Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 548.1 Million |

| Market Size (2030) | USD 610.7 Million |

| Growth Rate (2025 - 2030) | 2.18% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Frozen Desserts Market Analysis by Mordor Intelligence

The North America Frozen Desserts Market size is estimated at 548.1 million USD in 2025, and is expected to reach 610.7 million USD by 2030, growing at a CAGR of 2.18% during the forecast period (2025-2030).

The North American frozen desserts industry is experiencing significant transformation driven by evolving retail landscapes and changing consumer preferences. Traditional brick-and-mortar establishments continue to dominate the market, with supermarkets and hypermarkets accounting for approximately 66% of frozen dessert sales in the United States as of 2022. The retail infrastructure continues to expand, with Canada alone hosting over 8,000 supermarkets and hypermarkets in 2023. The convenience store sector has also witnessed remarkable growth, with the United States recording 150,174 operational stores as of January 2023, representing a 1.5% increase from the previous year. This extensive retail network has significantly enhanced product accessibility and consumer reach across the region.

Digital transformation is revolutionizing the frozen desserts market, driven by increasing smartphone penetration and evolving consumer shopping behaviors. In 2022, approximately 95% of the Gen Z population used smartphones, with an average daily usage of 10 hours, facilitating the growth of mobile commerce. Major brands have strategically partnered with prominent online retailers, including Instacart, Amazon Fresh, Walmart, Kroger, and Shipt, to enhance consumer convenience. The digital transformation has particularly resonated with Canadian consumers, where surveys indicate that 22% of consumers now regularly plan their grocery purchases through online channels.

The industry is witnessing a significant shift towards product premiumization and price diversification to cater to various consumer segments. Manufacturers have implemented strategic pricing models, with products ranging from an accessible base price of USD 2.45 to premium offerings at USD 130, ensuring market penetration across different consumer segments. This pricing strategy has been complemented by the introduction of innovative flavors, clean-label products, and healthier variants, particularly targeting health-conscious consumers seeking low-calorie and low-fat alternatives. Notably, the demand for ice cream and other frozen dairy products is on the rise as consumers seek indulgent yet healthier frozen treats.

Distribution networks have evolved to become more sophisticated and consumer-centric, with retailers implementing advanced cold chain solutions and last-mile delivery capabilities. Major retail chains have invested significantly in upgrading their frozen food sections with modern freezers and appealing product displays, enhancing the shopping experience. The integration of artificial intelligence and chatbot features in online retail platforms has further streamlined the purchasing process, while the implementation of sustainable packaging solutions reflects the industry's commitment to environmental responsibility. These advancements in distribution and retail technology have collectively contributed to improved product accessibility and consumer satisfaction.

North America Frozen Desserts Market Trends and Insights

The consumption of milk and dairy products is influenced by factors such as population growth, changing dietary preferences, and economic conditions, leading to variations in milk consumption patterns over time

- In 2020, the output of raw milk grew by 2.15%. In 2021, the growth rate of raw milk production was 3.4% higher than in 2019. The US Department of Agriculture (USDA) states that the demand for ice cream continued to rebound and grew by 4% Y-o-Y in 2020. In November 2021, milk production in the United States totaled 18.0 billion pounds, down by 0.4% from November 2020. The number of milk cows on US farms was 9.39 million heads, 47,000 less than in November 2020. Production per cow in the United States averaged 1,922 pounds in November 2021, three pounds above November 2020 and 10,000 heads lesser than in October 2021.

- In 2019, the consistency of raw milk production saw a modest increase as raw milk output experienced a minimal increase of 0.36% compared to 2018. The declining raw milk production was due to the closure of milk manufacturing facilities in the area and associated macroeconomic factors like rising milk demand but falling milk prices.

- When the statistics are compared to 2016, the growth rate of milk production in North America increased by 1.83% in 2019. In the United States, big farms managed 55.2% of all herds, and the number of milking cows increased to 1,953 heads. Such substantial dairy enterprises were increasingly found throughout the region's West, Southwest, and Upper Midwest. Similarly, the region gained 1.10% momentum in 2018. The average number of milking cows was 9.41 million heads in 2018, up by 40,000 heads over the previous year. The amount of milk produced per cow reached a record-high 5,781 pounds in 2018.

Understand The Key Trends Shaping This Market

Download PDF

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- The rising number of milking cows in the country is largely driving the production of raw milk in North America

Segment Analysis: Distribution Channel

Off-trade Segment in North American Frozen Desserts Market

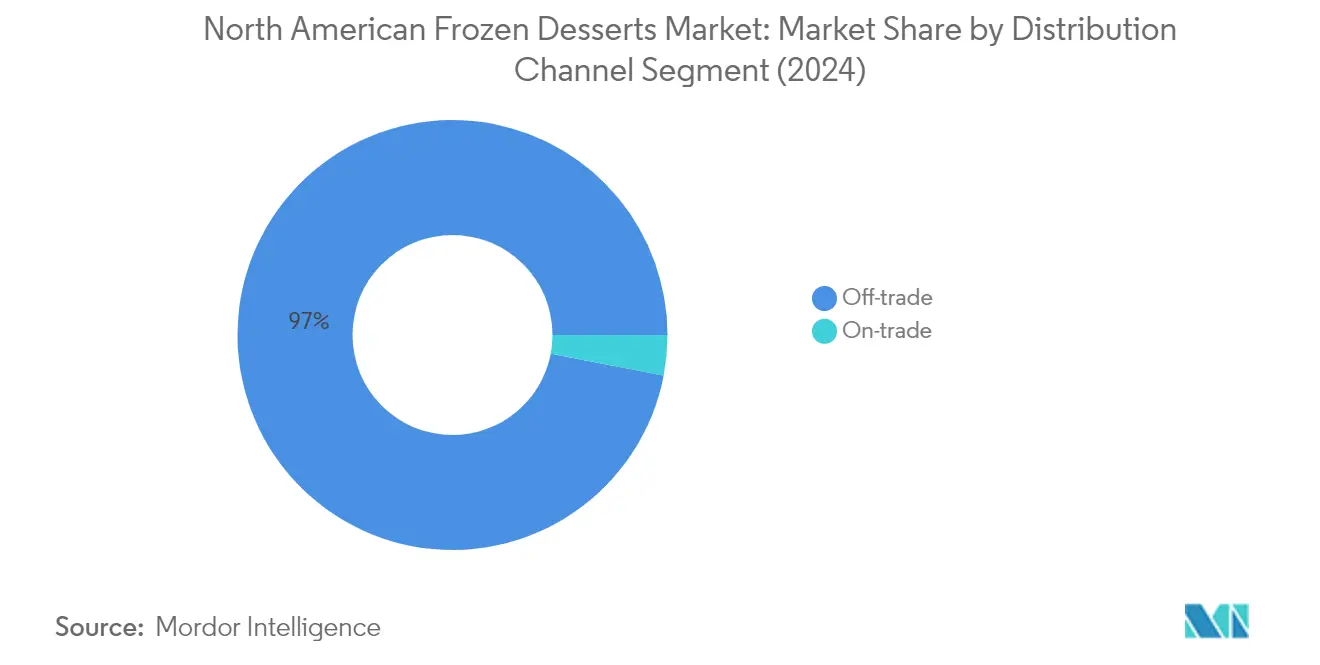

The off-trade segment dominates the North American frozen desserts market, accounting for approximately 97% of the total market share in 2024. This substantial market presence is primarily driven by hypermarkets and supermarkets, which have consistently maintained a strong lead in frozen dessert sales. The proximity factor of these channels, especially in large and developed cities, gives them the added advantage of influencing consumer decisions through a wide variety of product offerings. Supermarkets and hypermarkets account for nearly 66% of frozen dessert sales in terms of value in the United States. The segment is projected to maintain its dominant position and demonstrate strong growth with an expected CAGR of around 2% during 2024-2029. This growth trajectory is supported by the increasing investment by modern grocery stores in online delivery infrastructure, responding to evolving consumer purchasing behaviors. Major brands have strengthened their presence through partnerships with online retailers, including Instacart, Amazon Fresh, Walmart, Kroger, Shipt, Thrive Market, Whole Foods, and FreshDirect, offering popular brands like Van Leeuwen, Great Value, Edwards, and Marie Callender's.

On-trade Segment in North American Frozen Desserts Market

The on-trade segment represents a smaller but significant channel in the North American frozen desserts market, focusing on out-of-home consumption patterns. This segment has been experiencing notable transformation as consumers increasingly shift toward healthier variants featuring reduced or no sugar content. About eight out of every ten US adults intentionally avoid or reduce sugar in their diets, with 16% stating sugar reduction as their primary dietary goal. This trend has created new opportunities for healthier variants of frozen treats across on-trade channels. Popular frozen desserts preferred by US consumers within on-trade channels include fried ice cream, frozen custard, brownie sundaes, ice cream cakes, and ice cream sandwiches. Consumer preferences are significantly influenced by the flavors and nutritional value offered by these products. The segment's growth is further supported by increasing consumer spending on out-of-home food consumption, with food consumed away from home accounting for 55% of total food expenditure.

North America Frozen Desserts Market Geography Segment Analysis

Frozen Desserts Market in United States

The United States dominates the North American frozen desserts landscape, commanding approximately 84% of the market value in 2024. The market is projected to grow at nearly 2% CAGR from 2024 to 2029, positioning it as the fastest-growing country in the region. This robust growth is driven by the increasing consumer preference for premium and innovative frozen dessert products. The trend of healthier living is significantly influencing product development, with manufacturers focusing on natural, organic, and clean-label offerings. The popularity of snacking at home has expanded to the ice cream and frozen dessert sections, particularly in novelty items, with 32% of baby boomers and over 44% of millennials preferring to snack at home. The market's strength is further reinforced by the presence of numerous companies offering gelato and ice cream, with the sector projected to include 9,476 businesses. The millennial generation's growing demand for frozen snacks continues to be a significant driver, especially in the consumption of chilled snacks including yogurt, ice cream, and pudding.

Frozen Desserts Market in Canada

Canada's frozen desserts market demonstrates strong potential, supported by evolving consumer preferences and expanding retail infrastructure. The market is characterized by increasing consumer inclination toward away-from-home snacking and experimental food choices. Ontario and Quebec host the majority of Canada's ice cream and frozen dessert manufacturing facilities, with Ontario alone housing 49 ice cream and frozen dessert production facilities out of 76 frozen food manufacturing facilities. The convenience store segment maintains its position as the second most preferred channel for frozen dessert purchases, benefiting from the fact that seven out of ten Canadians live less than 500 meters from a convenience store. The country's retail landscape is evolving with modern grocery stores investing significantly in online delivery infrastructure. Consumer preferences are increasingly influenced by health consciousness, with retailers offering products at varied price points to cater to different market segments. The market's growth is further supported by the presence of over 25,000 convenience stores and major retail chains providing diverse frozen dessert options.

Frozen Desserts Market in Mexico

Mexico's frozen desserts market exhibits significant potential, characterized by a robust manufacturing base and expanding retail infrastructure. The market structure is notably diverse, with 80% of businesses being small and medium-sized enterprises (SMEs), fostering continuous expansion and industry training. The consolidation of modern retailers, particularly the explosive rise of convenience stores, has been instrumental in driving frozen dessert sales. These modern retailers are better equipped with freezers and more appealing frozen product displays, providing consumers with expanded choices and improved accessibility. The market's growth is supported by the significant investment in processed food and retail industries, leading to steady increases in demand for dairy goods, including dairy components, fluid milk, and frozen desserts. Supermarkets and hypermarkets serve as the primary distribution channel, with major chains like Walmart, Soriana, Chedraui, and La Comer leading the market. The growing availability of different types and variants of ready-to-eat dairy desserts across retail outlets continues to drive market expansion.

Frozen Desserts Market in Other Countries

The frozen desserts market in other North American countries demonstrates dynamic growth potential, driven by evolving consumer preferences and retail modernization. These markets are characterized by increasing consumer sophistication and growing demand for premium frozen dessert products. The retail landscape in these regions continues to evolve, with modern trade formats gaining prominence and offering wider product varieties. Consumer preferences are increasingly influenced by global trends, with a growing emphasis on health-conscious and innovative offerings. The expansion of convenience store networks and modern retail formats has significantly improved product accessibility. Countries like Guatemala have shown particular promise in the frozen desserts category, with supermarkets, discount retailers, and convenience stores emerging as key marketing channels. The market dynamics in these regions are shaped by the increasing presence of international brands and the growing popularity of various frozen dessert formats, from traditional ice creams to innovative frozen treats.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

