Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2031 |

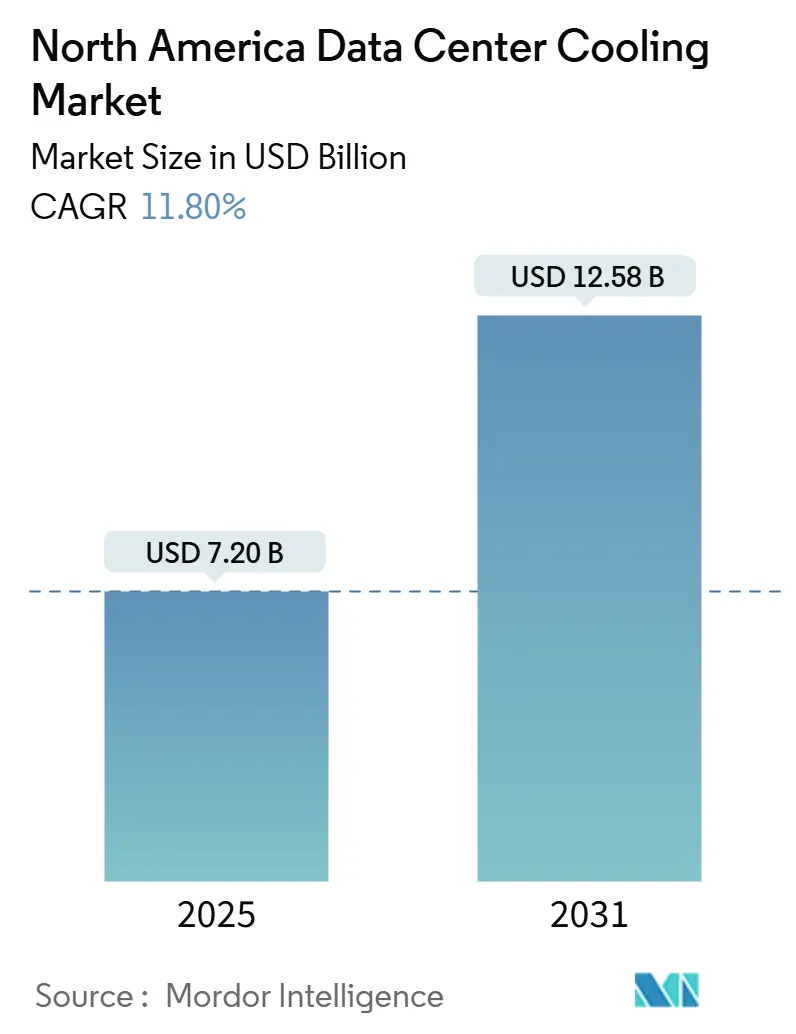

| Market Size (2025) | USD 7.20 Billion |

| Market Size (2031) | USD 12.58 Billion |

| Growth Rate (2025 - 2031) | 11.80% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Data Center Cooling Market Analysis by Mordor Intelligence

The North America data center cooling market size reached USD 7.2 billion in 2025 and is projected to advance at an 11.80% CAGR, arriving at USD 12.58 billion by 2031. Rapid expansion of artificial-intelligence infrastructure, escalating rack densities above 100 kW, and regulatory pressure to improve power-usage effectiveness are reshaping the North America data center cooling market. Operators are replacing legacy computer-room air conditioners with liquid systems that remove up to 300 times more heat per rack, while variable-speed chillers and economizers gain favor for incremental efficiency. Colocation providers sustain demand by offering shared, energy-efficient platforms, yet hyperscale owners dominate new capacity additions with aggressive adoption of immersion and direct-to-chip solutions. Vendors that integrate monitoring software, refrigerant-flexible hardware, and heat-reuse capabilities capture an outsized share as buyers seek verifiable sustainability gains. The competitive landscape balances scale advantages of incumbents with the specialized know-how of liquid-cooling start-ups, foreshadowing deeper collaboration across the ecosystem.

Key Report Takeaways

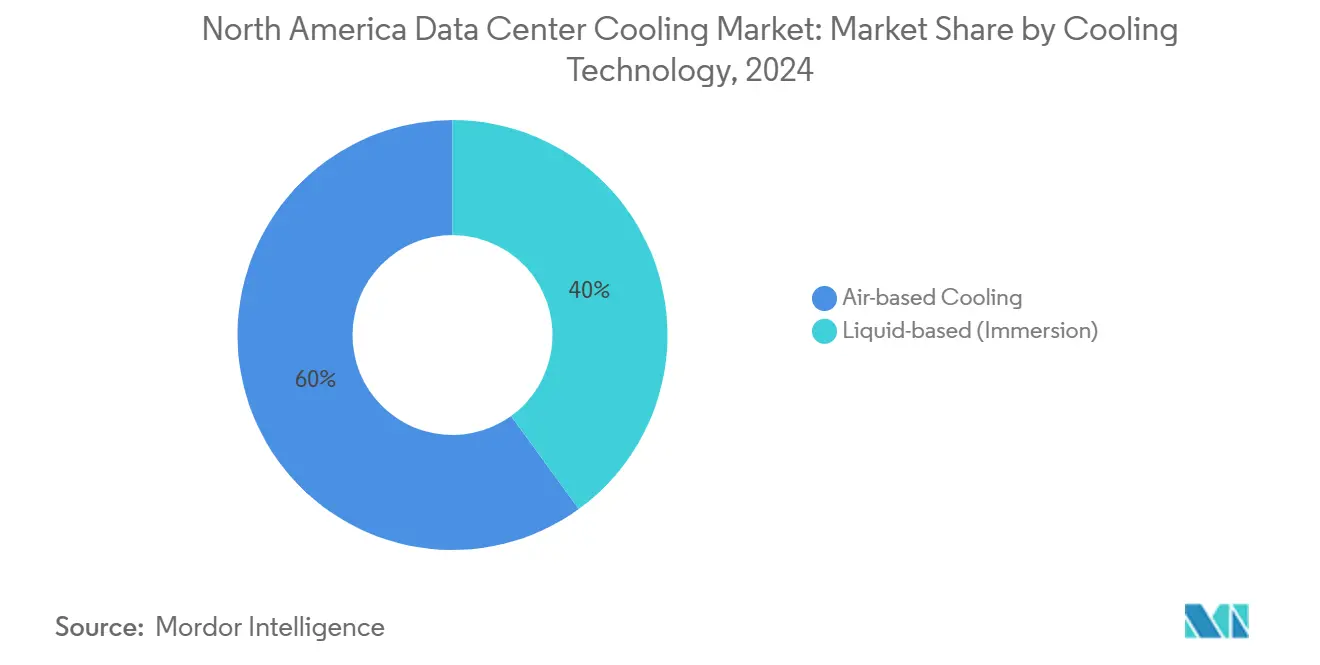

- By cooling technology, air-based systems held 60% of the North America data center cooling market share in 2024, while liquid solutions are expanding at a 12.10% CAGR through 2031.

- By cooling component, CRAH/CRAC units commanded 41% of the North America data center cooling market size in 2024; immersion systems record the fastest 11.9% CAGR to 2031.

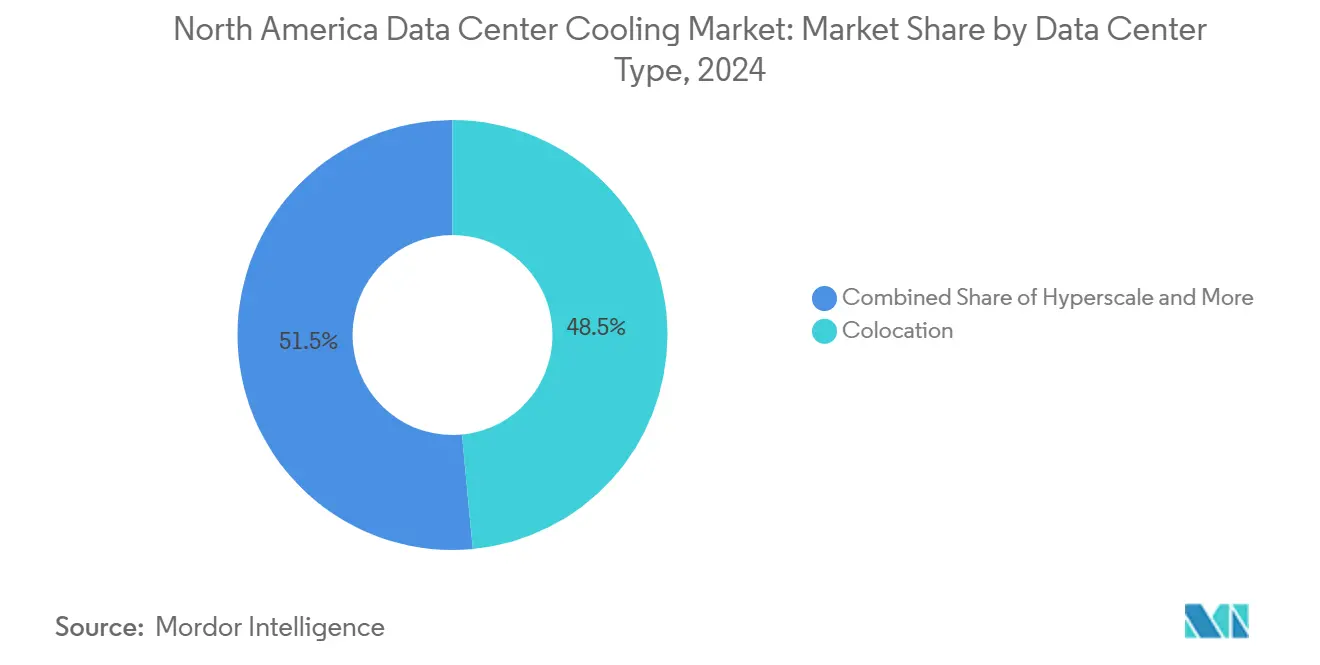

- By data center type, colocation facilities captured 48.50% revenue in 2024, whereas hyperscale sites are advancing at a 14.10% CAGR through 2031.

- By end-user industry, IT and telecom retained a 40% share in 2024; healthcare workloads are set to grow at an 11.80% CAGR during the forecast horizon.

North America Data Center Cooling Market Trends and Insights

Drivers Impact Analysis

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent PUE targets under U.S. Executive Order on Federal Sustainability | +2.1% | United States (DC metro, California) | Medium term (2-4 years) |

| Escalating rack densities in hyperscale facilities | +2.8% | Virginia, Texas, Arizona | Short term (≤ 2 years) |

| Growing adoption of liquid cooling for AI/ML workloads | +3.2% | Seattle, Austin, Atlanta | Short term (≤ 2 years) |

| Data-center tax incentives tied to LEED and ENERGY STAR compliance | +1.5% | Texas, Arizona, North Carolina | Medium term (2-4 years) |

| Edge-data-center growth in Tier-2 metros | +1.8% | Phoenix, Denver, Nashville | Long term (≥ 4 years) |

| Heat-reuse mandates in Canadian provinces | +0.9% | Ontario, British Columbia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent PUE targets under U.S. Executive Order on Federal Sustainability

Federal directives compel agencies to reduce site energy intensity, steering procurement toward high-efficiency chillers, variable-speed drives, and hybrid evaporative systems able to document measurable PUE gains.[1]Johnson Controls, “Everything Your Data Center Needs in One Place,” johnsoncontrols.com Bid specifications increasingly require ENERGY STAR certification and real-time performance reporting, giving vendors with integrated controls an edge. The mandate’s influence extends to contractors hosting government workloads, widening market scope beyond federal campuses. Because appropriations cycles span multiple years, the policy delivers steady demand rather than one-time surges. Manufacturers that pre-qualify equipment on GSA schedules shorten sales cycles and strengthen installed-base stickiness.

Escalating rack densities in hyperscale facilities

Deployment of GPU clusters for generative AI pushes heat flux past thresholds manageable by conventional air, forcing operators to retrofit with direct-to-chip liquid loops capable of dissipating loads above 100 kW per cabinet.[2]Joe Burns, “LiquidStack Makes High-Performance Coolant System Available for Advanced Data Centers,” Facilities Dive, facilitiesdive.com Airflow upgrades alone cannot bridge the gap, so complete mechanical-plant redesigns accelerate capital expenditure. Hyperscalers leverage scale economics to pilot novel dielectric coolants that promise 300x water savings, creating fast-track opportunities for niche fluid suppliers. Rack-density escalation, therefore, operates as both a technology catalyst and an equipment-replacement trigger, compressing refresh timelines to three years or fewer.

Growing adoption of liquid cooling for AI/ML workloads

Machine-learning training doubles compute intensity annually, driving thermal envelopes that exceed CRAC capabilities and hasten adoption of cold-plate and immersion platforms rated at 2,200 W per socket.[3]Trane, “HVAC Systems Transform How Data Centers Are Developed, Designed and Operated,” trane.com Early pilots prove stable PUE below 1.1, persuading cloud providers to standardize across new builds. Colocation operators follow suit, adding liquid-ready suites to attract high-density tenants otherwise lost to hyperscale rivals. Supply-chain partnerships between legacy HVAC majors and liquid start-ups proliferate to de-risk integration. Software that monitors coolant flow and detects micro-leaks becomes essential, expanding revenue beyond hardware.

Data-center tax incentives tied to LEED and ENERGY STAR compliance

Property-tax abatements in Texas, Arizona, and North Carolina link award value to documented efficiency gains, converting sustainability into a line-item return on investment. Operators justify higher upfront spend on low-GWP refrigerants and magnetic-bearing chillers by modeling 10-15-year incentive cash flows. Vendors able to deliver measurement and verification packages lock in service contracts, ensuring annuity-style income. The linkage of fiscal benefits to third-party certification also raises the bar for component quality and transparency.

Restraints Impact Analysis

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Volatility in refrigerant prices amid HFC phase-down | -1.8% | North American manufacturing hubs | Short term (≤ 2 years) |

| Power-grid constraints delaying new builds in Northern Virginia | -2.1% | Virginia / DC metro | Medium term (2-4 years) |

| Limited skills for immersion-cooling maintenance | -1.2% | Secondary markets globally | Long term (≥ 4 years) |

| Insurance-premium surcharges for water-based systems in drought zones | -0.7% | California, Arizona, Nevada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in refrigerant prices amid HFC phase-down

EPA quota cuts lifted the cost of certain HFC blends by up to 300%, straining project budgets and prompting stockpiling behavior that distorts supply. While low-GWP alternatives exist, limited production volume keeps premiums high, raising total system cost for chillers and packaged units. OEMs must retool lines, causing delivery lead-times to spike. Retrofit projects suffer most, as swapping refrigerants demands additional certification and site downtime, delaying revenue realization for facility owners.

Power-grid constraints delaying new builds in Northern Virginia

Dominion Energy halted 60 projects after transmission capacity maxed out, pushing developers toward Texas and the Midwest. Cooling suppliers lose predictable pipeline volume in the nation’s largest cluster and must recalibrate logistics. Delay-driven holding costs discourage speculative construction, dampening near-term equipment orders. Grid upgrades are underway but require multi-year horizons, extending uncertainty.

Segment Analysis

By Cooling Technology: Liquid Solutions Challenge Air Dominance

Liquid platforms are expanding at a 12.10% CAGR, far outpacing air-based solutions that nonetheless retained 60% share of the North America data center cooling market in 2024. Within liquids, immersion emerged as the fastest mover thanks to turnkey tanks that replace raised-floor layouts. The North America data center cooling market size for immersion is forecast to more than double by 2031 as hyperscalers standardize direct-to-coolant motherboards. Air approaches remain relevant where rack loads stay under 20 kW, and ongoing efficiency upgrades—such as electronically commutated fans and structured aisle containment—stretch their lifespan. Yet, as processors trend toward 800-W chip envelopes, liquid’s thermodynamic superiority becomes decisive, cementing a clear bifurcation between legacy and high-performance environments. Economizer configurations that tap cool outside air retain a niche, particularly across Canada’s colder provinces where free-cooling hours offset higher building envelopes.

Air-based architectures still offer speed-to-market advantages; contractors are familiar with CRAC sizing and airflow modeling. However, operators planning AI clusters factor the inevitable shift toward liquid, often designing shell space with future retrofits in mind. Vendors address this interim phase by shipping combination skids that couple chilled-water coils with rear-door heat exchangers, allowing gradual migration. Direct-to-chip platforms led by ZutaCore and LiquidStack partner with mainstream manufacturers, merging innovation with global service networks, further accelerating transition.

By Cooling Component: CRAH Units Face Immersion System Competition

CRAH/CRAC cabinets generated 41% of 2024 component revenue but now contend with immersion racks integrating pumps, heat exchangers, and filtration in a single enclosure. The North America data center cooling market share for monitoring software is rising as operators prioritize data-driven optimization. Magnetic-bearing chillers launch at capacities up to 850 tons, trimming energy use by 30% and meeting low-GWP mandates without performance penalties. Dry coolers, once regional, broaden appeal amid water-scarcity pressures, especially when paired with adiabatic pads for peak temperatures.

Control platforms increasingly employ machine-learning algorithms that predict thermal load shifts and adjust flow rates proactively, raising demand for IoT sensors embedded in pumps and valves. Component vendors that bundle hardware with analytics secure annuity service streams and improve customer retention. Heat exchanger advancements—microchannel geometries and corrosion-resistant alloys—enable tighter approach temperatures, shrinking overall plant footprints. Manufacturers publicize mean time between failures exceeding 80,000 hours to prove reliability parity with traditional gear.

By Data Center Type: Hyperscalers Drive Innovation Adoption

Hyperscale campuses hold the fastest 14.10% CAGR, funneling vast orders into the North America data center cooling market and dictating technical roadmaps. Their preference for large modular blocks simplifies mechanical integration and creates purchasing power that compresses margins but lifts volume. Concurrently, colocation maintains 48.50% share because enterprise clients favor capital-light models. These multitenant facilities differentiate by offering suites certified for both air and immersion, raising complexity for cooling designers.

Edge and enterprise segments adopt prefabricated modules shipping with factory-charged refrigerants and plug-and-play controls, shortening deployment to 12 weeks. The North America data center cooling market size for edge is modest today yet strategic for vendors seeking diversified revenue. Compass Data Centers’ hybrid plant in Columbus exemplifies edge innovation, using fluid coolers that toggle between dry and adiabatic modes to meet AI bursts without water penalties.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Healthcare Accelerates Cooling Investments

IT and telecom continues to generate 40% of 2024 demand but faces slower growth relative to healthcare’s 11.80% CAGR. Hospitals and research institutes digitize imaging archives and genomic datasets, necessitating strict humidity and temperature tolerances. The North America data center cooling market size for healthcare deployments is poised to surpass USD 1 billion by 2031, underpinned by HIPAA compliance and life-safety redundancy requirements. Retail and media users modernize existing footprints with rear-door heat exchangers to support seasonal traffic spikes while deferring costly full-scale retrofits.

Federal and institutional agencies migrate toward high-secure cloud regions, adopting identical cooling topologies to maintain accreditation. Mandatory uptime architectures translate into N+2 cooling redundancy, benefiting suppliers of independent chilled-water loops. Vertical nuance thus propels tailored offerings, from antimicrobial coolant formulations for hospitals to shielded airflow designs for broadcast studios.

Geography Analysis

The United States anchors over 80% of current spending in the North America data center cooling market, led by clusters in Virginia, Texas, and California. Grid restrictions in Loudoun County redirected new builds toward Dallas and Columbus, redistributing purchase orders and stimulating regional manufacturing such as STULZ’s plant in Denton County, Texas. Water-neutral cooling gains ground in Phoenix, where operators exploit nocturnal evaporative windows and daytime dry operation to straddle performance and conservation goals.

Canada’s share accelerates on the back of heat-reuse directives that reward facilities feeding municipal district-energy loops. Projects in Toronto’s Port Lands demonstrate 5 MW of recovered heat displacing natural-gas boilers, elevating liquid-loop adoption. Provincial incentives rebated up to 30% of capital spent on qualifying heat-exchanger equipment, improving payback and nudging U.S. vendors northward. The North America data center cooling market size attached to Canadian projects is expected to grow at 10% annually through 2031.

Mexico’s emerging hub in Querétaro benefits from federal clean-energy goals and proximity to U.S. cloud nodes. AWS and Google announce multi-availability-zone campuses outfitted with closed-loop coolant circuits minimizing potable-water draw. Alliance Air’s USD 121 million HVAC factory in Tijuana positions Mexico as a cross-border component supplier, shortening lead-times for Southwest U.S. builds. Government harmonization with U.S. HFC phase-down schedules ensures technology alignment, easing vendor certification burdens.

Competitive Landscape

Incumbents such as Vertiv, Schneider Electric, and Johnson Controls deploy acquisition and joint-venture playbooks to keep pace with liquid-cooling disruption. Vertiv posted 25% revenue and 60% order growth in 2024, fueled by hyperscale retrofits, and funneled R&D into coolant-agnostic pumps for immersion racks. Schneider bolstered its portfolio via the USD 850 million purchase of Motivair, securing cold-plate patents. Johnson Controls reorganized under its Global Data Center Solutions vertical to bundle YORK chillers with OpenBlue analytics, enhancing cross-sell velocity.

Specialists like LiquidStack, ZutaCore, and Submer capture mindshare by demonstrating 40% energy savings and sub-1.05 PUE in pilot sites. Their strategy hinges on alliances: ZutaCore paired with Munters for global service coverage, while Submer co-develops dielectric formulas with Castrol. Although individually small, these innovators influence architecture decisions at design stage, eroding incumbents’ specification dominance.

White-space entrants, typified by Katrick Technologies, pitch passive airflow units that claim 50% energy reduction without compressors, targeting edge deployments with tight capex ceilings. Patent filings around micro-channel immersion tanks and oil-free compressors surged 18% year-on-year, indicating intensifying IP competition. Overall, the North America data center cooling market balances scale efficiency with nimble innovation, fostering a partnership-rich environment.

North America Data Center Cooling Industry Leaders

-

Vertiv Group Corp.

-

Stulz GmbH

-

Schneider Electric SE

-

Rittal GmbH & Co. KG

-

Asetek A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Trane Technologies launched the Fan Coil Wall platform for customizable closed-loop thermal management of AI racks.

- March 2025: Trane introduced magnetic-bearing and Ascend air-cooled chillers using low-GWP refrigerants for high ambient zones.

- February 2025: Carrier unveiled QuantumLeap, promising double-digit efficiency gains for hyperscale campuses.

- December 2024: Castrol released a direct-to-chip coolant optimized for AI load densities.

North America Data Center Cooling Market Report Scope

The equipment, tools, methods, and procedures used to maintain an ideal operating temperature inside a data center building are collectively referred to as data center cooling. There is a growing need for energy-efficient cooling of IT equipment mainly due to the increased capacity and higher data density. In addition, advantages provided by technology and government support by imposing efficiency rules for data centers are anticipated to directly contribute to developing the data center cooling market in several applications, including IT, BFSI, telecommunication, etc.

The North American data center cooling market is segmented by cooling technology (air-based cooling (CRAH, chiller and economizer, cooling tower (covers direct, indirect & two-stage cooling), and others)), liquid-based cooling (immersion cooling, direct-to-chip cooling, rear-door heat exchanger), end-user vertical (IT & telecom, retail & consumer goods, healthcare, media & entertainment, federal & institutional agencies, and other end-user verticals), and geography (United States, Canada, and the Rest of North America). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Cooling Technology

| Air-Based Cooling | CRAH |

| Chiller and Economizer | |

| Cooling Tower (Direct, Indirect, Two-Stage) | |

| Others | |

| Liquid-Based Cooling | Immersion Cooling |

| Direct-to-Chip Cooling | |

| Rear-Door Heat Exchanger |

By Cooling Component

| Computer-Room Air Handlers (CRAH/CRAC) |

| Chillers and Heat-Exchanger Units |

| Cooling Towers and Dry Coolers |

| Pumps and Valves |

| Control and Monitoring Software |

By Data Center Type

| Hyperscale |

| Colocation |

| Enterprise/Edge |

By End-User Industry

| IT and Telecom |

| Retail and Consumer Goods |

| Healthcare |

| Media and Entertainment |

| Federal and Institutional Agencies |

| Others |

By Country

| United States |

| Canada |

| Mexico |

| By Cooling Technology | Air-Based Cooling | CRAH |

| Chiller and Economizer | ||

| Cooling Tower (Direct, Indirect, Two-Stage) | ||

| Others | ||

| Liquid-Based Cooling | Immersion Cooling | |

| Direct-to-Chip Cooling | ||

| Rear-Door Heat Exchanger | ||

| By Cooling Component | Computer-Room Air Handlers (CRAH/CRAC) | |

| Chillers and Heat-Exchanger Units | ||

| Cooling Towers and Dry Coolers | ||

| Pumps and Valves | ||

| Control and Monitoring Software | ||

| By Data Center Type | Hyperscale | |

| Colocation | ||

| Enterprise/Edge | ||

| By End-User Industry | IT and Telecom | |

| Retail and Consumer Goods | ||

| Healthcare | ||

| Media and Entertainment | ||

| Federal and Institutional Agencies | ||

| Others | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

How large is the North America data center cooling market in 2025?

It is valued at USD 7.2 billion, with an 11.80% CAGR projected through 2031.

Which cooling technology is growing fastest across North America?

Liquid-based solutions, particularly immersion and direct-to-chip platforms, are rising at a 12.10% CAGR through 2031.

Why are hyperscale operators accelerating cooling upgrades?

AI workloads push rack densities beyond 100 kW, requiring liquid systems that manage higher heat flux while improving PUE.

What impact do U.S. sustainability mandates have on cooling purchases?

Executive-order PUE targets compel federal and contractor sites to adopt high-efficiency chillers and hybrid cooling, sustaining multi-year demand.

How are Canadian regulations shaping cooling choices?

Provincial heat-reuse mandates incentivize systems that capture and export waste heat, boosting adoption of liquid loops with integrated exchangers.

Which vendors lead recent innovation in data center cooling?

Vertiv, Schneider Electric, Johnson Controls, LiquidStack, and ZutaCore stand out for acquisitions, product launches, and hyperscale partnerships.

Page last updated on: