Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

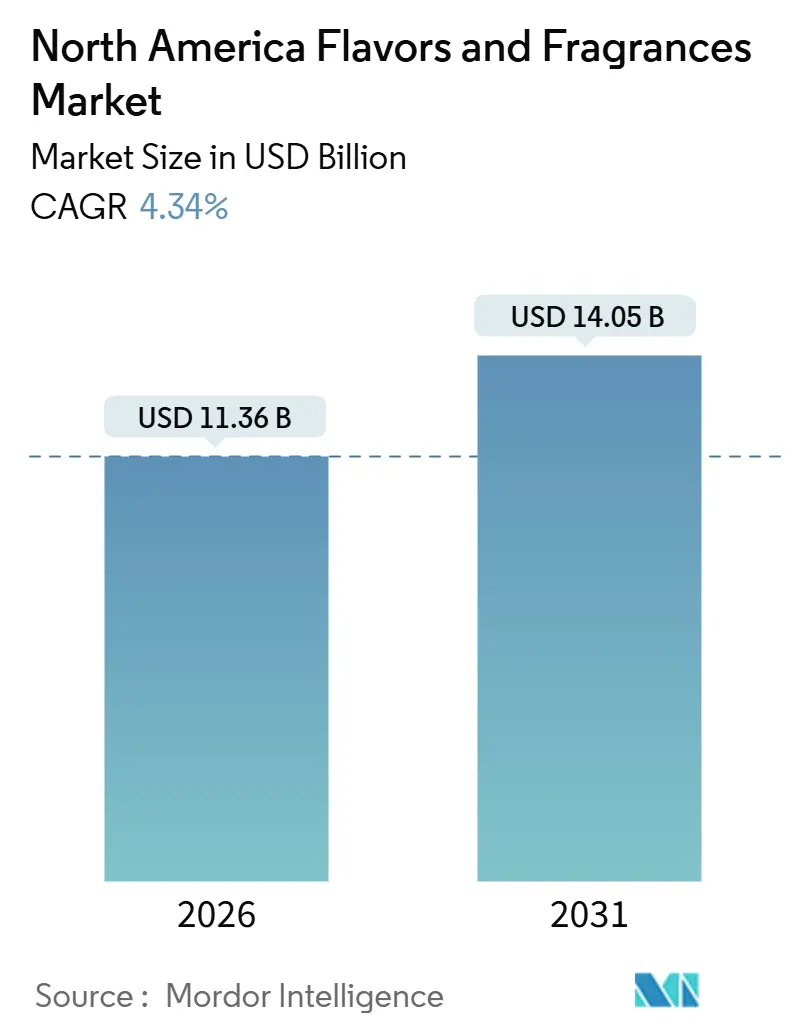

| Market Size (2025) | USD 11.36 Billion |

| Market Size (2031) | USD 14.05 Billion |

| Growth Rate (2026 - 2031) | 4.34% CAGR |

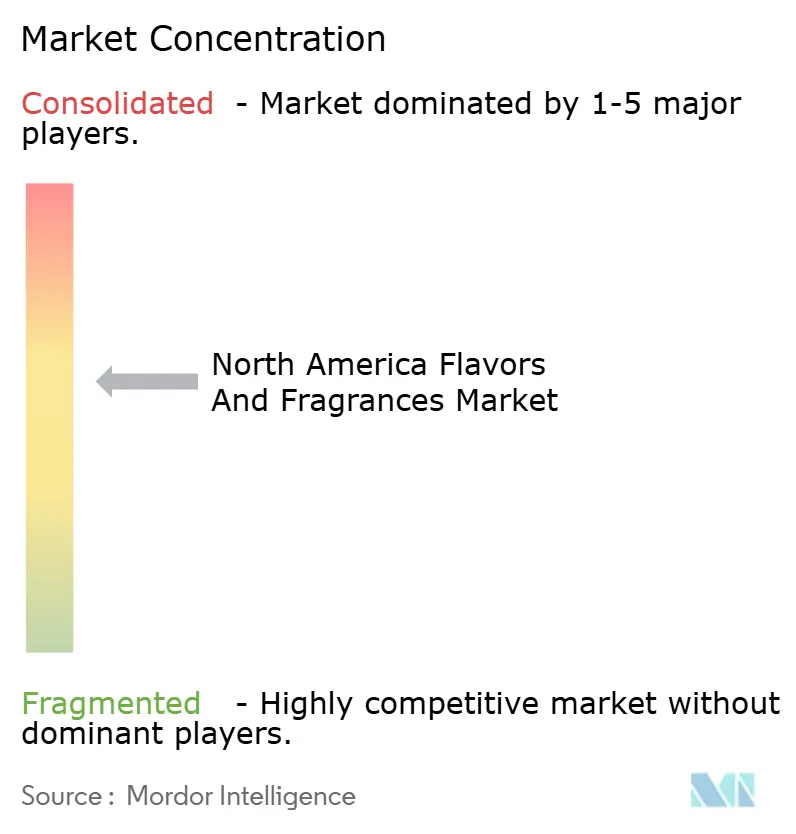

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Flavors And Fragrances Market Analysis by Mordor Intelligence

The North America flavors and fragrances market size stood at USD 11.36 billion in 2026 and is projected to reach USD 14.05 billion by 2031, advancing at a 4.34% CAGR through the forecast period. Strong demand for clean-label solutions, premium personal care products, and precision-fermented molecules is driving market growth, despite regulatory agencies narrowing the definition of "natural." The United States leads in value creation, supported by its advanced biotechnology capabilities and clear regulatory pathways. Meanwhile, Mexico is experiencing the fastest growth, driven by increasing disposable incomes and rising beauty product consumption. Encapsulation technologies that stabilize natural oils without synthetic carriers are transitioning from niche applications to mainstream adoption, following the FDA's 2024 ban on brominated vegetable oil. Additionally, AI-driven formulation processes are reducing development timelines, prompting regional customers to move away from traditional iterative bench trials. Competitive strategies focus on vertical integration, with major players co-locating extraction, fermentation, and blending operations to safeguard intellectual property and reduce lead times.

Key Report Takeaways

- By product type, flavors captured 54.18% of the North America flavors and fragrances market share in 2025, while fragrances are forecast to register a 5.37% CAGR from 2026-2031.

