Market Trends of North America Fuel Cell Technology Industry

This section covers the major market trends shaping the North America Fuel Cell Technology market according to our research experts:

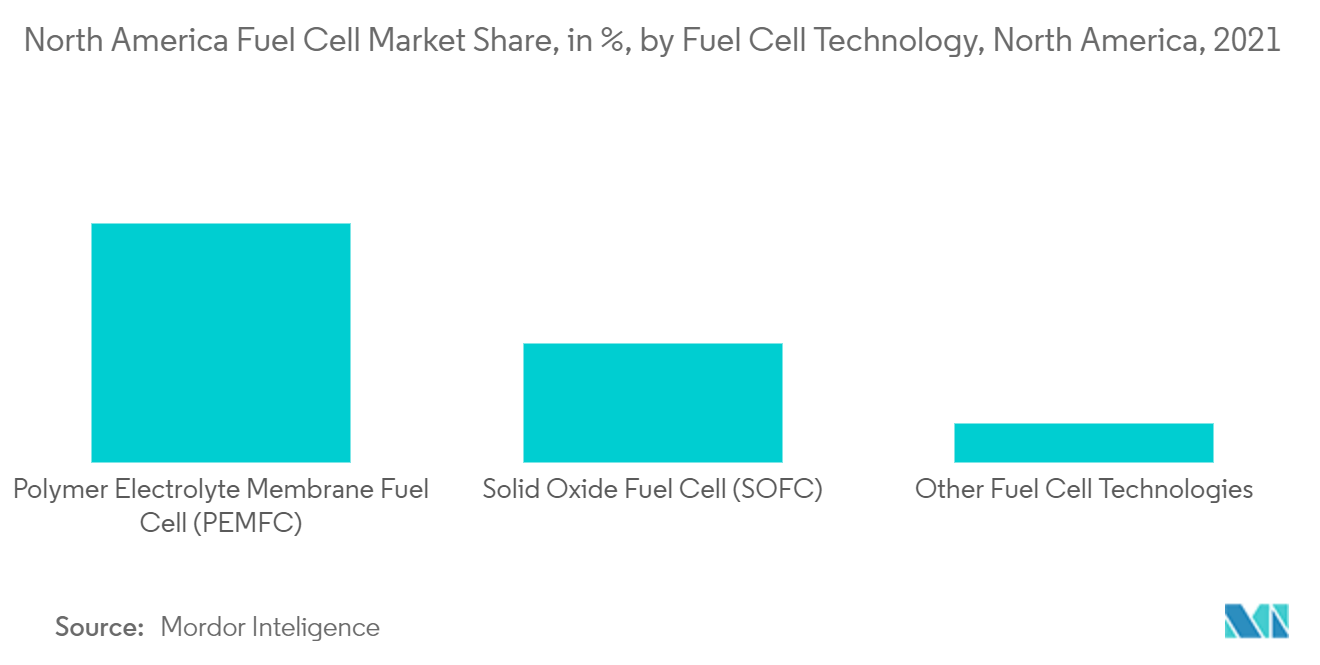

Polymer Electrolyte Membrane Fuel Cell (PEM) to Dominate the Market

- PEM fuel cell used for electrical power generation continues to dominate the stationary application, while household heat and power are nascent. During 2018, trucks and other heavy vehicles have increasingly started the significant application of PEM fuel cells.

- Among the various types of support materials, carbon black (Vulcan XC -72) has been widely used in PEM fuel cells due to its high electrical conductivity and specific area. However, it suffers from electro-oxidation under fuel cell operating conditions, resulting in the loss of catalytic activity after long-term operation.

- The North American region (primarily the United States) is one of the early adopters of the commercial-scale deployment of polymer electrolyte membrane (PEM)-based fuel cells. It was supported by government funding and had an increased uptake by end-users like the automobile industry.

- California Energy Commission's Alternative and Renewable Fuel and Vehicle Technology Program, a government initiative in 2013, established long-term plans to develop 100 retail hydrogen stations by 2021-22. This has encouraged the private sector to invest in the fuel cell market.

- As of 2021, around 11,956 fuel cells, including PEM fuel cells, powered light-duty vehicles were on the road in California. California has 115 retail hydrogen stations in development as of 2021.

- Therefore, development and government support are expected to drive the PEM fuel cell technology market in the region.

Understand The Key Trends Shaping This Market

Download PDF

United States is Expected to Drive the Market

- The United States leads the global fuel cell electric vehicle (FCEV) deployed worldwide, and as of 2021, there were more than 535.6 MW of fuel cell stationary power, serving more than 40 states in the United States.

- California leads the deployment, where the Zero Emission Vehicle Program has significantly supplemented FCEV sales and is expected to remain the same in the coming years.

- PEM remains the dominant chemistry for the transportation sector in the country, though both DMFC and SOFC variants of vehicle systems are under development. Automotive giants, such as Toyota and Hyundai, have ventured into PEM stack cell technology to reduce the overall production costs of FCEVs.

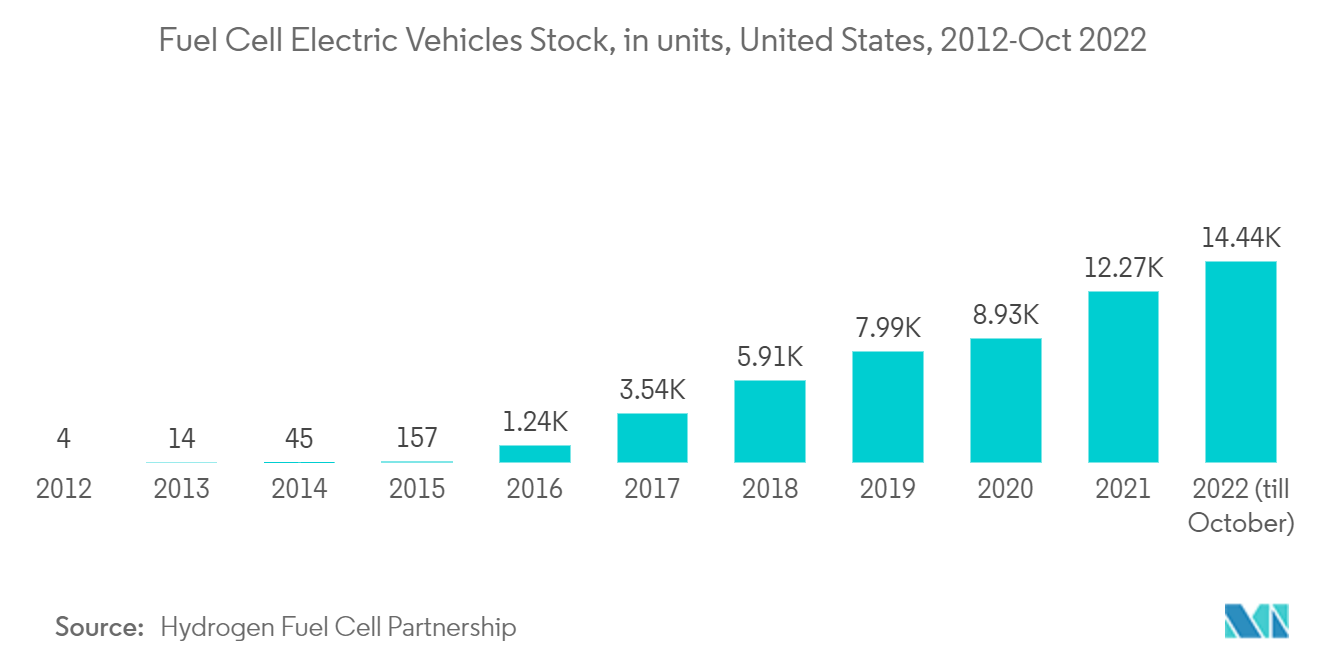

- Besides, more than 80% of the fuel cell systems deployed in the United States are expected to be for the transportation sector. The cumulative number of fuel-cell electric vehicles in the United States grew from 4 in 2012 to 14,435 in 2022 till October.

- In May 2022, Hyundai Motor Company emphasized its plan to ramp up the United States commercial vehicle market entry with XCIENT Fuel Cell trucks at the 2022 Advanced Clean Transportation (ACT) Expo.

- Such collaborative efforts by the government and industry players are expected to significantly reduce PEMFC and FCEVs' costs and, in turn, increase the demand for fuel cells in the country.

Get Analysis on Important Geographic Markets

Download PDF