Market Size of North America Hemodynamic Monitoring Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

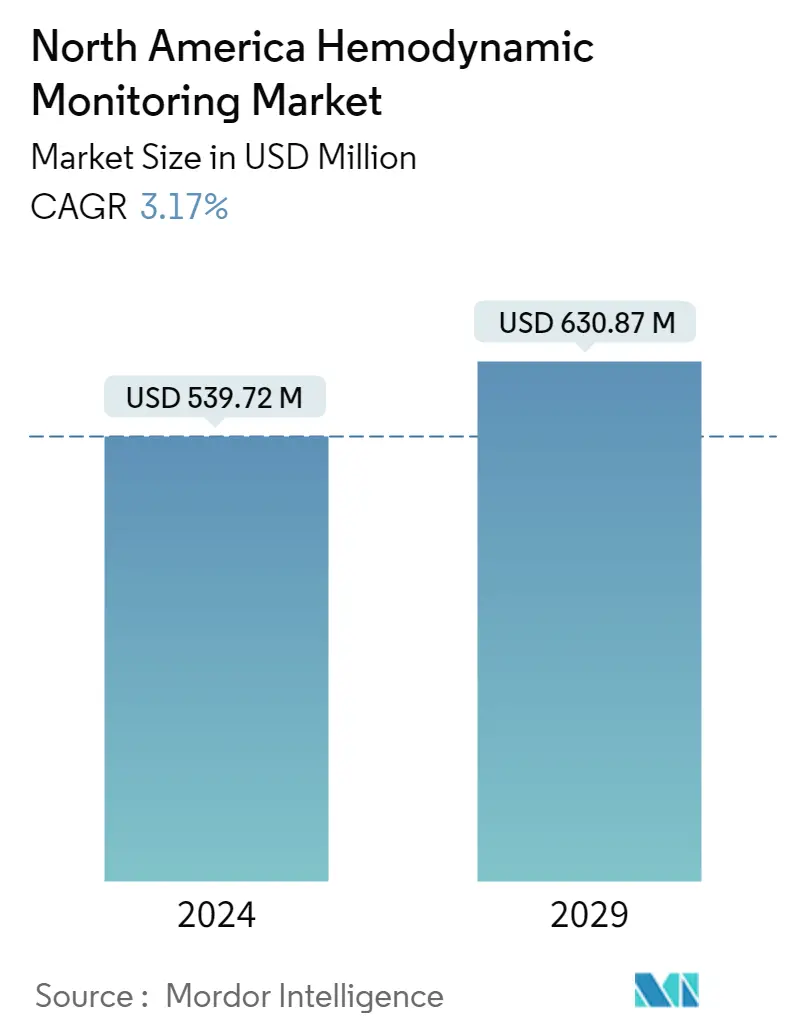

| Market Size (2024) | USD 539.72 Million |

| Market Size (2029) | USD 630.87 Million |

| CAGR (2024 - 2029) | 3.17 % |

Major Players

*Disclaimer: Major Players sorted in no particular order |

North America Hemodynamic Monitoring Market Analysis

The North America Hemodynamic Monitoring Market size is estimated at USD 539.72 million in 2024, and is expected to reach USD 630.87 million by 2029, growing at a CAGR of 3.17% during the forecast period (2024-2029).

The COVID-19 pandemic significantly impacted the North American hemodynamic monitoring market. Patients with COVID-19 respiratory failure showed a marked rise in blood pressure over time, not accompanied by distinctive markers of circulatory failure. For instance, according to the study published by the National Library of Medicine, in May 2022, comparing cardiac cases in COVID-19 to respiratory cases, cardiac injuries were documented in 19.7% to 29.8% of the patients. Numerous pathways contributed to the involvement of the cardiac myocardium in COVID-19, and up to 20%-30% of hospitalized patients exhibit this involvement, such as high troponin levels. This increased demand for hemodynamic monitors during the pandemic to assess critically ill patients admitted for COVID-19. Furthermore, the postponed treatment procedures and surgeries were resumed worldwide as the COVID-19 cases declined and pandemic restrictions were uplifted. This led to an increase in cardiac surgeries, creating a huge demand for hemodynamic monitoring. For instance, according to an article published by the Journal of the American College of Cardiology, in May 2022, there was a modest (3%-13%) increase in cardiac procedure volumes from pre-pandemic to 2021, associated with recovery rates of 105% to 119% in the United States and Canada. Hence, the COVID-19 pandemic has had a significant impact on market growth.

The key factors propelling the growth of this market are an increase in the number of critically ill geriatric cases, a rise in the prevalence of cardiac disorders and diabetes, increasing demand for home-based and non-invasive monitoring systems, and an increase in the number of people suffering from hypertension. For instance, as per the Heart&Stroke report of 2022, more than 750,000 people were living with heart failure in Canada in 2022, with over 106,000 new cases every year. Hence, for proper diagnosis and treatment of heart-related diseases, hemodynamic monitoring plays an important role which is likely to drive the market growth over the forecast period. Furthermore, according to American Heart Association data updated in July 2022, the number of elderly patients with calcific aortic stenosis is projected to more than double by 2050 in the United States. Thus, the demand for hemodynamic monitoring is likely to increase with the number of critically ill geriatric patients which is expected to promote market growth in North America.

Additionally, various strategies adopted by the key market players such as product launches, mergers and acquisitions are anticipated to drive the market over the forecast period. For instance, in April 2021, Spacelabs Healthcare, a division of OSI Systems, Inc. was awarded a three-year Premier agreement for physiological patient monitoring and non-invasive cardiology solutions in the United States. Such development is expected to propel the market growth in North America.

Hence, the abovementioned factors are attributed collectively to the market growth. However, increasing incidences of complications associated with invasive monitoring systems and stringent FDA guidelines for approval of new systems are the major factors restraining the market growth.

North America Hemodynamic Monitoring Industry Segmentation

As per the scope of the report, critically ill patients require continuous monitoring of their vital parameters. This is done by direct pressure monitoring systems, which are also known as hemodynamic systems. The main function of these systems is to monitor cardiac activity. The hemodynamic systems give information about blood pressure, blood volume, and fluid balance. The North America Hemodynamic Monitoring Market is Segmented by System (Minimally Invasive Monitoring Systems, Invasive Monitoring Systems, and Non-invasive Monitoring Systems), Application (Laboratory-based Monitoring Systems, Home-based Monitoring Systems, Hospital-based Monitoring Systems), and Geography (United States, Canada, and Mexico). The report offers the value (USD million) for the above segments.

| By System | |

| Minimally Invasive Monitoring Systems | |

| Invasive Monitoring Systems | |

| Non-invasive Monitoring Systems |

| By Application | |

| Laboratory-based Monitoring Systems | |

| Home-based Monitoring Systems | |

| Hospital-based Monitoring Systems |

| Geography | |||||

|

North America Hemodynamic Monitoring Market Size Summary

The North American hemodynamic monitoring market is poised for growth, driven by several key factors. The market has experienced a significant impact due to the COVID-19 pandemic, which heightened the demand for hemodynamic monitors as they were essential in assessing critically ill patients with respiratory failure and cardiac injuries. As the pandemic subsided and treatment procedures resumed, there was a surge in cardiac surgeries, further fueling the demand for these monitoring systems. The increasing prevalence of cardiac disorders, diabetes, and hypertension, coupled with a growing geriatric population, is expected to propel market expansion. Non-invasive monitoring systems are gaining traction due to their ease of use and the rising number of elderly patients, which is anticipated to stimulate market growth over the forecast period.

The competitive landscape of the North American hemodynamic monitoring market is moderately concentrated, with key players such as Getinge Group, Koninklijke Philips NV, Edwards Lifesciences Corporation, and GE Healthcare actively participating. These companies are engaging in strategic initiatives like product launches, mergers, and acquisitions to enhance their market presence. The United States is expected to lead the market growth, supported by advanced healthcare infrastructure and well-established insurance policies. The rising incidence of cardiovascular diseases and the introduction of innovative monitoring solutions, such as those receiving FDA clearance, are likely to drive the market forward. Despite challenges like complications associated with invasive systems and stringent regulatory guidelines, the market is set to experience steady growth, supported by ongoing technological advancements and strategic collaborations.

North America Hemodynamic Monitoring Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.2.1 Increasing Geriatric Population and Rise in the Prevalence of Cardiac Disorders and Diabetes

-

1.2.2 Increasing Demand for Home-based and Non-invasive Monitoring Systems

-

1.2.3 Advances in Technology due to Funding by Private Players and Government Bodies

-

-

1.3 Market Restraints

-

1.3.1 Increasing Incidences of Complications Associated with Invasive Monitoring Systems

-

1.3.2 Stringent FDA Guidelines for Approval of New Systems

-

-

1.4 Porter's Five Force Analysis

-

1.4.1 Threat of New Entrants

-

1.4.2 Bargaining Power of Buyers/Consumers

-

1.4.3 Bargaining Power of Suppliers

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION (Market Size by Value - USD million)

-

2.1 By System

-

2.1.1 Minimally Invasive Monitoring Systems

-

2.1.2 Invasive Monitoring Systems

-

2.1.3 Non-invasive Monitoring Systems

-

-

2.2 By Application

-

2.2.1 Laboratory-based Monitoring Systems

-

2.2.2 Home-based Monitoring Systems

-

2.2.3 Hospital-based Monitoring Systems

-

-

2.3 Geography

-

2.3.1 North America

-

2.3.1.1 United States

-

2.3.1.2 Canada

-

2.3.1.3 Mexico

-

-

-

North America Hemodynamic Monitoring Market Size FAQs

How big is the North America Hemodynamic Monitoring Market?

The North America Hemodynamic Monitoring Market size is expected to reach USD 539.72 million in 2024 and grow at a CAGR of 3.17% to reach USD 630.87 million by 2029.

What is the current North America Hemodynamic Monitoring Market size?

In 2024, the North America Hemodynamic Monitoring Market size is expected to reach USD 539.72 million.