Market Trends of North America Construction Industry

Residential Construction Segment Holds the Major Share in the Market

- Residential construction, already reeling from rising mortgage rates, is expected to continue to contract and be joined by nonresidential construction as the commercial sector retrenches. The funds provided to the construction industry through the Infrastructure Investment and Jobs Act (IIJA), the CHIPS and Science Act, and the Inflation Reduction Act (IRA) will counter the downturn, allowing the construction industry to tread water.

- The US housing market has borne the brunt of the interest rate hikes amid efforts by the Federal Reserve (Fed) to tame inflation. The Fed announced its ninth straight interest rate hike of 25 basis points in March 2023. This move increased the federal funds rate from nearly 0% in March 2022 to a range of 4.75-5%. The Fed will likely hike rates further by 25 basis points in early May 2023, as the job market remains tight and inflation is still at higher levels despite easing in recent months.

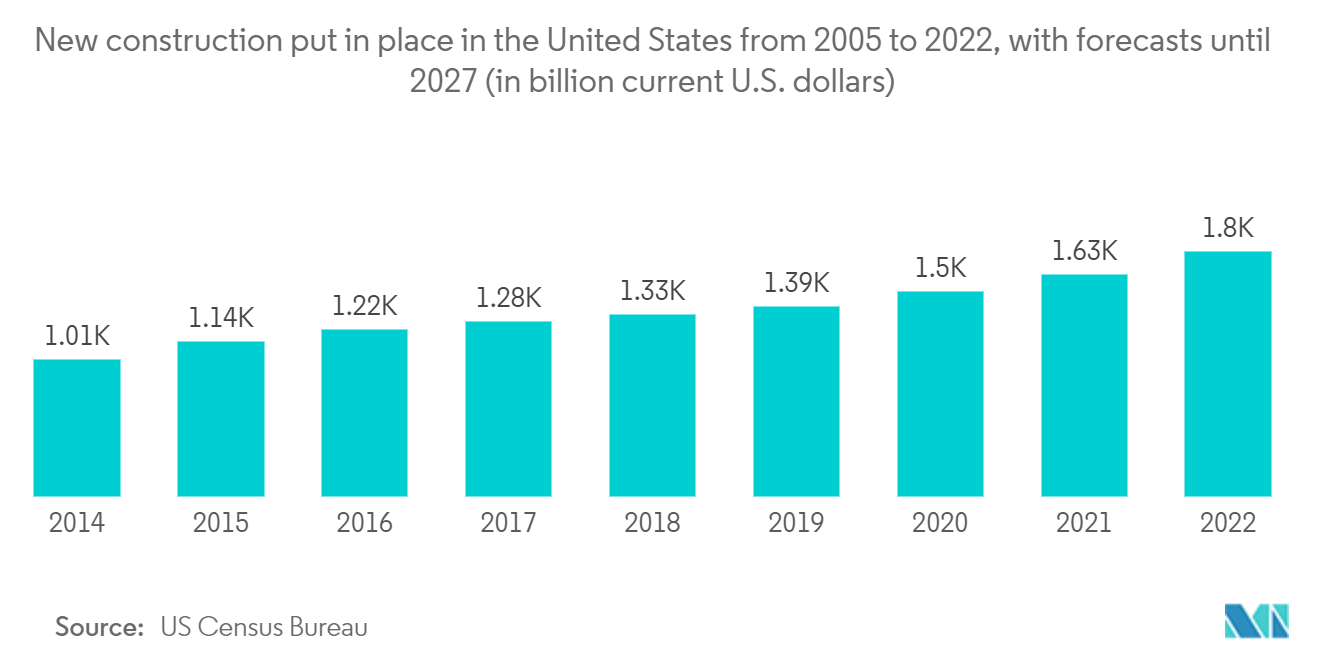

- In July 2023, the US saw a substantial increase in construction spending due to a lack of housing available on the market, which led to higher expenditures for single-family residential projects. According to the Commerce Department, construction expenditure rose by 0.7%. To show that construction spending increased by 0.6% rather than 0.5%, as reported earlier, data for June 2023 have been revised up a little.

- In July 2023, construction expenditure increased by 5.5% year over year. Private construction spending increased by 1.0% after rising 1.5% in the previous month, while investment in residential buildings increased by 1.4%. In June, private building expenditure increased by 0.6%. In July, the spending on single-family housing projects jumped by 2.8%. A shortage of houses drives construction for sale, although higher mortgage interest rates could slow it down.

- As the market is currently expecting a cut in rates, housing construction will start to recover somewhat in Canada in 2024. However, for the next five years, residential construction is expected to decrease at an annualized rate of 1.1% and reach a value of USD 156.7 billion due to continued high overnight rates.

Understand The Key Trends Shaping This Market

Download PDF

United States Expected to Witness Growth

- US construction output was forecast to contract by 5% in 2023 due to a slump in residential construction. Rising interest rates lead to higher project financing costs, while inflation has increased construction material costs. Lack of skilled workers and supply chain disruptions have led to longer lead times and project delays. In addition, an aging workforce could curtail potential construction output in the future.

- The residential building segment is expected to see the most significant contraction because aggressive monetary tightening is feeding into higher mortgage rates, and high inflation weighs on the affordability of homeownership. However, non-residential construction remains more resilient due to government stimulus. The Infrastructure Investment and Jobs Act is expected to stimulate construction, aiming at comprehensive investments in aging infrastructure (including roads, highways, bridges, rail, and broadband development).

- Construction activities in the US residential sector started on a weaker note in 2023, with the total value of construction put in place (measured in seasonally adjusted nominal terms) falling by 4.1% year-on-year (Y-o-Y) in the first two months of 2023. Due to the economic slowdown, subdued demand in residential construction, and rising pressure on margins, payment delays, and insolvencies were expected to increase. With high interest rates and a slowdown in activity, businesses with limited liquidity and elevated debt levels will face difficulties servicing their obligations.

- Given the more subdued credit management situation and business performance of the construction industry, the market outlook has been downgraded from “Good” to “Fair.” Privately‐owned housing units authorized by building permits in April 2023 were at a seasonally adjusted annual rate of 1,416,000. This is 1.5% below the revised March rate of 1,437,000 and 21.1% below the April 2022 rate of 1,795,000.

- Single‐family authorizations in April were at a rate of 855,000, 3.1% above the revised March figure of 829,000. Authorizations of units in buildings with five units or more were at a rate of 502,000 in April 2023. Privately owned housing started in April at a seasonally adjusted annual rate of 1,401,000. This is 2.2% (±11.9%) above the revised March estimate of 1,371,000 but is 22.3% (±8.7%) below the April 2022 rate of 1,803,000.

- Single‐family housing starts in April 2023 were at a rate of 846,000, 1.6% (±12.3%) above the revised March 2023 figure of 833,000. The April rate for units in buildings with five units or more was 542,000. Privately‐owned housing completions in April were at a seasonally adjusted annual rate of 1,375,000. This is 10.4% below the revised March 2023 estimate of 1,534,000 but is 1% above the April 2022 rate of 1,361,000. Single‐family housing completions in April were at a rate of 971,000, 6.5% below the revised March rate of 1,039,000. The April rate for units in buildings with five units or more was 400,000.

Get Analysis on Important Geographic Markets

Download PDF