Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

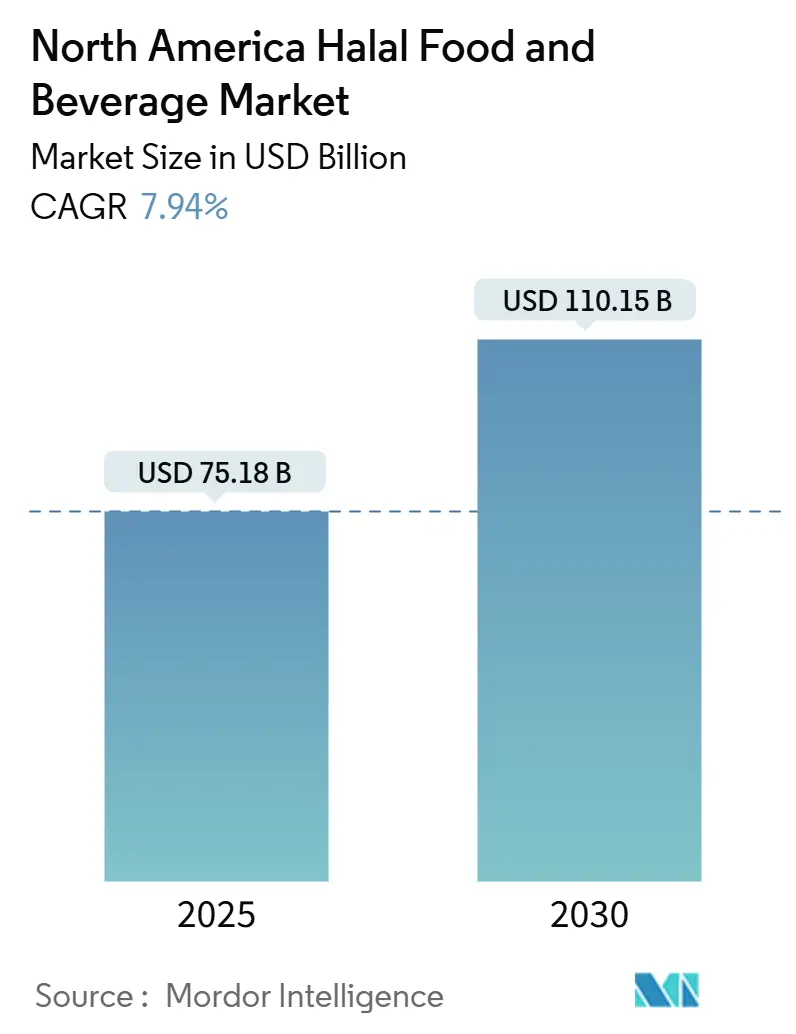

| Market Size (2025) | USD 75.18 Billion |

| Market Size (2030) | USD 110.15 Billion |

| Growth Rate (2025 - 2030) | 7.94% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Halal Food And Beverage Market Analysis by Mordor Intelligence

The North America halal food and beverage market size stands at USD 75.18 billion in 2025 and is projected to reach USD 110.15 billion by 2030, advancing at a 7.94% CAGR. Robust population growth in Muslim communities, a widening appeal among health-minded non-Muslim consumers, and retailer push into clean-label offerings keep demand on an upward slope. Mainstream supermarkets now place halal meat in prime refrigerated cases, while beverage players shift to halal-compliant enzymes, shortening reformulation cycles and accelerating product launches. At the policy level, the Canadian Food Inspection Agency’s labeling framework and the United States Department of Agriculture’s 2024 accreditation of several certifiers create a permissive if fragmented regulatory environment that manufacturers navigate for speed-to-market advantage. Online grocery platforms further expand reach into rural zip codes, effectively enlarging the North America halal food and beverage market beyond its traditional urban core.

Key Report Takeaways

- By product type, halal food commanded 81.28% of the North America halal food and beverage market share in 2024, while halal beverages are forecast to post the fastest growth at an 8.21% CAGR through 2030.

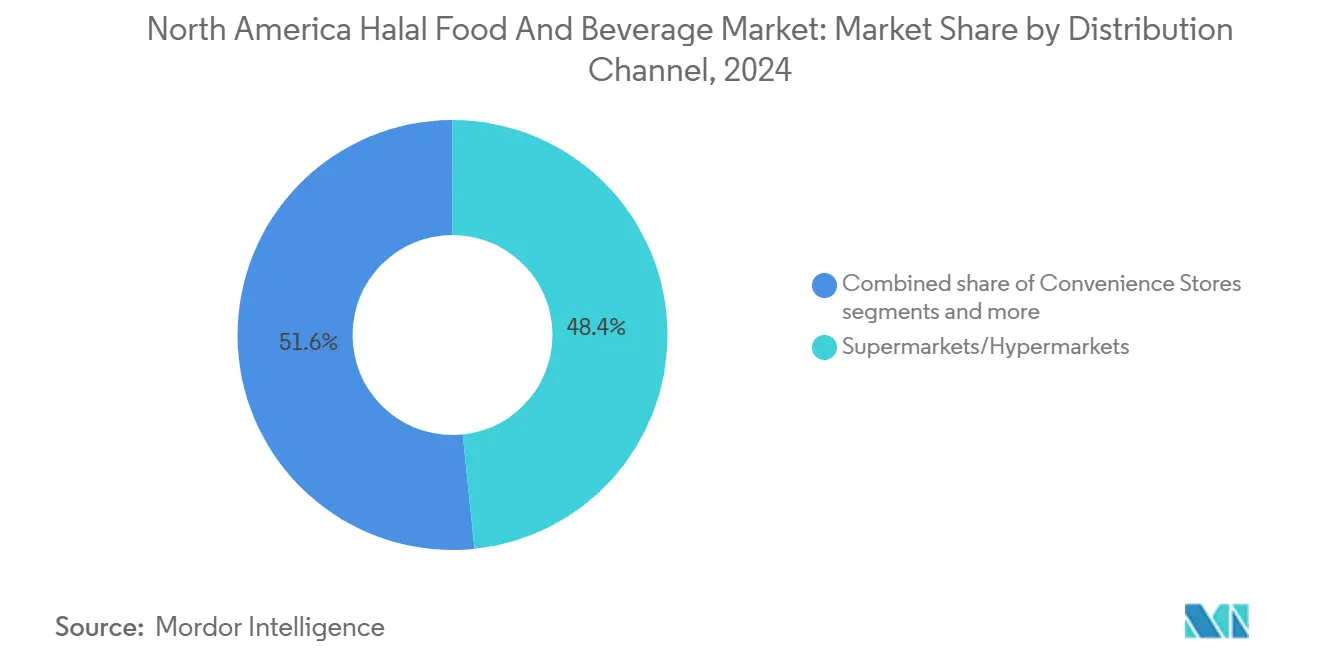

- By distribution channel, supermarkets and hypermarkets led with 48.36% revenue share in 2024; online retail stores are poised for the quickest expansion at an 8.78% CAGR to 2030.

- By geography, the United States held 75.41% of the North America halal food and beverage market size in 2024, whereas Mexico is set to record the highest CAGR at 8.05% between 2025 and 2030.

North America Halal Food And Beverage Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in tourism and expatriate communities demanding halal food | +1.8% | United States (major gateway cities), Canada (Toronto, Vancouver), Mexico (resort corridors) | Medium term (2-4 years) |

| Increasing number of halal food certifications and regulatory bodies | +1.2% | United States, Canada | Long term (≥ 4 years) |

| Growing awareness and demand for halal-certified products | +1.5% | North America-wide, with urban concentration | Medium term (2-4 years) |

| Rising health-conscious consumers preferring clean, ethically sourced foods | +0.9% | United States, Canada | Short term (≤ 2 years) |

| Rising demand for convenient, ready-to-eat halal meals | +1.1% | United States (major metros), Canada | Short term (≤ 2 years) |

| Expanding availability of halal products in mainstream grocery stores | +0.8% | United States, Canada, Mexico (urban centers) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in tourism and expatriate communities demanding Halal food

Surging tourism flows and the expansion of expatriate communities in major North American cities are significantly boosting demand for halal food and beverages, as travelers and migrants seek products aligned with Islamic dietary requirements across retail, foodservice, and hospitality channels. International Trade Administration data indicate that the United States welcomed 6,456,562 international visitors in December 2024, a 9.5% increase over the previous year[1]Source: International Trade Administration, "December and Annual 2024 Total International Travel Volume to and from the United States", trade.gov, highlighting the strengthening tourism base that underpins this demand. Growing inflows from Muslim-majority countries, combined with established expatriate clusters in hubs such as New York, Toronto, Houston, and Los Angeles, are encouraging airports, hotels, and quick-service restaurants to integrate halal-certified options into their menus. This expanding and increasingly affluent customer pool is prompting retailers and manufacturers to broaden halal assortments beyond meat into snacks, ready meals, dairy, and beverages, thereby accelerating the mainstreaming and growth of the halal food and beverage segment in North America.

Increasing number of Halal food certifications and regulatory bodies

Increasing number of halal food certifications and specialized regulatory bodies is a key driver of the North America halal food and beverage market. Independent halal certifiers, Islamic councils, and audit organizations are expanding their presence, standardizing requirements, and improving oversight. The proliferation of bodies such as the Islamic Food and Nutrition Council of America (IFANCA) in the U.S. and the Halal Monitoring Authority in Canada creates wider certification access and clearer signals of compliance for brands [2]Source: Islamic Food and Nutrition Council of America, "Halal for All", ifanca.org. This enhances consumer trust by reducing uncertainty around ingredient sources, slaughter methods, and processing standards. In turn, retailers and foodservice operators gain confidence to scale halal assortments and private-label offerings. At the same time, differing standards and logos can create some friction and complexity for multinational manufacturers navigating multiple schemes.

Growing awareness and demand for Halal-certified products

Growing awareness and demand for halal-certified products is a critical driver of the North America halal food and beverage market. Muslim consumers are increasingly seeking clear halal labeling to ensure products comply with religious dietary requirements, while non-Muslim shoppers perceive halal as a proxy for cleanliness, humane treatment, and stringent quality control. Retailers and foodservice operators are responding by expanding halal ranges across meat, packaged foods, snacks, and beverages, moving halal from ethnic aisles into mainstream shelves. Digital media, community organizations, and influencers are playing a key role in educating consumers about halal standards and available brands. This heightened visibility is encouraging national brands and private labels to pursue certification as a route to market differentiation. As awareness rises, halal demand is shifting from niche to mass, supporting premiumization, broader distribution, and sustained category growth across North America.

Rising health-conscious consumers preferring clean, ethically sourced foods

Rising health-conscious consumers preferring clean, ethically sourced foods are increasingly supporting growth in the North America halal food and beverage market. Many shoppers view halal standards such as controlled sourcing, specific slaughter practices, and restrictions on certain additives as aligned with broader concerns around animal welfare, product integrity, and traceability. This perception positions halal as overlapping with “better-for-you” and “ethical” food segments rather than only a religious requirement. As a result, halal-certified products are attracting interest from flexitarians and non-Muslim health-conscious consumers seeking minimally processed and transparently sourced options. Brands are responding by highlighting halal certification alongside claims such as organic, natural, and antibiotic-free on packaging and marketing. This convergence of health, ethics, and faith-driven preferences is expanding the consumer base for halal offerings and encouraging retailers to integrate them into mainstream assortments.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited consumer awareness in non-urban and emerging markets | -0.5% | Rural areas in South Asia, Sub-Saharan Africa, interior South America | Long term (≥ 4 years) |

| Perception of inferior taste or mouthfeel versus regular butter | -0.4% | Global, particularly among traditional dairy consumers in Europe and North America | Medium term (2-4 years) |

| Shorter shelf life due to processing sensitivities | -0.3% | Global, with acute impact in regions lacking cold-chain infrastructure (Africa, Southeast Asia) | Medium term (2-4 years) |

| Stringent food safety and labeling compliance burdens | -0.4% | Global, disproportionately affecting small and medium producers in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High cost of Halal certification for manufacturers

High cost of halal certification for manufacturers is a notable restraint in the North America halal food and beverage market. Certification involves recurring fees for audits, plant inspections, documentation reviews, and logo usage, which can be particularly burdensome for small and mid-sized processors. Additional operational expenses arise from segregated production lines, dedicated storage, and traceability systems needed to comply with halal standards. These costs can erode margins or force higher retail prices, limiting competitiveness against conventional products. Manufacturers with broad portfolios may also face complexity and expense in certifying multiple SKUs and facilities. In some cases, varying requirements across certifying bodies add further duplication of effort and cost. Consequently, certain companies delay or avoid entering the halal segment, constraining product availability and slowing overall market expansion.

