Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

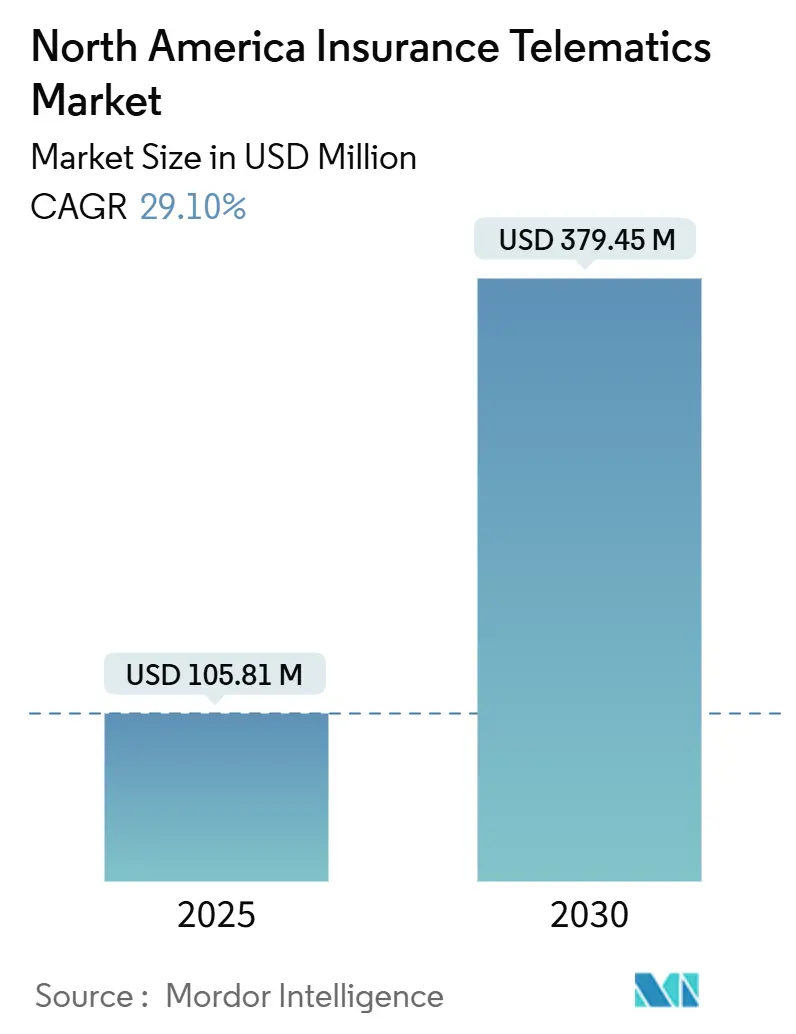

| Market Size (2025) | USD 105.81 Million |

| Market Size (2030) | USD 379.45 Million |

| Growth Rate (2025 - 2030) | 29.10% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Insurance Telematics Market Analysis by Mordor Intelligence

The North America insurance telematics market size reached USD 105.81 million in 2025 and is forecast to climb to USD 379.45 million by 2030, reflecting a compelling 29.1% CAGR over the period. Elevated premium rates, rapid sensor-accuracy gains, maturing OEM data platforms, and widening regulatory clarity are jointly propelling adoption as insurers search for granular risk signals that stabilize loss ratios while preserving customer retention. Smartphone-based programs benefit from a 54.9% 2024 share thanks to universal device ownership and driver-trip classification accuracy that now tops 96.5%. Embedded solutions, although smaller today, are poised for the quickest expansion because automakers such as General Motors have converted connected-car data pipelines into full-stack insurance offerings. Parallel growth drivers include fleet managers’ pursuit of lower liability costs, lender-insurance tie-ups that extend usage-based pricing to sub-prime borrowers and accelerating AI governance that legitimizes algorithmic underwriting across 24 U.S. states.[1]National Association of Insurance Commissioners, “Data Privacy and Insurance,” naic.org

Key Report Takeaways

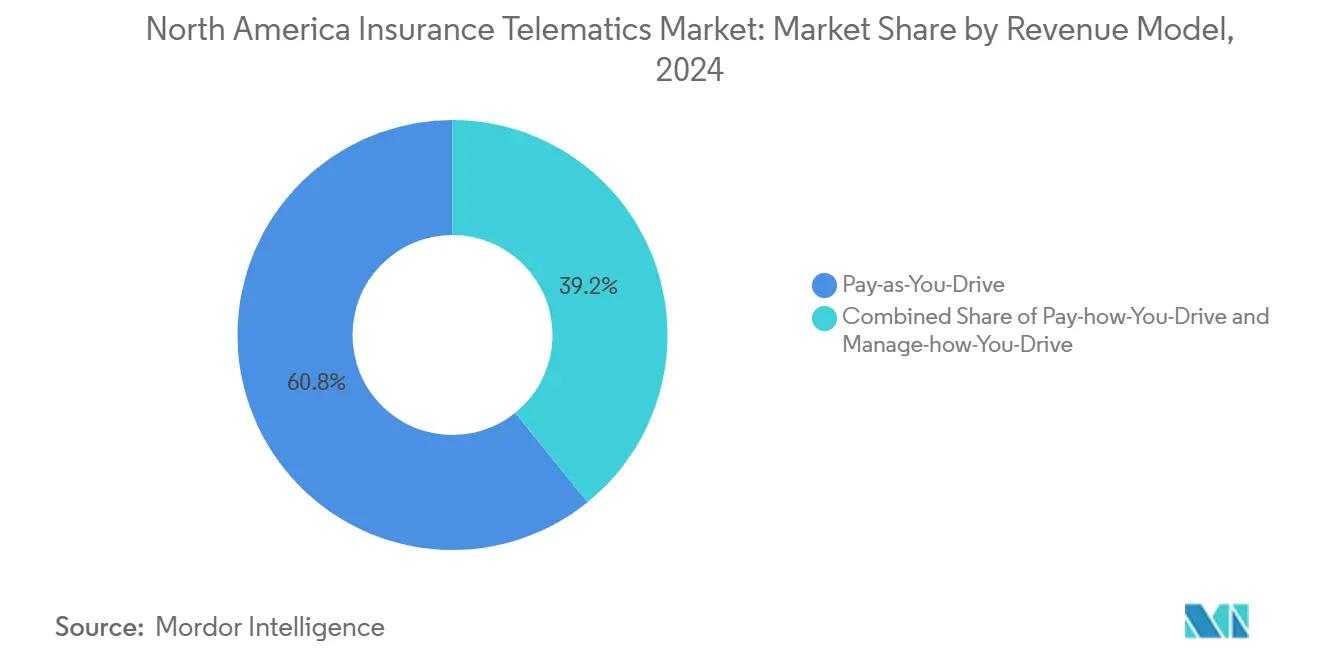

- By revenue model, pay-as-you-drive held 60.8% of North America insurance telematics market share in 2024, while manage-how-you-drive is projected to compound at a 34.82% CAGR through 2030.

- By hardware, smartphone-based systems captured 54.9% revenue in 2024; embedded telematics is forecast to expand at a 33.82% CAGR to 2030.

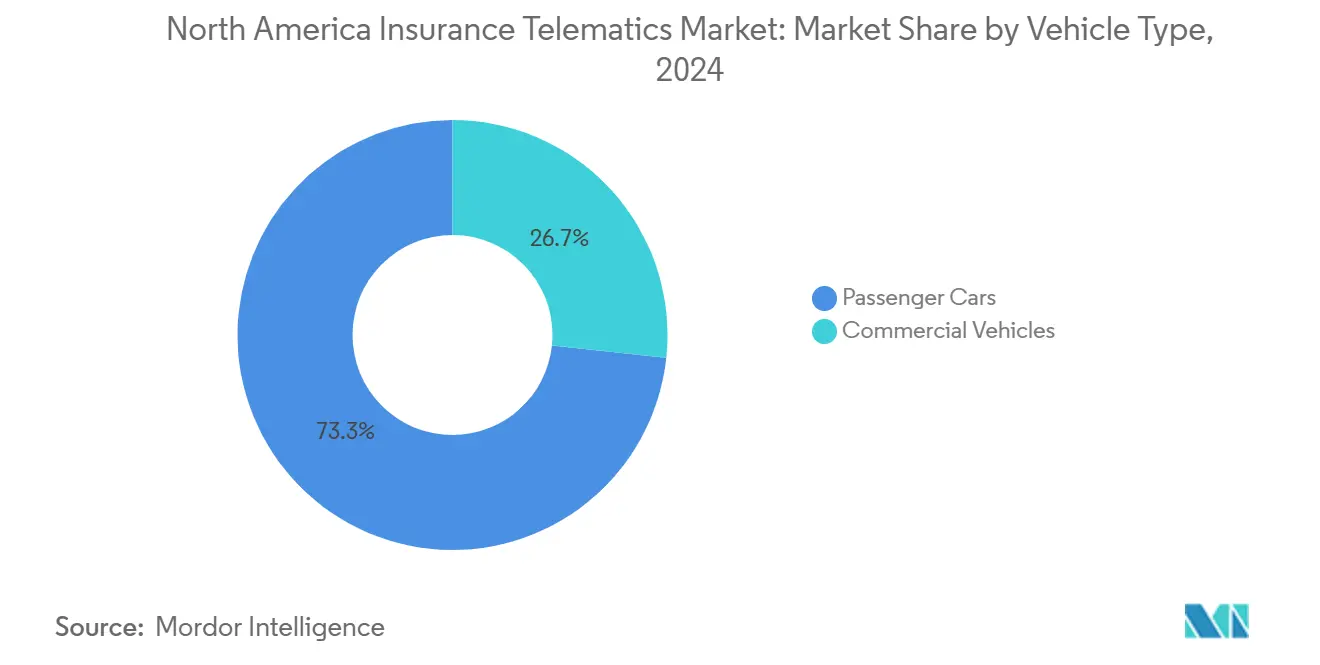

- By vehicle type, passenger cars accounted for 73.33% of the 2024 North America insurance telematics market size, whereas commercial vehicles are advancing at a 34.11% CAGR across the forecast window.

- By end-user, personal lines generated 89.52% of 2024 revenue, but commercial fleets are growing at a 33.54% CAGR through 2030.

- By geography, the United States contributed roughly 85% revenue in 2024; Canada exhibits the faster growth trajectory from a smaller base.

North America Insurance Telematics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price-hardening in Auto Premiums | +8.20% | Global, concentrated in high-cost states like California, Texas, Florida | Short term (≤ 2 years) |

| Smartphone Sensor Accuracy and API Access | +6.80% | North America core, spillover to connected vehicle ecosystems | Medium term (2-4 years) |

| OEM Embedded Telematics Penetration | +7.50% | US and Canada, with early adoption in premium vehicle segments | Long term (≥ 4 years) |

| Auto-Lender Partnerships for Mileage-linked Products | +4.90% | National, with concentration in subprime lending markets | Medium term (2-4 years) |

| Commercial Fleet Insurance Cost Pressures | +5.30% | National, with concentration in high-liability transportation sectors | Short term (≤ 2 years) |

| Advanced Crash Detection and Emergency Response | +3.80% | North America core, expanding to rural coverage areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price-hardening in Auto Premiums

Auto premiums climbed another 22% during 2024 after a 15% first-half surge, prompting insurers to deploy telematics for sharper risk differentiation and customer segmentation.[2]: Insurance Business, “Auto insurance premium increases slowed in 2024 in the U.S.,” insurancebusinessmag.com Usage-based policyholders show 10% lower accident frequency in high-adoption states, improving loss ratios and reinforcing carrier appetite for expanded programs. Carriers such as Nationwide and American Family now advertise mileage plans that deliver savings up to 25% for low-mileage drivers, widening mainstream awareness of telematics incentives. As premium pressure persists, competitive necessity is expected to maintain strong program rollouts across both national and regional insurers.

Smartphone Sensor Accuracy and API Access

Advances in gyroscope and accelerometer fusion algorithms have pushed driver-trip classification accuracy to 96.5%, eliminating a long-standing impediment to smartphone telematics scale. API aggregators such as Smartcar now cover 161 million North American vehicles, letting insurers verify VIN, mileage, and garaging data with no hardware shipping or installation.[3]Smartcar, “Auto Insurance APIs,” smartcar.com Crash-detection SDKs from DriveQuant deliver real-time impact location, g-force, and speed metrics, allowing claims teams to expedite triage and reduce fraud loss dollars. These technical milestones reduce onboarding friction, positioning smartphone-led models as the entry gateway for most new telematics users.

OEM Embedded Telematics Penetration

Automakers have shifted from pure data suppliers to full insurance intermediaries. General Motors re-launched OnStar Insurance as General Motors Insurance in 2024, leveraging in-car modules to reward safe driving across Chevrolet, Buick, GMC, and Cadillac models from 2016 onward. Regulatory scrutiny has intensified, evidenced by the 2025 Federal Trade Commission order barring GM from selling driving data for five years after unauthorized data-sharing revelations affecting 16 million motorists. Similar privacy litigation faces Toyota over alleged Progressive data transfers. Clarifying data-ownership rules is expected to spur OEM-led programs once compliance frameworks mature.

Auto-Lender Partnerships for Mileage-Linked Products

Banks and captive finance arms are embedding telematics into loan origination, blending insurance quotes with credit approvals. American Family’s MilesMyWay requires only bi-annual odometer photos yet grants tiered discounts, illustrating low-touch data capture that resonates with budget-sensitive borrowers. Porsche partnered with Mile Auto to deliver luxury mileage-based premiums that match typically low annual utilization among sports-car drivers. These cross-industry tie-ups unlock alternative distribution channels and expand telematics penetration into demographics underserved by traditional agency networks.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy and Consent Regulations | -3.40% | California, with CCPA influence spreading to federal level | Short term (≤ 2 years) |

| Data Quality and Compatibility Issues in Smartphone UBI | -2.10% | Global, particularly affecting cross-platform implementations | Medium term (2-4 years) |

| Consumer Privacy Concerns and Adoption Resistance | -2.80% | National, with higher resistance in privacy-conscious demographics | Medium term (2-4 years) |

| Technology Standardization Challenges Across Platforms | -1.90% | North America, affecting multi-carrier and cross-border implementations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Consent Regulations

State regulators now treat telematics as sensitive personal data. The California Privacy Protection Agency’s USD 632,500 settlement with Honda required overhauls to consent flows and UX disclosures, setting a high-visibility precedent for nationwide insurers. NAIC’s pending Privacy Protections Model Act #674 and its AI Bulletin adopted by 24 states compel carriers to implement algorithm auditing, vendor oversight, and governance documentation. Compliance lift raises costs, potentially slowing small-carrier adoption until turnkey governance solutions emerge.

Data Quality and Compatibility Issues in Smartphone UBI

Although accuracy rates are climbing, residual misclassification can still surface in multi-driver households, nudging risk scores off target and triggering consumer disputes. Differing iOS and Android battery-optimization protocols sometimes interrupt background data collection, forcing carriers to build device-specific fixes that increase engineering overhead. Lack of uniform data schemas among telematics vendors complicates carrier integrations, adding middleware spend and elongating rollout timelines.

Segment Analysis

By Revenue Model: Behavioral Analytics Drive Premium Differentiation

Pay-as-you-drive commanded 60.8% of 2024 revenue, underpinned by consumers who equate mileage counts with fairness and instantly see savings via low-usage discounts. Nationwide’s SmartMiles illustrates the appeal, delivering transparent per-mile rates without on-board hardware.[4]Nationwide, “Pay-Per-Mile Car Insurance with SmartMiles,” nationwide.com The segment’s large footprint provides stable cash-flow but limited behavioural feedback. In contrast, manage-how-you-drive is forecast to post a 34.82% CAGR, reshaping the North America insurance telematics market through real-time coaching and eco-scoring that pre-empt risky manoeuvres and emissions. Cambridge Mobile Telematics now bundles Fuel Score and Eco Score, proving that multidimensional feedback enriches customer engagement and deepens carrier data pools. As regulatory AI mandates emphasize transparency, carriers are likely to Favor manage-how-you-drive frameworks that actively guide rather than merely rate motorists.

