Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

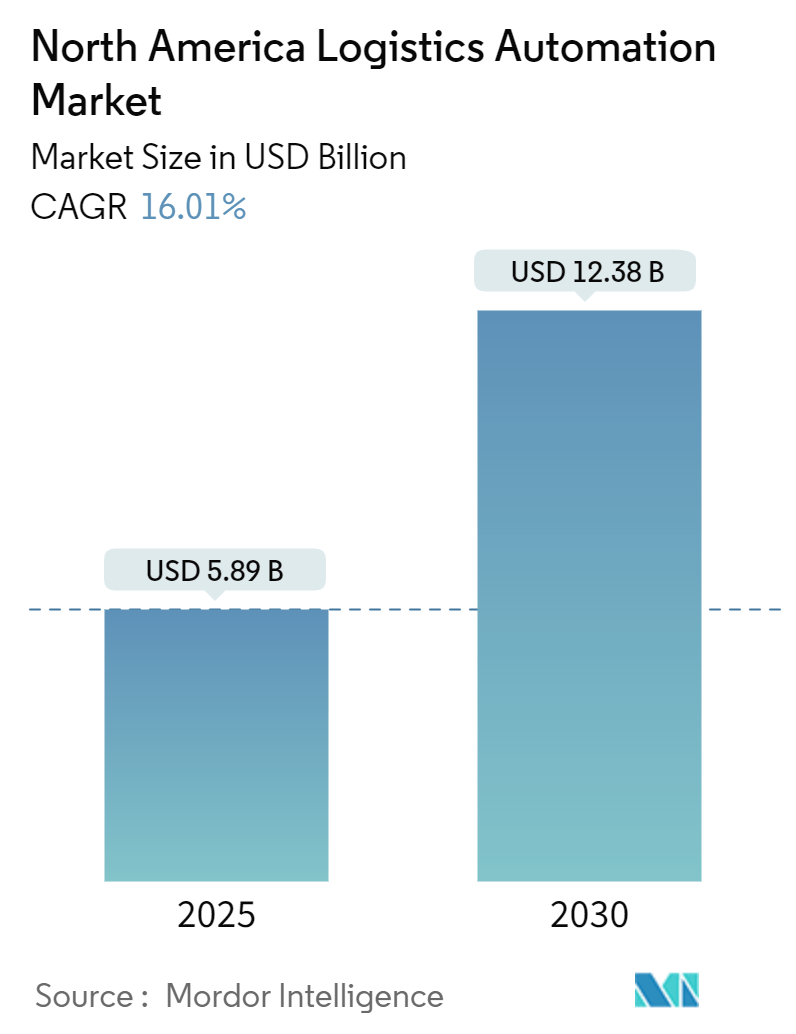

| Market Size (2025) | USD 5.89 Billion |

| Market Size (2030) | USD 12.38 Billion |

| Growth Rate (2025 - 2030) | 16.01% CAGR |

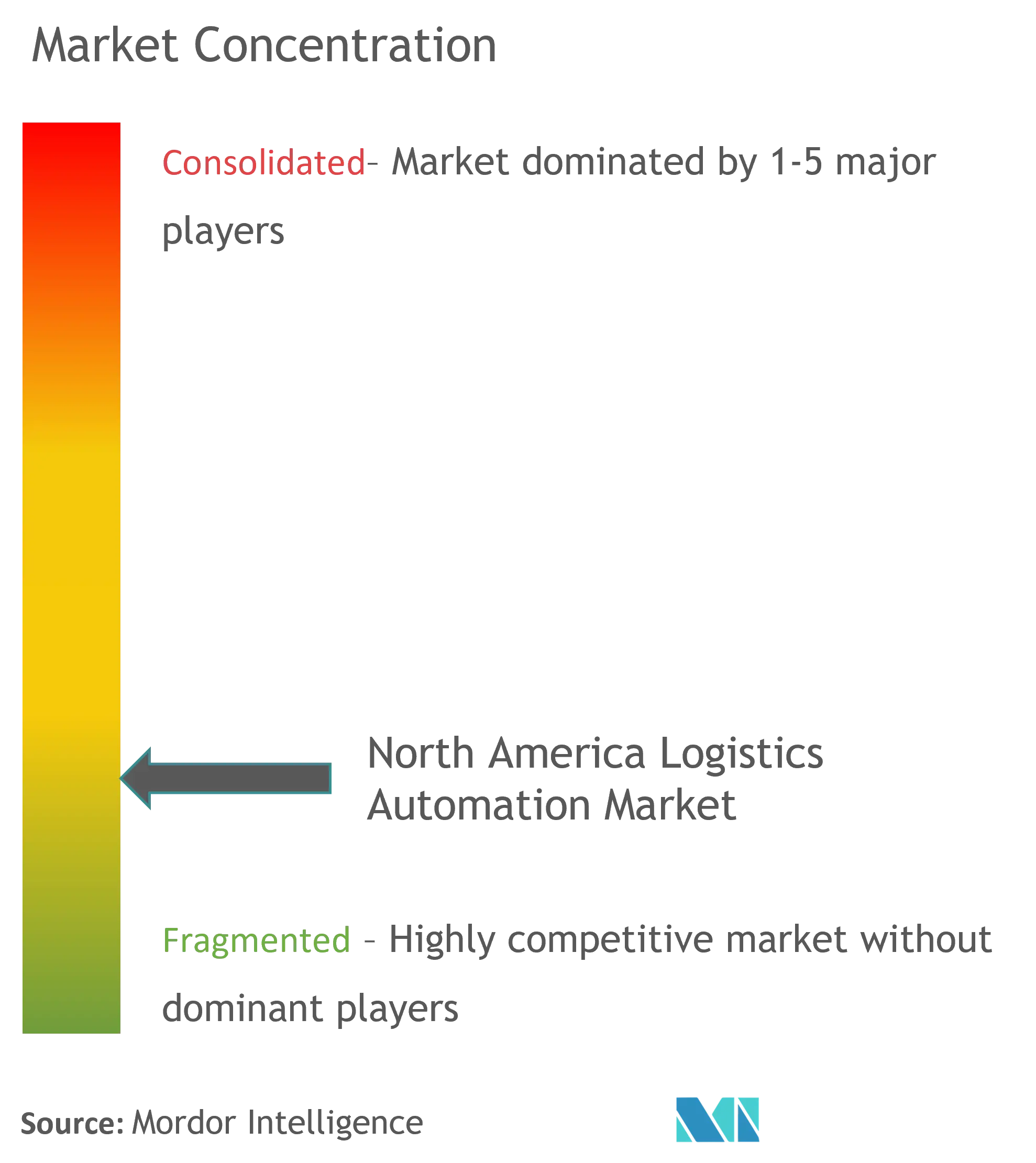

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Logistics Automation Market Analysis by Mordor Intelligence

The North America Logistics Automation Market size is estimated at USD 5.89 billion in 2025, and is expected to reach USD 12.38 billion by 2030, at a CAGR of 16.01% during the forecast period (2025-2030).

The North American logistics automation landscape is undergoing a significant transformation driven by technological advancements and changing industry dynamics. The integration of artificial intelligence, machine learning, and robotics has revolutionized traditional warehouse operations, enabling more efficient and accurate order fulfillment processes. According to industry research, automated storage and retrieval solutions can reduce warehouse footprints by up to 85% while simultaneously increasing operational productivity. This shift towards smart warehousing has become particularly crucial as businesses seek to optimize their operations and maintain competitiveness in an increasingly digital marketplace.

The adoption of advanced identification and tracking technologies has emerged as a cornerstone of modern logistics automation operations. Recent studies indicate that companies implementing Electronic Product Code (EPC)-enabled radio frequency identification (RFID) systems have achieved remarkable improvements in inventory management, with order accuracy rates reaching 99.9%. This technological integration extends beyond basic tracking, encompassing sophisticated warehouse execution systems, automated storage and retrieval systems (AS/RS), and intelligent conveyor systems that work in harmony to streamline operations and reduce human error.

The industry is witnessing a notable shift towards the implementation of autonomous mobile robots (AMRs) and automated guided vehicles (AGVs) in warehouse operations. These technologies are being deployed alongside advanced warehouse management systems (WMS) to create fully integrated warehouse automation solutions. A significant finding from logistics industry analysis reveals that approximately 12% of companies become unprofitable after accounting for distribution costs, highlighting the critical importance of automation in optimizing operational efficiency and maintaining competitive advantages in the market.

The market is experiencing rapid advancement in piece-picking technologies and sortation systems, driven by the need for greater precision and speed in order fulfillment. Major logistics providers are increasingly investing in robotic piece-picking solutions that combine artificial intelligence with advanced vision systems for improved accuracy. This technological evolution is particularly evident in the development of smart conveyor systems and automated palletizing solutions, which are being enhanced with machine learning capabilities to adapt to varying package sizes and weights, ultimately leading to more flexible and efficient logistics automation operations.

North America Logistics Automation Market Trends and Insights

Increased E-Commerce Activity

The explosive growth of e-commerce has become a primary catalyst for logistics automation adoption across North America. With e-commerce sales contributing approximately 14.3% to total retail sales, retailers are being compelled to revolutionize their fulfillment operations to meet escalating consumer demands for faster and more accurate deliveries. This transformation is exemplified by major retailers like Amazon, which has expanded its warehouse automation network from just 3 facilities in 2000 to over 177 facilities by 2020, demonstrating the massive scale of automation required to support modern e-commerce operations. The integration of automated solutions has become essential for retailers to maintain competitive advantages in speed, accuracy, and operational efficiency.

The shift in consumer buying behavior has created unprecedented pressure on traditional warehouse operations, driving the need for sophisticated automation solutions that can handle high-volume order processing and complex multi-channel fulfillment requirements. This is evidenced by strategic partnerships like Kroger's collaboration with Ocado to implement advanced warehouse automation technology for handling operations, logistics, and delivery route planning. Such partnerships highlight how retailers are leveraging smart logistics to transform their entire supply chain operations, from warehouse management to last-mile delivery, in response to evolving e-commerce demands.

Understand The Key Trends Shaping This Market

Download PDF

Growing Distribution Centers, Labor Shortages, and Rising Labor Rates

The warehousing and storage sector faces significant challenges with labor availability and rising costs, as evidenced by the substantial workforce of over 732,660 employees across various roles, including material movers, stock clerks, and equipment operators. Despite this large workforce, the industry continues to grapple with persistent labor shortages and increasing wage pressures, compelling organizations to turn to logistics technology solutions. The situation is particularly acute in distribution centers, where the combination of labor-intensive operations and the need for skilled workers has created a perfect storm driving automation adoption.

The expansion of distribution networks, coupled with rising real estate costs, has forced companies to optimize their existing spaces through automation rather than expanding physically. This trend is particularly notable as approximately 80% of warehouses in North America are still manually operated, representing a massive opportunity for warehouse automation implementation. Companies are increasingly investing in automated solutions for smaller spaces, as evidenced by the industry shift toward micro-fulfillment centers and automated storage and retrieval systems (AS/RS). These solutions enable organizations to maximize productivity in smaller footprints while addressing both labor challenges and space constraints. Major retailers and logistics providers are leading this transformation, implementing various automation technologies from mobile robots to sophisticated sortation systems, demonstrating the industry's commitment to addressing these fundamental challenges through technological innovation, including the use of automated material handling systems in automated distribution centers.

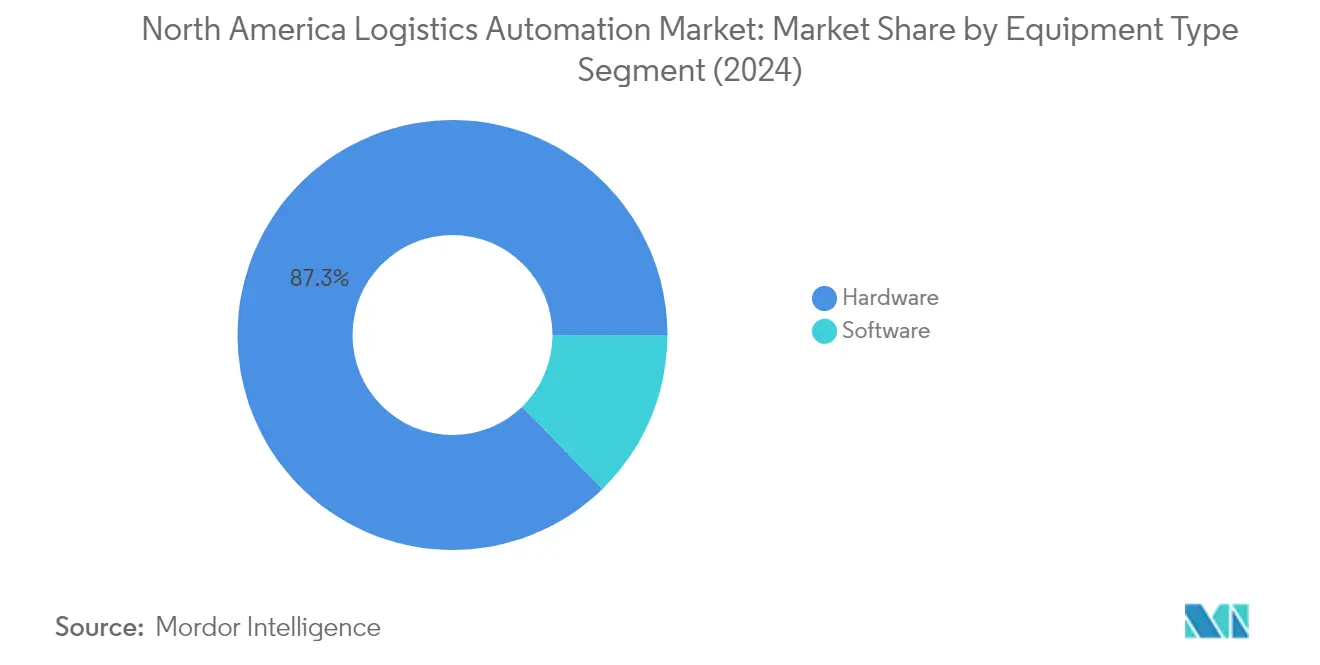

Segment Analysis: By Equipment Type

Hardware Segment in North America Logistics Automation Market

The hardware segment dominates the North America logistics automation market, commanding approximately 87% market share in 2024. This substantial market presence is driven by the increasing adoption of automated solutions like mobile robots, automated storage and retrieval systems (AS/RS), conveyors, palletizers/de-palletizers, sortation systems, and piece-picking robots across various industries. The segment's dominance is particularly evident in e-commerce fulfillment centers, retail distribution facilities, and manufacturing plants where automation hardware plays a crucial role in improving operational efficiency and reducing labor dependencies. Major retailers and logistics providers across the United States and Canada are increasingly investing in hardware automation solutions to handle growing order volumes and address labor shortage challenges.

Piece-Picking Robots Segment in North America Logistics Automation Market

The piece-picking robots segment is emerging as the fastest-growing category within the hardware segment, projected to grow at approximately 62% during 2024-2029. This exceptional growth is driven by the increasing need for precise and efficient item handling in e-commerce fulfillment operations. The segment's rapid expansion is fueled by advancements in robotic technologies, particularly in areas of artificial intelligence, machine learning, and computer vision, enabling robots to handle diverse product sizes and shapes with greater accuracy. The adoption is further accelerated by the growing need for flexible automation solutions that can seamlessly integrate with existing warehouse automation systems while reducing dependency on manual labor for picking operations.

Remaining Segments in Equipment Type

The software segment, comprising Warehouse Management Systems (WMS), Warehouse Execution Systems (WES), and Warehouse Control Systems (WCS), plays a vital complementary role in the logistics automation ecosystem. These software solutions are essential for orchestrating and optimizing the performance of hardware components, enabling real-time inventory tracking, order processing, and resource allocation. The integration capabilities of these software systems with various hardware components make them indispensable for achieving end-to-end automation in logistics operations, while their cloud-based deployment options offer scalability and flexibility for businesses of all sizes.

Segment Analysis: By Industry

General Merchandise Segment in North America Logistics Automation Market

The General Merchandise segment continues to dominate the North America Logistics Automation market, commanding approximately 31% of the total market share in 2024. This significant market position is driven by major retailers and e-commerce giants in North America that are establishing automated fulfillment distribution centers to meet growing demand from their channels. The implementation of micro-fulfillment centers has shown to increase productivity by up to ten times through improved speed, accuracy, and efficiency, while providing real-time automated inventory management information that significantly reduces product substitutions. The segment's growth is further supported by the increasing adoption of automated picking system robots working alongside staff in warehouses, with companies like Walmart implementing autonomous carts for automated item picking and storage at room temperatures.

Pharmaceutical Segment in North America Logistics Automation Market

The Pharmaceutical segment is emerging as the fastest-growing segment in the North America Logistics Automation market, with a projected growth rate of approximately 19% during 2024-2029. This remarkable growth is driven by the increasing need for maintaining high-quality products and safety standards in the healthcare industry, coupled with the growing complexity of pharmaceutical logistics operations. The segment's expansion is further fueled by the dynamic and agile nature of pharmaceutical production, where constant movement of semi-finished goods from warehouse to production lines and finished goods from production lines to warehouse necessitates advanced automated material handling solutions. The adoption of automated guided vehicle systems in pharmaceutical facilities for transporting materials between production and warehouse areas is becoming increasingly common, optimizing internal material flow and workflows while freeing staff resources for higher-value activities.

Remaining Segments in Industry Segmentation

The other significant segments in the North America Logistics Automation market include Food and Beverages, Manufacturing, Post & Parcel, Groceries, and Apparel, each serving distinct industry needs. The Food and Beverages segment is driven by stringent food safety regulations and the need for precise storage operations, while the Manufacturing segment benefits from the increasing adoption of automation in automotive and electronics industries. The Post & Parcel segment focuses on enhancing delivery efficiency and accuracy, while the Groceries segment is transforming through micro-fulfillment centers and automated storage solutions. The Apparel segment is leveraging automation to handle the complexities of multi-channel sales and returns processing, with particular emphasis on automated sorting and storage systems.

North America Logistics Automation Market Geography Segment Analysis

North America Logistics Automation Market in the United States

The United States dominates the North American logistics automation landscape, commanding approximately 88% of the regional market share. The country's leadership position is driven by its robust e-commerce sector, extensive warehouse networks, and widespread adoption of advanced logistics technology. The presence of major e-commerce giants and retailers has catalyzed the implementation of sophisticated automated distribution center solutions across distribution centers. The country's logistics infrastructure continues to evolve with significant investments in automated storage and retrieval systems, mobile robots, and intelligent software solutions. The strong economy, notable port traffic, increased e-commerce activity, and key manufacturing indices have collectively contributed to substantial growth in industrial automation. Various sectors, including retail, automotive, food and beverage, and pharmaceutical industries, represent the largest sources of demand for automated logistics solutions in the country. The trend toward automating production in both domestic and global markets remains the main driving force behind robot installations in the United States.

North America Logistics Automation Market in Canada

Canada represents a rapidly expanding market for logistics automation solutions, projected to grow at approximately 19% annually from 2024 to 2029. The country's manufacturing sector, accounting for approximately CAD 174 billion of its GDP and representing more than 10% of the total GDP, serves as a significant driver for automation adoption. The Canadian warehouse portfolio, predominantly comprised of e-commerce operations, is estimated to constitute more than 50% of the warehouse business in the country. The nation's commitment to technological advancement is evident through various government initiatives and investments in automated solutions. Rising labor costs, waning employee productivity, and the need for larger distribution centers to accommodate increasing inventory volumes are compelling retailers to embrace warehouse automation. The country's strategic position as a hub for traffic between Asia, Europe, and the Americas further necessitates efficient automated logistics solutions to manage complex supply chain operations.

North America Logistics Automation Market in Other Countries

The North American logistics automation market primarily focuses on the United States and Canada, as these two nations represent the entirety of the region's significant market activity. While other territories such as Mexico are part of the broader North American continent, they are typically analyzed under different market segments or regional classifications. The concentration of market analysis on the United States and Canada reflects their advanced technological infrastructure, mature e-commerce sectors, and sophisticated supply chain networks. These two nations have established themselves as pioneers in adopting and implementing cutting-edge logistics automation solutions, setting benchmarks for other regions globally. Their combined market dynamics and technological advancement continue to shape the evolution of logistics automation across the continent.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

Top Companies in North America Logistics Automation Market

The North American logistics automation market features established players like Honeywell, Daifuku, Swisslog, Dematic, and SSI Schaefer leading the competitive landscape through continuous innovation and strategic expansion. These companies are heavily investing in research and development to enhance their automated storage and retrieval systems, robotics solutions, and warehouse management software capabilities. The market is characterized by strategic partnerships with technology providers to incorporate artificial intelligence, machine learning, and advanced robotics into existing product portfolios. Companies are focusing on developing micro-fulfillment solutions and modular automation systems to address the growing e-commerce demands. Major players are also expanding their manufacturing facilities and service networks across the region while strengthening their integration capabilities through acquisitions of specialized automation technology providers.

Market Consolidation Drives Industry Evolution Pattern

The logistics automation market structure exhibits a mix of global conglomerates and specialized automation solution providers competing for market share. Global players like Honeywell and Daifuku leverage their extensive resources and cross-industry expertise to offer comprehensive logistics technology solutions, while specialized firms like Swisslog and Kardex focus on developing niche technological capabilities in specific automation segments. The market is witnessing increasing consolidation through strategic acquisitions, as larger players seek to enhance their technological capabilities and expand their solution portfolios.

The competitive dynamics are shaped by the presence of both established material handling equipment manufacturers who have expanded into automation and pure-play automation specialists. Market participants are increasingly focusing on developing end-to-end solutions rather than standalone products, leading to strategic partnerships and acquisitions to fill capability gaps. The industry is seeing a trend toward vertical integration, with companies acquiring software and controls capabilities to offer more comprehensive solutions while maintaining strong relationships with system integrators and distribution partners.

Innovation and Integration Drive Future Success

Success in the logistics automation market increasingly depends on companies' ability to provide integrated solutions that combine hardware, software, and services while maintaining technological leadership through continuous innovation. Market incumbents are focusing on expanding their service and support networks, developing cloud-based solutions, and offering flexible financing options to maintain their competitive positions. Companies are also investing in building industry-specific expertise and developing customized solutions for different end-user segments while strengthening their local presence through partnerships with regional system integrators.

New entrants and challenger companies are finding opportunities by focusing on specific market niches, developing innovative technologies, and offering more flexible and scalable solutions. The market's future competitive landscape will be influenced by the ability to address increasing end-user demands for flexibility, scalability, and quick return on investment. Regulatory requirements related to workplace safety and environmental sustainability are becoming increasingly important factors in product development and market strategy. Companies that can demonstrate clear value propositions in terms of operational efficiency improvements and labor cost reduction while maintaining strong service capabilities will be better positioned for success.

North America Logistics Automation Industry Leaders

-

SSI SCHÄEFER AG

-

Daifuku Co. Limited

-

Kardex Group

-

Honeywell Intelligrated

-

Beumer Group GMBH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2021: Kardex Group signed up for a global partnership agreement with Autostore AS which is a high-performance and space-saving storage and picking solution for the rapid processing of small parts orders with the help of autonomous robots. As a global partner of AutoStore and Kardex will in the future sell, project-manage, and install AutoStore solutions worldwide.

- February 2021: Urban Outfitters, Inc., one of the leading lifestyle products and services companies, which operates a portfolio of global consumer brands comprised of Anthropologie, BHLDN, Free People, Terrain, Urban Outfitters, Nuuly, and a Food and Beverage division has partnered with TGW to design and implement an automation solution for their new fulfillment center in Kansas City, in the US. According to the company, TGW's FlashPick system is at the heart of the solution as the product picks orders fully automatically and ensures the next phase of picking is being addressed. These kinds of partnerships help the company to scale its business in the market.

North America Logistics Automation Market Report Scope

Warehouses and distribution centers form the most vital part of the logistics sector. They perform products transit that starts from the process of the production facility, acknowledgment, organizing, and also the tagging for delivering product on the required address.

The Hardware component includes Mobile robots, AS/RS, Conveyor & Sortation Systems, Palletizers, Piece Picking Robots. Whereas, WMS/WCS/WES is also being made part of the study. Further a geographical analysis with the United States and Canada is covered.

By Solution Type

| Hardware | Mobile Robots (Automated Guided Vehicle (AGV) and Autonomous Mobile Robots (AMR)) |

| Automated Storage and Retrieval System (AS/RS) (Unit Load - Fixed and Movable Aisle, Mini Load, Shuttle & Bot Systems and Other Systems - Carousels and Vertical Lift Modules) | |

| Conveyor (Belt, Roller, Pallet and Overhead) | |

| Palletizer/De-palletizer (Conventional - High Level + Low Level, and Robotic) | |

| Sortation System | |

| Software - Warehouse Management Systems (WMS), WES and WCS | |

| Other Solutions | Transportation Management Solutions |

| Others (Piece-picking robots, collaborative robots, warehouse drones, and supporting infrastructure) |

By Industry

| General Merchandise |

| Apparel |

| Food and Beverages |

| Groceries |

| Post & Parcel |

| Manufacturing (Durable and Non-Durable) |

| Other Industries |

By Country

| United States |

| Canada |

| By Solution Type | Hardware | Mobile Robots (Automated Guided Vehicle (AGV) and Autonomous Mobile Robots (AMR)) |

| Automated Storage and Retrieval System (AS/RS) (Unit Load - Fixed and Movable Aisle, Mini Load, Shuttle & Bot Systems and Other Systems - Carousels and Vertical Lift Modules) | ||

| Conveyor (Belt, Roller, Pallet and Overhead) | ||

| Palletizer/De-palletizer (Conventional - High Level + Low Level, and Robotic) | ||

| Sortation System | ||

| Software - Warehouse Management Systems (WMS), WES and WCS | ||

| Other Solutions | Transportation Management Solutions | |

| Others (Piece-picking robots, collaborative robots, warehouse drones, and supporting infrastructure) | ||

| By Industry | General Merchandise | |

| Apparel | ||

| Food and Beverages | ||

| Groceries | ||

| Post & Parcel | ||

| Manufacturing (Durable and Non-Durable) | ||

| Other Industries | ||

| By Country | United States | |

| Canada | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the North America Logistics Automation Market?

The North America Logistics Automation Market size is expected to reach USD 5.89 billion in 2025 and grow at a CAGR of 16.01% to reach USD 12.38 billion by 2030.

What is the current North America Logistics Automation Market size?

In 2025, the North America Logistics Automation Market size is expected to reach USD 5.89 billion.

Who are the key players in North America Logistics Automation Market?

SSI SCHÄEFER AG, Daifuku Co. Limited, Kardex Group, Honeywell Intelligrated and Beumer Group GMBH & Co. KG are the major companies operating in the North America Logistics Automation Market.

What years does this North America Logistics Automation Market cover, and what was the market size in 2024?

In 2024, the North America Logistics Automation Market size was estimated at USD 4.95 billion. The report covers the North America Logistics Automation Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the North America Logistics Automation Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: