Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Growth Rate | 3.68% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Hard Facility Management Market Analysis by Mordor Intelligence

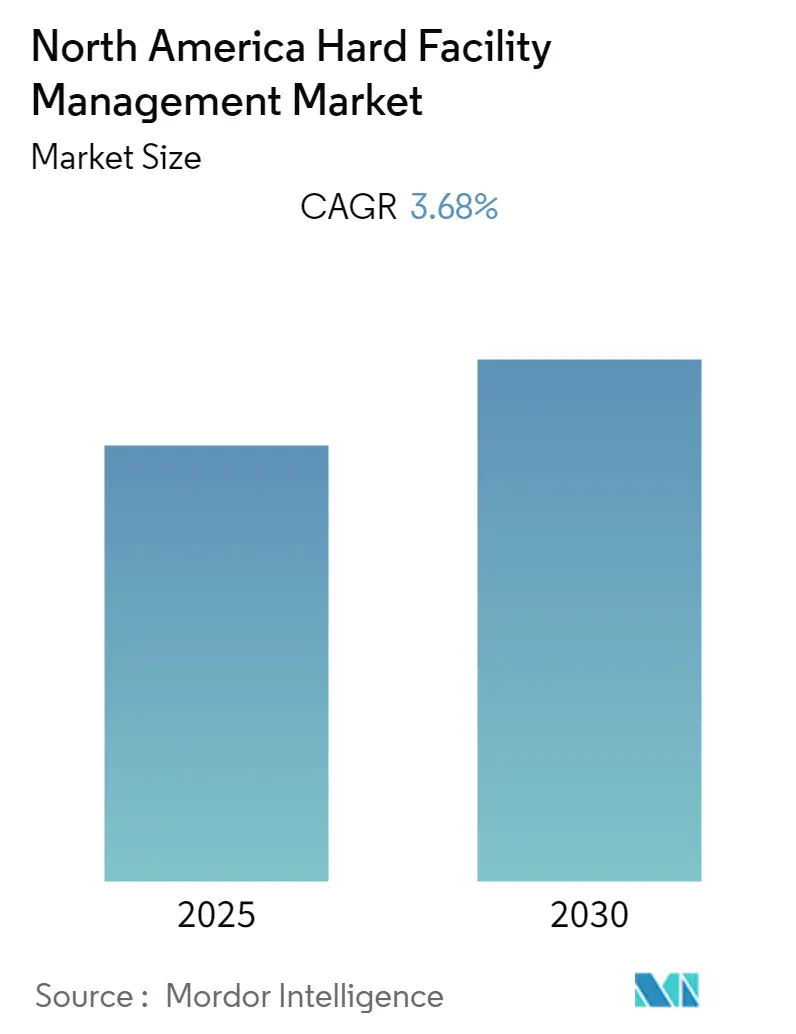

The North America Hard Facility Management Market is expected to register a CAGR of 3.68% during the forecast period.

The North American hard facility management landscape is experiencing significant transformation driven by robust economic growth and construction sector expansion. The United States construction industry has demonstrated remarkable resilience, with the construction sector contributing USD 1,007.1 billion to the GDP in 2022, marking substantial growth from previous years. This expansion has created increased demand for comprehensive building systems management services across various sectors, particularly in commercial and industrial spaces. The commercial real estate sector has emerged as a key growth driver, with the United States market alone valued at USD 10,558.73 billion as of December 2022, necessitating sophisticated infrastructure management solutions to maintain and optimize these assets.

The industry is witnessing a paradigm shift towards integrated facility management solutions, combining traditional maintenance services with advanced technological capabilities. This evolution is exemplified by strategic acquisitions such as CBRE Group's purchase of E2C technology in August 2023, enhancing its facilities management service offering through AI/ML data-driven solutions. The integration of smart building technologies and automation systems is becoming increasingly prevalent, with facility managers leveraging these advancements to optimize operational efficiency and reduce maintenance costs. This technological transformation is particularly evident in the HVAC sector, where producer prices increased by 20% in 2022, reflecting the growing sophistication and demand for advanced climate control systems.

Sustainability and energy efficiency have emerged as critical priorities in facility management operations. In July 2023, the Biden administration launched the Climate Smart Buildings Initiative, targeting the implementation of energy-efficient services across 350,000 federal buildings. This initiative reflects a broader industry trend towards environmental responsibility and cost optimization through sustainable practices. The market is seeing increased adoption of energy management systems, smart meters, and green building technologies, with facility management providers expanding their service portfolios to include specialized sustainability solutions.

The industry is experiencing significant consolidation through strategic partnerships and technological collaborations. In June 2023, Eaton's partnership with FMX to implement preventative maintenance programs demonstrates the industry's move towards predictive maintenance solutions. The commercial construction sector continues to expand, with the value of new private construction reaching approximately USD 115.55 billion in 2022, driving demand for specialized building services. Market players are increasingly focusing on developing comprehensive service offerings that combine traditional hard facility management services with digital solutions, reflecting the evolving needs of modern facilities and their operators. The emphasis on building operations and technical building services is becoming more pronounced as facilities strive for efficiency and sustainability.

North America Hard Facility Management Market Trends and Insights

HIGH HVAC SERVICES DEMAND IN THE UNITED STATES

The United States experiences diverse climate conditions across its regions, from extreme cold in the northern states to intense heat in the southern regions, necessitating robust HVAC systems to maintain comfortable indoor environments year-round. This climatic diversity has created a substantial demand for HVAC services, reflected in the employment statistics from the US Bureau of Labor Statistics, which show that around 415,800 heating, air conditioning, and refrigeration mechanics and installers were employed in 2022, with projections indicating growth to 438,800 by 2032. The increasing emphasis on energy efficiency and sustainability has further amplified this demand, as facility management providers are essential in implementing energy-efficient technologies such as smart thermostats, variable-speed motors, and advanced controls that align with both public and private sector sustainability goals.

The integration of advanced technologies in HVAC systems has transformed the service landscape, with IoT sensors and smart controls offering unprecedented opportunities for innovation and optimization. Facility management providers that adopt these technologies can deliver enhanced system performance, predictive maintenance, and real-time monitoring capabilities to their clients. Additionally, stringent environmental regulations and building codes mandate compliance with specific HVAC-related standards, including energy efficiency mandates, refrigerant phase-outs, and emissions reductions. This regulatory environment has created a critical need for expert HVAC management services, as non-compliance can result in significant penalties and operational disruptions, making professional facility management services indispensable for maintaining regulatory compliance while ensuring optimal system performance. The role of HVAC maintenance is crucial in this context, ensuring systems are not only compliant but also efficient and reliable.

Understand The Key Trends Shaping This Market

Download PDF

RISE IN INFRASTRUCTURAL ACTIVITIES IN THE REGION

The North American region is experiencing significant growth in infrastructural development, particularly in the commercial and industrial sectors. According to the US Census Bureau, the value of commercial construction reached USD 114.79 billion in 2022, marking a substantial 21.47% increase from 2021. This growth is further supported by projections from the American Institute of Architects, which anticipates approximately 19.7% growth in the US non-residential construction market in 2023, with industrial construction expected to show the most substantial year-on-year change at around 55%. These developments have created an unprecedented demand for comprehensive facility management services to ensure the efficient operation and maintenance of these new infrastructures.

The infrastructure expansion is particularly evident in the corporate sector, with major technology companies establishing new facilities across the region. For instance, in July 2023, Infosys Public Services announced the opening of its new subsidiary in Canada, with headquarters in Ottawa and local offices in multiple locations including Mississauga, Calgary, and Burnaby. This trend of corporate expansion is complemented by significant investments in public infrastructure projects. For example, in May 2023, the U.S. General Services Administration announced a USD 43.5 million investment for upgrades at ten federal buildings, focusing on improving building infrastructure and installing new technology to enhance energy efficiency. These developments demonstrate the robust growth in infrastructure activities across various sectors, driving the demand for specialized facility management services to maintain and optimize these new and upgraded facilities. The need for infrastructure maintenance and building maintenance is increasingly critical to support these expansions, ensuring the longevity and efficiency of the facilities. Additionally, the integration of building engineering services is vital to address the complex needs of modern infrastructure.

Segment Analysis: By Type

MEP and HVAC Maintenance Services Segment in North America Hard FM Market

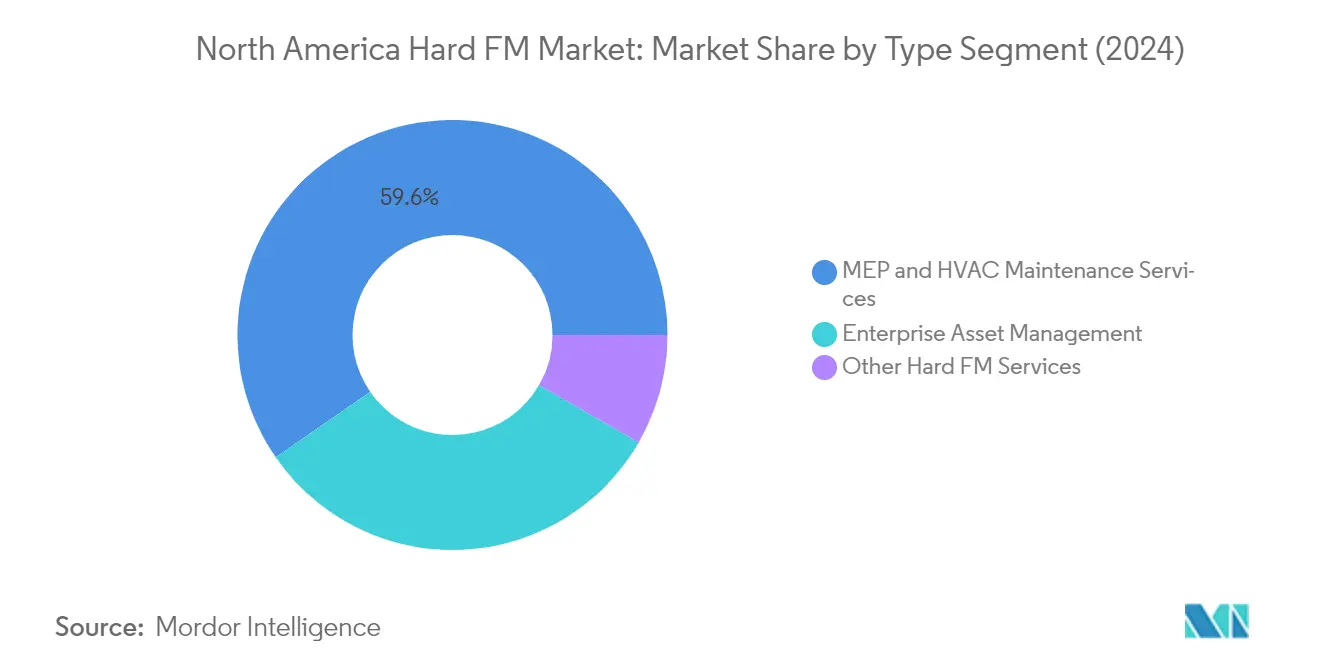

The MEP (Mechanical, Electrical, Plumbing) and HVAC maintenance services segment dominates the North American Hard Facility Management market, commanding approximately 60% market share in 2024. This significant market position is primarily driven by the increasing adoption of smart buildings in industrial, commercial, and institutional sectors across the region, which necessitates advanced HVAC systems for automating their functionalities. The segment's prominence is further reinforced by various government initiatives and rebate schemes, including tax credit systems that encourage building operators and owners to upgrade their HVAC systems for efficient performance. The growing emphasis on building systems management and the critical need for maintaining optimal indoor air quality in commercial and institutional buildings have also contributed to the segment's market leadership.

Enterprise Asset Management Segment in North America Hard FM Market

The Enterprise Asset Management segment is projected to demonstrate substantial growth in the North American Hard Facility Management market from 2024 to 2029. This growth is primarily driven by the increasing adoption of IoT and AI/ML-based technologies for automating asset performance monitoring, particularly in the industrial landscape. The segment's expansion is supported by organizations' growing focus on optimizing asset lifecycle costs, improving performance reliability, and implementing strategic maintenance schedules. The integration of advanced technologies for predictive maintenance, coupled with the rising demand for asset tracking and monitoring solutions across various industries, particularly in the manufacturing and healthcare sectors, is expected to fuel the segment's growth trajectory during the forecast period.

Remaining Segments in North America Hard FM Market

Other hard FM services, including energy management, offshore FM, fire protection systems, access control systems, and structural maintenance systems, play a vital role in the market's ecosystem. These services are particularly crucial in supporting the region's transition towards sustainable operations and enhanced building security. The segment's significance is amplified by stringent safety regulations and the growing emphasis on energy efficiency in commercial and industrial facilities. The increasing focus on integrated security solutions and sustainable building operations continues to drive innovation and service expansion in these auxiliary but essential hard facility management services.

Segment Analysis: By End User

Commercial Segment in North America Hard Facility Management Market

The commercial segment dominates the North America Hard Facility Management market, holding approximately 32% market share in 2024, equivalent to USD 75.75 billion. This significant market position is primarily driven by the robust growth in commercial construction activities and the increasing adoption of advanced facility management solutions in office buildings, retail spaces, and corporate facilities. The segment's strength is further reinforced by the growing digitalization trends in commercial spaces, with businesses increasingly implementing smart building technologies and integrated facility management solutions. The demand is particularly strong in the United States and Canada, where commercial real estate development and modernization of existing commercial infrastructure continue to drive the need for comprehensive hard facility management services, including HVAC maintenance, electrical systems management, and building automation solutions.

Public/Infrastructure Segment in North America Hard Facility Management Market

The public/infrastructure segment is emerging as the fastest-growing segment in the North America Hard Facility Management market, with a projected growth rate of approximately 7% in Canada and 5% in the United States from 2024 to 2029. This accelerated growth is primarily driven by significant government investments in infrastructure development and modernization projects across both countries. The segment's growth is supported by an increasing focus on sustainable infrastructure development, smart city initiatives, and the modernization of public facilities. The implementation of advanced facility management solutions in government buildings, transportation hubs, and public utilities is creating substantial opportunities for service providers. The segment is witnessing increased adoption of energy-efficient solutions and smart building technologies, particularly in federal buildings and public infrastructure projects.

Remaining Segments in North America Hard Facility Management Market

The institutional, industrial, and other end-user segments collectively represent significant portions of the North America Hard Facility Management market, each serving distinct needs and requirements. The institutional segment, encompassing healthcare facilities and educational institutions, is characterized by its focus on specialized maintenance requirements and strict regulatory compliance. The industrial segment, serving manufacturing plants and industrial facilities, emphasizes operational efficiency and asset management services. The other end-users segment, which includes tourism and entertainment facilities, focuses on specialized maintenance requirements for unique infrastructure types. These segments are experiencing varying growth rates driven by sector-specific developments, technological advancements, and increasing focus on operational efficiency and sustainability.

North America Hard Facility Management Market Geography Segment Analysis

North America Hard Facility Management Market in the United States

The United States dominates the North American hard facility management landscape, commanding approximately 87% of the total market share in 2024. The country's prominence in the market is driven by its extensive commercial real estate sector, robust industrial infrastructure, and growing emphasis on building automation and energy efficiency. The market is particularly strong in MEP (Mechanical, Electrical, Plumbing) and HVAC maintenance services, reflecting the country's advanced technological infrastructure and stringent building maintenance requirements. The presence of major facility management service providers, coupled with increasing adoption of smart building technologies and IoT integration, has created a sophisticated ecosystem for hard facility management services. The market is further strengthened by significant investments in commercial construction, industrial facilities, and public infrastructure projects, particularly in major metropolitan areas. The growing focus on sustainable building operations and energy optimization has also catalyzed the demand for advanced facility management solutions, while the expansion of data centers and technology hubs continues to create new opportunities for service providers. Additionally, the integration of building services and property maintenance solutions is pivotal in enhancing the efficiency of physical asset management across the region.

North America Hard Facility Management Market in Canada

Canada represents a dynamic growth market in the North American hard facility management sector, with a projected CAGR of approximately 5% from 2024 to 2029. The country's market is characterized by increasing investments in infrastructure development, particularly in commercial and institutional sectors. The Canadian government's commitment to sustainable building practices and energy efficiency has created substantial opportunities for hard facility management service providers. The market is witnessing significant transformation through the adoption of advanced technologies and integrated facility management solutions, particularly in major urban centers like Toronto, Vancouver, and Montreal. The country's focus on clean energy initiatives and efficient energy management services has become a key driver for market growth, supported by stringent regulatory frameworks and sustainability goals. The industrial sector, particularly in manufacturing and natural resources, continues to generate substantial demand for specialized facility management services. Additionally, the healthcare and educational sectors are emerging as significant contributors to market growth, driven by ongoing infrastructure modernization efforts and the need for specialized maintenance services. The emphasis on building engineering and infrastructure management is crucial in supporting Canada's rapid market expansion.

North America Hard Facility Management Market in Other Markets

The North American hard facility management market primarily revolves around the United States and Canada, with these two nations forming the core of the regional market structure. Both countries demonstrate distinct market characteristics shaped by their unique economic landscapes, regulatory environments, and infrastructure development patterns. The integration of advanced technologies, sustainability initiatives, and energy efficiency measures remains a common thread across both markets. While the United States leads in terms of market size and technological adoption, Canada shows promising growth potential driven by infrastructure investments and sustainability initiatives. The market dynamics in both countries are influenced by similar trends, including the shift towards integrated facility management solutions, increasing focus on predictive maintenance, and the growing importance of energy management services. The competitive landscape across both markets is characterized by the presence of both global facility management companies and regional specialists, creating a robust service ecosystem that caters to diverse client needs across various sectors.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

Top Companies in North America Hard Facility Management Market

The North American hard facility management market features prominent players including Sodexo, Johnson Controls International PLC, Carrier Global Corporation, Jacobs Solutions Inc., AECOM, ARAMARK, CBRE Group Inc., Cushman & Wakefield PLC, Guardian Service Industries Inc., Jones Lang LaSalle Incorporated, and EMCOR Facilities Services Inc. These companies are actively pursuing technological innovation through the integration of IoT, AI, and smart building solutions to enhance their service offerings and operational efficiency. Market leaders are emphasizing sustainability and energy management solutions, particularly in HVAC and building automation systems. Companies are expanding their geographical presence through strategic acquisitions and partnerships, especially in emerging market segments. The industry witnesses continuous investment in digital capabilities, with firms developing proprietary platforms for asset management, preventive maintenance, and energy optimization. Additionally, there is a growing focus on providing integrated facility management solutions that combine both hard and soft services to meet evolving client demands.

Market Consolidation Drives Industry Evolution Pattern

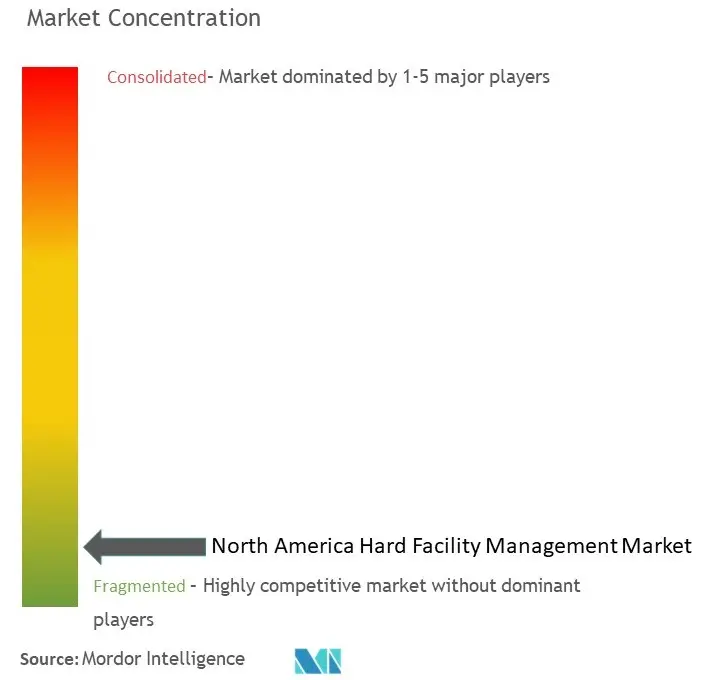

The North American hard facility management market exhibits a mix of global conglomerates and specialized regional players, with large multinational corporations holding significant market share through their comprehensive service portfolios and extensive geographical coverage. The market structure is characterized by ongoing consolidation through mergers and acquisitions, as larger players seek to expand their technical capabilities and regional presence by acquiring specialized service providers and technology firms. Companies are particularly targeting acquisitions that strengthen their digital transformation capabilities and enhance their sustainable facility management solutions portfolio.

The competitive landscape is evolving with increasing emphasis on strategic partnerships between facility management providers and technology companies, creating integrated service offerings that combine traditional hard FM services with advanced digital solutions. Market leaders are investing heavily in developing proprietary technologies and platforms, while regional players are focusing on specialized services and local market expertise. The industry also witnesses collaboration between competitors for large-scale projects, particularly in government and healthcare sectors, where comprehensive service capabilities are required.

Innovation and Integration Drive Future Success

Success in the North American hard facility management market increasingly depends on companies' ability to integrate advanced technologies while maintaining cost-effective service delivery. Market incumbents are focusing on developing comprehensive digital platforms that enable predictive maintenance, real-time monitoring, and energy optimization, while also expanding their sustainable facility management solutions. Companies are investing in workforce development and technical training to address the growing complexity of building systems and increasing demand for specialized maintenance services. The ability to provide integrated solutions that combine multiple service offerings while maintaining service quality and operational efficiency has become a critical differentiator.

For new entrants and smaller players, success lies in identifying and serving niche markets or specialized service segments while building strong local presence and expertise. Companies must navigate the increasing regulatory focus on environmental sustainability and energy efficiency, adapting their service offerings to meet evolving compliance requirements. The market shows moderate barriers to entry in basic services but high barriers in specialized technical services and integrated solutions. Customer relationships and service quality remain crucial factors, with clients increasingly seeking long-term partnerships with providers who can demonstrate consistent performance and innovation capabilities. The industry's future success will be determined by providers' ability to balance technological advancement with practical service delivery while maintaining strong client relationships.

North America Hard Facility Management Industry Leaders

Sodexo

Johnson Controls International PLC

Carrier Global Corporation

Jacobs Solutions Inc.

AECOM

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2023 - Carrier Global Corporation strategically acquired Viessmann Climate Solutions, marking a significant step in its Portfolio Transformation. This acquisition underscores Carrier Global Corporation's commitment to expanding its footprint in Intelligent Climate and Energy Solutions. This move aligns seamlessly with their market growth strategy, aimed at bolstering their market share in the realm of Hard FM services.

- July 2023: EMCOR Group, Inc., a prominent player in the industry, successfully acquired ECM Holding Group, Inc., a Wisconsin-based firm specializing in energy efficiency retrofit services. This strategic acquisition is set to fortify EMCOR's presence in the energy efficiency specialty services sector. It will also enhance the breadth of their nationwide portfolio, allowing them to offer a more comprehensive array of bundled energy conservation and sustainability solutions.

North America Hard Facility Management Market Report Scope

Hard facility management (HFM) services involve managing the people, technology, systems, and equipment that make up a company's physical structure.

The North American hard facility management market is segmented by type (MEP (mechanical, electrical, and plumbing), HVAC maintenance services, enterprise asset management, and other HFM services)) by end users (commercial, institutional, public/infrastructure, industrial, and other end-users), and geography (United States and Canada)

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Country

| United States | By Type | MEP (Mechanical, Electrical, Plumbing), and HVAC Maintenance services |

| Enterprise Asset Management | ||

| Other Hard FM Services | ||

| By End User | Commercial | |

| Institutional | ||

| Public/Infrastructure | ||

| Industrial | ||

| Other End Users | ||

| Canada | By Type | MEP (Mechanical, Electrical, Plumbing), and HVAC Maintenance services |

| Enterprise Asset Management | ||

| Other Hard FM Services | ||

| By End User | Commercial | |

| Institutional | ||

| Public/Infrastructure | ||

| Industrial | ||

| Other End Users | ||

| By Country | United States | By Type | MEP (Mechanical, Electrical, Plumbing), and HVAC Maintenance services |

| Enterprise Asset Management | |||

| Other Hard FM Services | |||

| By End User | Commercial | ||

| Institutional | |||

| Public/Infrastructure | |||

| Industrial | |||

| Other End Users | |||

| Canada | By Type | MEP (Mechanical, Electrical, Plumbing), and HVAC Maintenance services | |

| Enterprise Asset Management | |||

| Other Hard FM Services | |||

| By End User | Commercial | ||

| Institutional | |||

| Public/Infrastructure | |||

| Industrial | |||

| Other End Users | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current North America Hard Facility Management Market size?

The North America Hard Facility Management Market is projected to register a CAGR of 3.68% during the forecast period (2025-2030)

Who are the key players in North America Hard Facility Management Market?

Sodexo, Johnson Controls International PLC, Carrier Global Corporation, Jacobs Solutions Inc. and AECOM are the major companies operating in the North America Hard Facility Management Market.

What years does this North America Hard Facility Management Market cover?

The report covers the North America Hard Facility Management Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the North America Hard Facility Management Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.