Competition from conventional food and beverage products

Competition from conventional food and beverage products acts as a key restraint on the North America halal food and beverage market. Mainstream products typically benefit from wider brand recognition, entrenched shelf space, and aggressive pricing supported by economies of scale. Many retailers still prioritize fast-moving conventional SKUs, limiting visibility and assortment depth for halal alternatives. Price-sensitive consumers, including some Muslim shoppers, may opt for cheaper non-halal options when certified products carry a premium. In categories where halal benefits are not clearly communicated, non-halal brands can dominate through stronger marketing and promotions. This intense competition makes it harder for halal manufacturers to secure national listings and scale volumes. As a result, overall halal market penetration and growth are slower than the underlying demand potential.

Segment Analysis

By Product Type: Protein Dominates, Beverages Accelerate

Halal food accounted for the dominant share of 81.28% in North America’s halal food and beverage market in 2024, establishing the segment as the clear market leader. The category’s strength is primarily anchored by meat, poultry, and seafood products, which continue to represent the core of halal consumption across the region. This dominance is driven by strong consumer confidence in halal certification standards that emphasize hygiene, humane animal treatment, and perceived product freshness. The broad acceptance of halal meat products among both Muslim and non-Muslim consumers has further expanded the category’s reach across mainstream retail and foodservice channels. Additionally, increasing availability of ready-to-cook and frozen halal meat-based meals supports convenience-driven demand.

Halal beverages, meanwhile, represent the fastest-growing segment and are projected to record a compound annual growth rate (CAGR) of 8.21% between 2025 and 2030, surpassing the overall market pace. Growth in this category is largely fueled by the ease with which soft drinks, energy drinks, and functional beverages can be reformulated using halal-compliant ingredients such as enzymes, emulsifiers, and natural flavorings. Beverage manufacturers are increasingly aligning their product portfolios with halal certification standards to tap into a widening consumer base seeking transparency and ethical sourcing. The shift toward halal-certified functional drinks resonates strongly with health-conscious younger consumers, particularly within urban markets. Growing investments from global beverage companies in halal product innovation and certification programs are further accelerating the segment’s expansion.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: E-Commerce Disrupts Traditional Retail

Supermarkets and hypermarkets dominated the North America halal food and beverage distribution landscape in 2024, capturing 48.36% of the total market share. Their leadership stems from the convenience of one-stop shopping, extensive product assortments, and strong price competitiveness compared with smaller ethnic or specialty grocers. These large-format retailers have increasingly expanded their halal-certified product ranges to cater to both Muslim and non-Muslim consumers seeking quality and authenticity. Strategic partnerships with halal-certified suppliers have enabled consistent product availability and enhanced consumer trust in labeling and sourcing. Additionally, attractive promotional campaigns, store branding, and in-store education initiatives have further driven traffic within this channel.

Online retail stores, by contrast, are emerging as the fastest-growing distribution channel, projected to register a CAGR of 8.78% from 2025 to 2030. This rapid expansion is propelled by increasing digital adoption, the rise of e-grocery platforms such as Amazon Fresh, and the growth of specialized halal e-tailers catering to niche consumer groups. Online channels eliminate the geographic limitations of brick-and-mortar outlets, allowing consumers to access a broader range of halal-certified products irrespective of location. The convenience of home delivery, flexible payment options, and improved product verification systems further enhance consumer confidence in online purchases. Moreover, digital marketing initiatives and subscription-based delivery models are helping e-retailers build sustained engagement within younger, tech-savvy demographics.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The United States held the dominant position in North America’s halal food and beverage market in 2024, accounting for 75.41% of the total regional share. This leadership is supported by a sizable Muslim population exceeding 3.5 million [3]Source: National Alliance on Mental Illness, Muslim Americans, namimd.org, primarily concentrated in key metropolitan hubs such as New York, Los Angeles, Chicago, and Houston. The strong presence of halal-certified restaurants, food manufacturers, and retail outlets in these cities has further reinforced the country’s market position. Growing awareness of halal standards among mainstream consumers, coupled with a rising interest in ethical and clean-label products, has widened the appeal of halal offerings beyond the Muslim community. Moreover, major U.S. retailers and quick-service restaurant chains have increasingly incorporated halal-certified product lines and menus, reflecting expanding consumer diversity.

Mexico, meanwhile, is projected to register the fastest growth in the region, with a compound annual growth rate (CAGR) of 8.05% from 2025 to 2030. The country’s growth trajectory is fueled by rising tourism from Muslim-majority nations and a small but expanding Muslim expatriate population in Mexico City and high-traffic resort destinations such as Cancún and Los Cabos. Growing hospitality industry awareness of halal preferences has led to the gradual introduction of halal-certified food options in hotels and restaurants catering to international visitors. Additionally, import partnerships with Middle Eastern and Southeast Asian suppliers are facilitating the availability of compliant ingredients and processed foods. Government initiatives aimed at diversifying tourism and promoting inclusive dining experiences further support market development.

Canada represents another significant market within the region, characterized by a mature halal ecosystem and steady demand across major urban centers such as Toronto, Vancouver, and Montreal. The country’s multicultural demographic composition and supportive regulatory environment have encouraged widespread acceptance and availability of halal food and beverages. Local producers and importers benefit from clear certification standards, enabling consistent product labeling and consumer trust. Retail chains and foodservice operators are expanding halal offerings, catering to both domestic demand and export opportunities across North America.

Competitive Landscape

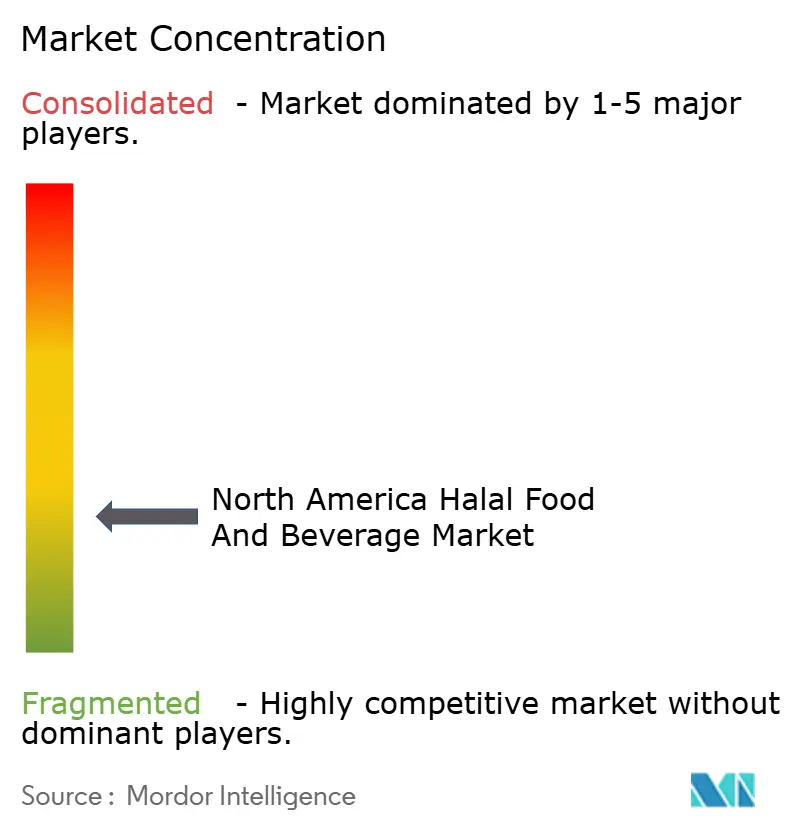

The North America halal food and beverage market is highly fragmented, characterized by the presence of numerous regional players, ethnic brands, and emerging startups competing alongside global food manufacturers. The competitive environment is shaped by diverse product portfolios, varying certification standards, and differences in supply chain integration. Large multinational companies such as Nestlé, Unilever, and PepsiCo have expanded their halal-certified offerings to leverage cross-regional demand, particularly in beverages, dairy, and packaged foods. Meanwhile, regional producers and specialty brands continue to dominate niche segments including halal meat, ready-to-eat meals, and bakery products. The coexistence of mainstream international corporations and community-focused enterprises contributes to a dynamic, competitive marketplace where brand credibility and certification authenticity are key differentiating factors.

Local and mid-sized companies play a critical role in shaping competition by offering culturally tailored products designed for diverse Muslim and non-Muslim consumer groups. These companies often emphasize traditional recipes, ethical sourcing, and traceability to strengthen brand loyalty within local markets. Strategic partnerships with halal certification bodies enhance transparency and help smaller brands gain consumer trust. Many operators are also adopting omnichannel retail models, including e-commerce distribution and direct-to-consumer sales, to reach geographically dispersed audiences. The ability to maintain price competitiveness while ensuring compliance with halal standards remains essential for sustaining market position.

The competitive landscape is further evolving as investment in product innovation and certification infrastructure intensifies across the region. Companies are focusing on reformulating existing product lines to meet halal certification requirements, while also developing new items in high-growth categories such as functional beverages, frozen meals, and confectionery. Mergers, acquisitions, and collaborations with certified suppliers are becoming more common as firms seek to streamline supply chains and expand portfolio reach. Additionally, the rise of private-label halal products in major retail chains adds another layer of complexity, increasing competition based on both pricing and branding.

North America Halal Food And Beverage Industry Leaders

-

American Foods Group, LLC

-

JBS S.A.

-

BRF S.A.

-

Crescent Foods, Inc.

-

Nestlé S.A.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2025: Maple Leaf Foods has launched Musafir, a new food brand that blends South Asian culinary traditions with modern convenience, addressing the growing consumer demand for global flavors and protein-rich foods. This launch reflects the Canadian food market's increasing embrace of diverse cuisines, particularly those inspired by the South Asian community, the country's fastest-growing visible minority.

- October 2024: Crescent Foods completed a comprehensive packaging rebrand emphasizing "no antibiotics ever" and "humanely raised" claims alongside halal certification, targeting health-conscious non-Muslim consumers. The rebrand coincided with expanded distribution into Costco, Walmart, Kroger, and H-E-B, positioning Crescent as a premium halal brand in mainstream retail.

- February 2024: Loblaws has entered into a partnership with Canadian halal meat brand Shahir to introduce halal deli meat slices across its stores in the Atlantic provinces, including Nova Scotia, New Brunswick, Prince Edward Island, and Newfoundland & Labrador. Shahir offers Canadian, hand‑slaughtered, CHFCA‑certified halal products that are also gluten-free, lactose-free, and free from artificial flavours, targeting Muslim consumers with both religious and health-driven needs.

North America Halal Food And Beverage Market Report Scope

Foods labeled "Halal" follow the dietary guidelines established by Islam and must go through a specific process from farm to package to be considered entirely halal.

The North American halal food and beverages market is segmented by product type, distribution channel, and geography. By geography, the market is segmented into halal food, halal beverages, and halal supplements. The halal food section is further divided into meat, dairy, bakery, confectionery, and other halal foods. By distribution channel, the market is segmented into supermarkets/hypermarkets, specialty stores, convenience/grocery stores, and other distribution channels. By geography, the market is segmented into the United States, Canada, Mexico, and the rest of North America.

For each segment, the market sizing and forecast have been done based on value (in USD million).

By Product Type

| Halal Food | Dairy and Dairy Alternatives |

| Confectionery | |

| Bakery Products | |

| Savory Snacks | |

| Baby Food | |

| Meat, Poultry and Seafood | |

| Ready Meals and Sauces | |

| Other Product Types | |

| Halal Beverages |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Country

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Halal Food | Dairy and Dairy Alternatives |

| Confectionery | ||

| Bakery Products | ||

| Savory Snacks | ||

| Baby Food | ||

| Meat, Poultry and Seafood | ||

| Ready Meals and Sauces | ||

| Other Product Types | ||

| Halal Beverages | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the North America halal food and beverage market?

The market is valued at USD 75.18 billion in 2025 and is projected to grow to USD 110.15 billion by 2030.

Which product category is growing fastest?

Halal beverages are forecast to expand at an 8.21% CAGR between 2025 and 2030, outpacing all other segments.

Why are mainstream retailers increasing halal offerings?

Clean-label positioning and rising non-Muslim interest make halal SKUs profitable additions to primary meat and dairy cases.

Which country will record the fastest growth through 2030?

Mexico is expected to grow at an 8.05% CAGR, driven by tourism and a nascent local production base.

What challenges do small processors face in halal certification?

Certification fees, segregated production lines, and ongoing audit costs can exceed USD 500,000 for mid-sized facilities.