Top Companies in North American Frozen Desserts Market

The frozen desserts market in North America is characterized by continuous product innovation and strategic expansion initiatives by leading players. Companies are focusing on developing healthier variants, including low-calorie, sugar-free, and clean-label products to meet evolving consumer preferences. Operational agility is demonstrated through investments in manufacturing capabilities, with companies upgrading facilities and adopting sustainable practices in production and packaging. Strategic moves predominantly involve partnerships with online retailers and foodservice establishments to enhance distribution networks. Market leaders are expanding their presence through acquisitions of regional players and the establishment of new production facilities, while simultaneously investing in research and development to introduce innovative flavors and formulations. The industry also witnesses significant emphasis on sustainability initiatives, with companies adopting eco-friendly packaging solutions and implementing waste reduction programs.

Fragmented Market with Strong Regional Players

The North American frozen desserts market exhibits a fragmented structure with a mix of global conglomerates and regional specialists competing for market share. Major multinational companies like Dairy Farmers of America, Froneri International, and Unilever maintain a significant presence through their established brands and extensive distribution networks. Regional players leverage their local market knowledge and specialized product offerings to maintain competitive positions in specific geographic areas. The market is characterized by strong family-owned businesses and medium-sized enterprises that focus on premium and artisanal frozen desserts.

The industry has witnessed considerable merger and acquisition activity, primarily driven by larger companies seeking to expand their product portfolios and geographic reach. Companies are actively pursuing strategic acquisitions to strengthen their manufacturing capabilities and gain access to new distribution channels. Vertical integration strategies are becoming increasingly common, with companies acquiring suppliers and distribution networks to enhance operational efficiency. The market also sees the emergence of specialized players focusing on specific product categories such as frozen dairy products and premium artisanal desserts, contributing to the competitive dynamics.

Innovation and Distribution Key to Growth

Success in the North American frozen desserts market increasingly depends on companies' ability to innovate while maintaining efficient distribution networks. Market leaders are strengthening their positions through investments in product development, focusing on clean-label ingredients and health-conscious formulations. Companies are also expanding their presence in the e-commerce channel and establishing partnerships with major retailers to enhance market penetration. The development of strong cold chain logistics capabilities and strategic placement of distribution centers has become crucial for maintaining market share. Successful players are those who can effectively balance premium positioning with competitive pricing while maintaining product quality and innovation.

For new entrants and smaller players, success lies in identifying and serving niche market segments with specialized products. Companies need to focus on developing unique value propositions through product differentiation and innovative marketing strategies. Building strong relationships with retailers and investing in direct-to-consumer channels are becoming increasingly important for market success. The ability to adapt to changing consumer preferences and regulatory requirements, particularly regarding labeling and ingredient transparency, will be crucial for sustained growth. Companies must also consider potential challenges from substitute products and maintain flexibility in their operational strategies to respond to market changes effectively.

North America Frozen Desserts Industry Leaders

-

Dairy Farmers of America Inc.

-

Froneri International Limited

-

HP Hood LLC

-

Unilever PLC

-

Walmart Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2022: Kemps replaced Dean Goods throughout Iowa as Dairy Farmers of America completed the USD 433 million acquisition of Dean Foods properties. The business took over the Le Mars milk factory, which can process numerous Kemps products, from cottage cheese to ice cream.

- August 2022: Dairy Farmers of America acquired two shelf-extended facilities of SmithFoods. The strategy of this acquisition was to assist the corporation in capitalizing on the market's growing demand for products with extended shelf lives.

- April 2022: Haagen-Dazs unveiled its new shop design with the grand opening of its location in Walnut Creek, California.

North America Frozen Desserts Market Report Scope

Off-Trade, On-Trade are covered as segments by Distribution Channel. Canada, Mexico, United States are covered as segments by Country.

Distribution Channel

| Off-Trade | By Sub Distribution Channels | Convenience Stores |

| Online Retail | ||

| Specialist Retailers | ||

| Supermarkets and Hypermarkets | ||

| Others (Warehouse clubs, gas stations, etc.) | ||

| On-Trade |

Country

| Canada |

| Mexico |

| United States |

| Rest of North America |

| Distribution Channel | Off-Trade | By Sub Distribution Channels | Convenience Stores |

| Online Retail | |||

| Specialist Retailers | |||

| Supermarkets and Hypermarkets | |||

| Others (Warehouse clubs, gas stations, etc.) | |||

| On-Trade | |||

| Country | Canada | ||

| Mexico | |||

| United States | |||

| Rest of North America |

Need A Different Region or Segment?

Customize Now

Market Definition

- Butter - Butter is a yellow-to-white solid emulsion of fat globules, water, and inorganic salts produced by churning the cream from cows’ milk

- Dairy - Dairy product include milk and any of the foods made from milk, including butter, cheese, ice cream, yogurt, and condensed and dried milk.

- Frozen Desserts - Frozen dairy dessert means and includes products containing milk or cream and other ingredients which are frozen or semi-frozen prior to consumption, such as ice milk or sherbet, including frozen dairy desserts for special dietary purposes, and sorbet

- Sour Milk Drinks - Sour milk is thick, curdled milk, with a sour taste, obtained from the fermentation of milk. Sour milk drinks such as kefir, laban, buttermilk have been considered in the study

| Keyword | Definition |

|---|---|

| Cultured Butter | Cultured butter is prepared by having the raw butter go through chemical processing and has been added with certain emulsifiers and foreign ingredients. |

| Uncultured Butter | This type of butter is one which has not been processed in any way |

| Natural Cheese | The type of cheese in its most natural form. It is made from natural and simple products and ingredients, including fresh and natural salts, natural colors, enzymes, and high-quality milk. |

| Processed Cheese | Processed cheese undergoes the same processes as natural cheese; however, it requires more steps and many different forms of ingredients. Making processed cheese involves melting natural cheese, emulsifying it, and adding preservatives and other artificial ingredients or colorings. |

| Single Cream | Single cream contains around 18% fat. It’s a single layer of cream that appears over boiled milk. |

| Double Cream | Double cream contains 48% fat, more than double the amount of fat of single cream. It’s heavier and thicker than single cream |

| Whipping Cream | This has a much higher fat percentage than single cream (36%). Used to top cakes, pies, and puddings and as a thickener for sauces, soups, and fillings. |

| Frozen Desserts | Desserts that are meant to be eaten in frozen condition. E.g., sherbets, sorbets, frozen yogurts |

| UHT Milk (Ultra-high temperature milk) | Milk heated at a very high temperature. Ultra-high-temperature processing (UHT) of milk involves heating for 1–8 sec at 135–154°C. which kills the spore-forming pathogenic microorganism, resulting in a product with a shelf-life of several months. |

| Non-dairy butter/Plant-based butter | Butter made from plant-derived oil such as coconut, palm, etc. |

| Non-dairy Yogurt | Yogurt made from typically made from nuts, like almonds, cashews, coconuts, and even other foods like soybeans, plantains, oats, and peas |

| On-trade | It refers to restaurants, QSRs, and bars. |

| Off-trade | It refers to supermarkets, hypermarkets, on-line channels, etc. |

| Neufchatel cheese | One of the oldest kinds of cheese in France. It is a soft, slightly crumbly, mold-ripened, bloomy-rind cheese made in the Neufchâtel-en-Bray region of Normandy. |

| Flexitarian | It refers to a consumer preferring a semi-vegetarian diet, that is centered on plant foods with limited or occasional inclusion of meat. |

| Lactose Intolerance | Lactose intolerance is a reaction in digestive system to lactose, the sugar in milk. It causes uncomfortable symptoms in response to the consumption of dairy products. |

| Cream Cheese | Cream cheese is a soft and creamy fresh cheese with a tangy taste made from milk and cream. |

| Sorbets | Sorbet is a frozen dessert made using ice combined with fruit juice, fruit purée, or other ingredients, such as wine, liqueur, or honey. |

| Sherbet | Sherbet is a sweetened frozen dessert made with fruit and some sort of dairy product such as milk or cream. |

| Shelf stable | Foods that can be safely stored at room temperature, or "on the shelf," for at least one year and do not have to be cooked or refrigerated to eat safely. |

| DSD | Direct Store Delivery is the process in supply chain management wherein the product is delivered from manufacturing plant directly to the retailer. |

| OU Kosher | Orthodox Union Kosher is a kosher certification agency based in New York City. |

| Gelato | Gelato is a frozen creamy dessert made with milk, heavy cream and sugar. |

| Grass-fed Cows | Grass-fed cows are allowed to graze in pastures, where they eat a variety of grasses and clover. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF