North America Facility Management Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

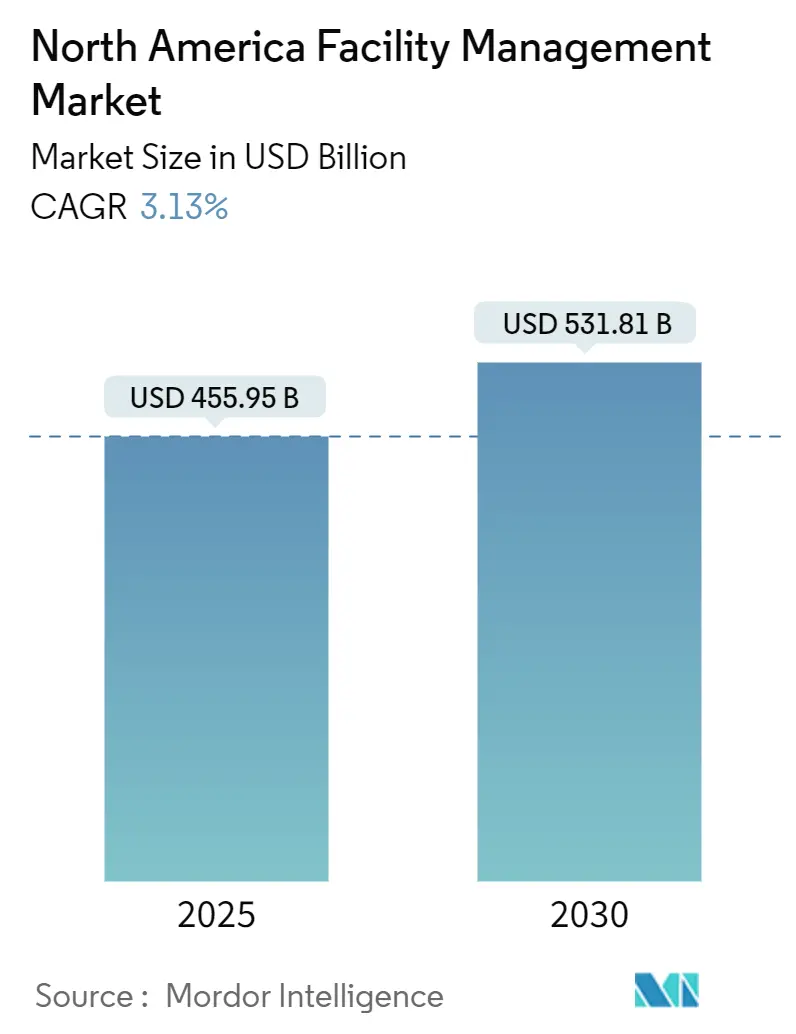

| Market Size (2025) | USD 455.95 Billion |

| Market Size (2030) | USD 531.81 Billion |

| Growth Rate (2025 - 2030) | 3.13% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Facility Management Market Analysis by Mordor Intelligence

The North America facility management market size stands at USD 455.95 billion in 2025 and is forecast to reach USD 531.8 billion by 2030, reflecting a 3.13% CAGR during the period. This expansion traces back to steady infrastructure modernization, stringent regulatory compliance, and rapid technology infusion that are reshaping service delivery across the region. Hard services remain the bedrock as mechanical, electrical, and plumbing (MEP) assets age, whereas soft services gain momentum thanks to heightened hygiene, sustainability, and security expectations. A decisive turn toward outsourcing is visible as enterprises protect core competencies while transferring non-core, capital-intensive tasks to specialized vendors. Coupled with hybrid-work policies and accelerating ESG mandates, these dynamics anchor a resilient, yet maturing North America facility management market.

Key Report Takeaways

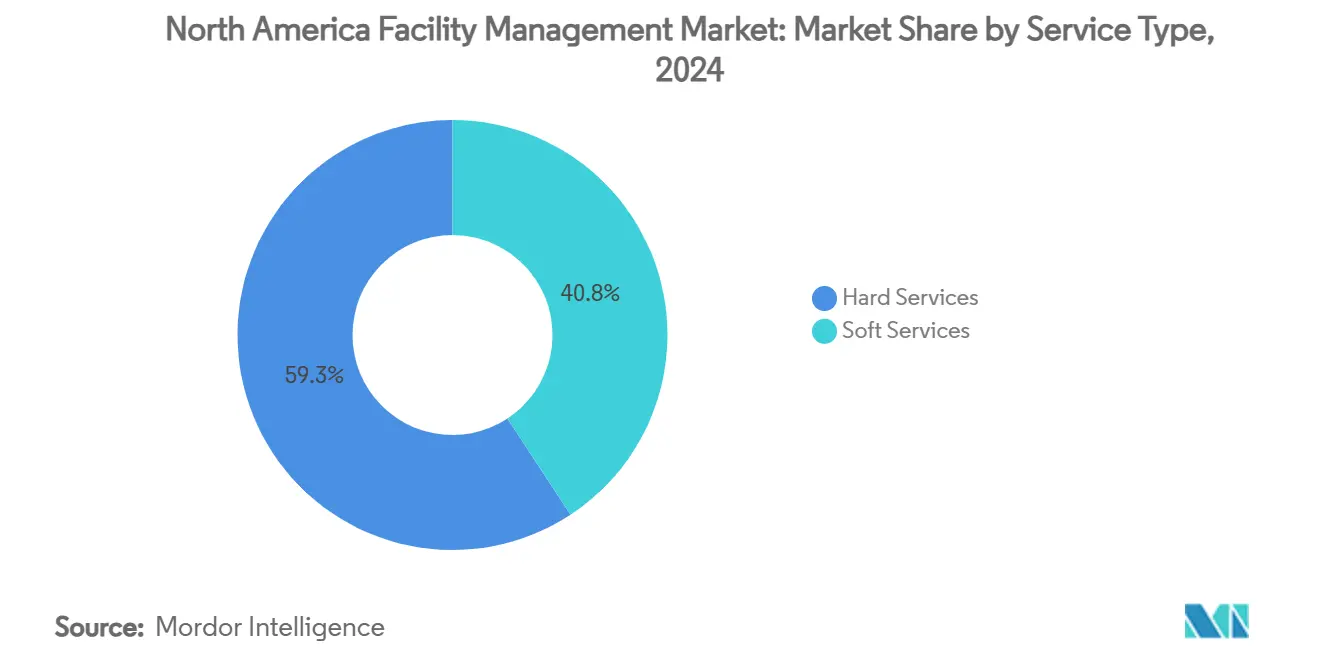

- By service type, hard services commanded 59.25% market share of the North America facility management market in 2024, while soft services exhibit the fastest advance at a 4.21% CAGR through 2030.

- By offering type, outsourced models held 66.05% of the North America facility management market size in 2024 and are projected to expand at 5.06% CAGR to 2030.

- By end-user, the commercial segment captured 40.23% of the North America facility management market share in 2024; institutional and public infrastructure is poised for the steepest climb at 6.25% CAGR to 2030.

- By country, the United States retained 80.41% of the North America facility management market in 2024, whereas Mexico is forecast to register the highest 5.78% CAGR through 2030.

North America Facility Management Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Infrastructure Development | +0.8% | North America, with stronger impact in Mexico and Canada | Medium term (2-4 years) |

| Rising Outsourcing in Building Management | +0.6% | Global, with highest penetration in United States | Short term (≤ 2 years) |

| Heightened Safety and Security Needs | +0.5% | North America, driven by regulatory changes | Short term (≤ 2 years) |

| Technological Advancements in Facility Management | +0.4% | Global, with early adoption in United States | Medium term (2-4 years) |

| Sustainability & ESG Compliance Pressures on Building Operations | +0.3% | North America, with regulatory focus in Canada | Long term (≥ 4 years) |

| Hybrid-Work Models Driving Demand for Flexible FM Solutions | +0.2% | North America, concentrated in commercial sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Infrastructure Development

Federal, state, and provincial mandates across the region elevate building performance thresholds, pushing asset owners to retrofit outdated HVAC, life-safety, and electrical systems. The U.S. General Services Administration’s 2024 P100 standards strengthen sustainability and resiliency criteria for federal properties, setting a template for private portfolios.[1]U.S. General Services Administration, “2024 P100, Facilities Standards,” gsa.gov Mexico’s push to accommodate nearshoring-driven industrial expansion offsets political budget constraints yet sustains demand for high-spec logistics and assembly space. In Canada, harmonized construction codes aimed at meeting climate targets are amplifying energy-efficiency retrofits. Hard-service contractors with deep MEP expertise are consequently seeing stable recurring revenue streams, while technology-enabled monitoring platforms reinforce compliance and extend asset life cycles within the North America facility management market.

Rising Outsourcing in Building Management

Corporate boards increasingly frame FM as a strategic lever rather than a commodity cost center. ABM Industries secured more than USD 1 billion in new contracts during 2024 as clients prioritized integrated offerings that limit vendor sprawl and guarantee single-point accountability. Bundled hard-plus-soft contracts improve economies of scale and often embed outcome-based KPIs tied to safety, uptime, and energy targets. For healthcare, vendor-neutral strategies such as Medxcel’s generated USD 104 million savings over three years by fine-tuning in-house resources and third-party spend. As a result, the outsourced slice of the North America facility management market is widening, with providers that can demonstrate transparent performance reporting and digital toolsets attracting multi-year, multi-site deals.

Heightened Safety and Security Needs

Regulatory shifts intensify cost-of-compliance pressures. OSHA’s forthcoming Heat Injury and Illness Prevention rule obliges employers to formalize mitigation plans, which cascade directly into new service scopes for FM providers in construction, manufacturing, and logistics.[2]OSHA, “Heat Injury and Illness Prevention in Outdoor and Indoor Work Settings,” osha.gov The revised Hazard Communication Standard additionally obliges refreshed chemical labeling and documentation, nudging cleaning and maintenance contracts toward higher technical rigor. Schools and universities are installing advanced surveillance, access control, and space-reconfiguration solutions to strengthen situational awareness while preserving learning environments. Vendors capable of integrating physical security with building automation and data analytics are, therefore, gaining a competitive edge in the North America facility management market.

Technological Advancements in Facility Management

AI, IoT, and edge-enabled platforms now underpin predictive maintenance, asset tracking, and energy optimization across varied property types. Case studies on HVAC systems show 73% downtime reduction and 4% energy gains after AI analytics deployment.[3]ESP International Journal of Advancements in Science & Technology, “AI-Driven Predictive Maintenance in HVAC Systems,” espjournals.org Smart-building nodes are projected to grow to 115 million installations by 2026, expanding the data universe for continuous commissioning and fault detection. Industrial leaders such as Eaton have leveraged Factory Insights-as-a-Service to boost overall equipment effectiveness by up to 15% across more than 200 plants. In the North America facility management market, service providers that bundle robust cybersecurity and scalable cloud architectures with their mobile workforce applications position themselves as indispensable partners for asset owners.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Security concerns over device and network vulnerabilities | -0.4% | North America, with heightened focus in United States | Short term (≤ 2 years) |

| High costs of advanced tech and skilled labor | -0.3% | Global, with acute impact in Canada and United States | Medium term (2-4 years) |

| Fragmented State-Level Labor Regulations Increasing Compliance Burden | -0.2% | United States, with varying impact across states | Medium term (2-4 years) |

| Limited Digital Maturity among Small & Mid-Sized FM Providers | -0.2% | North America, concentrated in mid-market segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Security Concerns Over Device and Network Vulnerabilities

Cyberattacks on BMS and IoT endpoints expose life-safety, HVAC, and access-control layers to potential sabotage, with 27% of facility managers reporting incidents over the past year. Insurance premiums for cyber coverage in critical infrastructure have spiked, further delaying large-scale rollouts. Healthcare and government campuses, sitting on sensitive data and mission-critical systems, demand end-to-end encryption, zero-trust frameworks, and 24/7 threat monitoring, raising barriers for smaller FM providers and elongating sales cycles across the North America facility management market.

High Costs of Advanced Tech and Skilled Labor

Skilled-trade wage escalations continue, with construction pay rising 4.4% in 2024 and forecast to remain above historical averages. Simultaneously, refrigerant phase-outs under EPA guidelines inflate replacement costs, with R-410A volatility squeezing HVAC budgets. These dynamics pressure service margins and elevate bid prices, especially for mid-size FM firms with limited economies of scale. Although technology promises lifecycle savings, upfront capex still deters prospective adopters, moderating overall growth velocity in the North America facility management market.

Segment Analysis

By Service Type: Hard Services Sustain the Market Core

Hard services account for 59.25% of the North America facility management market in 2024 and progress in lock-step with overall expansion at a 3.13% CAGR to 2030. This branch anchors operational continuity through disciplined MEP upkeep, fire-safety compliance, and structural asset preservation. Widespread building-system obsolescence and code updates around energy and life-safety create predictable demand for retrofit programs, condition-based monitoring, and asset-lifecycle planning.

Soft services, although smaller, rise faster at a 4.21% CAGR driven by wellness, security, and concierge expectations. Elevated indoor-air-quality protocols and health-security certifications fuel premium cleaning packages. Office support and front-of-house roles increasingly integrate smart-locker and visitor-management technologies, broadening scope. This divergence positions integrated suppliers to cross-sell soft-service innovations while defending recurring hard-service annuities, thereby enhancing wallet share inside the North America facility management market.

By Offering Type: Outsourced Partnerships Outpace In-house Models

Outsourcing commands 66.05% of the North America facility management market size in 2024 and is slated for 5.06% CAGR growth through 2030. C-suite leaders view integrated FM partnerships as accelerators of operational resilience, tapping provider scale for 24/7 coverage, multi-trade expertise, and investment in cutting-edge platforms. Single-provider governance reduces audit complexity and embeds performance-based incentives, a popular feature across data-center, aviation, and pharma portfolios.

Conversely, in-house delivery retains 33.95% share. Healthcare systems and high-security government installations often preserve direct staff for immediate patient or mission mandates. Still, these operators increasingly pursue hybrid models, outsourcing specialized tasks—like vertical transportation or energy analytics—while retaining custodial or biomedical engineering roles. Cost parity analyses repeatedly tip the balance toward external expertise where asset mix is diverse, underpinning the steady drift toward outsourcing in the North America facility management market.

By End-user Industry: Commercial Dominance Meets Institutional Upswing

Commercial estates—encompassing corporate offices, retail chains, and omnichannel warehouses—held 40.23% of North America facility management market share in 2024. Adaptive-reuse projects and coworking conversions sustain FM volume as landlords right-size footprints yet heighten amenity packages. Smart-locker support, tenant-experience apps, and demand-controlled ventilation are now standard contract inclusions.

Institutional and public-infrastructure properties, while smaller, register a brisk 6.25% CAGR on the back of multi-billion-dollar school and transit modernization programs. Deferred-maintenance backlogs create robust pipelines for roofing, envelope, and mechanical replacements. Healthcare campuses sustain steady activity as regulatory bodies tighten infection-control and emergency-preparedness requirements. Industrial/manufacturing plants cushion cyclical risk, integrating predictive-maintenance suites and energy-optimization audits to maintain uptime. Collectively, these varied demand nodes strengthen diversification, limiting downside risk for the North America facility management market.

Geography Analysis

The United States dominates with 80.41% share of the North America facility management market and benefits from extensive real-estate stock, entrenched outsourcing culture, and a deep vendor ecosystem. Federal incentives such as the Section 179D tax deduction inject fresh capex into energy-efficient retrofits, while the GSA’s new P100 standards raise the bar for performance outcomes. Major providers like EMCOR Group, forecasting up to USD 16.9 billion revenue in 2025, leverage nationwide branch networks to serve multi-site clients. Early AI-driven FM adoption and a large base of mission-critical campuses ensure sustained technology investment.

Canada contributes a moderate slice yet sees policy-driven tailwinds. Harmonized energy codes and carbon-reporting schemes force deep-retrofit projects, opening avenues for providers versed in ESG analytics. Labor-code amendments banning replacement workers from June 2025 heighten contingency-planning demand, and provincial facility-temperature rules add operational complexity. Market participants thus favor partners offering workforce-management agility and bilingual service desks, bolstering the North America facility management market.

Mexico presents the fastest 5.78% CAGR owing to nearshoring as manufacturers localize supply chains closer to U.S. consumption zones. New industrial parks in Bajío and northern corridors require construction quality oversight, commissioning, and ongoing technical FM. While federal budget constraints temper public-sector outlays, private equity pours capital into logistics warehouses and assembly plants, creating greenfield opportunities. FM suppliers that can deploy bilingual technicians and align with international EHS standards stand to capture share and diversify risk across the broader North America facility management market.

Competitive Landscape

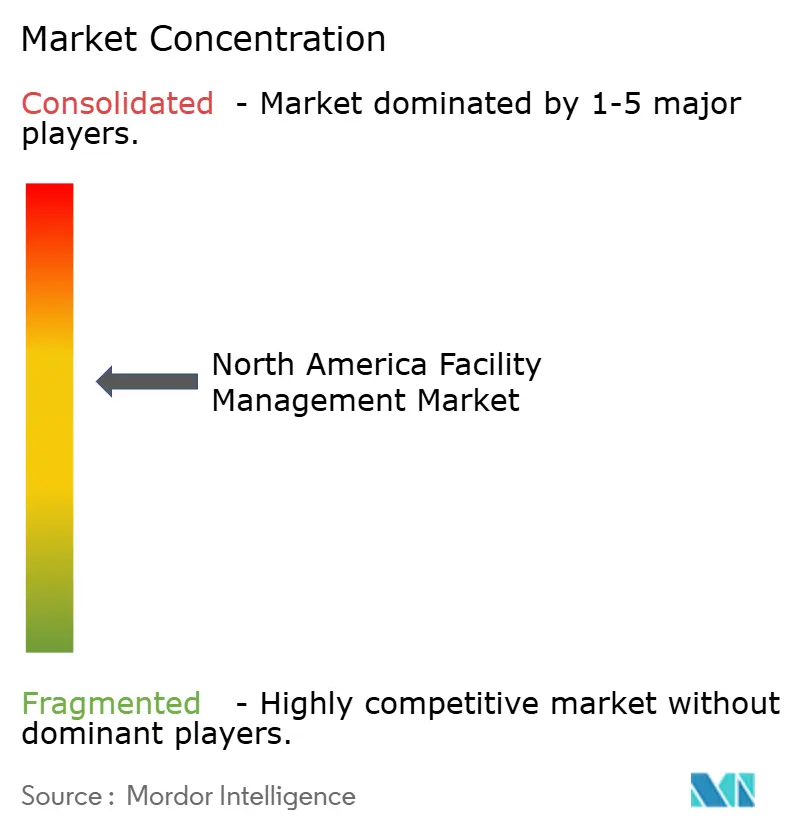

The North America facility management market is moderately consolidated: the five largest vendors hold an estimated 45-50% combined revenue, providing scale economies yet leaving room for regional specialists. EMCOR Group tops the table with USD 14.57 billion revenue in 2024 and backlog growth of 14.2%, underscoring a balanced mix of construction and services. ABM Industries, meanwhile, expanded its data-center footprint via the USD 119 million acquisition of Quality Uptime Services to deepen mission-critical domain knowledge. International conglomerates such as ISS and Compass Group continue to evolve through digital investments, targeting AI enabled help-desks and robotic floor-care to enhance labor productivity.

Technology innovation constitutes the primary differentiator. Providers rapidly embed IoT sensors, real-time CMMS, and analytics dashboards to deliver condition-based maintenance and greenhouse-gas reporting. Patent filings in demand-responsive heat pumps and autonomous inspection drones signal an arms race to capture high-margin smart-service niches. Elsewhere, partnerships between vendors and prop-tech start-ups accelerate rollouts of workplace-experience applications that integrate access control, environmental monitoring, and mobile concierge features.

M&A remains a central growth lever. Construction Briefing anticipates a surge in contractor consolidation during 2025 as founders seek succession exits and private-equity dry powder converts to platform plays. Such roll-ups aim to expand geographic scope, add specialty trades, and unlock cross-selling of bundled FM packages. For buyers, immediate synergies stem from shared procurement, centralized scheduling, and unified data platforms-all pillars that can amplify competitiveness in the North America facility management market.

North America Facility Management Industry Leaders

-

CBRE Group, Inc.

-

Emeric Facility Services Llc

-

JLL (Jones Lang LaSalle IP, Inc.)

-

Cushman and Wakefield PLC

-

SMI Facility Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: EMCOR Group disclosed record USD 14.57 billion FY 2024 revenue and projects USD 16.1-16.9 billion in 2025; management attributes growth to backlog conversion and cross-sell success across construction and services.

- January 2025: The U.S. Department of Energy introduced the 179D Portal, simplifying deduction calculations and expected to accelerate building-retrofit pipelines, thereby creating incremental demand for energy-focused FM contracts.

- December 2024: Compass Group, Aramark, and Sodexo each reported FY 2024 revenue growth and highlighted AI-driven culinary-service platforms that integrate with building-management data to optimize footfall-based staffing.

- November 2024: Siemens, SwiftConnect, and Fortive executed software acquisitions and API integrations to broaden cloud-native FM suites, signaling intensifying competition in analytics-rich service orchestration.

North America Facility Management Market Report Scope

Facility management (FM) services involve the management of building upkeep, utilities, maintenance operations, waste services, security, etc. These services are further segmented by hard facility management services and soft facility management services. The adoption of FM solutions and services is likely to be driven by several factors, including an increase in demand for cloud-based FM solutions and a rise in demand for FM systems linked to intelligent software.

The North America facility management market is segmented by type (in-house facility management, outsourced facility management, (single fm, bundle fm, and integrated FM)), offering type (hard FM and soft FM), and end-user vertical (commercial, institutional, public/infrastructure, industrial, and other end-user verticals). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

| Commercial (IT and Telecom, Retail and Warehouses) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| United States |

| Canada |

| Mexico |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

What is the current size of the North America facility management market?

The North America facility management market size is USD 455.95 billion in 2025, with a forecast to reach USD 531.8 billion by 2030.

Which service type leads the market?

Hard services dominate with 59.25% share in 2024, though soft services are expanding faster at a 4.21% CAGR to 2030.

How significant is outsourcing in the region?

Outsourced delivery represents 66.05% of the market and is projected to grow at 5.06% CAGR, reflecting a strong shift away from in-house models.

Which country shows the fastest growth?

Mexico is the quickest-growing geography, expected to register a 5.78% CAGR through 2030 due to nearshoring and industrial expansion.

What technological trend is most transformative for facilities management?

AI-enabled predictive maintenance and IoT analytics are reducing unplanned downtime by as much as 73% and improving energy performance, making them decisive differentiators for service providers.

How do ESG regulations influence market demand?

Enhanced tax incentives and carbon-reporting rules drive deep retrofits and data-centric reporting, prompting owners to partner with FM firms that can deliver measurable emission reductions and compliance documentation.

Page last updated on: