Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

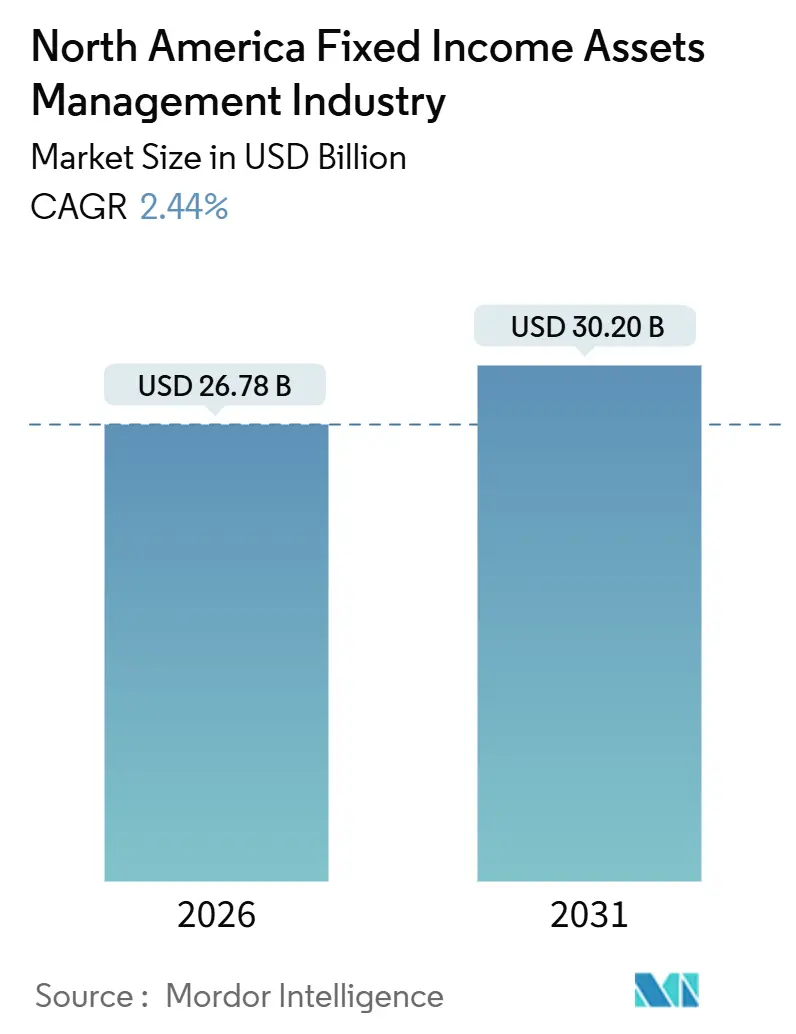

| Market Size (2026) | USD 26.78 Billion |

| Market Size (2031) | USD 30.20 Billion |

| Growth Rate (2026 - 2031) | 2.44% CAGR |

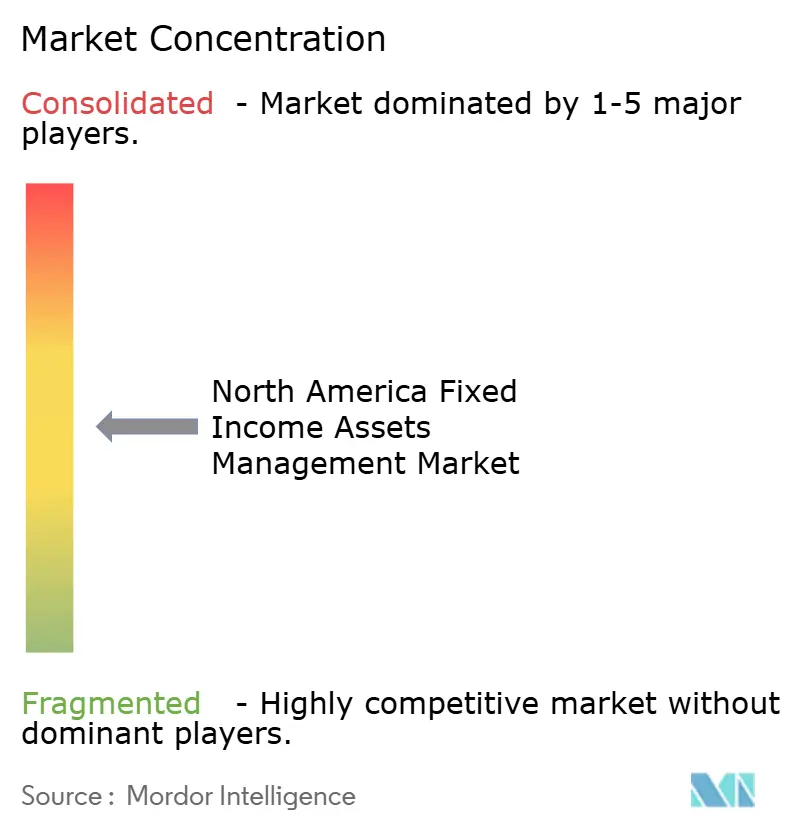

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Fixed Income Assets Management Market Analysis by Mordor Intelligence

The North America fixed income assets management market size is USD 26.78 billion in 2026 and is projected to reach USD 30.2 billion by 2031 at a 2.44% CAGR. Institutional and retail demand is supported by the scale and depth of the United States debt markets, where fixed income securities outstanding reach USD 48.9 trillion in Q3 2025 and continue to expand. Bond funds and ETFs remain central channels for allocations, with bond fund assets at USD 5,500.8 billion in November 2025 and robust issuance and trading activity sustaining liquidity. Monetary policy normalization by the Federal Reserve and rate stability by the Bank of Canada create a constructive environment for income generation and portfolio rebalancing. Technology-enabled execution, electronic trading penetration, and portfolio analytics platforms reinforce efficiency and transparency, which support durable participation across client segments in the North America fixed income asset management market.

Key Report Takeaways

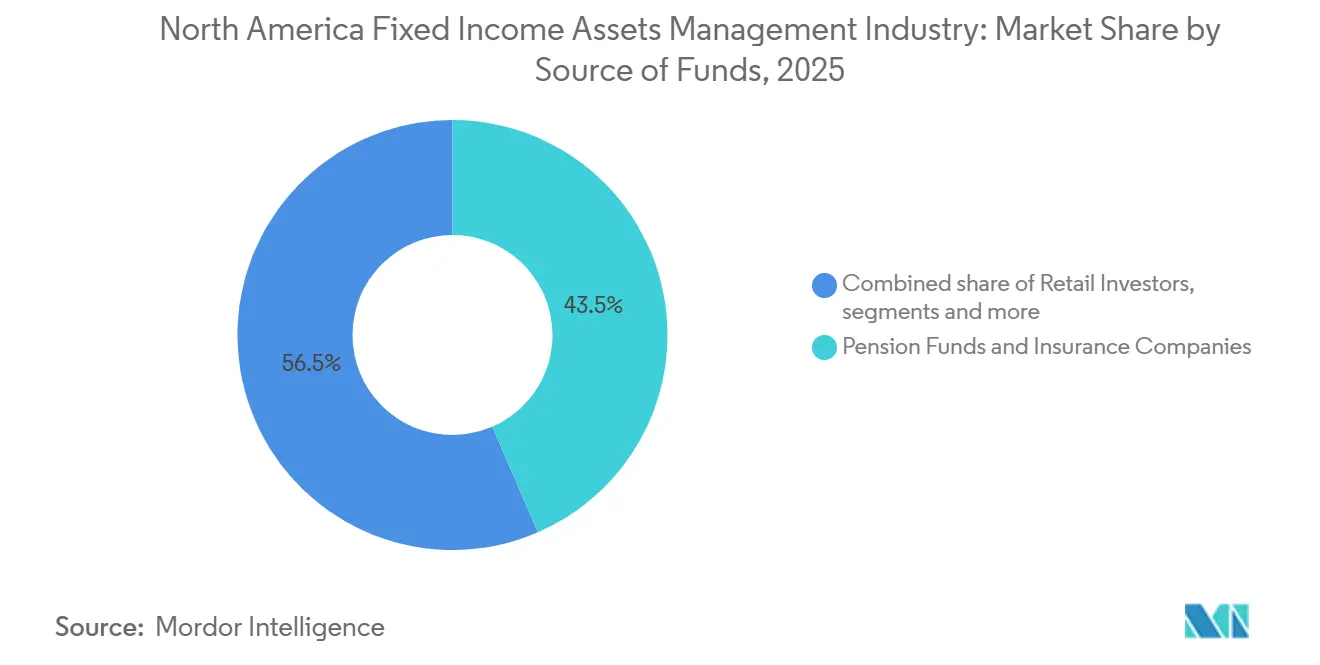

- By source of funds, pension funds and insurance companies led with 43.50% revenue share of the North America fixed income asset management market in 2025, while retail investors are forecast to expand at a 4.84% CAGR through 2031.

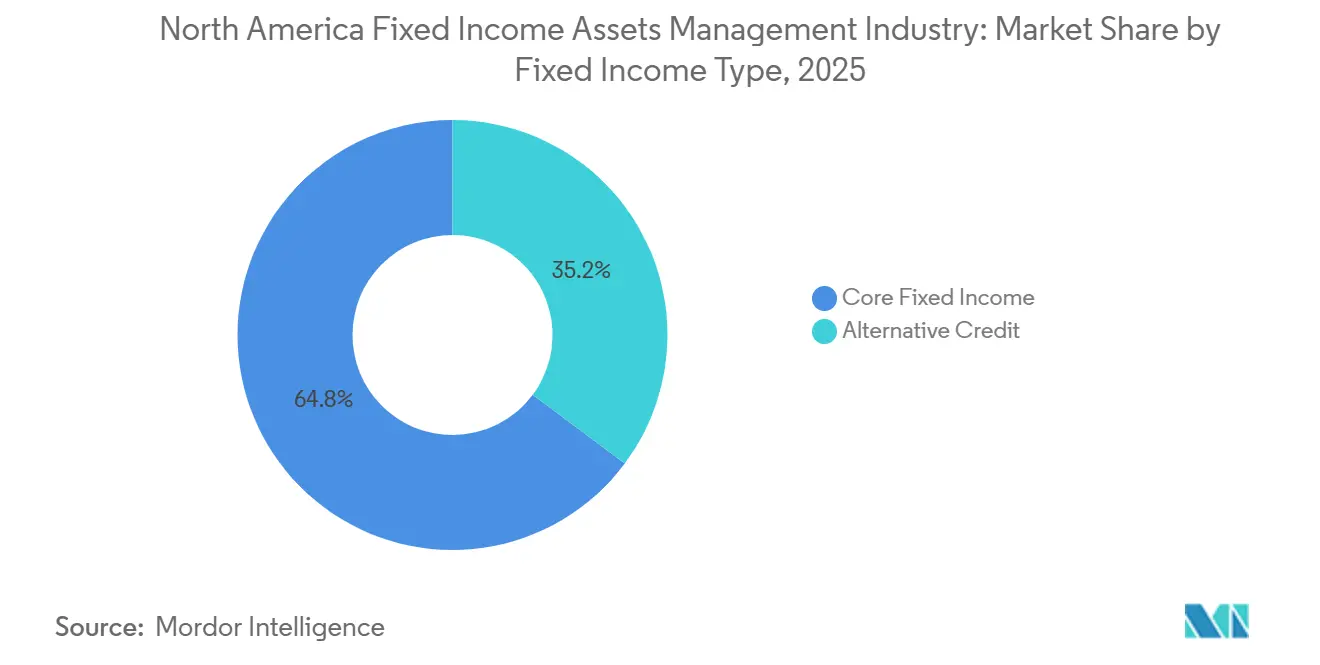

- By fixed income type, core fixed income accounted for a 64.80% share of the North America fixed income asset management market size in 2025, and alternative credit is advancing at a 6.54% CAGR through 2031.

- By type of asset management firms, large financial institutions and bulge bracket banks held 28.76% share of the North America fixed income asset management market in 2025, while mutual funds and ETFs recorded the highest projected CAGR at 5.48% through 2031.

- By Geography, the United States accounted for 82.2% of the North America fixed income asset management market and is forecast to expand at a 4.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Fixed Income Assets Management Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong institutional demand from pension funds, insurers, and asset managers seeking stable, income-oriented returns | +0.8% | Global, strongest in the United States and Canada core pension markets | Medium term (2-4 years) |

| Aging demographics are driving preference for low-risk, predictable income among retirees and conservative investors | +0.9% | United States and Canada, with a concentration in Florida, Arizona, and British Columbia | Long term (≥ 4 years) |

| Rising adoption of passive fixed income products, including bond ETFs, due to cost efficiency, liquidity, and diversification | +0.6% | Global, led by the United States, institutional and retail adoption | Medium term (2-4 years) |

| Growth in ESG-focused bond investments, encouraging capital flows toward sustainable and green fixed income instruments | +0.3% | Canada's leadership with sovereign green bonds, and the United States growth despite regulatory uncertainty | Medium term (2-4 years) |

| Advanced analytics and AI integration enhancing portfolio construction, risk assessment, and performance optimization | +0.5% | United States technology hubs, Canada financial centers, Toronto and Montreal | Long term (≥ 4 years) |

| High market liquidity and trading depth in the US, supporting sustained fixed income participation | +0.7% | United States Treasury and corporate bond markets, Canada government bonds | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Strong Institutional Demand from Pension Funds, Insurers, and Asset Managers Seeking Stable, Income-Oriented Returns

The United States retirement assets have reached USD 49.6 trillion in 2024, driving demand for fixed income allocations in public and private plans. Public defined benefit pension plans in the U.S. allocate an average of 23% to fixed income, with variations based on liability profiles, ensuring stable demand for government and high-grade credit securities. Canada’s CPP, valued at CAD 714.4 billion as of March 31, 2025 (USD 521.76 billion), also allocates significantly to fixed income, reinforcing institutional stability. Insurers consistently purchase corporate bonds to support liabilities and capital frameworks, maintaining credit demand through rate cycles. By November 2025, bond mutual funds attracted USD 94.638 billion in net inflows, with total assets reaching USD 5,500.8 billion, highlighting strong demand for externally managed fixed income strategies. These trends sustain the North American fixed income asset management market as plan sponsors and insurers align cash flows with liabilities and retirees seek income. Public plans targeting 6% to 7% income focus on high-quality, duration-managed portfolios and diversified credit exposures managed by experienced professionals. This approach stabilizes net flows and supports long-term mandates across various investment vehicles. Institutions also explore private credit and infrastructure debt, creating opportunities for multi-asset fixed income managers. This diversification sustains fee pools and supports the evolving North American fixed income asset management market.

Aging Demographics Driving Preference for Low-Risk, Predictable Income Among Retirees and Conservative Investors

The share of Americans at or near retirement continues to grow, and this demographic shift increases the preference for bond income over equity volatility. Savings vehicles show this behavior, with traditional IRA investors in their sixties holding 22.5% in bonds and bond funds compared with much lower allocations in younger cohorts. Regions with high concentrations of older households exhibit elevated interest in tax-exempt and income strategies, which supports municipal bond demand and flows into conservative portfolios. Municipal bond fund inflows reached USD 47 billion in 2025, while tax-exempt yields near 3% to 4% continued to attract high-income investors seeking after-tax income. These structural trends steer more household assets into taxable and tax-exempt fixed income, reinforcing product demand and the advisor toolkit for retirement planning. Demographics, therefore, remain a steady tailwind for the North America fixed income asset management market as income and preservation objectives rise in importance through 2031.

Rising Adoption of Passive Fixed Income Products, Including Bond ETFs, Due to Cost Efficiency, Liquidity, and Diversification

Passive bond vehicles continue to gain share as investors pursue cost and transparency benefits. Index bond funds held USD 2,905.5 billion in assets in November 2025, equal to 37.6% of total bond fund assets, and they drew USD 27.547 billion of net inflows that month, while active bond funds drew USD 25.462 billion. Bond ETFs also saw robust activity, including net issuance of USD 11.090 billion in the week ended December 30, 2025, with both taxable and municipal ETFs participating. Benchmark yields enhance the case for low-cost core exposure, with intermediate investment grade yields near 5% at year-end 2024 and index yield-to-worst measures supportive in late 2025[1]ICI Research Department, “Combined Estimated Long-Term Flows and ETF Net Issuance,” ICI, ici.org. Market structure supports efficient execution through electronic trading, with investment-grade corporate bonds transacting electronically near the 50% mark and high-yield near the mid-30s in 2025. Fee pressure on active managers reinforces the shift as firms disclose lower average fee rates due to the mix, which further accelerates the appeal of scalable passive products within the North America fixed income asset management market.

Growth in ESG-Focused Bond Investments, Encouraging Capital Flows Toward Sustainable and Green Fixed Income Instruments

Sustainable fixed income continues to evolve, with Canada providing leadership in sovereign green issuance and framework innovation. Canada priced its fifth green bond on October 26, 2025, for USD 1.825 billion with a 10-year maturity and a book exceeding USD 4.015 billion, with 70% of allocations to ESG-mandated investors. Canada’s updated Green Bond Framework allows certain nuclear-related expenditures, making it the first sovereign to include nuclear in a green framework and broadening the pool of eligible green projects[2]Department of Finance Canada, “Canada Successfully Prices Green Bonds to Raise $2.5 Billion,” Government of Canada, canada.ca. Ontario remains the largest and most consistent CAD green bond issuer, adding USD 1.53 billion (CAD 2.1 billion) in November 2025 and bringing cumulative issuance to USD 17.958 billion (CAD 24.6 billion) with USD 14.471 billion outstanding ( CAD 19.85 billion). Export Development Canada has issued green bonds since 2014, and its 2022 Sustainable Bond Framework added transition bonds that help issuers move from high to lower carbon activities. Despite United States regulatory uncertainty after the SEC voted to stop defending its 2024 climate disclosure rule in March 2025, institutional demand for ESG-aligned debt remains evident in flows to core, corporate, and treasury ETFs managed by leading firms, which sustains ESG product relevance in the North America fixed income asset management market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Evolving regulatory frameworks and compliance burdens, including ESG disclosure requirements, increasing operational costs | -0.4% | United States SEC jurisdiction, Canada OSC and CIRO oversight | Medium term (2-4 years) |

| Volatility in interest rates and inflation, negatively affecting bond valuations and yield stability | -0.5% | Global, with Federal Reserve and Bank of Canada policy driving North America rates | Short term (≤ 2 years) |

| Exposure to transaction costs and foreign exchange risks in cross-border fixed income investments | -0.2% | Cross-border flows between United States and Canada, emerging markets exposure | Medium term (2-4 years) |

| Margin pressure on active managers due to intensifying competition and a shift toward passive investment strategies | -0.6% | United States asset management industry, Canada mutual fund sector | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Evolving Regulatory Frameworks and Compliance Burdens, Including ESG Disclosure Requirements, Increasing Operational Costs

Policy shifts change cost curves and project plans for asset managers. In March 2025 the SEC voted to end its defense of the 2024 climate disclosure rule, creating uncertainty for firms that invested in related data and reporting systems[3]U.S. Securities and Exchange Commission, “Statement on Ending Defense of Climate Disclosure Rules,” SEC, sec.gov. Treasury market structure is also changing, with mandatory central clearing deadlines arriving over 2026 and 2027, which will require systems upgrades, clearer connectivity, and margin workflows for cash and repo. Discussions around bank capital recalibrations continue, and the industry seeks rules that do not impair dealer market-making, which matters for liquidity and execution quality. The SEC’s updated fund names regime requires affected managers to ensure at least 80% alignment with stated approaches, which necessitates compliance investment for some fixed income funds. Canadian regulators adapted to U.S. clearing rule changes by restating recognition orders for FICC, while firms also disclosed one-off costs linked to legal and regulatory matters, which shows how compliance and oversight can influence economics in the North America fixed income asset management market.

Volatility in Interest Rates and Inflation, Negatively Affecting Bond Valuations and Yield Stability

Policy rates and inflation trends set the backdrop for fixed income returns and risk. The effective federal funds rate is 3.64% as of January 9, 2026, after 175 basis points of cuts since September 2024, and FOMC participants' views differ on the trough level through 2026. Long-term Treasury yields remain elevated, with the 10-year at 4.18% and the 30-year at 4.82% on January 9, 2026, reflecting inflation dynamics and fiscal considerations[4]Federal Reserve Board Staff, “H.15 Selected Interest Rates,” Federal Reserve Board, federalreserve.gov. In Canada, the policy rate stands at 2.25% as of December 10, 2025, and headline CPI slowed to 2.2% in October 2025, with core measures in the 2.5% to 3% range. Government of Canada yields are steady with 10-year at 3.38% and 30-year at 3.82% as of January 9, 2026, providing real income for Canadian investors. United States inflation is expected to run near 3% in 2026, which could limit the scope for aggressive easing and sustain higher term premiums, creating price risk that managers must mitigate in the North America fixed income asset management market.

Segment Analysis

By Source of Funds: Institutional Anchors Drive Stable Demand While Aging Demographics Propel Retail Growth

Institutional allocators, including pension funds and insurance companies, hold a 43.50% share in 2025, driven by liability-matching needs and demand for high-quality duration and diversified credit. U.S. retirement assets, totaling USD 49.6 trillion in 2024, support stable fixed income allocations across DB and DC plans. Public plans in the United States allocate an average of 23% to fixed income, highlighting the need for scalable managers with diverse products. Canada’s CPP segments invest significantly in bonds and credit within CAD 714.4 billion (USD 521.76 billion), anchoring institutional participation in sovereign and credit markets. Insurers favor corporate bonds to align asset duration with liabilities, ensuring consistent credit demand. These structures sustain predictable flows to external managers meeting performance and fiduciary standards in North America’s fixed-income asset management market.

Retail investors are the fastest-growing funding source, with a 4.84% CAGR projected from 2026 to 2031, driven by aging demographics and demand for income preservation. Traditional IRA investors in their sixties allocate 22.5% to bonds, reflecting rising retirement income needs. Bond fund assets reached USD 5,500.8 billion in November 2025, with steady inflows, while ETFs offer liquidity and low fees. Municipal inflows of USD 47 billion in 2025 highlight tax-aware strategies. Cross-border exposure adds diversification but requires currency management. Retail channels and advisory platforms are expanding their role in North America’s fixed-income asset management market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Fixed Income Type: Core Strategies Dominate While Alternative Credit Captures Highest Growth on Yield-Seeking Demand

Core fixed income holds 64.80% in 2025, reflecting the foundational need for high-quality duration, investment-grade corporates, and municipal securities at the center of diversified portfolios. United States Treasury securities outstanding stand at USD 28.7 trillion, with corporate bonds at USD 11.4 trillion in Q3 2025, which shows the depth that supports benchmark-oriented core mandates. Issuance and secondary volume remain high in 2025, providing liquidity and flexibility for managers implementing duration and sector strategies across mandates. Core bond funds represent the central allocation channel for many DC plans and retail households, and the asset base of USD 5,500.8 billion as of November 2025 mirrors that importance. Intermediate investment grade yields near 5% at year-end 2024, and index yield-to-worst measures in late 2025 maintain the attractiveness of core exposures for income and risk balancing. This level and breadth of core demand remains the anchor of the North America fixed income asset management market as investors balance return targets with volatility management.

Alternative credit records the highest projected growth at a 6.54% CAGR through 2031, led by private credit, direct lending, and other non-traditional credit strategies that help close funding gaps as syndicated markets repriced. The global private credit asset class is valued near USD 1.5 trillion with fundraising at USD 59 billion in Q1 2025, and North America-focused allocations led activity. Return experience in 2024 shows competitive outcomes versus high-yield bonds and leveraged loans, which sustains allocator interest across cycles. Fund managers expand capabilities in infrastructure debt and private credit to meet institutional demand for higher income and diversification. Closed-end credit vehicles provide another route to access, with selective use of leverage and derivatives to manage income and risk. As institutions and qualified retail channels build allocations, alternative credit becomes a larger source of flows into the North America fixed income asset management market.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Type of Asset Management Firms: Integrated Platforms Maintain Share While Mutual Fund-ETF Complexes Lead Growth on Passive Shift

Large financial institutions and bulge-bracket platforms hold a significant 28.76% of assets in 2025. They utilize integrated research, trading, and distribution to serve institutions and intermediaries effectively. Bank-affiliated managers combine primary and secondary market insights with product development in credit and rates, ensuring strong representation in both active and index vehicles. Regulatory discussions on capital and Treasury clearing intersect with dealer capacity and liquidity provision, which are critical for institutional execution. Their product offerings include sovereign, corporate, securitized, and liquidity solutions, addressing mandates from cash to long duration. These firms’ scale supports operations, risk systems, and client service capabilities across North America, reinforcing their central role in the fixed income asset management market.

Mutual funds and ETF complexes are projected to grow at a 5.48% CAGR through 2031, driven by passive adoption and targeted active strategies. A leading manager reported USD 164 billion in fixed income net inflows in 2024, with USD 112 billion in ETFs and USD 42 billion in non-ETF indices, reflecting the shift toward index exposures. Another provider, managing over USD 11 trillion in assets, highlights substantial ETF scale and a cost model aligned with shareholder interests. Index bond funds reached USD 2,905.5 billion by late 2025, while active fixed income continues to outperform benchmarks in many periods. Specialist managers face fee compression but remain competitive where alpha is evident, creating a balanced market where scale indexing and targeted active strategies coexist.

Geography Analysis

The United States fixed-income market remains a cornerstone of the region, supported by expanding outstandings and robust secondary trading. Fixed income securities totaled USD 48.9 trillion in Q3 2025, reflecting a 5.6% year-over-year growth across Treasuries, corporates, and other segments. Average daily trading volume reached USD 1.4 trillion, ensuring strong execution quality. The effective federal funds rate was 3.64%, and the 10-year yield stood at 4.18% as of January 9, 2026. Balance sheet management shifted in late 2025 to prioritize reserves, signaling an evolving liquidity framework. Central clearing mandates are driving operational readiness to enhance market resiliency in North America's fixed-income asset management market.

Canada's fixed income market is characterized by a sophisticated mix of sovereign, provincial, and corporate issuances, alongside leading green bond frameworks. The Bank of Canada maintained its policy rate at 2.25% as of December 10, 2025, with headline CPI at 2.2% in October 2025 and core inflation between 2.5% and 3%. Government of Canada 10-year and 30-year yields were 3.38% and 3.82%, respectively, on January 9, 2026. Sovereign green bond issuance remains active, highlighted by a CAD 2.5 billion (USD 1.82 billion) 10-year issuance in October 2025, which included nuclear expenditures in the green framework. Ontario, the largest CAD green bond issuer, continues to provide a pipeline of ESG-aligned projects. Non-residents and Canadian pension plans hold a significant share of GoC bonds, reflecting Canada’s integration into global fixed income allocations.

Institutional investors play a critical role in both countries. CPP Investments reported CAD 714.4 billion (USD 521.76 billion) in assets, with 26% allocated to government bonds and credit as of March 31, 2025. PSP Investments managed CAD 299.7 billion (USD 218.88 billion) in net AUM with substantial fixed income exposures. These institutions support liquidity and influence credit demand. Corporate bond issuance and secondary trading remain strong, while advancements in electronic and portfolio trading enhance execution. ESG frameworks in Canada and United States product innovations expand the investable universe, ensuring depth and diversity in North America's fixed income asset management market.

Competitive Landscape

Competitive Landscape

The North America fixed income asset management market is driven by global platforms, major index providers, and specialized managers in municipal, credit, and multi-sector strategies. A leading manager reported significant total assets under management (AUM), with a substantial portion allocated to fixed income and notable net inflows during the year. Another firm, with a large global AUM, emphasized its ETF scale and client-aligned cost structure. Specialist firms excel in securitized, multi-sector, and credit opportunities, supported by strong performance records and client relationships. Larger platforms utilize technology-driven models and broad distribution networks to achieve scale benefits across ETFs, mutual funds, and separate accounts, fostering a dynamic market environment.

Technology integration, product diversification, and private market expansion are key strategies. One firm’s investment platform generated significant revenue from technology services. Another firm initiated a multi-year effort to unify technology across asset classes. A platform’s acquisition of a major infrastructure manager added substantial fee-paying AUM and enhanced infrastructure debt capabilities. New products, including short-duration ETFs and liquidity vehicles, addressed income needs amid higher rates. These initiatives reflect a focus on client solutions through data, analytics, and diversified returns.

Competitive pressures are evident in fee rate declines and fund flow patterns. Active managers faced revenue challenges due to lower-fee vehicles and mix shifts, with some specialist platforms experiencing long-term net outflows. However, index bond funds attracted significant inflows. Active fixed income remains vital in defined contribution plans, addressing diversification and downside risk management. Corporate and municipal market depth, portfolio trading, and electronic venues enhance strategy execution. Scale, cost efficiency, alpha generation, and technology define competition in this market.

North America Fixed Income Assets Management Industry Leaders

BlackRock

PIMCO

The Vanguard Group

Franklin Templeton

Fidelity Investments

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2025: Ontario Financing Authority issued CAD 2.1 billion (USD 1.53 billion) in dual-tranche green bonds, bringing total green issuance to CAD 24.6 billion (USD 17.96 billion) and reinforcing Ontario’s position in sustainable debt.

- November 2025: The United States banking agencies finalized changes to certain capital standards, including SLR adjustments with implications for Treasury market-making capacity across dealer balance sheets.

- March 2025: SEC voted to end its defense of the March 2024 climate disclosure rule, altering U.S. ESG reporting trajectories for public companies and asset managers.

North America Fixed Income Assets Management Market Report Scope

The fixed income asset management market refers to the organized industry of investment products and strategies focused on bonds, credit instruments, and other income‑oriented securities. It plays a critical role in providing stable returns, diversification, and predictable income streams for pension funds, insurers, asset managers, and retail investors. The market is shaped by strong institutional demand, aging demographics driving preference for low‑risk investments, rising adoption of passive fixed income products such as bond ETFs, and growing capital flows into ESG‑focused instruments. Advanced analytics, AI integration, and high liquidity in the United States further enhance portfolio construction, risk assessment, and sustained participation in fixed income markets.

The market is segmented by source of funds, fixed income type, type of asset management firms, and geography. By source of funds, it includes pension funds and insurance companies, retail investors, institutional investors, government and sovereign wealth funds, and others, reflecting the diverse investor base driving demand. By fixed income type, the market is divided into core fixed income and alternative credit, capturing both traditional bond strategies and innovative credit solutions. By type of asset management firms, the market spans large financial institutions and bulge bracket banks, mutual funds, ETFs, private equity and venture capital firms, fixed income funds, managed pension funds, and others, highlighting the breadth of providers offering fixed income products. By geography, the market covers the United States, Canada, and the rest of North America, with the United States leading due to its depth, liquidity, and institutional participation. The report offers market size and forecasts for the North America Fixed Income Assets Management Market in terms of transaction volume and/or revenue (USD) for all the above segments.

By Source of Funds

| Pension Funds and Insurance Companies |

| Retail Investors |

| Institutional Investors |

| Government/Sovereign Wealth Fund |

| Others |

By Fixed Income Type

| Core Fixed Income |

| Alternative Credit |

Type of Asset Management Firms

| Large financial institutions/Bulge bracket banks |

| Mutual Funds ETFs |

| Private Equity and Venture Capital |

| Fixed Income Funds |

| Managed Pension Funds |

| Others |

By Geography

| United States |

| Canada |

| Rest of North America |

| By Source of Funds | Pension Funds and Insurance Companies |

| Retail Investors | |

| Institutional Investors | |

| Government/Sovereign Wealth Fund | |

| Others | |

| By Fixed Income Type | Core Fixed Income |

| Alternative Credit | |

| Type of Asset Management Firms | Large financial institutions/Bulge bracket banks |

| Mutual Funds ETFs | |

| Private Equity and Venture Capital | |

| Fixed Income Funds | |

| Managed Pension Funds | |

| Others | |

| By Geography | United States |

| Canada | |

| Rest of North America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size and growth outlook for the North America fixed income asset management market?

The North America fixed income asset management market size is USD 26.78 billion in 2026 and it is projected to reach USD 30.2 billion by 2031 at a 2.44% CAGR.

Which investor groups are driving the most demand in North America?

Pension funds and insurance companies lead with 43.50% in 2025 due to liability matching, while retail investors are the fastest growing with a projected 4.84% CAGR through 2031, supported by aging demographics and income needs.

Which strategy segments are largest and fastest growing?

Core fixed income holds 64.80% given demand for high-quality duration and diversified credit, while alternative credit is the fastest growing with a 6.54% CAGR on rising private market allocations

How are passive bond funds affecting the competitive landscape?

Index bond funds now account for 37.6% of bond fund assets and continue to attract strong flows, which increases the importance of scale and cost leadership across ETFs and mutual funds

What macro and policy factors most influence near-term returns?

The effective federal funds rate is 3.64% as of January 9, 2026 and U.S. 10-year yields are near 4.18%, while the Bank of Canada policy rate is 2.25% and GoC 10-year yields are 3.38%, shaping duration returns and curve positioning.

Which recent developments should asset managers in North America track?

Treasury clearing mandates, changes to U.S. capital rules, Canada’s sovereign green bond program, and product launches such as new short duration bond ETFs are key updates with operational and allocation implications .