Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Growth Rate | 4.50% CAGR |

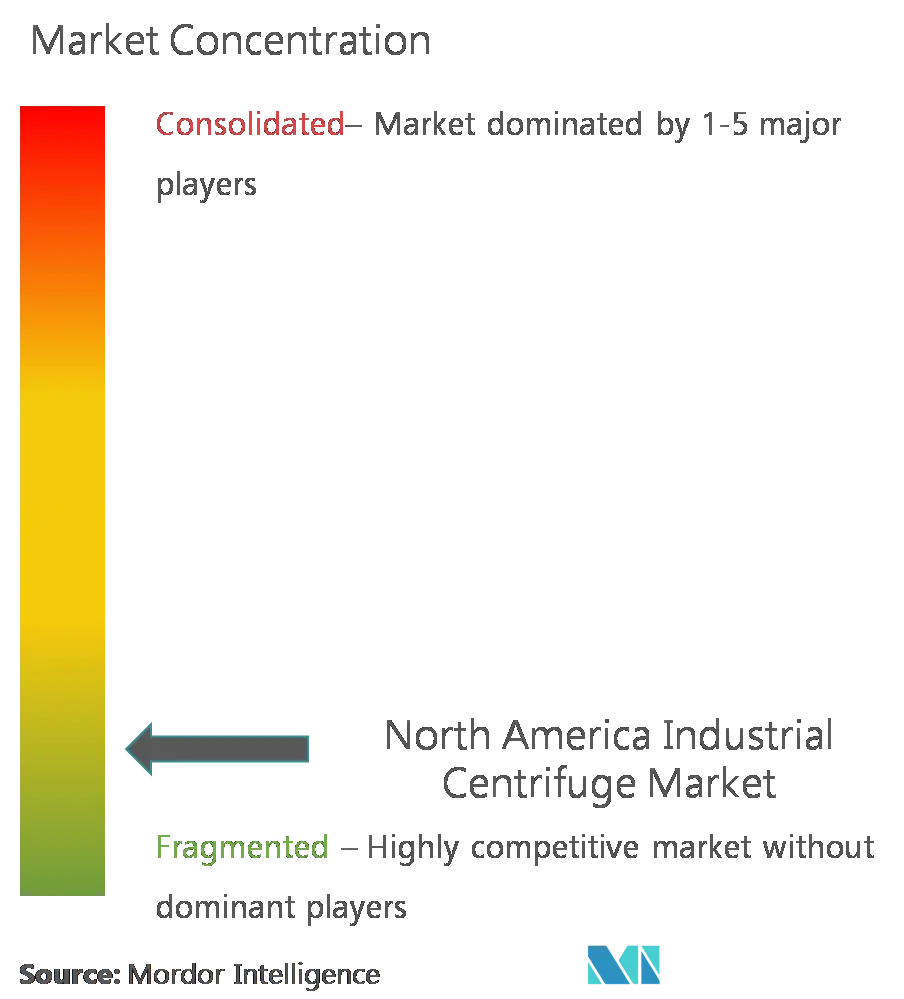

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Industrial Centrifuge Market Analysis by Mordor Intelligence

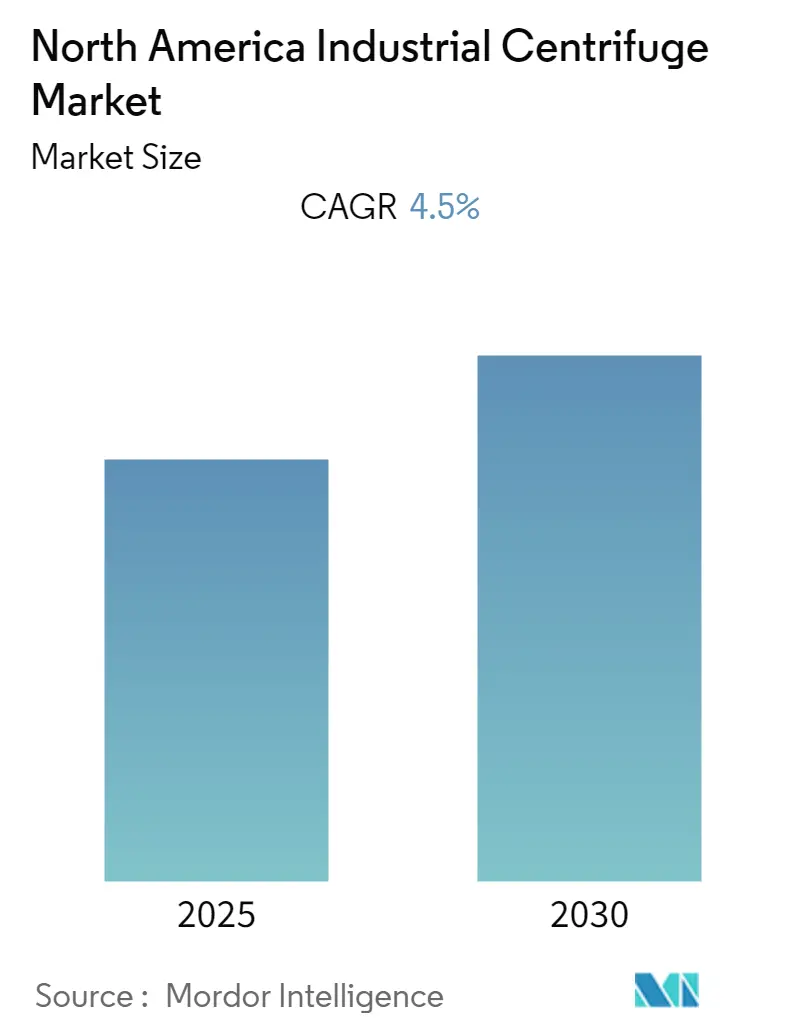

The North America Industrial Centrifuge Market is expected to register a CAGR of 4.5% during the forecast period.

The North American industrial centrifuge market is experiencing significant transformation driven by broader industrial modernization and technological advancement. The chemical industry, a major end-user of industrial centrifuges, has demonstrated remarkable strength, contributing approximately 25% to the United States GDP in 2022. This robust performance is complemented by substantial investments in new manufacturing facilities, as evidenced by Dow's landmark USD 6.5 billion commitment to the Fort Saskatchewan Path2Zero project announced in November 2023, which includes building the world's first net-zero Scope 1 and 2 emissions ethylene cracker and derivatives facility in Alberta, Canada.

Technological innovation continues to reshape the industrial centrifuge landscape, with manufacturers focusing on developing more sophisticated and efficient solutions. In January 2024, GEA launched X Control, a groundbreaking control system for centrifuges that enhances integration, connectivity, data processing, and safety while laying the foundation for artificial intelligence integration. This development represents a significant step toward smart manufacturing and demonstrates the industry's commitment to digital transformation and operational efficiency improvements.

The pharmaceutical sector remains a crucial growth driver for the industrial centrifuge market, with total pharmaceutical sales in the United States reaching USD 529.19 billion in 2022. The industry's expansion is further evidenced by recent investments, including Evonik's USD 220 million commitment to a global-scale production facility for pharmaceutical specialty lipids in Lafayette, Indiana, announced in March 2023, and Indivior's expansion plans for a sterile pharmaceutical production facility in Raleigh, announced in November 2023.

The market is witnessing significant regional developments across various industrial sectors. In Canada, chemical shipments demonstrated strong performance, reaching CAD 72.7 billion in 2022, indicating robust demand for industrial centrifuges in chemical processing applications. Meanwhile, Mexico's mining sector has shown remarkable growth, attracting USD 2.9 billion in foreign direct investment during the first three quarters of 2023, representing the highest recorded FDI for a similar period since 2013, which has stimulated demand for industrial centrifuges in mineral processing applications.

North America Industrial Centrifuge Market Trends and Insights

Growing Adoption of Centrifuges in End-User Industries

The growing demand for industrial centrifuges across various end-user industries is driving significant market growth in North America. In the chemical sector, since 2010, the industry has invested $135 billion in new and expanded facilities in the United States alone, with 235 projects completed and operational. The momentum continues with 44 projects worth $31 billion currently under construction, while another 72 projects valued at $68 billion are in the planning phase. This robust pipeline of chemical industry projects is complemented by major investments like Dow's $6.5 billion Fort Saskatchewan Path2Zero project announced in 2023, which includes building a new ethylene cracker and expanding polyethylene capacity by two million metric tonnes per annum.

The pharmaceutical sector represents another major growth driver, with the United States maintaining its position as the global leader with a 43% share of the worldwide pharmaceutical market. The industry's strength is evidenced by the fact that five out of the top ten global pharmaceutical companies are headquartered in the United States. Recent investments underscore this growth trajectory, such as Eli Lilly's November 2023 announcement of a $2.5 billion investment in a new manufacturing plant for injectable drugs and devices. The food and beverage industry also demonstrates strong adoption, with over 33% of the world's top 50 food and beverage processing companies based in the United States. The Chemistry Industry Association of Canada is tracking approximately 20 additional chemical and plastics-associated projects worth about $20 billion, encompassing applications such as ammonia production, hydrogen production, carbon capture and storage, plastics recycling, and battery chemicals for electric vehicles.

The increasing utilization of industrial centrifuge technology is particularly notable in these sectors, where efficiency and precision are paramount. Industrial centrifuge manufacturers are continuously innovating to meet the diverse needs of these industries. Additionally, the role of industrial separators in enhancing production processes cannot be overstated, as they contribute significantly to the operational efficiency and product quality across various applications.

Understand The Key Trends Shaping This Market

Download PDF

Segment Analysis: Type

Sedimentation Segment in North America Industrial Centrifuge Market

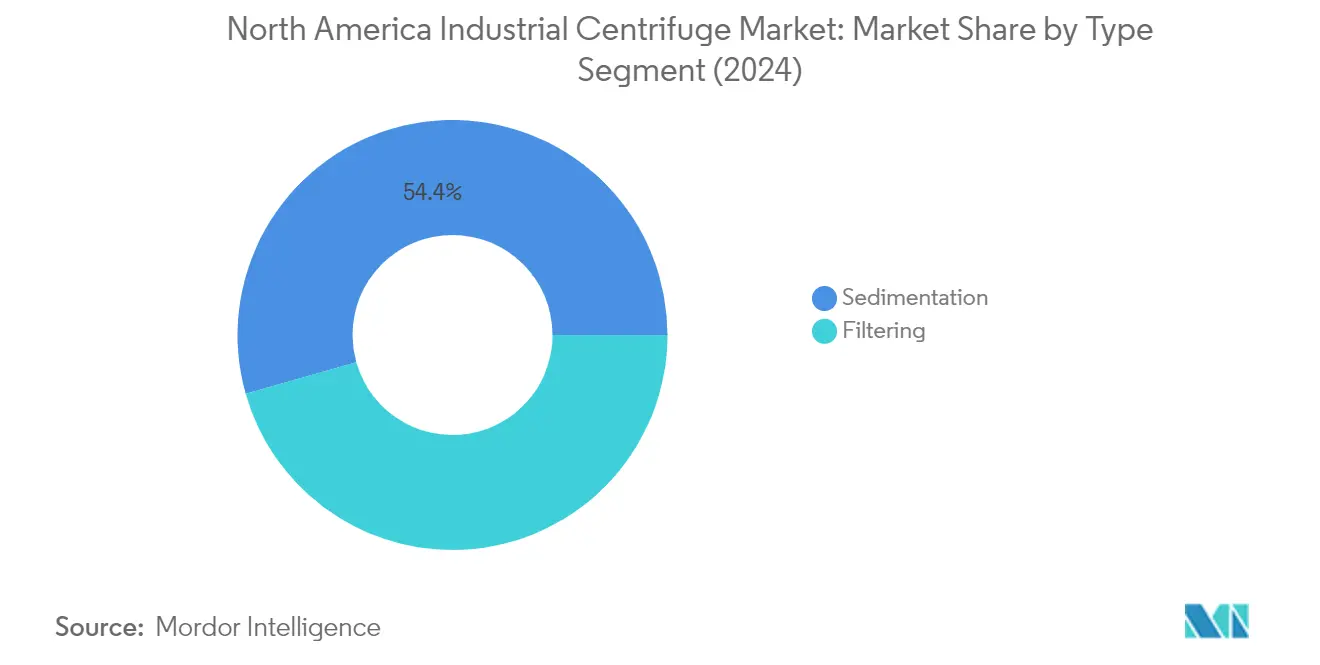

The sedimentation centrifuge market dominates the North American industrial centrifuge market, holding approximately 54% market share in 2024, while also demonstrating the strongest growth trajectory with a projected growth rate of around 5% during 2024-2029. This segment's prominence is driven by its extensive applications across various industries, particularly in chemical processing, pharmaceutical manufacturing, and wastewater treatment. The segment's growth is further bolstered by increasing investments in chemical manufacturing facilities across North America, with significant projects like Dow's USD 6.5 billion Fort Saskatchewan Path2Zero project in Alberta, Canada. Sedimentation centrifuges are particularly valued for their ability to separate liquids from solids based on density differences, making them essential in applications ranging from crude oil processing to pharmaceutical production. The technology's versatility in handling different particle sizes and its high separation efficiency have made it the preferred choice for industries requiring precise solid-liquid separation processes.

Filtering Segment in North America Industrial Centrifuge Market

The filtering segment represents a significant portion of the North American industrial centrifuge market, complementing the sedimentation segment with its specialized applications in various industries. This segment is particularly crucial in applications requiring high-purity separation, such as in pharmaceutical manufacturing and fine chemical production. Filtering centrifuges are distinguished by their pass-through bowl design with openings, offering unique advantages in separation efficiency and overall centrifuge design. The segment's growth is supported by increasing demand from water treatment facilities, food processing plants, and chemical manufacturing industries across North America. Recent developments in the segment include technological advancements focusing on improved maintainability, enhanced performance, and energy efficiency, making these systems more attractive to end-users seeking sustainable solutions.

Segment Analysis: By Design

Horizontal Centrifuge Segment in North America Industrial Centrifuge Market

The horizontal centrifuge segment dominates the North America industrial centrifuge market, commanding approximately 61% of the market share in 2024. This significant market position is attributed to its extensive applications across various industries, including pharmaceutical, oil and gas, and metals and mining sectors. Horizontal centrifuges offer superior flexibility in operation and can handle solids of different sizes ranging from 10 to 15 millimeters, making them particularly valuable in diverse industrial applications. The segment's prominence is further strengthened by its higher rotational speed capabilities compared to vertical centrifuges, enabling greater discharge speeds and improved separation efficiency. Major manufacturers like Heinkel have continued to innovate in this space, with developments such as the BlueTector horizontal peeler centrifuge specifically designed for pharmaceutical and chemical industries, featuring advanced capabilities like direct drive and easy access to mechanical sections.

Vertical Centrifuge Segment in North America Industrial Centrifuge Market

The vertical centrifuge segment is projected to experience the fastest growth rate in the North America industrial centrifuge market, with an expected CAGR of approximately 4.4% during the forecast period 2024-2029. This accelerated growth is driven by several key advantages that vertical centrifuges offer, including cost-effectiveness due to their compact size and lower power consumption compared to horizontal centrifuges. The segment's growth is further propelled by its superior solid-liquid separation performance, higher throughput capabilities, and maximum purity achievement. Vertical centrifuges are increasingly preferred in applications requiring precise separation, such as in pharmaceutical manufacturing and biotechnology processes. The segment's expansion is also supported by ongoing technological advancements that enhance operational efficiency and reduce maintenance requirements, making these centrifuges particularly attractive for industries seeking to optimize their separation processes while maintaining high product quality standards.

Segment Analysis: By Operation Mode

Continuous Segment in North America Industrial Centrifuge Market

The continuous centrifuge segment dominates the North America industrial centrifuge market, holding approximately 53% market share in 2024. This significant market position is driven by the segment's widespread adoption across various industries, including pharmaceutical manufacturing, water treatment, and chemical processing. Continuous centrifuges are particularly valued for their ability to handle large volumes of materials efficiently, making them ideal for high-throughput industrial applications. The technology's capability to provide uninterrupted operation, reduced labor requirements, and consistent separation quality has made it the preferred choice for many industrial processes. Additionally, continuous centrifuges offer advantages such as automated control systems, real-time monitoring capabilities, and integration with modern industrial automation systems, which has further strengthened their market position.

Batch Segment in North America Industrial Centrifuge Market

The batch centrifuge segment is emerging as the fastest-growing segment in the North America industrial centrifuge market, projected to grow at approximately 5% CAGR from 2024 to 2029. This growth is primarily driven by increasing demand from specialized applications in the pharmaceutical and biotechnology industries, where precise control over separation processes is crucial. The segment's growth is further supported by technological advancements in batch centrifuge designs, including improved automation features, enhanced safety systems, and better process control capabilities. The flexibility offered by batch centrifuges in handling different types of materials and their ability to maintain product quality through controlled processing conditions has made them increasingly popular in research and development applications, specialty chemical manufacturing, and other niche industrial processes.

Segment Analysis: By Industry

Food and Beverage Segment in North America Industrial Centrifuge Market

The Food and Beverage segment dominates the North America industrial separator market, holding approximately 22% market share in 2024. This segment's leadership position is driven by extensive applications in milk separation, cheese production, pulp control in juices, edible oil production, essential oil recovery, and the production of starch and yeast. The United States plays a crucial role through its processed food industry, with over 33% of the world's top 50 food and beverage processing companies based in the country. Major investments continue to strengthen this segment, such as Walmart's USD 350 million investment in a milk processing plant in Lowndes County announced in October 2023, and Nissin Foods USA's USD 228 million investment for their third manufacturing facility in South Carolina announced in November 2023. The segment's dominance is further reinforced by the presence of approximately 66 new projects in the food and beverage industry across North America as of January 2024, with 24 new plants and 16 expansion projects in development.

Metal and Mining Segment in North America Industrial Centrifuge Market

The Metal and Mining segment is emerging as the fastest-growing segment in the North America Industrial Centrifuge market, projected to grow at approximately 6% CAGR from 2024 to 2029. This robust growth is driven by increasing investment in mining projects across the region, particularly in critical minerals essential for clean energy technologies. The United States government is actively working with private companies to increase investment in more than 15 critical minerals projects. Significant developments include the Hermosa mining project in Arizona, which was included in the FAST-41 process in May 2023, aimed at supplying battery-grade manganese to the North American electric vehicle industry. In Canada, the sector has witnessed substantial growth with 124 mining projects valued at approximately USD 88.3 billion, while Mexico has announced 11 new projects worth USD 2.71 billion, focusing on extracting metals like gold, copper, silver, zinc, and lead.

Remaining Segments in North America Industrial Centrifuge Market

The other segments in the North America Industrial Centrifuge market include Pharmaceuticals, Water and Wastewater Treatment, Chemicals, Power, and Pulp and Paper industries, each contributing significantly to the market's diversity. The Pharmaceutical segment benefits from the region's strong healthcare infrastructure and continuous investments in drug development facilities. The Water and Wastewater Treatment segment is driven by increasing environmental regulations and infrastructure development projects. The Chemical sector leverages centrifuges for various separation processes in manufacturing and processing applications. The Power sector, particularly nuclear power plants, utilizes centrifuges for uranium enrichment processes. The Pulp and Paper industry, despite facing some challenges, continues to use centrifuges for various separation processes in paper manufacturing and recycling operations.

North America Industrial Centrifuge Market Geography Segment Analysis

Industrial Centrifuge Market in the United States

The United States dominates the North American industrial centrifuge market, commanding approximately 89% of the total market share in 2024. The country's market leadership is driven by its robust pharmaceutical, food and beverage, chemical, and wastewater treatment sectors. The presence of major industrial centrifuge manufacturers and a strong focus on technological advancement has created a sophisticated market ecosystem. The country's stringent environmental regulations governing industrial waste disposal and water treatment have necessitated the widespread adoption of industrial centrifuges across various sectors. The United States also benefits from significant investments in research and development, particularly in the pharmaceutical sector, where industrial centrifuges play a crucial role in drug development and manufacturing processes. The market is further strengthened by the presence of a large number of end-user industries and their continuous focus on process optimization and efficiency improvements.

Industrial Centrifuge Market in Mexico

Mexico, as part of the Rest of North America region, is positioned to experience robust growth with a projected CAGR of approximately 6% from 2024 to 2029. The country's industrial centrifuge market is experiencing rapid expansion driven by increasing investments in manufacturing facilities and growing environmental concerns. The food and beverage industry in Mexico has been particularly active in adopting industrial centrifuges, with several major international companies establishing or expanding their production facilities in the country. The country's strategic location and trade agreements with the United States and Canada have attracted significant foreign investment in manufacturing sectors that require industrial centrifuge applications. Mexico's growing focus on wastewater treatment and environmental protection has also created new opportunities for industrial centrifuge manufacturers. The government's initiatives to modernize industrial infrastructure and improve manufacturing capabilities have further accelerated market growth.

Industrial Centrifuge Market in Canada

Canada represents a significant market for industrial centrifuges, driven by its strong presence in the mining, oil and gas, and chemical processing industries. The country's commitment to environmental sustainability has led to increased adoption of industrial centrifuges in wastewater treatment applications. Canadian industries are increasingly focusing on modernizing their manufacturing processes, with particular emphasis on efficiency and environmental compliance. The country's robust pharmaceutical sector has been actively investing in research and development facilities, creating sustained demand for specialized centrifuge equipment. The presence of stringent environmental regulations and the government's support for industrial modernization have created a favorable environment for market growth. Canadian companies are also showing increased interest in advanced centrifuge technologies that offer better efficiency and reduced environmental impact.

Industrial Centrifuge Market in Other Countries

The industrial centrifuge market in other North American countries, including those in Central America such as Belize, Costa Rica, El Salvador, Guatemala, Honduras, Nicaragua, and Panama, presents unique opportunities and challenges. These markets are characterized by their growing food processing industries and increasing focus on environmental regulations. The regional market dynamics are influenced by factors such as foreign investment in manufacturing sectors, modernization of industrial processes, and growing awareness of environmental protection. These countries are gradually adopting advanced industrial centrifuge technologies, particularly in their food and beverage processing sectors. The market in these regions is also benefiting from increasing investments in wastewater treatment infrastructure and growing industrial activities. While smaller in scale compared to the major markets, these countries are showing promising developments in terms of industrial modernization and environmental compliance requirements.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

Top Companies in North America Industrial Centrifuge Market

The market features established players like Alfa Laval AB, Andritz AG, Ferrum Ltd, and GEA Group AG leading the competitive landscape through continuous innovation and strategic expansion. Companies are focusing on developing energy-efficient industrial centrifuge solutions while incorporating advanced automation and control systems to meet evolving industry demands. The competitive dynamics are shaped by significant investments in research and development, particularly in areas like pharmaceutical applications and wastewater treatment. Market leaders are strengthening their positions through strategic partnerships with end-user industries and expanding their service networks across the region. Product customization capabilities, technical support infrastructure, and after-sales service quality have emerged as key differentiators in the industrial centrifuges market, with companies investing heavily in building comprehensive solution portfolios that address specific industry requirements.

Consolidated Market with Strong Global Players

The North American industrial centrifuge market exhibits a moderately consolidated structure dominated by global industrial equipment manufacturers with diverse product portfolios. These established players leverage their extensive manufacturing capabilities, well-established distribution networks, and strong relationships with end-users across various industries, including pharmaceuticals, chemicals, and food processing. The market is characterized by high entry barriers due to significant capital requirements, technical expertise needs, and stringent quality standards, which favor larger established players with robust financial resources and research capabilities.

The competitive landscape is witnessing increased merger and acquisition activities as companies seek to expand their technological capabilities and geographic presence. Major players are actively pursuing strategic acquisitions of regional specialists and technology providers to enhance their product offerings and strengthen their market position. The trend towards consolidation is particularly evident in specialized segments like pharmaceutical centrifuges and environmental applications, where technical expertise and industry-specific knowledge are crucial for success.

Innovation and Service Excellence Drive Growth

Success in the industrial centrifuge manufacturers market increasingly depends on companies' ability to offer comprehensive solution packages that combine advanced technology with superior service support. Market leaders are focusing on developing innovative products with enhanced automation capabilities, improved energy efficiency, and reduced maintenance requirements. The ability to provide customized solutions for specific industry applications, coupled with strong technical support and maintenance services, has become crucial for maintaining a competitive advantage. Companies are also investing in digital technologies to offer predictive maintenance and remote monitoring capabilities, addressing the growing demand for smart manufacturing solutions.

For new entrants and smaller players, success lies in identifying and serving niche market segments with specialized requirements. Companies need to focus on developing strong relationships with end-users in specific industries while maintaining flexibility in product customization and service delivery. The increasing emphasis on environmental regulations and sustainability requirements presents opportunities for companies offering eco-friendly and energy-efficient solutions. Building strong local service networks and establishing partnerships with industry-specific solution providers can help companies overcome entry barriers and gain market share in specific segments.

North America Industrial Centrifuge Industry Leaders

Alfa Laval AB

Andritz AG

GEA Group AG

Centrisys Corporation

Flottweg SE.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2022: GEA launched a new range of pharmaceutical industrial centrifuge systems for North America called Kytero. Kytero is ready for manufacturing. Filter regions can be reduced by 75%. The system requires a standard power connection; intermediate tanks are obsolete. The simple exchange eliminates CIP (clean-in-place) and SIP (sterilize-in-place).

- February 2022: Beckman Coulter introduced the Allegra V-15R refrigerated centrifuge. With ten rotor configurations, 50 programmed runs, and a large assortment of adapters, a wide range of workflows and applications may be carried out.

North America Industrial Centrifuge Market Report Scope

An industrial centrifuge is a device that employs centrifugal force to subject a specimen to a constant force, such as separating different components of a fluid. This is accomplished by rapidly spinning the fluid within a receptacle, separating fluids of varying densities or liquids from solids.

The North American industrial centrifuge market is segmented by type, design, operation mode, industry, and geography. By type, the market is segmented into sedimentation and filtering. By design, the market is segmented into horizontal centrifuge and vertical centrifuge. By operation mode, the market is segmented into batch and continuous. By industry, the market is segmented into food and beverage, pharmaceutical, water and wastewater treatment, chemical, metal and mining, power, pulp and paper, and others. The report also covers the market size and forecasts for the industrial centrifuge market across the major countries in the region. For each segment, market sizing and forecasts have been done based on revenue (USD billion).

Type

| Sedimentaion |

| Filtering |

Design

| Horizontal Centrifuge |

| Vertical Centrifuge |

Operation Mode

| Batch |

| Continuous |

Industry

| Food and Beverage |

| Pharmaceutical |

| Water and Wastewater Treatment |

| Chemical |

| Metal and Mining |

| Power |

| Pulp and Paper |

| Other Industries |

Geography

| United States |

| Canada |

| Rest of North America |

| Type | Sedimentaion |

| Filtering | |

| Design | Horizontal Centrifuge |

| Vertical Centrifuge | |

| Operation Mode | Batch |

| Continuous | |

| Industry | Food and Beverage |

| Pharmaceutical | |

| Water and Wastewater Treatment | |

| Chemical | |

| Metal and Mining | |

| Power | |

| Pulp and Paper | |

| Other Industries | |

| Geography | United States |

| Canada | |

| Rest of North America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current North America Industrial Centrifuge Market size?

The North America Industrial Centrifuge Market is projected to register a CAGR of 4.5% during the forecast period (2025-2030)

Who are the key players in North America Industrial Centrifuge Market?

Alfa Laval AB, Andritz AG, GEA Group AG, Centrisys Corporation and Flottweg SE. are the major companies operating in the North America Industrial Centrifuge Market.

What years does this North America Industrial Centrifuge Market cover?

The report covers the North America Industrial Centrifuge Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the North America Industrial Centrifuge Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.