Note: Segment shares of all individual segments available upon report purchase

By Telematics Hardware Type: Embedded Solutions Gain Momentum

Smartphone-based apps retained a 54.9% share in 2024 due to zero-cost entry and rapid feature iteration. Smartcar’s 37-brand compatibility spanning 161 million vehicles underscores ecosystem breadth that shields insurers from OEM lock-in. Nonetheless, embedded units are on a 33.82% CAGR arc because automakers can stream diagnostics, mileage, and driver-behaviour signals with no user action, creating frictionless data acquisition that insurers prize. GM’s carrier pivot exemplifies embedded leverage despite the FTC’s data-sales freeze. Portable add-on devices will persist in retrofit and specialty-vehicle niches but face share erosion as smartphones and embedded modules blanket the mainstream fleet.

By Vehicle Type: Commercial Segment Accelerates

Passenger cars delivered 73.33% of 2024 revenue, reflecting sheer unit volume and entrenched agency distribution. Years of personal UBI experimentation have yielded mature scoring models and gamified dashboards that stimulate steady enrolment. Yet commercial vehicles are on pace for a 34.11% CAGR, transforming the North America insurance telematics market through tighter safety compliance and cost control. UPS reported 15-minute idle reductions per driver and 1.4-million-gallon annual fuel savings after scaled telematics deployment, validating ROI narratives that resonate with fleet CFOs. Dash-cam evidence exonerated Satellites Unlimited drivers in liability disputes, reinforcing insurer confidence in fleet-data integrity.

By End-user: Fleet Applications Expand Rapidly

Personal lines generated 89.52% of 2024 spend as mobile apps and multi-policy discounts simplified sign-up for mainstream households. Heavy marketing by Progressive, Allstate, and State Farm has normalized telematics and diffused privacy concerns through incentive framing. Commercial fleets, however, are advancing at a 33.54% CAGR, as integrated risk dashboards combine maintenance alerts, regulatory reporting, and usage-based premiums. Munich Re’s analytics indicate fleet sharing of telematics data can compress insurance expense ratios by highlighting risky drivers and streamlining claims validation. Structured procurement cycles and professional risk managers ensure telematics adoption is methodically budgeted across multi-year capital plans.

Geography Analysis

The United States accounted for roughly 85% of North America insurance telematics market revenue in 2024, buoyed by high vehicle density, fragmented state oversight, and competitive premium dynamics that favour differentiated pricing strategies. California’s privacy enforcement headlines, including the Honda settlement, sharpen data-consent compliance statewide and signal forthcoming national harmonization. Texas and Florida exhibit faster growth as high loss-cost geographies motivate carriers to accelerate UBI discount programs, while hurricane-exposed fleets seek real-time vehicle visibility for loss mitigation.

Canada delivered the remaining 15% of 2024 revenue yet holds outsized future potential as provincial regulators converge on privacy and rate-filing standards conducive to telematics-based products. Ontario’s dense metro corridors and Alberta’s energy logistics fleets create natural demand pockets. Carriers such as Intact and Desjardins have seeded pilot programs, but wider adoption awaits clearer actuarial evidence that satisfies prudential regulators. Harmonization under the federal Personal Information Protection and Electronic Documents Act provides a common data-protection bedrock that multinational insurers can leverage for cross-border platforms.

Forecast comparisons illustrate acceleration in both territories: U.S. historical CAGR of ~18% over 2019-2024 is projected to lift to 29.1% during 2025-2030 as smartphone accuracy and OEM participation unlock new cohorts. Canada is on a similar growth slope from a smaller base, amplified by expected provincial approval of algorithmic underwriting models that mirror NAIC’s AI Bulletin. Cross-border insurer groups stand to consolidate data lakes, extracting predictive insights at continental scale once privacy frameworks interoperate.

Competitive Landscape

Market structure remains moderately concentrated. Octo Telematics maintains the largest global install base, but its North America insurance telematics market influence is increasingly challenged by domestic analytics specialists. Cambridge Mobile Telematics amplified scale via its 2024 acquisition of Amodo and recently won a Frost & Sullivan leadership award, underlining momentum behind its sensor-agnostic platform. OEM insurgents are also reshaping rivalry; GM’s insurance arm directly targets policyholders without broker intermediaries, signalling a future where automaker-carriers own the primary customer interface.

Strategic consolidation highlights include Powerfleet’s USD 200 million purchase of Fleet Complete, forming a 2.6 million-subscriber fleet AIoT powerhouse focused on commercial telematics analytics. Competitive tactics pivot around differentiated crash detection, eco-scoring, and open-API ecosystems that simplify carrier integration. White-space niches remain in motorcycle, RV, and usage-based commercial liability lines where incumbent scoring models lag. Regulatory complexity is emerging as a competitive moat; firms with embedded governance and model-audit workflows can onboard carriers faster, driving further consolidation through capability acquisitions.

North America Insurance Telematics Industry Leaders

State Farm Mutual Automobile Insurance Co.

Progressive Corp.

Allstate Corp.

USAA

Intact Financial Corp. (Canada)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Powerfleet completed its USD 200 million acquisition of Fleet Complete, creating a combined entity with 2.6 million subscribers and projected USD 400 million revenue.

- May 2024: Cambridge Mobile Telematics acquired Amodo to enhance global platform reach and AI analytics.

- April 2024: Powerfleet and MiX Telematics closed their business combination, forming a unified AIoT fleet platform.

- April 2024: Cambridge Mobile Telematics launched Fuel Score and Eco Score metrics for insurers and drivers.

North America Insurance Telematics Market Report Scope

Insurance telematics is used to track how people drive. It involves technology, such as GPS and sensors, to monitor and collect data on an individual's driving behavior. Insurance organizations use this data to assess risk and set personalized premiums accurately. Telematics devices installed in a vehicle help to track various parameters, such as speed, distance, and driving habits, which allows insurers to reward safe driving or adjust premiums based on actual usage patterns. Various telematics devices include cigarette-lighter plugs, smart tags, OBD (On-Board Diagnostic) devices, battery lines, windshield-mounted devices, black boxes, and smartphone apps.

The market for insurance telematics was analyzed considering the total number of active premiums filed by the various insurance providers across North America. The scope of the study includes different usage-based insurance telematics revenue models that are pay-as-you-drive, pay-how-you-drive, and manage-how-you-drive. The study also compares various types of telematics hardware insurance solutions across the United States and Canada, such as portable, embedded, and smartphone-based. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates during the forecast period. The study further analyzes the overall impact of COVID-19 and macroeconomic trends on the ecosystem. The report's scope encompasses market sizing and forecasts for the various market segments.

The North American insurance telematics market is segmented by country (United States, Canada). The market size and forecasts regarding the number of active premiums for all the above segments are provided.

By Revenue Model

| Pay-as-You-Drive |

| Pay-how-You-Drive |

| Manage-how-You-Drive |

By Telematics Hardware Type

| Portable |

| Embedded |

| Smartphone Based |

By Vehicle Type

| Passenger Cars |

| Commercial Vehicles |

By End-user

| Personal Lines |

| Commercial Fleets |

By Country

| United States |

| Canada |

| By Revenue Model | Pay-as-You-Drive |

| Pay-how-You-Drive | |

| Manage-how-You-Drive | |

| By Telematics Hardware Type | Portable |

| Embedded | |

| Smartphone Based | |

| By Vehicle Type | Passenger Cars |

| Commercial Vehicles | |

| By End-user | Personal Lines |

| Commercial Fleets | |

| By Country | United States |

| Canada |

Key Questions Answered in the Report

What is the projected value of the North America insurance telematics market in 2030?

It is forecast to reach USD 379.45 million by 2030, expanding at a 29.1% CAGR.

Which telematics hardware format holds the largest share today?

Smartphone-based applications lead with 54.9% 2024 revenue due to high device penetration and no install cost.

Why are commercial fleets adopting telematics faster than passenger vehicles?

Fleets see measurable ROI through lower liability premiums, fuel savings, and compliance benefits, supporting a 34.11% CAGR outlook.

How do privacy regulations affect telematics growth?

Regulations such as Californian's CCPA require explicit consent and data-governance audits, raising compliance costs but clarifying legal frameworks that ultimately support sustainable expansion.

Which revenue model is growing the fastest?

Manage-how-you-drive programs, which combine real-time coaching with pricing, are forecast to grow at 34.82% CAGR through 2030.

What competitive moves are reshaping the market landscape?

Major acquisitions such as Powerfleet-Fleet Complete and CMT-Amodo indicate consolidation toward end-to-end AI analytics platforms.

Page last updated on: