| Study Period | 2017 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Market Size (2024) | USD 18.54 Billion |

| Market Size (2029) | USD 25.64 Billion |

| CAGR (2024 - 2029) | 6.70 % |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order |

North America Engineering Plastics Market Analysis

The North America Engineering Plastics Market size is estimated at 18.54 billion USD in 2024, and is expected to reach 25.64 billion USD by 2029, growing at a CAGR of 6.70% during the forecast period (2024-2029).

The North American engineering plastics industry is experiencing significant transformation driven by technological advancements and changing consumer preferences. The integration of advanced materials, organic electronics, and miniaturization technologies is revolutionizing manufacturing processes across various sectors. The adoption of smart manufacturing practices, powered by artificial intelligence and Internet of Things (IoT) technologies, is reshaping production capabilities and efficiency. The electrical and electronics sector, which generated substantial revenue of USD 576.1 billion in 2022, has emerged as a crucial driver of innovation in the engineering plastics industry, particularly in applications for electric vehicles, autonomous robots, and defense technologies.

The evolution of consumer lifestyle patterns and urbanization has significantly influenced end-user industry dynamics. The packaging sector has witnessed remarkable growth, with North America producing 22.4 million tons of plastic packaging in 2022, representing 16.6% of global production. This surge is primarily attributed to the increasing demand for functional, prepackaged, and convenient food products, driven by changing family demographics and urbanization trends. The rise of the work-from-home culture has also catalyzed demand for electronic devices and components, creating a sustained need for engineering plastics in consumer electronics manufacturing.

The industry is witnessing substantial developments in manufacturing and supply chain optimization. Major industry players are actively expanding their production capabilities through strategic acquisitions and facility expansions. For instance, in 2023, Alfa's acquisition of OCTAL Holding for USD 620 billion significantly enhanced the region's production capacity. Similarly, companies like Indorama Ventures are strengthening their market presence through strategic acquisitions of facilities producing recycled PET, demonstrating a shift towards sustainable manufacturing practices. This reflects broader plastics market trends towards sustainability and efficiency.

Sustainability initiatives and technological innovation are becoming increasingly central to industry development. Companies are investing heavily in research and development to create eco-friendly alternatives and improve recycling capabilities. The industry is witnessing a growing emphasis on developing technical plastics with reduced environmental impact, particularly in packaging applications. This trend is supported by government initiatives and changing consumer preferences, with many manufacturers committing to increasing the use of recycled content in their products. For example, several companies have announced targets to incorporate up to 50% recycled content in their plastic products by 2030, indicating a significant shift towards sustainable manufacturing practices.

North America Engineering Plastics Market Trends

Strong growth of technological innovations to augment the overall growth of the industry

- Electrical and electronics production in North America witnessed a CAGR of over 1.4% between 2017 and 2019 owing to the advancement of technology, coupled with the increasing demand for consumer electronics products, such as smart TVs, refrigerators, air conditioners, and other products. The rapid pace of electronic technological innovation is driving the demand for newer and faster electronic products. As a result, it has also increased the electrical and electronics production in the region.

- Electronic device sales in North America fell by around 9% in 2020 compared to 2019, owing to the COVID-19 impact, because of the production facility shutdowns, supply chain disruptions, and various other constraints. As a result, revenue from electrical and electronics production in the region decreased by 4.7% in 2020 compared to the previous year.

- In 2021, the sales of consumer electronics in the region reached around USD 113 billion, 4% higher than in 2020. As a result, North America’s electrical and electronics production grew by 13.8% in 2021 in terms of revenue compared to the previous year.

- By 2027, North America is projected to be the third-largest region for electrical and electronics production and account for a share of around 10.5% of the global market. The emergence of advanced technologies such as virtual reality, IoT solutions, and robotics into consumer electronic products to achieve efficiency and low cost has provided a significant advantage to the consumer electronics industry. The consumer electronics industry in the region is projected to reach a market volume of around USD 161.8 billion by 2027 from USD 127.6 billion in 2023. As a result, the demand for electrical and electronic products in the region is projected to increase.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- Increasing investments in the civil aviation and defense sectors to drive the industry

- Government initiatives for electric vehicles to support the automotive production

- Strong growth in residential construction to drive the industry

- Evolving lifestyle to increase the plastic packaging applications

- United States to remain as the cornerstone of the regional fluoropolymer trade

- Abundant availability of polyamide raw materials to promote regional resin exports

- Growing automotive industry to create larger regional trade avenues

- North America to remain as a net importer of PET resins

- Increasing domestic consumption to significantly impact the regional PMMA trade

- Local manufacturing presence may be sufficient for the increasing demand for POM

- Increasing domestic production to reduce the regional import dependence

- Resin prices to remain under the influence of crude oil prices in the international market

- Recycling policies from governments in the region to boost the recycling rates of engineering plastics

- Methods being developed to use eco-friendly glycerol to recycle PC to recover up to 98% of the plastic's monomer

- The PET recycling rate in Mexico stood at 56%, the United States at 28.6%, and Canada at 9%

- With growing electrical waste of around 13.1 million tons is an opportunity for many ABS manufacturers across the region to produce R-ABS

Segment Analysis: End User Industry

Packaging Segment in North American Engineering Plastics Market

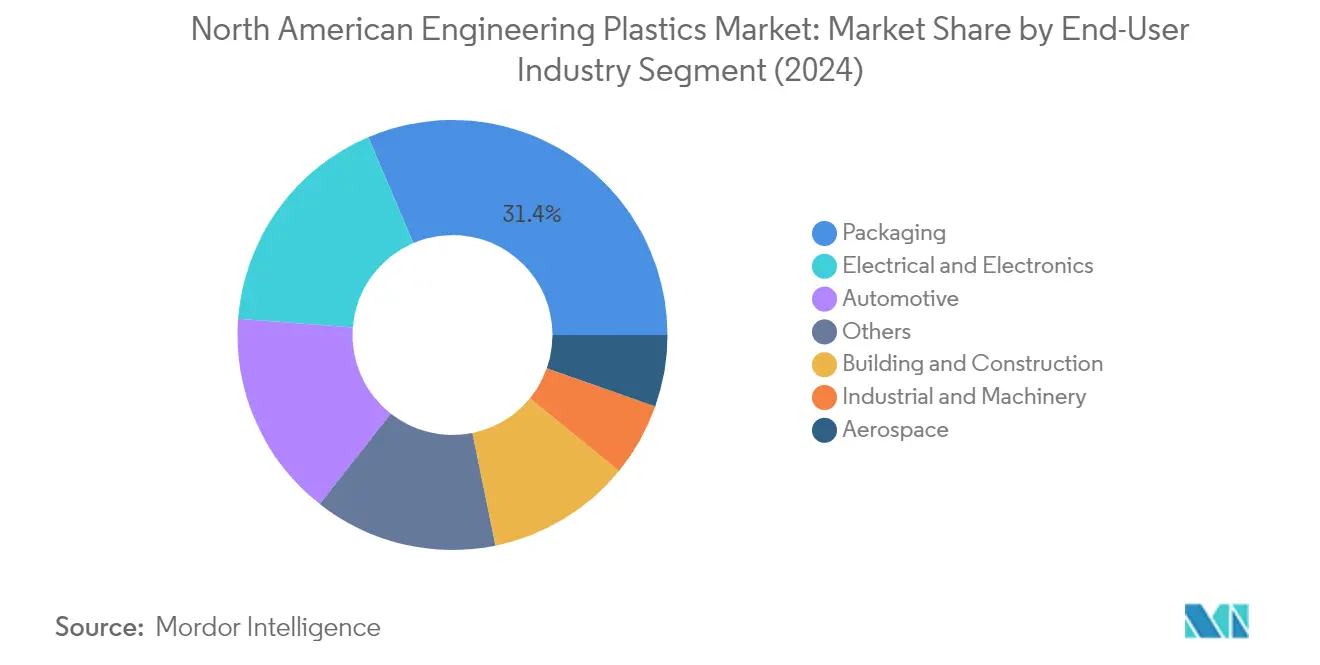

The packaging segment maintains its dominant position in the North American engineering plastics market, accounting for approximately 31% of the total market value in 2024. This leadership is primarily driven by the increasing demand for functional, prepackaged, and convenient food products, stemming from significant changes in urbanization and family demographics across the region. The segment's strength is further reinforced by North America's substantial plastic packaging production volume, which represents about 17% of global production. The growing consumer demand for packaged food and beverages, coupled with busier lifestyles and rising purchasing power, continues to fuel the segment's growth. Additionally, the segment's prominence is supported by the widespread adoption of engineering plastics in various packaging applications, including containers, bottles, drums, trays, boxes, cups, and protective packaging solutions.

Electrical & Electronics Segment in North American Engineering Plastics Market

The electrical and electronics segment is demonstrating remarkable growth potential in the North American engineering plastics market, projected to grow at approximately 9% annually from 2024 to 2029. This accelerated growth is driven by multiple factors, including the rapid adoption of smart manufacturing practices, the integration of advanced materials, and the increasing implementation of organic electronics and miniaturization technologies. The segment's expansion is further fueled by the emergence of disruptive technologies such as artificial intelligence and the Internet of Things. The growth is also supported by the increasing demand for electronic devices, particularly with the rise of work-from-home arrangements and the subsequent need for home office setups. The consistent demand for newer and faster electronic products, coupled with technological innovations, continues to drive the segment's expansion in the region.

Remaining Segments in End User Industry

The other significant segments in the North American engineering plastics market include automotive, building and construction, industrial machinery, and aerospace sectors. The automotive segment plays a crucial role in driving market growth through the increasing adoption of lightweight materials and the growing electric vehicle sector. The building and construction segment contributes significantly through the use of engineering plastics in facades, insulation, and structural components. The industrial machinery segment maintains steady demand through applications in manufacturing equipment and components. The aerospace segment, while smaller in market share, represents a high-value segment with specialized applications in aircraft components and interior materials. Each of these segments contributes uniquely to the market's diversity and overall growth trajectory.

Segment Analysis: Resin Type

PET Segment in North American Engineering Plastics Market

Polyethylene terephthalate (PET) maintains its dominant position in the North American engineering plastics market, commanding approximately 29% market share in 2024. The segment's leadership is primarily driven by its extensive applications in the packaging industry, where it serves as a crucial material for food and beverage containers due to its excellent physicochemical properties, including rigidity and high transparency. PET's popularity stems from its ability to protect food freshness and extend shelf life, while also offering significant advantages as a glass substitute in food packaging applications owing to its extreme lightness, recyclability, and shatterproof characteristics. The material's versatility extends beyond packaging, finding applications in automotive components, building materials, and electrical devices, further solidifying its market leadership.

Styrene Copolymers Segment in North American Engineering Plastics Market

The styrene copolymers (ABS and SAN) segment is emerging as the fastest-growing category in the North American engineering plastics market, projected to achieve approximately 6% volume growth annually from 2024 to 2029. This remarkable growth trajectory is primarily driven by increasing demand from the electrical and electronics industry, where these materials are extensively used in manufacturing housing appliances, laptops, computers, keyboards, and mobile phones. The automotive sector's transition toward lightweight components and the construction industry's growing need for durable materials are further accelerating the segment's expansion. The materials' exceptional properties, including durability, good mechanical and thermal stability, and significant tensile strength, make them increasingly preferred choices across various applications.

Remaining Segments in Resin Type

The North American engineering plastics market encompasses several other significant resin types, each serving unique applications across various industries. Liquid Crystal Polymer (LCP) and Polyether ether ketone (PEEK) demonstrate strong growth potential, particularly in high-performance applications. Polyamide (PA), Polybutylene Terephthalate (PBT), and Polycarbonate (PC) maintain steady market presence in automotive and industrial applications. Fluoropolymers serve specialized applications requiring extreme chemical resistance, while Polymethyl Methacrylate (PMMA) and Polyoxymethylene (POM) cater to specific industrial and consumer needs. Polyimide (PI) continues to serve high-temperature applications in aerospace and electronics sectors, contributing to the market's diversity and technological advancement.

North America Engineering Plastics Market Geography Segment Analysis

Engineering Plastics Market in United States

The United States engineering plastics market dominates the North American engineering plastics market, commanding approximately 81% of the total market value in 2024. The country's market leadership is driven by its robust manufacturing infrastructure, particularly in the automotive plastics and electrical/electronics sectors. The presence of major engineering plastic manufacturers and well-established distribution networks has further strengthened the country's position. The implementation of the United States-Mexico-Canada Agreement (USMCA) has created additional opportunities for domestic manufacturers by enforcing that 75% of components must be manufactured within North America to qualify for zero tariffs. The country's focus on sustainable practices and increasing adoption of recycled engineering plastics has created new market opportunities. The automotive industry's transition towards electric vehicles and lightweight materials has been a significant driver for engineering plastics market demand. Additionally, the growing packaging industry, driven by increasing e-commerce activities and changing consumer preferences for convenient packaging solutions, has sustained market growth.

Engineering Plastics Market in Mexico

Mexico has emerged as the most dynamic market for engineering plastics in North America, projected to grow at approximately 8% annually from 2024 to 2029. The country's strategic geographical location and competitive manufacturing costs have attracted significant investments in various end-user industries. The automotive plastics sector has been particularly instrumental in driving market growth, with several global automotive manufacturers establishing production facilities in the country. The implementation of the USMCA requirements has created new opportunities for local manufacturing, especially in the automotive sector where specific content requirements must be met. The packaging industry has shown remarkable growth potential, driven by changing consumer lifestyles and increasing demand for processed food products. The country's industrial machinery sector has also witnessed substantial growth, supported by government initiatives to modernize manufacturing facilities. Mexico's focus on developing its electronics manufacturing capabilities has further diversified the application scope of industrial plastics.

Engineering Plastics Market in Canada

Canada's engineering plastics market has established itself as a significant contributor to the North American region, supported by its strong manufacturing base and innovative technological capabilities. The country's market is characterized by its focus on sustainable practices and environmental regulations, which have influenced the adoption of recycled and bio-based engineering plastics. The automotive sector remains a crucial end-user, with manufacturers increasingly incorporating engineering plastics to meet stringent emission standards and fuel efficiency requirements. The country's robust aerospace industry has been a consistent consumer of high-performance aerospace plastics, particularly in applications requiring exceptional mechanical and thermal properties. The packaging industry has shown steady growth, driven by increasing demand for sustainable packaging solutions and changing consumer preferences. Canada's strong focus on research and development has led to innovations in engineering plastic applications, particularly in medical devices and renewable energy sectors.

Engineering Plastics Market in Other Countries

The engineering plastics market in other North American countries and territories encompasses various smaller markets that contribute to the region's overall growth. These markets are characterized by their unique industrial focuses and specific application requirements. While their individual market sizes may be smaller, they play important roles in specific niches within the engineering plastics industry. These markets often benefit from the spillover effects of major manufacturing activities in the larger markets and are increasingly integrated into regional supply chains. The implementation of regional trade agreements has created opportunities for these markets to participate in the broader North American engineering plastics value chain. Their growth is often linked to specific industrial sectors where they have developed expertise or competitive advantages. These markets also serve as important testing grounds for new applications and innovations in engineering plastics, particularly in specialized industrial applications.

North America Engineering Plastics Industry Overview

Top Companies in North American Engineering Plastics Market

The North American engineering plastics market is characterized by companies focusing on sustainable innovation and technological advancement to maintain their competitive edge. Major players are investing heavily in research and development to create eco-friendly products, including bio-based and recycled materials, to address growing environmental concerns. Companies are strengthening their market positions through strategic acquisitions and partnerships, particularly to expand their distribution networks and enhance their product portfolios. Operational agility is being achieved through investments in smart manufacturing technologies and supply chain optimization, while capacity expansions are being undertaken to meet growing demand from key end-use industries such as automotive, packaging, and electronics. The industry is also witnessing an increased focus on developing specialized grades for emerging applications in electric vehicles and 5G infrastructure.

Consolidated Market with Strong Global Players

The North American engineering plastics market exhibits a highly consolidated structure dominated by global chemical conglomerates with integrated operations across the value chain. These major players leverage their extensive research capabilities, established distribution networks, and economies of scale to maintain their market positions. The market is characterized by high entry barriers due to significant capital requirements, technical expertise needs, and established customer relationships of incumbent players. Mergers and acquisitions have been a key strategy for market consolidation, with companies acquiring specialized manufacturers to expand their product portfolios and geographic presence.

The competitive landscape is further shaped by the presence of regional specialists focusing on specific product segments or end-user industries, particularly in high-performance technical plastics. These companies compete through product customization, technical support, and close customer relationships. The market has witnessed increased collaboration between manufacturers and end-users for product development, particularly in emerging applications such as electric vehicles and sustainable packaging solutions. Joint ventures and strategic partnerships have become common for technology sharing and market access.

Innovation and Sustainability Drive Future Success

Success in the North American performance plastics market increasingly depends on companies' ability to develop sustainable solutions while maintaining performance standards. Incumbent players are focusing on vertical integration, expanding recycling capabilities, and developing bio-based alternatives to strengthen their market positions. Companies are also investing in digitalization and advanced manufacturing technologies to improve operational efficiency and customer service. The ability to provide complete solutions, including technical support and custom formulations, has become crucial for maintaining a competitive advantage. Market leaders are establishing innovation centers near production facilities to facilitate faster product development and customer response.

For contenders looking to gain market share, specialization in high-growth segments and the development of innovative solutions for specific applications offer promising opportunities. Success factors include building strong relationships with end-users, particularly in emerging industries, and developing sustainable products that meet increasingly stringent environmental regulations. Companies must also focus on building robust supply chains and distribution networks to ensure reliable product availability. The market's future will be shaped by the ability to address increasing demand for lightweight materials in automotive applications, sustainable packaging solutions, and high-performance materials for electronics, while managing regulatory compliance and environmental concerns. The development of advanced polymers and structural plastics will be crucial in meeting these demands.

North America Engineering Plastics Market Leaders

-

Alfa S.A.B. de C.V.

-

Ascend Performance Materials

-

Indorama Ventures Public Company Limited

-

Koch Industries, Inc.

-

SABIC

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

North America Engineering Plastics Market News

- February 2023: Covestro AG introduced Makrolon 3638 polycarbonate for healthcare and life sciences applications such as drug delivery devices, wellness and wearable devices, and single-use containers for biopharmaceutical manufacturing.

- November 2022: Solvay and Orbia announced a framework agreement to form a partnership for the production of suspension-grade polyvinylidene fluoride (PVDF) for battery materials, resulting in the largest capacity in North America.

- November 2022: Celanese Corporation completed the acquisition of the Mobility & Materials (“M&M”) business of DuPont. This acquisition enhanced the company's product portfolio of engineered thermoplastics through the addition of well-recognized brands and intellectual properties of DuPont.

North America Engineering Plastics Market Report - Table of Contents

1. EXECUTIVE SUMMARY & KEY FINDINGS

2. REPORT OFFERS

3. INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4. KEY INDUSTRY TRENDS

-

4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

-

4.2 Import And Export Trends

- 4.2.1 Fluoropolymer Trade

- 4.2.2 Polyamide (PA) Trade

- 4.2.3 Polycarbonate (PC) Trade

- 4.2.4 Polyethylene Terephthalate (PET) Trade

- 4.2.5 Polymethyl Methacrylate (PMMA) Trade

- 4.2.6 Polyoxymethylene (POM) Trade

- 4.2.7 Styrene Copolymers (ABS and SAN) Trade

- 4.3 Price Trends

-

4.4 Recycling Overview

- 4.4.1 Polyamide (PA) Recycling Trends

- 4.4.2 Polycarbonate (PC) Recycling Trends

- 4.4.3 Polyethylene Terephthalate (PET) Recycling Trends

- 4.4.4 Styrene Copolymers (ABS and SAN) Recycling Trends

-

4.5 Regulatory Framework

- 4.5.1 Canada

- 4.5.2 Mexico

- 4.5.3 United States

- 4.6 Value Chain & Distribution Channel Analysis

5. MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

-

5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

-

5.2 Resin Type

- 5.2.1 Fluoropolymer

- 5.2.1.1 By Sub Resin Type

- 5.2.1.1.1 Ethylenetetrafluoroethylene (ETFE)

- 5.2.1.1.2 Fluorinated Ethylene-propylene (FEP)

- 5.2.1.1.3 Polytetrafluoroethylene (PTFE)

- 5.2.1.1.4 Polyvinylfluoride (PVF)

- 5.2.1.1.5 Polyvinylidene Fluoride (PVDF)

- 5.2.1.1.6 Other Sub Resin Types

- 5.2.2 Liquid Crystal Polymer (LCP)

- 5.2.3 Polyamide (PA)

- 5.2.3.1 By Sub Resin Type

- 5.2.3.1.1 Aramid

- 5.2.3.1.2 Polyamide (PA) 6

- 5.2.3.1.3 Polyamide (PA) 66

- 5.2.3.1.4 Polyphthalamide

- 5.2.4 Polybutylene Terephthalate (PBT)

- 5.2.5 Polycarbonate (PC)

- 5.2.6 Polyether Ether Ketone (PEEK)

- 5.2.7 Polyethylene Terephthalate (PET)

- 5.2.8 Polyimide (PI)

- 5.2.9 Polymethyl Methacrylate (PMMA)

- 5.2.10 Polyoxymethylene (POM)

- 5.2.11 Styrene Copolymers (ABS and SAN)

-

5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

6. COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

-

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Alfa S.A.B. de C.V.

- 6.4.2 Arkema

- 6.4.3 Ascend Performance Materials

- 6.4.4 BASF SE

- 6.4.5 Celanese Corporation

- 6.4.6 Covestro AG

- 6.4.7 DuPont

- 6.4.8 Eastman Chemical Company

- 6.4.9 Formosa Plastics Group

- 6.4.10 Indorama Ventures Public Company Limited

- 6.4.11 INEOS

- 6.4.12 Koch Industries, Inc.

- 6.4.13 SABIC

- 6.4.14 Solvay

- 6.4.15 Trinseo

7. KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8. APPENDIX

-

8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter’s Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

North America Engineering Plastics Industry Segmentation

Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging are covered as segments by End User Industry. Fluoropolymer, Liquid Crystal Polymer (LCP), Polyamide (PA), Polybutylene Terephthalate (PBT), Polycarbonate (PC), Polyether Ether Ketone (PEEK), Polyethylene Terephthalate (PET), Polyimide (PI), Polymethyl Methacrylate (PMMA), Polyoxymethylene (POM), Styrene Copolymers (ABS and SAN) are covered as segments by Resin Type. Canada, Mexico, United States are covered as segments by Country.| End User Industry | Aerospace | |||

| Automotive | ||||

| Building and Construction | ||||

| Electrical and Electronics | ||||

| Industrial and Machinery | ||||

| Packaging | ||||

| Other End-user Industries | ||||

| Resin Type | Fluoropolymer | By Sub Resin Type | Ethylenetetrafluoroethylene (ETFE) | |

| Fluorinated Ethylene-propylene (FEP) | ||||

| Polytetrafluoroethylene (PTFE) | ||||

| Polyvinylfluoride (PVF) | ||||

| Polyvinylidene Fluoride (PVDF) | ||||

| Other Sub Resin Types | ||||

| Liquid Crystal Polymer (LCP) | ||||

| Polyamide (PA) | By Sub Resin Type | Aramid | ||

| Polyamide (PA) 6 | ||||

| Polyamide (PA) 66 | ||||

| Polyphthalamide | ||||

| Polybutylene Terephthalate (PBT) | ||||

| Polycarbonate (PC) | ||||

| Polyether Ether Ketone (PEEK) | ||||

| Polyethylene Terephthalate (PET) | ||||

| Polyimide (PI) | ||||

| Polymethyl Methacrylate (PMMA) | ||||

| Polyoxymethylene (POM) | ||||

| Styrene Copolymers (ABS and SAN) | ||||

| Country | Canada | |||

| Mexico | ||||

| United States | ||||

Need A Different Region or Segment?

Customize Now

North America Engineering Plastics Market Research FAQs

How big is the North America Engineering Plastics Market?

The North America Engineering Plastics Market size is expected to reach USD 18.54 billion in 2024 and grow at a CAGR of 6.70% to reach USD 25.64 billion by 2029.

What is the current North America Engineering Plastics Market size?

In 2024, the North America Engineering Plastics Market size is expected to reach USD 18.54 billion.

Who are the key players in North America Engineering Plastics Market?

Alfa S.A.B. de C.V., Ascend Performance Materials, Indorama Ventures Public Company Limited, Koch Industries, Inc. and SABIC are the major companies operating in the North America Engineering Plastics Market.

Which segment has the biggest share in the North America Engineering Plastics Market?

In the North America Engineering Plastics Market, the Packaging segment accounts for the largest share by end user industry.

Which country has the biggest share in the North America Engineering Plastics Market?

In 2024, United States accounts for the largest share by country in the North America Engineering Plastics Market.

What years does this North America Engineering Plastics Market cover, and what was the market size in 2023?

In 2023, the North America Engineering Plastics Market size was estimated at 18.54 billion. The report covers the North America Engineering Plastics Market historical market size for years: 2017, 2018, 2019, 2020, 2021, 2022 and 2023. The report also forecasts the North America Engineering Plastics Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Our Best Selling Reports

North America Engineering Plastics Market Research

Mordor Intelligence provides a comprehensive analysis of the engineering plastics industry. We specialize in evaluating industrial plastics and performance plastics across North America. Our extensive research covers key materials such as polycarbonate, polyamide, ABS plastic, and polyacetal. We also examine crucial applications in the automotive plastics and aerospace plastics sectors. The report PDF, available for download, offers in-depth insights into advanced polymers and industrial polymers, with a particular focus on technical plastics applications.

Stakeholders gain valuable insights into emerging trends in heat resistant plastics and high temperature plastics, which are essential for modern manufacturing processes. The analysis includes structural plastics and composite plastics, detailing how durable plastics meet evolving industry demands. Our research thoroughly examines specialty plastics like PEEK plastic, providing strategic intelligence for businesses investing in thermoplastic solutions. The report offers a detailed analysis of reinforced plastics applications across various sectors, supporting informed decision-making in the rapidly evolving North American plastics industry.