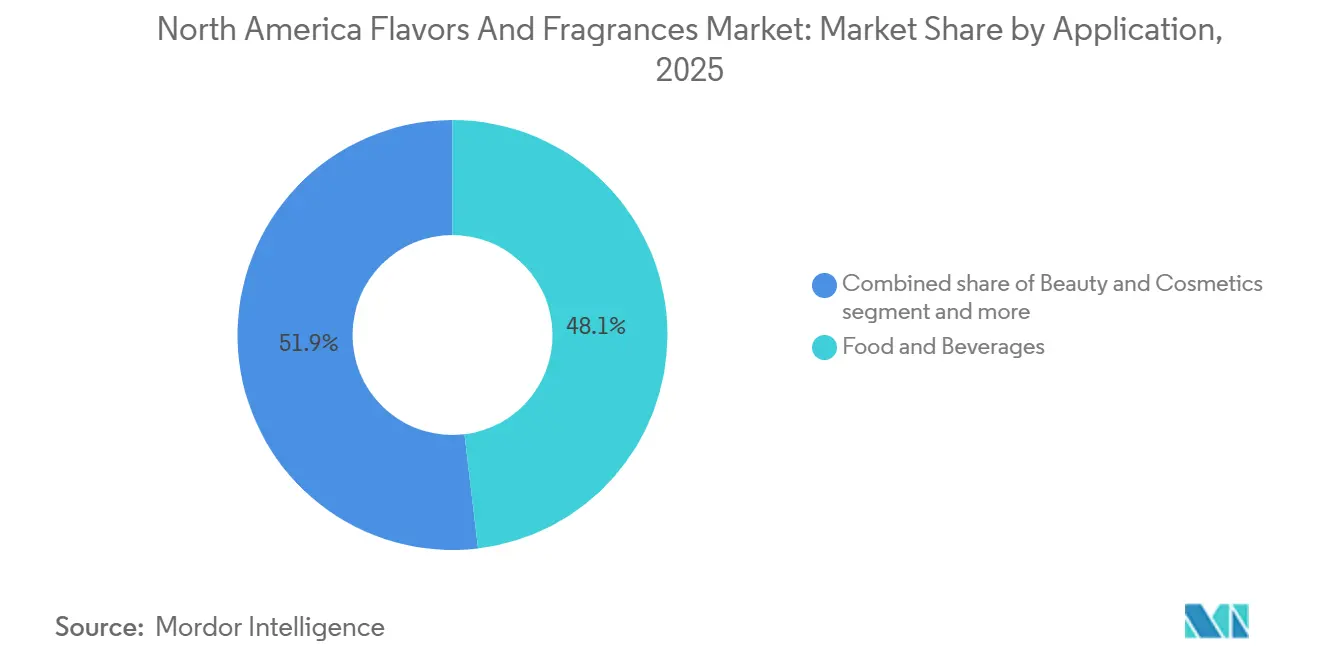

- By application, food and beverages held 48.10% of the North America flavors and fragrances market size in 2025, whereas beauty and cosmetics is projected to advance at a 6.89% CAGR through 2031.

- By geography, the United States accounted for 28.56% of 2025 revenue, and Mexico is expected to expand at a 7.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Flavors And Fragrances Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for clean‑label and natural ingredients | +0.8% | United States, Canada, spillover to Mexico | Medium term (2-4 years) |

| Expansion of convenience and ready to eat (RTE) foods | +0.6% | United States, emerging in Canada | Short term (≤2 years) |

| Premiumization in beauty and personal care | +0.5% | United States, Canada | Medium term (2-4 years) |

| Innovations in biotechnology and precision fermentation for sustainable flavors | +0.7% | United States, later Canada and Mexico | Long term (≥4 years) |

| Increasing popularity of exotic, ethnic, and fusion flavors | +0.4% | Multicultural United States cities, Mexico border | Short term (≤2 years) |

| Technological advancements like AI‑driven flavor formulation and encapsulation | +0.5% | United States research and development hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for clean-label and natural ingredients

Consumer preferences in North America are increasingly influencing the flavors and fragrances market, with a notable shift toward natural and clean-label ingredients. Growing skepticism toward synthetic additives is prompting manufacturers to source USDA organic-certified ingredients, positioning these products as safer and more transparent options. Retail shelf space, once dominated by nature-identical compounds, is now being occupied by organic and naturally derived flavors, reflecting a significant transformation driven by consumer demand. This trend is particularly evident in the United States, where 36% of consumers prefer foods labeled as natural, emphasizing a strong market segment that prioritizes authenticity, traceability, and perceived health benefits[1]Source: International Food Information Council, "2024 IFIC Food & Health SURVEY," ific.org. The commercial impact of this shift is demonstrated by robust sales growth for organic products. To meet consumer expectations, manufacturers are developing natural and organic flavor compounds that cater to health-conscious buyers and those seeking clean-label alternatives. In 2024, U.S. sales of organic food products reached USD 65.4 billion, highlighting consumers' willingness to pay a premium for products aligned with natural and clean-label preferences [2]Source: Economic Research Service U.S. DEPARTMENT OF AGRICULTURE, "Organic Agriculture," ers.usda.gov .

Expansion of convenience and ready to eat (RTE) foods

The increasing popularity of convenience and ready-to-eat (RTE) foods is driving demand for innovative food flavors, as consumers prioritize quick and easy meal solutions without compromising on taste. Products such as meal kits, frozen entrees, and pre-packaged snacks require flavors that remain appealing over extended shelf lives while catering to diverse taste preferences. In 2024, 82% of adults in the U.S. reported consuming ultra-processed foods, underscoring the widespread reliance on convenient options and the resulting opportunities for flavor innovation [3]Source: Ayana Bio, "SURVEY DATA REVEALS TWO-THIRDS OF AMERICAN ADULTS WOULD EAT MORE AND PAY MORE FOR ULTRA-PROCESSED FOODS THAT INCLUDE MORE NUTRITIOUS INGREDIENTS," ayanabio.com. Taste and convenience are key factors influencing product choices. Moreover, the report revealed that 62% of consumers identified taste and 59% identified convenience as the primary reasons for selecting ultra-processed foods. This highlights the importance of high-quality, appealing flavors in driving repeat purchases. Consequently, food manufacturers are increasingly adopting tailored flavor solutions, including natural and clean-label options, to enhance consumer satisfaction and capitalize on growth opportunities across retail, online, and foodservice channels.

Premiumization in beauty and personal care

Luxury fragrance and skincare brands are utilizing ingredient storytelling to support price points that are 30-50% higher than mass-market alternatives. This approach relies on traceable and sustainably sourced aromatics. Estée Lauder Companies reported in its fiscal 2025 earnings that prestige beauty experienced faster growth than the mass market in North America, with fragrance significantly contributing to operating margin expansion. Fragrance houses are addressing this trend by establishing multi-year supply agreements with growers of high-value crops such as Bulgarian rose, Haitian vetiver, and Indian sandalwood. Additionally, they are investing in traceability systems to ensure farm-to-bottle provenance. In February 2025, Unilever announced the development of an in-house fragrance creation capability, reflecting a strategic move toward vertical integration. This initiative aims to reduce lead times for limited-edition launches and safeguard proprietary scent profiles from competitor reverse-engineering.

Innovations in biotechnology and precision fermentation for sustainable flavors

Precision fermentation is progressing from pilot-scale operations to commercial production, enabling flavor manufacturers to produce molecules such as vanillin, squalane, and rare fruit esters. These molecules are chemically identical to plant-derived extracts but eliminate agricultural variability and the risks associated with deforestation. Advances in biotechnology and precision fermentation are revolutionizing flavor development by facilitating the production of high-quality, natural-tasting ingredients without dependence on traditional agricultural practices. These technologies provide manufacturers with the ability to achieve greater consistency, scalability, and reduced environmental impact. By utilizing microbes, enzymes, and fermentation processes, companies can replicate complex flavor profiles, such as those of dairy, meat, or fruit, while significantly reducing the use of land, water, and other resources, thereby meeting increasing sustainability demands.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High research and development costs for stable, clean-label alternatives | -0.4% | United States and Canada, with limited impact in Mexico | Long term (≥ 4 years) |

| Stringent regulatory scrutiny | -0.5% | United States (FDA), Canada (Health Canada), Mexico (COFEPRIS) | Medium term (2-4 years) |

| Consumer skepticism toward "natural" claims requiring third-party certifications | -0.3% | United States and Canada premium retail channels | Short term (≤ 2 years) |

| Limited shelf life and batch variability of natural extracts | -0.3% | United States and Canada, with supply-chain implications for Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High research and development costs for stable, clean-label alternatives

Developing natural flavor systems that align with the performance and cost profiles of synthetic alternatives requires extensive multi-year research and development investments, which many mid-tier suppliers find challenging to sustain. The variability in botanical extraction yields further complicates this process, vanilla bean harvests are influenced by weather conditions in Madagascar and Indonesia, while citrus oil production is affected by freeze risks in Florida and California. These fluctuations compel formulators to maintain buffer inventories or resort to synthetic alternatives, which can compromise clean-label objectives. Smaller flavor companies are either consolidating or exiting the natural segment, thereby ceding market share to larger players such as Givaudan, IFF, Symrise, and Firmenich, which can distribute research and development costs across their global customer bases. This trend is less pronounced in Mexico, where price sensitivity limits the demand for premium natural ingredients. However, in the United States and Canada, clients increasingly expect suppliers to demonstrate robust innovation pipelines, creating higher barriers to entry for new or smaller competitors.

Stringent Regulatory Scrutiny

Regulatory agencies are increasingly tightening ingredient definitions and enforcement measures, leading to higher compliance costs that disproportionately affect smaller suppliers and delay product launches. For instance, the FDA's decision in July 2024 to revoke the use of brominated vegetable oil, a citrus-flavor emulsifier used for decades, provided manufacturers with only 12 months to reformulate their products. This compressed timeline has impacted stability testing and consumer acceptance trials. Similarly, Health Canada's cosmetic ingredient notification system mandates suppliers to disclose formulation details 10 days prior to market entry, diminishing first-mover advantages and exposing proprietary blends to competitor scrutiny. In Mexico, the Federal Economic Competition Commission initiated an investigation in August 2024 into alleged price coordination among transnational fragrance suppliers. This investigation, conducted in collaboration with the U.S. Department of Justice and the U.K. Competition and Markets Authority, highlights increased antitrust scrutiny, which could influence contract terms and pricing transparency.

Segment Analysis

By Product Type: Fermentation Redefines Natural

Flavors accounted for 54.18% of North America's revenue in 2025, driven by reformulation mandates in packaged foods and beverages. Fragrances are projected to grow at an annual rate of 5.37% through 2031, as beauty and personal care brands emphasize ingredient transparency and premiumization. Within the flavors segment, natural variants are gaining market share at the expense of synthetic and nature-identical options. This shift is influenced by retailer clean-label initiatives and consumer skepticism toward chemical-sounding ingredient names. Synthetic flavors continue to offer cost advantages in applications where performance outweighs label appeal, such as industrial bakery mixes and low-cost confectionery. However, they face challenges due to the FDA's stricter definitions and retailer exclusion lists.

Natural fragrances encounter technical challenges in certain applications. For instance, essential oils oxidize under alkaline conditions commonly found in detergents, and their volatility limits scent longevity compared to synthetic musks designed for slow release. The International Fragrance Association's 51st Amendment, effective June 2023, restricted 48 materials, including legacy synthetic musks. This regulation has accelerated reformulation timelines and created opportunities for suppliers with extensive natural-ingredient portfolios.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Beauty Outpaces Food on Premiumization

In 2025, food and beverages accounted for 48.10% of North America's applications, highlighting the segment's significant volume and the widespread use of flavors in processed foods. However, the beauty and cosmetics segment is projected to grow at an annual rate of 6.89% through 2031, driven by consumer preference for brands that emphasize ingredient transparency and avoid synthetic preservatives. Within the food and beverages category, savory and snack products are growing at a faster pace compared to bakery or confectionery items. This growth is fueled by the demand for bold, globally inspired flavors such as gochujang, harissa, and yuzu, which help products stand out in competitive retail environments. Dairy products, particularly yogurt and ice cream, are increasingly incorporating botanical flavors like lavender, matcha, and cardamom to attract health-conscious consumers seeking indulgent options free from artificial additives.

The personal care, beauty and cosmetics segment is increasingly focused on premiumization and ingredient transparency. Sustainability narratives are becoming more prominent, with less emphasis on fragrance intensity and longevity. Estée Lauder's fiscal 2025 report revealed that prestige beauty outperformed mass-market products in North America, with fragrance contributing significantly to margin growth. This underscores the segment's resilience to economic challenges. Other applications, such as pharmaceuticals and industrial uses, remain relatively small but stable. In pharmaceuticals, flavors are used to mask the bitterness of active ingredients, while fragrances enhance the user experience in cleaning products and automotive interiors.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The United States accounted for 28.56% of North America's revenue in 2025, benefiting from advantages in biotechnology infrastructure, regulatory predictability, and consumer willingness to pay premiums for clean-label products. The country has established itself as a leader in precision fermentation, with activities concentrated in biotechnology hubs such as Boston, San Francisco, and San Diego. These hubs provide access to venture capital and synthetic biology talent, enabling companies to scale rapidly from pilot projects to commercial production. Notable partnerships, such as Symrise with Cellibre and IFF with Amyris, capitalize on United States-based fermentation capacity to produce ingredients like vanillin, squalane, and rare fruit esters. These products are manufactured at cost parity with conventional extraction methods, highlighting the efficiency and innovation within the United States market.

Mexico is projected to be the fastest-growing market in North America, with a forecasted CAGR of 7.18% through 2031. This growth is driven by several factors, including rising disposable incomes, increasing urbanization, and Mexico's position as Latin America's leading exporter of cosmetics and personal care products. The demand for flavors and fragrances in Mexico is divided into two distinct segments. Multinational food and beverage companies operating in the country adopt United States clean-label standards to maintain consistency across their supply chains. In contrast, domestic brands prioritize cost considerations, which keeps synthetic flavors dominant in price-sensitive categories. This bifurcation reflects the diverse consumer preferences and market dynamics within the country.

Canada's market trajectory is shaped by Health Canada's cosmetic ingredient notification requirements, which mandate disclosure 10 days prior to market entry. While this regulatory framework reduces first-mover advantages for companies, it also minimizes downstream reformulation risks by ensuring compliance from the outset. This approach provides a level of predictability and stability for businesses operating in the Canadian market. In contrast, the rest of North America, primarily comprising Caribbean nations, represents a negligible share of regional revenue. These countries have limited domestic production capabilities and rely heavily on imports from the United States and Mexico to meet their needs. This reliance underscores the disparities in production capacity and market development across the region.

Competitive Landscape

The North America flavors and fragrances market demonstrates moderate concentration. Unilever's planned initiative in February 2025 to establish in-house fragrance creation capabilities reflects a strategic move toward vertical integration. This approach aims to shorten innovation cycles and decrease dependence on external suppliers, a strategy that other multinational consumer goods companies may consider adopting. By bringing fragrance creation in-house, Unilever seeks to enhance its control over the innovation process, potentially accelerating product development and improving cost efficiencies. This move could set a precedent for other companies in the industry, encouraging a shift toward self-reliance and streamlined operations.

Opportunities for growth exist in the household products segment, where synthetic fragrances currently dominate. However, clean-label trends are beginning to influence this category as consumers increasingly demand transparency across all product types, extending beyond food and personal care. The growing consumer preference for natural and sustainable products is driving this shift, creating a need for manufacturers to adapt their offerings. Emerging disruptors in the market include fermentation-focused startups that circumvent traditional botanical supply chains. These startups offer cost parity with synthetic options while meeting "natural" labeling standards, although regulatory uncertainties surrounding fermentation-derived ingredients remain a challenge. The ability of these startups to address both cost and labeling concerns positions them as key players in the evolving market landscape, despite the hurdles posed by unclear regulatory frameworks.

AI-driven flavor formulation is significantly reducing development timelines, cutting them from 18-24 months to 6-9 months. Examples of this shift toward data-driven innovation include Symrise's Symvision AI platform and McCormick's collaboration with IBM Watson, which aim to minimize reliance on traditional iterative bench trials. By leveraging AI, companies can analyze vast datasets to predict consumer preferences and optimize formulations more efficiently. This technological advancement not only accelerates the product development process but also enhances the precision and customization of flavors, enabling companies to better meet evolving consumer demands. The integration of AI into flavor formulation represents a transformative step for the industry, offering a competitive edge to early adopters.

North America Flavors And Fragrances Industry Leaders

-

International Flavors & Fragrances

-

Symrise AG

-

Givaudan SA

-

dsm-firmenich

-

The Archer Daniels Midland Company (ADM)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: Sensapure Flavors has unveiled SensaNaturals Flavor Solutions, a clean-label flavor platform composed entirely of recognizable whole-food and plant-based ingredients. This innovation allows brands to list specific components, such as blueberry juice powder or acai extract, on product labels instead of generic terms like “natural flavors.” The platform was developed in response to growing consumer demand for ingredient transparency and cleaner labeling practices.

- October 2025: Natural Perfume House Abel has relaunched with a renewed emphasis on sustainable luxury and wellness-focused fragrance experiences. The brand has reintroduced its signature collection of natural perfumes, crafted with high-quality botanical ingredients and refined scent compositions. This relaunch caters to conscious consumers seeking sustainable alternatives to conventional synthetic fragrances.

- August 2025: T. Hasegawa USA has introduced HASECITRUS, a citrus flavor stabilization technology aimed at helping beverage manufacturers maintain vibrant and fresh citrus taste for extended periods. This innovation addresses oxidation challenges commonly faced in ready-to-drink and powdered beverages. Developed through the company’s “Bridge to Tokyo” research and development program, HASECITRUS ensures the retention of color, aroma, and taste without the need for refrigeration or specialized packaging. It supports clean-label, preservative-free formulations while extending product shelf life.

- July 2025: Sensient Flavors & Extracts has introduced BioSymphony, a portfolio of natural flavor compounds created through biotransformation using nature-derived ingredients. This portfolio is designed to meet the evolving needs of food and beverage formulation by enabling manufacturers to develop deeper and more sophisticated taste profiles. BioSymphony is globally recognized as a “natural flavor” and eliminates the need for special regional labeling, simplifying product formulation for diverse markets.

North America Flavors And Fragrances Market Report Scope

Flavors and fragrances create scents and tastes in a broad range of consumer products, including prepared foods, personal care products, household products, fine fragrances, cosmetics, and beverages.

The North American flavor and fragrance market is segmented by type into natural and synthetic. Based on the application, the market is segmented into food, beverages, beauty and personal care, and other applications. The report offers an analysis of major economies in the region, namely, the United States, Canada, Mexico, and the Rest of North America.

The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| Flavors | Synthetic |

| Natural | |

| Nature-Identical | |

| Fragrances | Synthetic |

| Natural |

By Application

| Food and Beverages | Savory and Snacks |

| Dairy Products | |

| Bakery | |

| Confectionery | |

| Meat Products | |

| Beverages | |

| Others | |

| Personal Care | |

| Beauty and Cosmetics | |

| Household Products | |

| Other Applications (Industrial, pharmaceuticals, etc) |

By Geography

| United States |

| Canada |

| Mexio |

| Rest of North America |

| By Product Type | Flavors | Synthetic |

| Natural | ||

| Nature-Identical | ||

| Fragrances | Synthetic | |

| Natural | ||

| By Application | Food and Beverages | Savory and Snacks |

| Dairy Products | ||

| Bakery | ||

| Confectionery | ||

| Meat Products | ||

| Beverages | ||

| Others | ||

| Personal Care | ||

| Beauty and Cosmetics | ||

| Household Products | ||

| Other Applications (Industrial, pharmaceuticals, etc) | ||

| By Geography | United States | |

| Canada | ||

| Mexio | ||

| Rest of North America | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the North America flavors and fragrances market today?

The market reached USD 11.36 billion in 2026 and is projected to climb to USD 14.05 billion by 2031.

Which product type leads revenue in the region?

Flavors commanded 54.18% of 2025 revenue, driven by food and beverage reformulation mandates.

How is precision fermentation changing supply chains?

Fermentation produces vanillin, squalane, and rare esters at commercial scale, reducing crop dependency and enabling consistent clean-label sourcing.

What regulatory changes most affect suppliers?

The FDA’s 2024 ban on brominated vegetable oil and the Modernization of Cosmetics Regulation Act increase reformulation and compliance costs.