Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 5.7 Billion |

| Market Size (2031) | USD 7.12 Billion |

| Growth Rate (2026 - 2031) | 4.54% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Food Flavor Market Analysis by Mordor Intelligence

The North America food flavor market is expected to grow from USD 5.45 billion in 2025 to USD 5.70 billion in 2026 and is forecast to reach USD 7.12 billion by 2031 at 4.54% CAGR over 2026-2031. This steady rise shows how consumer migration toward natural ingredients, AI-enabled formulation tools, and increasing label scrutiny are reshaping purchasing priorities. Synthetic products, while still dominant, face tightening regulation and slowing adoption, whereas natural variants gain momentum through shorter approval cycles and widening clean-label demand. Beverage manufacturers anchor volume because liquid matrices carry complex flavor payloads, yet savory snack makers spark incremental growth through ethnic and heat-forward profiles. Across the value chain, supply security for botanical extracts, new encapsulation methods, and cross-border trade optimization under USMCA create additive tailwinds. As a result, the North American food flavors market is transitioning from maturation to innovation-led expansion.

Key Report Takeaways

- By type, synthetic flavoring retained 54.21% of the North America food flavor market share in 2025, while natural flavoring is on track for a 5.76% CAGR through 2031.

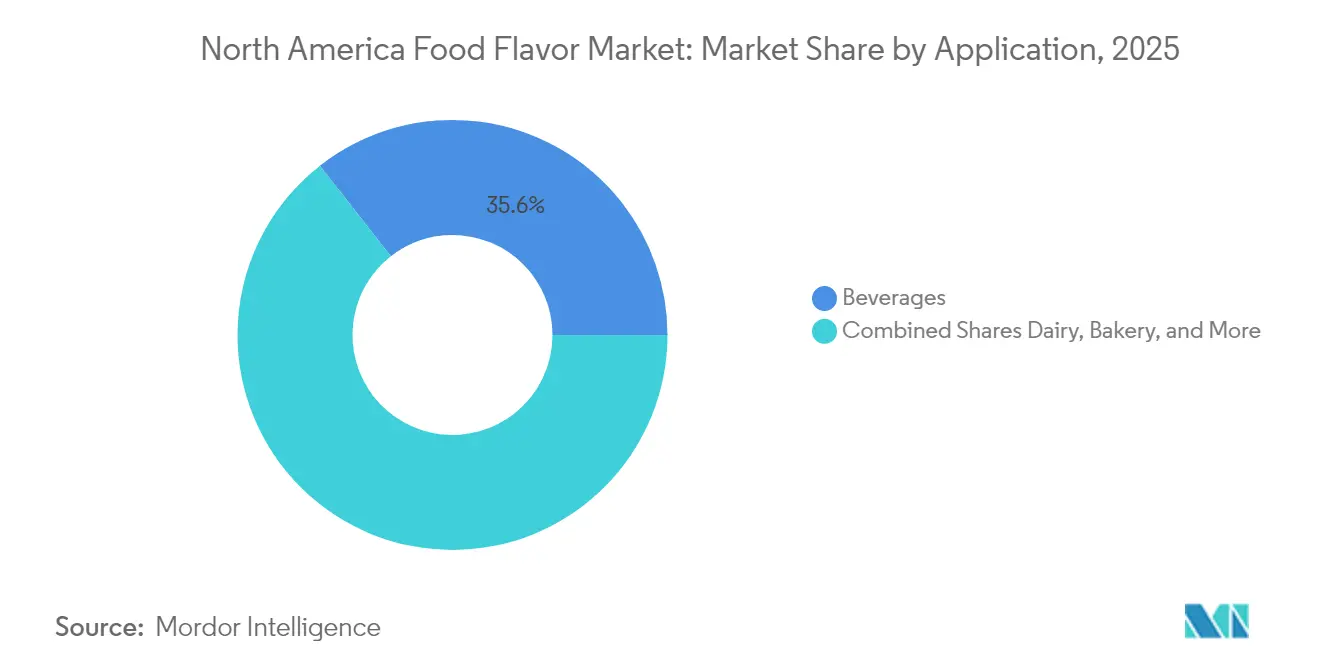

- By application, beverages commanded 35.57% of the North America food flavor market share in 2025, and savory snacks are advancing at a 6.24% CAGR to 2031.

- By geography, the United States accounted for a 72.16% share in the North America food flavor market during 2025, whereas Mexico is forecast to expand at a 5.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Food Flavor Market Trends and Insights

Driver Impact Analysis

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for natural and clean-label ingredients | +1.2% | North America, with strongest adoption in United States and Canada | Medium term (2-4 years) |

| Growth of functional foods, beverages, and wellness products | +0.8% | US-led, expanding to Mexico through multinational brands | Long term (≥ 4 years) |

| Expansion of processed food and beverage industry | +0.7% | Regional, with Mexico showing highest growth rates | Medium term (2-4 years) |

| Growing interest in vegan and cruelty-free ingredients | +0.6% | US and Canada urban centers, limited Mexico penetration | Long term (≥ 4 years) |

| Technological advances in flavor encapsulation and modulation | +0.4% | North America manufacturing hubs, Research and Development concentrated in United States | Short term (≤ 2 years) |

| AI-driven flavor development and innovation | +0.3% | Global, with North American companies leading implementation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Rising Demand for Natural and Clean-Label Ingredients

Consumer preference shifts toward natural flavoring accelerate as regulatory pressure mounts against synthetic additives. FDA's[1]U.S Food and Drug Administration, "Substances Added to Food (formerly EAFUS)", fda.gov announcement of Red 3 prohibition by January 2027 exemplifies this trend, forcing manufacturers to reformulate products with natural alternatives. Clean-label positioning becomes a competitive necessity rather than premium differentiation, with major food manufacturers investing heavily in natural flavor sourcing and processing capabilities. This transition creates supply-demand imbalances for key botanical extracts, driving price premiums that smaller manufacturers struggle to absorb. The regulatory momentum suggests similar restrictions on other synthetic additives will follow, making natural ingredient procurement a strategic imperative for sustained market access.

Expansion of Processed Food and Beverage Industry

In North America, particularly in Mexico, the processed food sector is witnessing significant growth, which is driving an increased demand for cost-effective flavoring solutions. The USMCA trade agreement plays a pivotal role in supporting Mexico's food processing industry by reducing tariff barriers for ingredient imports from the United States and Canada. This reduction facilitates the incorporation of more sophisticated and diverse flavor profiles into products that were traditionally simpler in nature. Flavor companies with well-established supply chains and regulatory approvals across the three countries are well-positioned to capitalize on this geographic expansion. Additionally, the growing trend of premiumization in Mexican food products is accelerating the adoption of more intricate and complex flavor systems. This evolving market dynamic creates substantial opportunities for mid-tier flavor houses to establish strategic regional partnerships and expand their presence in the region.

Growth of Functional Foods, Beverages, and Wellness Products

As manufacturers work to harmonize taste appeal with health-focused positioning, innovation in functional beverages is driving the development of increasingly complex flavor profiles. The integration of nutraceutical ingredients with advanced flavor systems introduces significant technical challenges, which tend to favor companies that possess sophisticated encapsulation technologies and extensive regulatory expertise. Consumers' willingness to pay a premium for products offering functional health benefits has created opportunities for high-value flavor applications, particularly in emerging categories such as adaptogenic beverages and protein-fortified snacks. This trend is pushing flavor houses to intensify their R&D efforts, focusing on the development of masking technologies to address the bitterness of bioactive compounds. Companies that successfully resolve the trade-offs between taste and health benefits are establishing strong competitive advantages in the market.

Growing Interest in Vegan and Cruelty-Free Ingredients

To replicate the taste profiles of animal-derived foods, innovation in plant-based foods increasingly relies on advanced flavoring techniques. This shift has significantly boosted the demand for specialized compounds designed to mimic umami and fat characteristics, which are essential for achieving the desired taste and mouthfeel. The technical complexity involved in developing plant-based meat and dairy alternatives creates substantial opportunities for flavor companies with expertise in protein interactions and the seamless integration of texture and flavor. For consumers, the authenticity of flavor remains a critical factor influencing their acceptance of plant-based products. As a result, the development of authentic and appealing taste profiles has become a fundamental success driver for manufacturers in the alternative protein market. This growing trend particularly benefits flavor houses that possess strong research and development (R&D) capabilities and maintain strategic partnerships with ingredient suppliers focused on creating innovative plant protein solutions.

Restraint Impact Analysis

| Restraints | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in prices and availability of key raw materials | -0.9% | North America, with agricultural regions most affected | Short term (≤ 2 years) |

| Stringent regulatory and customer-specific compliance requirements | -0.6% | US and Canada primarily, Mexico catching up | Medium term (2-4 years) |

| Supply chain disruptions and logistic constraints | -0.5% | Regional, with cross-border trade most vulnerable | Short term (≤ 2 years) |

| Rising health concerns over the use of artificial additives | -0.4% | Consumer-driven across North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Prices and Availability of Key Raw Materials

Natural flavor costs are heavily influenced by fluctuations in agricultural commodity prices. Vanilla, citrus oils, and spice extracts, in particular, have experienced significant price volatility, primarily due to climate disruptions and geopolitical tensions. The concentration of essential flavor raw materials in specific geographic regions exacerbates supply chain vulnerabilities, making it difficult for manufacturers to implement effective hedging strategies. For instance, recent drought conditions in Mexico and extreme weather events across North America have disrupted established sourcing patterns. These disruptions have compelled flavor companies to adopt more diversified supplier networks to mitigate risks, as noted by the USDA[2]U.S. Department of Agriculture, “Press Releases,” usda.gov. However, this volatility disproportionately impacts smaller flavor houses, which often lack the procurement scale, financial resources, and capacity to maintain adequate strategic inventory levels, leaving them more exposed to supply chain challenges.

Stringent Regulatory and Customer-Specific Compliance Requirements

As Health Canada[3]Government of Canada, “Food Additives,” canada.ca and the FDA implement stricter regulations on food additive oversight, the regulatory environment becomes increasingly intricate. The approval process for new flavor compounds now requires comprehensive documentation and extensive testing to meet compliance standards. These heightened regulatory demands significantly increase costs, disproportionately affecting smaller companies that often lack the resources to navigate such complexities. This creates substantial barriers to market entry and stifles innovation within the industry. Additionally, major food manufacturers impose customer-specific requirements, including unique testing protocols and quality certifications, which further complicate the process. These demands fragment R&D resources, making it challenging for smaller players to compete effectively. In contrast, larger flavor companies are better positioned to manage these challenges due to their dedicated regulatory affairs teams and well-established relationships with approval agencies, giving them a competitive edge in adapting to the evolving regulatory framework.

Segment Analysis

By Type: Natural Flavoring Gains Despite Synthetic Dominance

Synthetic flavoring maintains commanding market leadership with 54.21% share in 2025, reflecting cost advantages and consistent supply availability that appeal to price-sensitive food manufacturers. However, natural flavoring emerges as the growth champion with 5.76% CAGR through 2031, driven by consumer clean-label preferences and regulatory pressure against artificial additives. Nature-identical flavoring occupies a middle position, offering cost-performance balance for manufacturers transitioning from synthetic to natural formulations. The synthetic segment's dominance stems from established manufacturing infrastructure and regulatory approvals that create switching costs for food producers.

Advanced encapsulation technologies enable natural flavor stability improvements that historically favored synthetic alternatives, reducing the performance gap between categories. DSM-Firmenich's investment in natural flavor processing capabilities exemplifies how major players are repositioning for the clean-label transition. FDA compliance frameworks treat natural and synthetic flavoring differently, with natural ingredients facing less stringent pre-market approval requirements that accelerate product development timelines. The cost premium for natural flavoring continues narrowing as production scales increase and synthetic alternatives face regulatory restrictions.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Beverages Lead While Savory Snacks Accelerate

The beverage application commands 35.57% market share in 2025, benefiting from high flavor loading requirements and premium positioning opportunities in functional drink categories. Savory snacks represent the fastest-growing application at 6.24% CAGR, driven by ethnic flavor exploration and heat-level escalation among North American consumers. Dairy applications maintain steady demand through cheese, yogurt, and ice cream innovations, while bakery applications face margin pressure from commodity ingredient cost inflation. Confectionery applications show resilience through seasonal product launches and premium chocolate flavor development.

Meat applications experience transformation as plant-based alternatives require sophisticated umami and fat-replication technologies that command higher pricing than traditional meat flavoring. The beverage segment's leadership reflects the liquid medium's ability to carry complex flavor profiles and functional ingredients that solid applications cannot easily accommodate. Edlong's identification of brown butter and speculoos as top dairy flavor trends for 2025 illustrates how application-specific innovation drives segment growth. Other applications, including sauces and seasonings, benefit from home cooking trends that emerged during recent years and persist through convenience-focused product development.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The United States anchors North America's food flavor landscape with 72.16% market share in 2025, leveraging the world's most sophisticated food processing infrastructure and consumer willingness to pay premiums for innovative flavor experiences. US market dynamics favor natural ingredient adoption, driven by FDA regulatory pressure and consumer health consciousness that creates opportunities for premium positioning. Major flavor companies concentrate R&D facilities in the US to access top-tier food science talent and maintain proximity to leading food manufacturers. The market's maturity enables focus on high-value applications like functional beverages and plant-based alternatives that require advanced flavor technologies.

Mexico represents the region's fastest-growing market at 5.72% CAGR through 2031, benefiting from processed food industry expansion and rising middle-class purchasing power that drives demand for more sophisticated flavor profiles. USMCA trade provisions reduce ingredient import costs from the US and Canada, enabling Mexican food manufacturers to access premium flavoring solutions previously cost-prohibitive. Recent drought conditions and agricultural challenges create supply chain vulnerabilities that favor flavor companies with diversified sourcing networks and local manufacturing capabilities. The peso's relative stability against the US dollar facilitates long-term supply agreements that support sustained market expansion.

Canada maintains a stable mature market position with growth tied to natural ingredient transitions and regulatory alignment with US standards that facilitates cross-border ingredient sourcing. Health Canada's strengthened food additive oversight creates compliance costs that favor larger flavor companies with established regulatory affairs capabilities. The country's agricultural sector provides key raw materials for natural flavor production, creating vertical integration opportunities for companies seeking supply chain control. Canadian food manufacturers increasingly source flavoring solutions from US suppliers to access broader ingredient portfolios and cost efficiencies, creating cross-border trade flows that benefit from USMCA provisions.

Competitive Landscape

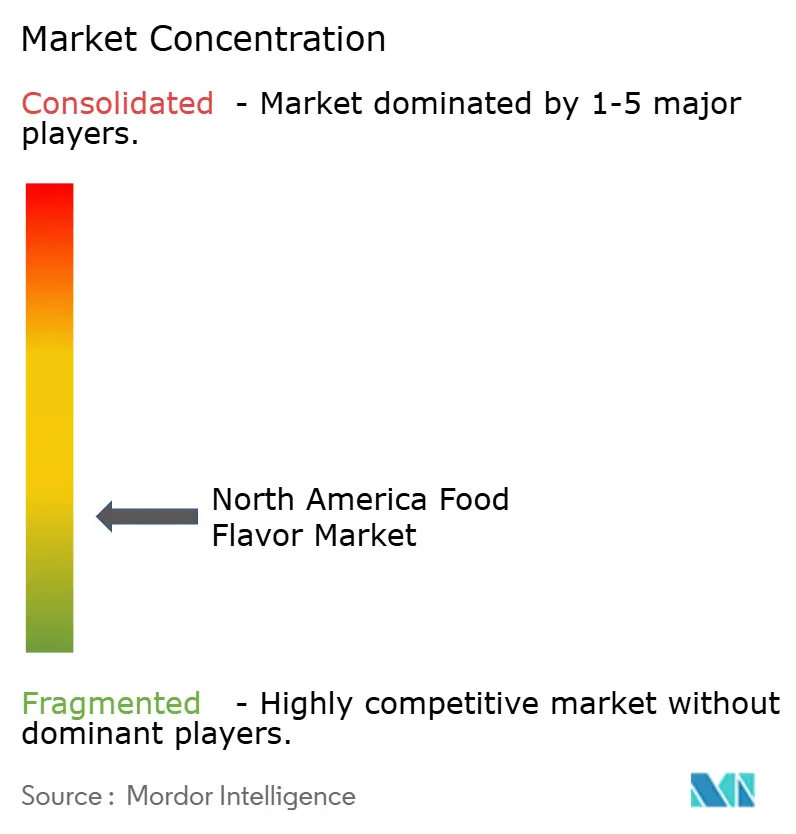

The North America food flavor market exhibits fragmented competition with a concentration score of 3 out of 10, creating opportunities for specialized players and technology-driven disruptors to capture share from established multinational corporations. Market leaders pursue vertical integration strategies through strategic acquisitions, exemplified by Glanbia's USD 300 million purchase of Flavor Producers and Roquette's USD 2.85 billion acquisition of IFF Pharma Solutions, aimed at controlling supply chains amid raw material volatility.

AI-powered flavor development emerges as a competitive differentiator, with companies like Symrise deploying machine learning algorithms to accelerate R&D cycles and reduce time-to-market for new flavor profiles. White-space opportunities exist in plant-based meat flavoring, functional beverage applications, and natural masking technologies for bitter bioactive compounds, where technical complexity creates barriers to entry that favor companies with advanced R&D capabilities.

Emerging disruptors leverage digital platforms and direct-to-manufacturer sales models to bypass traditional distribution channels, while established players respond through facility expansions and technology partnerships. FDA compliance frameworks create regulatory moats that benefit companies with established GRAS approvals and extensive safety databases, making regulatory expertise a key competitive asset in the fragmented landscape.

North America Food Flavor Industry Leaders

-

International Flavors and Fragrances

-

Symrise AG

-

Kerry Group PLC

-

DSM-Firmenich

-

Givaudan SA

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2023: Archer Daniels Midland Company acquired Revela Foods, a Wisconsin-based developer and manufacturer of innovative dairy flavor ingredients and solutions. With this acquisition, the company aims to expand its product portfolio.

- October 2023: Symrise introduced SET Flavors, a brand that leverages enrichment technologies to deliver premium and genuine taste solutions. Through its Selective Enrichment technology, SET Flavors, in collaboration with its partners, adeptly captures the intricacies of nature. This is made possible by employing cutting-edge equipment and streamlined processes, culminating in flavor profiles that are truly unique and true to their origins.

- September 2023: Robertet acquired BioPod, an environmentally conscious cultivation tool that foresees the difficulties of procuring natural components and their production. BioPod is a deployable greenhouse that measures 11 meters in length, 5 meters in width, and 6 meters in height.

- June 2023: Nelson-Jameson Inc., a leading distributor in the food processing industry, expanded its agreement with DSM-Firmenich. Nelson-Jameson has been the exclusive distributor for cheese ingredients of DSM-Firmenich for many years and will now be the exclusive distributor for its fresh dairy segment ingredients, including yogurt, buttermilk, and sour cream.

North America Food Flavor Market Report Scope

Food flavors are used to improve the flavor of food products, such as meats and vegetables, candies, and snacks. The North America food flavor market is segmented by type into natural flavors, synthetic flavors and natural-identical flavorings. The market is segmented by application into dairy, bakery and confectionery, savory, beverages, and other applications. The market is segmented by Geography into the United States, Canada, Mexico, and the Rest of North America. The market sizing has been done in value terms in USD for all the abovementioned segments.

Type

| Synthetic |

| Natural |

| Nature-Identical |

Application

| Dairy |

| Bakery |

| Confectionery |

| Savory Snack |

| Meat |

| Beverage |

| Other Applications |

Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| Type | Synthetic |

| Natural | |

| Nature-Identical | |

| Application | Dairy |

| Bakery | |

| Confectionery | |

| Savory Snack | |

| Meat | |

| Beverage | |

| Other Applications | |

| Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the North America food flavor market in 2026?

It is valued at USD 5.70 billion, with forecast growth to USD 7.12 billion by 2031.

Which product type is expanding fastest?

Natural flavoring is advancing at a 5.76% CAGR through 2031 due to clean-label demand and regulatory pressure on synthetics.

Why do beverages hold the largest share?

Beverages need multilayer flavor systems to balance functional ingredients, giving them 35.57% revenue in 2025.

Which country is growing quickest?

Mexico leads regional growth at a 5.72% CAGR, supported by USMCA-enabled ingredient trade and processed food expansion.