North America Cotton Market Analysis by Mordor Intelligence

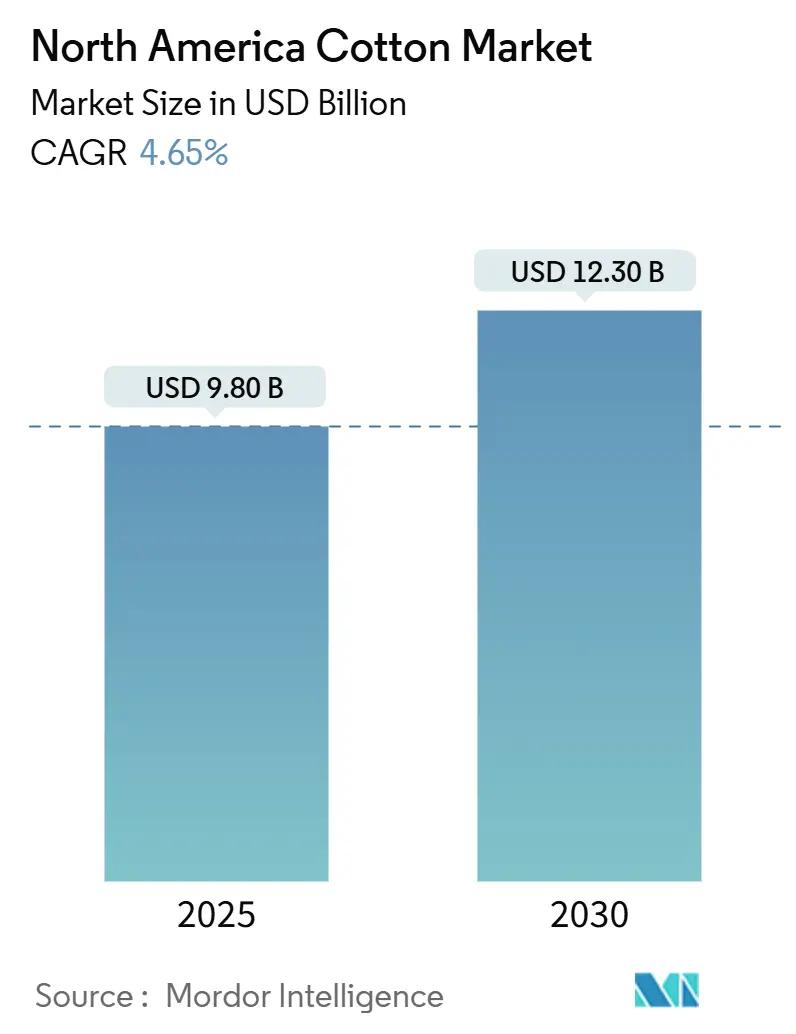

The North America cotton market size is estimated at USD 9.8 billion in 2025 and is projected to reach USD 12.3 billion by 2030, representing a 4.65% CAGR during the forecast period. The expansion is rooted in federal revenue-support programs, rising global demand for traceable natural fibers, and the steady adoption of water-saving irrigation methods[1]Source: USDA Foreign Agricultural Service, “Cotton: World Markets and Trade,” fas.usda.gov. Farm-level carbon-credit payments, which add USD 20-45 per acre of incremental income, improve grower margins even in periods of futures-price volatility. Subsurface drip irrigation now covers 180,000 acres across the Texas High Plains, cutting water use by 30% and keeping yields above 1,000 pounds per acre. At the same time, bollworm resistance to Bacillus thuringiensis (Bt) traits raises pest-control costs by USD 40–60 per acre in hot-spot states, eating into producer profits. Marketing loans and crop insurance subsidies offset these headwinds, sustaining planted area at close to 11.5 million acres despite competing crop alternatives.

Key Report Takeaways

By geography, the United States captured 88.4% of North America cotton market share in 2024, while Mexico is advancing at a 6.2% CAGR through 2030.

North America Cotton Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stable United States Department of Agriculture (USDA) support programs | +0.8% | United States dominant and modest spillover to Mexico | Medium term (2-4 years) |

| Rising global demand for sustainable natural fibers | +0.9% | North America as principal supplier to European Union and Asian mills | Long term (≥ 4 years) |

| Expansion of regenerative-agriculture acreage | +0.7% | United States core and early adoption in Mexico | Medium term (2-4 years) |

| Growth in textile-recycling initiatives driving virgin-cotton blending | +0.5% | North America benefits as major exporter | Long term (≥ 4 years) |

| Increasing water-efficient drip-irrigation adoption | +0.6% | United States (Texas High Plains, Arizona) while limited in Mexico | Short term (≤ 2 years) |

| Surge in farm-level carbon-credit monetization opportunities | +0.5% | United States leading and Mexico nascent | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stable United States Department of Agriculture (USDA) Support Programs

Price loss coverage, agriculture risk coverage, and subsidized crop insurance provide predictable revenue floors, insulating growers from volatile ICE futures swings. Reference prices fixed at 76.3 cents per pound guarantee breakeven returns on roughly 70% of national acreage. Emergency Conservation Assistance of USD 84.7 per acre encourages the adoption of cover crops and precision input management. This financial safety net underpins annual plantings between 11 million and 12 million acres, preventing a mass switch to soybeans or sorghum when cotton prices dip.

Rising Global Demand for Sustainable Natural Fibers

Apparel brands such as Hennes and Mauritz (H&M) and Inditex have committed to eliminating virgin polyester by 2030, redirecting procurement toward certified cotton. United States Cotton Trust Protocol enrollment rose from 18% to 25% of national acreage in one year, enabling mills in Bangladesh and Vietnam to meet European Union due diligence mandates. Certified lint trades at a 5-8% premium, rewarding growers who implement full traceability systems and disadvantaging conventional sellers.

Expansion of Regenerative-Agriculture Acreage

The Kellanova and Archer-Daniels-Midland (ADM) partnership pays USD 15–25 per acre for 120 thousand acres of cotton to integrate cover crops and implement reduced tillage. Cargill, Incorporated's RegenConnect expanded to 500 thousand acres, with cotton accounting for 20%. Protocol Level 2 verification unlocks up to USD 45 per acre, making regenerative practices financially viable in water-stressed West Texas. Stronger soil structure and higher organic matter also improve lint quality, resulting in downstream benefits for spinners.

Growth in Textile-Recycling Initiatives Driving Virgin-Cotton Blending

Mechanical recycling shortens fiber length by as much as 30%, forcing mills to blend recycled feedstock with new lint to preserve yarn strength[2]Source: Government Accountability Office, “Textile Recycling: Challenges and Opportunities,” gao.gov. Brands targeting 50% recycled content by 2030 must therefore source virgin cotton to maintain fabric durability, creating a structural demand floor even as post-consumer waste volumes rise. Chemical recycling technologies, such as Circ's hydrothermal process, can preserve fiber length; although pilot-scale costs remain 40% above those of virgin cotton, limiting commercial deployment. This dynamic suggests that North American producers will continue to supply blending-grade cotton to mills in Turkey and Pakistan that specialize in recycled-virgin hybrid yarns.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile commodity pricing tied to futures speculation | −0.9% | Global, North America as price-taker in ICE futures | Short term (≤ 2 years) |

| Escalating pest-resistance to Bt traits | −0.7% | United States Southeast and Mid-South, emerging in Mexico | Medium term (2-4 years) |

| Stricter labor-traceability requirements from brands | −0.4% | Global, compliance costs concentrated in United States export channels | Medium term (2-4 years) |

| Growing hemp fiber substitution in technical textiles | −0.3% | North America and European Union, niche displacement | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Commodity Pricing Tied to Futures Speculation

Futures market dynamics amplify price swings beyond fundamental supply-and-demand signals, destabilizing planting decisions. New York ICE cotton futures traded in a 16-cent range during the 2024 marketing year, with speculative positioning by commodity trading advisors accounting for 40% of open interest according to Commodity Futures Trading Commission data. A March 2024 International Cotton Advisory Committee report attributed a 12-cent price surge to algorithmic trading strategies that misinterpreted Chinese reserve-release announcements, triggering a short-covering rally disconnected from physical mill demand. This volatility compresses forward-contracting windows, forcing producers to accept basis risk or forgo price discovery entirely.

Escalating Pest-Resistance to Bt Traits

Bollworm populations have developed resistance to pyramided Bt traits across the Cotton Belt, eroding the economic advantage of genetically engineered varieties. Texas A&M AgriLife Extension documented bollworm survival rates above 20% on WideStrike 3 and Bollgard 3 cotton in 2024, necessitating supplemental insecticide applications that add USD 40 to USD 60 per acre in input costs. The Environmental Protection Agency's Insect Resistance Management requirements mandate refuge acreage, but compliance audits in Georgia and Alabama found that 30% of growers failed to plant the required 5% non-Bt refuge, thereby accelerating the evolution of resistance[3]Source: Environmental Protection Agency, “Insect Resistance Management for Bt Cotton,” epa.gov. Seed companies are developing next-generation traits that stack Bt proteins with RNA interference mechanisms, yet commercial release is not anticipated until 2027, leaving a multi-year window where growers must rely on conventional chemistries.

Geography Analysis

The United States contributed 88.4% to the North America cotton market size in 2024, equal to 14.4 million bales, while Mexico grew at a 6.2% CAGR and Canada remained a net importer. New irrigation systems in Chihuahua and Baja California have expanded the planted area in Mexico to 102,000 hectares.

The lack of access to genetically engineered seeds restricts average yields to 890 kilograms per hectare, far below the 1,200 kilograms achieved in Texas and Georgia. United States growers leverage loan-rate guarantees and 62% crop-insurance subsidies to manage revenue risk, allowing the segment to maintain 11–12 million acres despite volatile prices. Mexico relies on lower land costs and proximity to Carolinas mills, which reduces freight charges by 20–30% compared to Panhandle origins[4]USDA Foreign Agricultural Service, “Mexico Cotton Annual,” fas.usda.gov.

Regenerative incentives further widen the competitiveness gap. Twenty-five percent of United States acreage, or roughly 3 million acres, already qualifies for the Protocol Level 2 premium, whereas Mexican lint lacks recognized traceability pathways. This premium tier commands a 5%–8% price differential and positions United States cotton as a default supply for brands operating under the European Union due-diligence regime. Canada, importing 50,000 metric tons annually, specifies Better Cotton lint for its technical-textile cluster in Quebec, a demand pull that disproportionately benefits United States suppliers.

Recent Industry Developments

- March 2025: Cargill, Incorporated expanded its RegenConnect platform across multiple crops in North America, with cotton representing approximately 20% of enrolled acreage. The program offers farmers USD 15 to USD 25 per acre for adopting cover crops, reduced tillage, and diverse rotations, creating a scalable pathway for growers to access carbon-credit markets while improving soil health.

- February 2025: The United States Cotton Trust Protocol launched a Level 2 verification tier, enabling growers who achieve a 10% reduction in greenhouse-gas intensity relative to the 2019 baseline to earn up to USD 45 per acre annually. The initiative enrolled 25% of domestic acreage by 2024 and aims to reach 40% by 2027.

- January 2025: Olam Agri Holdings announced a partnership with the Soil Health Institute to scale regenerative cotton production across 200 thousand acres in Texas and Oklahoma, United States. The collaboration will deploy AtSource traceability technology to provide mill customers with farm-level data on carbon sequestration and water use.

North America Cotton Market Report Scope

The North America Cotton Market Report is Segmented by Geography (United States, Canada, and Mexico). The Study Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Export Analysis (Value and Volume), Import Analysis (Value and Volume), and Price Trend Analysis. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

By Geography (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis)

| United States |

| Canada |

| Mexico |

| By Geography (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis) | United States |

| Canada | |

| Mexico |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the North America cotton market?

The North America cotton market is valued at USD 9.8 billion in 2025 and is projected to reach USD 12.3 billion by 2030.

How fast is the market growing?

The market is expanding at a 4.65% CAGR over 2025-2030.

Which country leads regional production?

The United States controls 88.4% of North American cotton output.

What sustainability programs offer the highest farm premiums?

United States Cotton Trust Protocol Level 2 verification can pay up to USD 45 per acre for meeting rigorous greenhouse-gas benchmarks.

How does drip irrigation impact water use?

Subsurface drip systems lower water application by 30% while maintaining yields above 1,000 pounds per acre in the Texas High Plains.

Page last updated on: