transport market outlook for cross-border specialists.

By Truckload Specification: FTL Efficiency Meets LTL Density Economics

FTL controlled 79.88% of revenue in 2025, catering to shippers that fill trailers with homogeneous freight requiring direct point-to-point service. LTL advances at a 4.30% CAGR (2026-2031), lifted by omnichannel inventory strategies that send smaller batches more frequently. Hub-and-spoke networks deliver load factors north of 95% and generate per-pound savings of up to 40% over FTL spot lanes. Yet FTL maintains lower cargo-damage claims and simpler pricing structures, keeping it the default for high-value or fragile shipments.

Digital load-matching applications reduced empty-mile ratios for FTL fleets to 14% by early 2025, closing part of the utilization gap with LTL. Hybrid services, such as dedicated truckload legs feeding white-glove final-mile teams, illustrate the ongoing convergence. LTL operators invest in automated dimensioning technology to avoid misclassification disputes, an area where early adopters gain an accuracy edge. Both models will coexist, yet the North America long-haul transport market rewards carriers agile enough to toggle between density-driven LTL and high-velocity FTL based on daily tender patterns.

By Containerization: Bulk Dominates, Intermodal Climbs on Rail Partnerships

Non-containerized freight represented 85.75% of revenue in 2025, underscoring the prevalence of bulk commodities and out-of-gauge equipment. Containerized intermodal traffic is projected to grow at a CAGR (2026-2031) of 3.97% as Class I railroads expand double-stack corridors and stabilize port dwell times. J.B. Hunt Intermodal volumes rose 8% year on year in early 2025 under rail-capacity guarantees, confirming demand for truck-to-rail modal shifts on hauls above 750 miles.

Chassis shortages and terminal congestion still constrain full adoption, but new inland ports in Chicago, Memphis, and Kansas City can now handle 12 million lifts annually, more than double 2021 capacity. Adoption of 53-foot domestic boxes improves volumetric efficiency on low-density freight such as furniture, nudging more traffic into intermodal networks. Flatbed operators continue to command premiums on oversized machinery, yet high insurance costs and specialized equipment requirements cap broader segment expansion. These countervailing forces keep the North America long-haul transport market balanced between high-volume bulk lanes and emerging intermodal corridors.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Goods Configuration: Solid Goods Lead, Fluid Gains with Energy Transition

Solid goods claimed 72.43% of overall tonnage in 2025, anchored by automotive parts, consumer electronics, and packaged foods. Fluid goods are set to climb at a 4.21% CAGR (2026-2031) as Gulf Coast refinery expansions and renewable diesel mandates raise tanker demand. Stainless-steel trailers with vapor-recovery units meet purity standards for semiconductor chemicals, unlocking higher-margin loads for tanker fleets.

Regulatory liability tied to spills keeps insurance premiums elevated, and specialized trailers costing USD 40,000 to USD 60,000 more than dry vans limit fleet flexibility. Solid-goods carriers contend with cargo-theft risks that require geofencing and tamper-evident seals, adding USD 200 to USD 400 per shipment. Fluid-goods haulers carry less theft exposure but face environmental penalties exceeding USD 1 million for contamination incidents. The two equipment pools complement each other, allowing diversified carriers to buffer cyclical swings in either sub-market of the North America long-haul transport market.

By Temperature Control: Ambient Prevails, Cold Chain Expands on Biologics

Non-temperature-controlled moves represented 94.70% of 2025 activity, reflecting the dominance of dry freight. Temperature-controlled freight will grow at a 4.25% CAGR (2026-2031) as biologics, specialty foods, and fresh produce require ever-tighter thermal bands. The North America long-haul transport market size for cold-chain lanes is therefore expected to expand steadily, besides FDA approvals that now average double-digit counts annually.

Reefer trailers priced USD 25,000 to USD 35,000 above dry vans add 15%-20% to operating costs, yet validated capacity can command rate premiums of similar magnitude. IoT sensor adoption reduces spoilage claims and demonstrates compliance, a prerequisite for high-value pharmaceuticals. Dry-van operators benefit from wider equipment redeployability, but oversupply of ambient trailers compresses yields whenever freight softens. Temperature-control diversification thus acts as a hedge for integrated carriers within the broader North America long-haul transport market.

Geography Analysis

The United States generated 85.22% of North America long-haul transport market revenue in 2025, fueled by dense consumer markets, four million miles of paved roads, and investments of USD 110 billion earmarked for freight infrastructure upgrades. E-commerce parcel volumes soared 12% year on year in 2025, accelerating hub reconfigurations for next-day commitments. Driver disqualifications removed 135,000 commercial licenses in four years, further tightening capacity.

Mexico is projected to advance at a 5.41% CAGR between 2026-2031 on the back of USD 36 billion of foreign capital inflows and MXN 87 billion (USD 4.25 billion) in highway spending that shaved transit times between Nuevo León and border gateways by 12%. Manufacturing construction reached MXN 412 billion (USD 20.14 billion) in 2024, anchoring sustained outbound truck traffic northward. Electronically enforced hours-of-service rules harmonized with United States standards in 2024, cutting border dwell to 55 minutes by 2025.

Canada rounds out the regional picture with USD 36.8 billion in March 2025 truck freight, much of it tied to auto parts, lumber, and refined products. Congestion in the Greater Toronto and Vancouver corridors lengthens transit times by up to 30% during peaks, encouraging off-peak programs and urban consolidation centers. Harmonized hours-of-service rules adopted in 2024 streamline cross-border operations and reduce administrative overhead. In aggregate, these dynamics sustain diversified lane growth and reinforce the resilience of the North America long-haul transport market.

Competitive Landscape

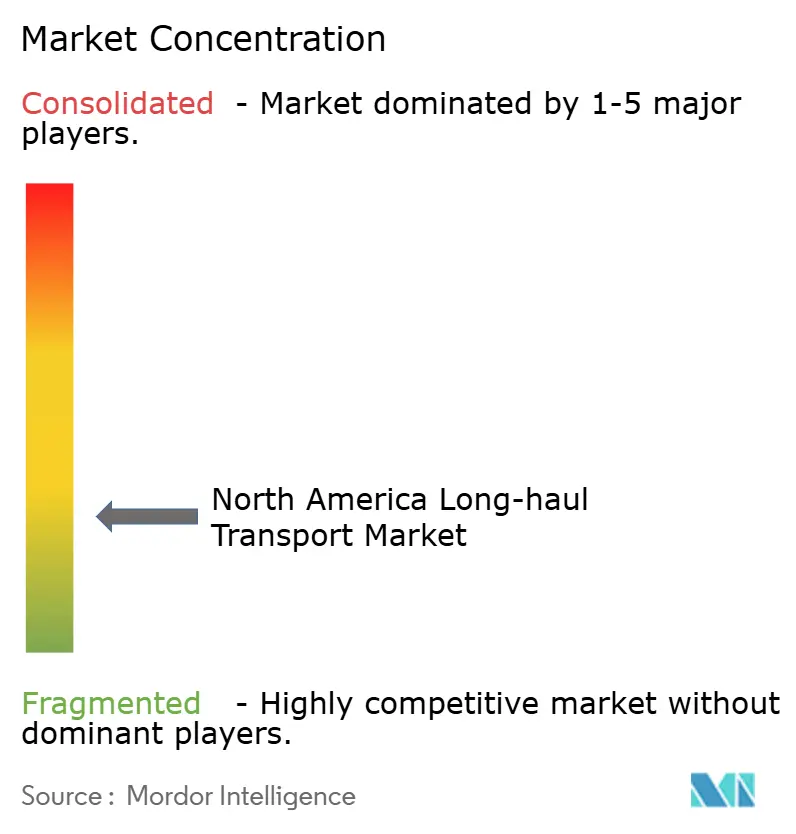

Roughly 35%-40% of industry revenue is held by the 10 largest carriers, indicating moderate concentration. Knight-Swift’s USD 808 million takeover of United States Xpress in June 2024 consolidated 18,000 tractors and 44,000 trailers, boosting its purchasing leverage on fuel and maintenance. XPO’s spin-off of RXO sharpened its LTL focus, while C.H. Robinson embedded generative AI into its Navisphere platform in January 2025, cutting booking times to five minutes.

Temperature-controlled pharmaceutical logistics represents a lucrative niche, yet compliance hurdles and high entry capital insulate incumbents. Autonomous-truck developers Aurora Innovation and Kodiak Robotics logged 2.5 million on-road miles in 2024 but still await a cohesive liability framework before commercial scaling. Meanwhile, retailers such as Walmart and Amazon expand private fleets to hedge against future spot-rate swings.

Horizontal consolidation among mid-sized fleets accelerates as insurance and fuel procurement rates increasingly reward scale. Digital brokerage margins shrank from 16% in 2023 to 13% in early 2025, but higher visibility and faster tender acceptance added throughput capacity. The North America long-haul transport market therefore balances legacy assets with agile technology entrants, while environmental regulation intensifies the capital barrier for newcomers.

North America Long-haul Transport Industry Leaders

FedEx

XPO, Inc.

United Parcel Service of America, Inc. (UPS)

Schneider National, Inc.

Knight-Swift Transportation Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: C.H. Robinson integrated generative AI into Navisphere, reducing load-booking time to five minutes and enabling brokers to handle 30% more shipments daily.

- September 2024: FedEx consolidated 29 ground and express facilities under its DRIVE program to capture USD 4 billion in annual savings.

- August 2024: Old Dominion added 12 service centers, lifting its network to 255 facilities and linehaul capacity by 8%.

- May 2024: Werner Enterprises purchased a regional LTL carrier for USD 185 million, gaining 22 service centers and 850 tractors.

North America Long-haul Transport Market Report Scope

Long-haul trucking (sometimes called 'over-the-road' trucking) involves long-distance cargo movements by truck, usually using tractor-trailer combinations. Long-haul drivers are often away from home for days or weeks at a time.

The North American long-haul transport market is segmented by destination (domestic and cross-border), country (United States, Canada, and Mexico), end user (manufacturing and automotive, oil and gas, mining and quarrying, agriculture, fishing and forestry, construction, distributive trade (wholesale and retail trade), pharmaceutical and healthcare, and other end users, including telecommunications.

The report offers the market size and forecasts for the North American long-haul transport market in value (USD billion) for all the above segments. The report also covers the impact of Covid-19 on the market.

End User Industry

| Agriculture, Fishing, and Forestry |

| Construction |

| Manufacturing |

| Oil and Gas, Mining and Quarrying |

| Wholesale and Retail Trade |

| Others |

Destination

| Domestic |

| International |

Truckload Specification

| Full-Truck-Load (FTL) |

| Less than-Truck-Load (LTL) |

Containerization

| Containerized |

| Non-Containerized |

Goods Configuration

| Fluid Goods |

| Solid Goods |

Temperature Control

| Non-Temperature Controlled |

| Temperature Controlled |

Country

| United States |

| Canada |

| Mexico |

| Rest of North America |

| End User Industry | Agriculture, Fishing, and Forestry |

| Construction | |

| Manufacturing | |

| Oil and Gas, Mining and Quarrying | |

| Wholesale and Retail Trade | |

| Others | |

| Destination | Domestic |

| International | |

| Truckload Specification | Full-Truck-Load (FTL) |

| Less than-Truck-Load (LTL) | |

| Containerization | Containerized |

| Non-Containerized | |

| Goods Configuration | Fluid Goods |

| Solid Goods | |

| Temperature Control | Non-Temperature Controlled |

| Temperature Controlled | |

| Country | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the North America long-haul transport market?

The market is valued at USD 499.53 billion in 2026 and is projected to reach USD 604.47 billion by 2031.

Which end-user segment is growing fastest?

Wholesale and Retail Trade is advancing at a 4.41% CAGR (2026-2031), outpacing all other end-user industries.

How large is the opportunity for temperature-controlled freight?

Temperature-controlled lanes will post a 4.25% CAGR between 2026-2031 as biologics and fresh-produce volumes rise.

Why is Mexico the fastest-growing geography?

Manufacturing nearshoring, USD 36 billion in foreign investment, and upgraded highways push Mexican freight at a 5.41% CAGR (2026-2031).

What impact does the driver shortage have on carrier costs?

Median pay rose 14% to USD 62,000 in 2024 and recruitment expenses can reach USD 12,000 per new driver, lifting operating ratios.

How are digital platforms changing brokerage margins?

AI-enabled load-matching cut booking times to five minutes and lowered broker margins from 16% in 2023 to 13% in 2025.