| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 2.58 Trillion |

| Market Size (2030) | USD 3.26 Trillion |

| CAGR (2025 - 2030) | 4.82 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

North America Construction Market Analysis

The North America Construction Market size is estimated at USD 2.58 trillion in 2025, and is expected to reach USD 3.26 trillion by 2030, at a CAGR of 4.82% during the forecast period (2025-2030).

The North American construction sector demonstrates remarkable resilience amid challenging economic conditions, characterized by high interest rates and limited credit availability following U.S. banking sector turbulence. The construction industry has adapted to these challenges through innovative financing approaches and strategic project planning. Despite these headwinds, builder confidence remains robust, with a significant 80% of construction firms planning to increase their housing starts in 2024, while 51% anticipate growth rates exceeding 10% compared to 2023 levels. This optimism is particularly noteworthy given the complex interplay of supply chain dynamics and labor market conditions shaping the industry landscape.

Infrastructure development and public sector initiatives are emerging as crucial growth catalysts across the region. A prime example is New York City's "Future Housing Initiative" launched in March 2023, which allocated USD 15 million for constructing 3,000 energy-efficient and all-electric affordable homes. This initiative exemplifies the growing integration of sustainable construction goals with infrastructure development, as it aligns with broader objectives to reduce greenhouse gas emissions by 85% by 2050. The focus on public infrastructure construction spending has become particularly pronounced in Mexico, where increased investment is driving sector growth in anticipation of presidential elections.

The residential construction landscape is experiencing a significant transformation, driven by the persistent housing shortage and evolving consumer preferences. The National Association of Home Builders projects housing starts to reach 1.3 million units by 2025, reflecting the industry's response to sustained demand. The scarcity of existing homes has created a unique market dynamic where new construction becomes increasingly vital to addressing housing needs. This trend is particularly evident in urban centers where land availability constraints are pushing developers to innovate with higher-density solutions and mixed-use developments.

Non-residential construction presents a mixed picture across different subsectors, with industrial and institutional projects showing strong momentum while commercial construction segments face challenges. In Canada, the commercial sector, which represents approximately half of non-residential construction, has experienced a decline of 3.5% year-over-year. This divergence highlights the shifting priorities in the construction landscape, where manufacturing reshoring initiatives and institutional development are gaining prominence over traditional commercial projects. The trend reflects broader economic transitions and changing workplace dynamics influencing construction demand patterns.

North America Construction Market Trends

Government Infrastructure Initiatives and Investment Support

The construction market in North America is significantly driven by substantial government infrastructure initiatives and investment support programs. The Infrastructure Investment and Jobs Act (IIJA), CHIPS and Science Act, and Inflation Reduction Act (IRA) have emerged as crucial catalysts for the industry's growth, providing essential funding for various infrastructure projects across the region. These initiatives are particularly focused on comprehensive investments in aging infrastructure, including roads, highways, bridges, rail networks, and broadband development, creating a strong foundation for sustained construction activity. The federal government's commitment to modernizing infrastructure has led to increased project opportunities, with significant allocations for sustainable and resilient construction projects.

The Canadian government's initiatives, such as the Smart Renewables and Electrification Pathways Program (SREPs), are driving the construction of low-emissions energy infrastructure and modernizing electricity system operations. In July 2023, the implementation of these programs has resulted in a 0.7% increase in construction spending, particularly in single-family residential projects. The government's "Housing Now" plan, introduced to build over 40,000 new residential units within a 12-year timeframe, further demonstrates the strong public sector support driving construction activity. These initiatives are complemented by provincial and municipal level programs, creating a multi-tiered support system for construction projects across various sectors.

Understand The Key Trends Shaping This Market

Download PDF

Rising Construction Spending and Housing Demand

The construction market is experiencing significant momentum driven by increased construction spending and persistent housing demand across North America. In July 2023, private construction spending demonstrated robust growth, increasing by 1.0% following a 1.5% rise in the previous month, while investment in residential buildings saw a 1.4% increase. The spending on single-family housing projects has shown particular strength, with a notable 2.8% jump in July 2023, primarily driven by the acute shortage of available housing inventory in the market. This sustained demand for housing, despite higher mortgage interest rates, continues to fuel construction activity across various residential segments.

The commercial and industrial sectors are also experiencing increased construction spending, driven by the strong demand for warehouse space and logistics facilities. The market is witnessing a significant transformation in construction requirements, with an estimated need for an additional 330 million square feet of warehouse space dedicated to online fulfillment by 2025 in the United States alone. This surge in demand is complemented by increased investment in sustainable construction practices, with numerous LEED-registered projects across various sectors, including office spaces, retail establishments, and multi-family residential developments. The construction industry's response to these demands is evident in the increasing number of large-scale development projects and the adoption of innovative construction technology methodologies.

Technological Advancements and Sustainable Building Practices

The construction market is experiencing a significant transformation driven by technological advancements and the increasing adoption of sustainable construction practices. The integration of Building Information Modeling (BIM), digital asset management, and artificial intelligence has revolutionized construction management methodologies, improving efficiency and project outcomes. The industry has witnessed widespread adoption of advanced technologies such as 3D/4D/5D/6D modeling, augmented reality, virtual reality, and UAV deployment for quality assurance and control, leading to more precise and efficient construction processes. These technological innovations are particularly evident in large-scale projects where digital transformation has become a crucial factor in project success.

The push towards green construction practices is evidenced by the significant number of LEED-registered projects across North America. As of March 2020, there were 1,906 LEED-registered office projects, 865 retail projects, and 635 multi-family residential projects in Canada alone, demonstrating the strong momentum in green building initiatives. The industry's focus on sustainability is further reinforced by government regulations and initiatives promoting energy-efficient buildings and environmentally friendly construction practices. This trend is supported by the increasing demand for buildings with improved energy efficiency, better indoor environmental quality, and reduced environmental impact, driving innovations in building materials and methodologies.

Urbanization and Population Growth

Urbanization and population growth continue to be fundamental drivers of the North American construction market, creating sustained demand for both residential and commercial construction projects. The increasing urban population has led to a significant rise in demand for various types of construction, particularly in metropolitan areas where housing shortages have become acute. This urbanization trend is evidenced by the substantial number of new rental units being delivered nationwide, with more than 330,000 new rental units expected to be completed, comparable to the previous four years of construction boom. The demand spans across various building types, from high-rise residential complexes to mixed-use developments, reflecting the changing preferences of urban populations.

The impact of urbanization is particularly visible in the development of comprehensive urban infrastructure projects and mixed-use developments. Major cities are witnessing significant construction activity in response to growing population needs, with projects incorporating both residential and commercial elements. For instance, Oxford Properties Group's plans to add apartment buildings to existing properties around Toronto, creating mixed-use neighborhoods that combine residential and retail spaces, exemplify this trend. The development of these integrated urban spaces is further supported by investments in supporting infrastructure, including transportation networks, utilities, and community facilities, creating a comprehensive response to urbanization-driven construction demands.

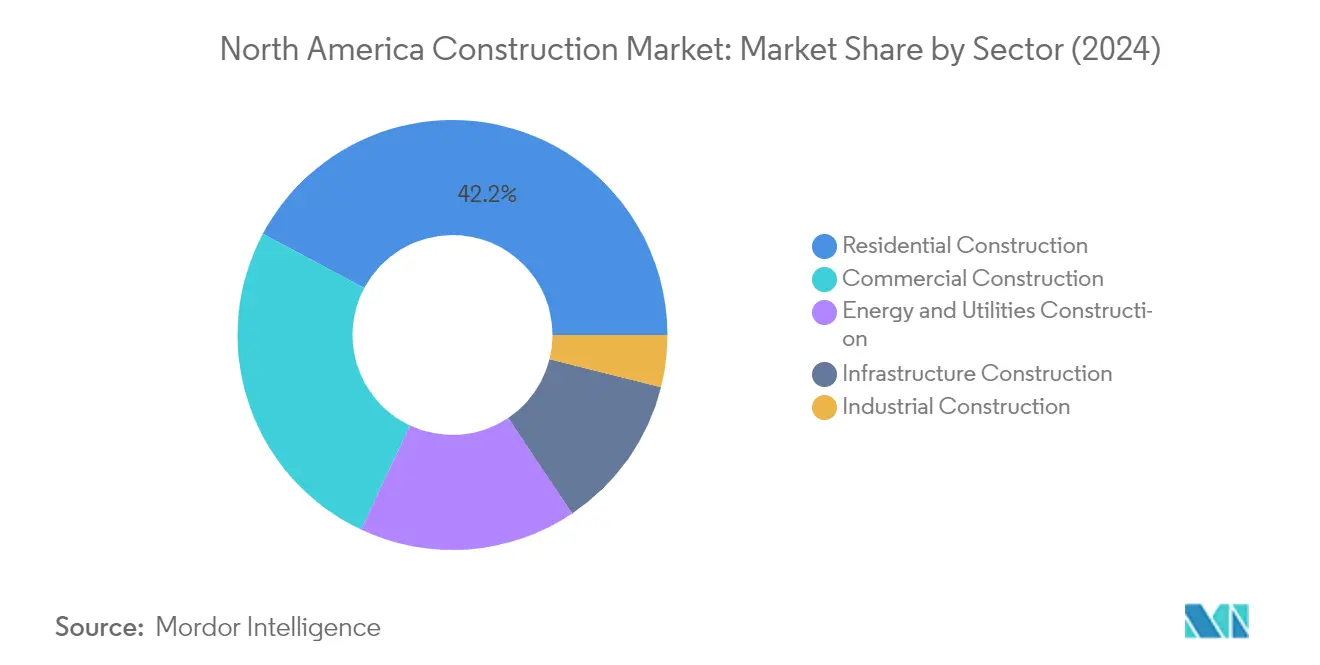

Segment Analysis: By Sector

Residential Construction Segment in North America Construction Market

The residential construction segment continues to dominate the North American construction market, holding approximately 42% market share in 2024. This significant market position is supported by strong demand for housing across major metropolitan areas and growing suburban developments. The segment's strength is particularly evident in regions like Texas, Florida, Georgia, Arizona, Washington, and Nevada, where residential developments are being driven by population growth and migration patterns. The sector's resilience is further reinforced by ongoing trends in single-family home construction and multi-family housing projects, with particular emphasis on energy-efficient and sustainable building practices.

Infrastructure Construction Segment in North America Construction Market

The infrastructure construction segment is emerging as the fastest-growing sector in the North American construction market, with an expected growth rate of approximately 6% during 2024-2029. This robust growth is being driven by significant government initiatives and investments in transportation infrastructure, including major highway projects, railway expansions, and airport modernization programs. The segment's expansion is particularly notable in Canada, where the government's commitment to infrastructure development through programs like the Investing in Canada Infrastructure Program is creating substantial opportunities. The focus on sustainable and resilient infrastructure construction development, coupled with the increasing adoption of advanced construction technologies, is expected to maintain this segment's strong growth trajectory.

Remaining Segments in North America Construction Market

The commercial construction, industrial, and energy & utilities construction segments each play vital roles in shaping the North American construction market landscape. The commercial construction sector continues to evolve with changing market demands, particularly in warehouse and logistics facility development driven by e-commerce growth. The industrial construction segment, though smaller in market share, is experiencing significant activity in manufacturing facility construction and technological upgrades. The energy and utilities construction segment maintains its importance through ongoing investments in renewable energy infrastructure and grid modernization projects, reflecting the region's commitment to sustainable development and energy security.

Segment Analysis: By Construction Type

New Constructions Segment in North America Construction Market

New constructions represent the dominant segment in the North American construction market, accounting for approximately 50% of the total market value in 2024. This segment's prominence is driven by extensive residential construction and commercial construction development projects across major metropolitan areas in the United States and Canada. The segment's strength is particularly evident in regions experiencing rapid urbanization and population growth, where new housing developments and commercial spaces are in high demand. The robust performance of this segment is supported by government infrastructure initiatives, private sector investments, and the continued expansion of urban centers across North America.

Demolition and New Construction Segment in North America Construction Market

The Demolition and New Construction segment is emerging as the fastest-growing sector in the North American construction market, with a projected growth rate of approximately 8% during 2024-2029. This accelerated growth is primarily driven by urban renewal projects, the increasing need to replace aging infrastructure, and the growing emphasis on sustainable building practices. The segment is benefiting from the rising demand for modern, energy-efficient buildings that necessitate the demolition of older structures. Additionally, the segment's growth is supported by technological advancements in demolition techniques and the increasing adoption of sustainable demolition practices that promote material recycling and waste reduction.

Remaining Segments in Construction Type Market

The Additions segment plays a vital role in the North American construction market, focusing on expanding and enhancing existing structures. This segment encompasses various activities including home renovation, commercial building expansions, and infrastructure upgrades. The segment's significance is particularly evident in established urban areas where new construction space is limited, making additions and modifications to existing structures a crucial alternative. The segment continues to be driven by the need to modernize aging buildings, adapt spaces for new uses, and implement energy-efficient improvements across residential and commercial properties.

Segment Analysis: By Structural Panel Market

United States Segment in North America Structural Panel Market

The United States dominates the North American structural panel market, accounting for approximately 89% of the total market value in 2024. This significant market share is driven by favorable regulations and rising adoption of various green building standards across the country. The strong growth in e-commerce has particularly boosted the industrial real estate sector, as developers and tenants continue to construct millions of square feet of warehouses and logistics centers requiring structural panels. The segment's prominence is further reinforced by increasing government initiatives to promote thermal insulation through federal funding in households and the US Department of Energy's support for developing highly insulating phenolic insulation foams. The residential segment has emerged as a particularly strong driver, with increasing investment in energy-efficient and advanced buildings boosting the utilization of structural insulated panels in residential construction.

Canada Segment in North America Structural Panel Market

The Canadian segment is experiencing the fastest growth in the North American structural panel market, with a projected growth rate of approximately 8% during 2024-2029. This robust growth is primarily attributed to Canada's position as a high-tech industrial country with thriving residential and commercial construction sectors. The segment's expansion is further supported by the government's initiatives like the "Housing Now" plan, which aims to significantly boost residential construction. The implementation of stringent building energy codes and the increasing focus on nearly zero-energy buildings (nZEBs) are creating substantial opportunities for structural panel manufacturers. The demand is particularly strong in multi-family buildings, where innovative building solutions are being rapidly adopted to speed up construction while maintaining energy efficiency standards.

North America Construction Market Geography Segment Analysis

Construction Market in United States

The United States continues to dominate the North American construction landscape, commanding approximately 85% of the total market share in 2024. The country's construction sector demonstrates remarkable resilience through its diverse project portfolio spanning residential, commercial construction, and infrastructure developments. The market is particularly strong in states like Texas, Florida, Georgia, Arizona, Washington, and Nevada, which are experiencing significant residential development growth. The construction industry's robustness is further enhanced by the ongoing expansion of e-commerce infrastructure, driving substantial warehouse and logistics facility development. The market's strength is also reflected in the continuous evolution of sustainable building practices, with increasing adoption of LEED certification and other green building standards. Urban development remains particularly active in major metropolitan areas, with significant investments in mixed-use developments and smart city infrastructure.

Construction Market in Canada

Canada's construction market demonstrates exceptional dynamism, with a projected growth rate of approximately 6% during the forecast period 2024-2029. The country's construction sector is experiencing a transformative phase driven by significant infrastructure modernization initiatives and sustainable development projects. The market's expansion is particularly notable in urban centers like Toronto, Vancouver, and Montreal, where major residential and commercial construction projects are reshaping the skyline. The industry's growth is further supported by the government's commitment to green building practices and energy-efficient construction methods. Innovation in construction technology, particularly in prefabricated construction and modular construction solutions, is revolutionizing project delivery methods. The market also benefits from strong public-private partnerships, facilitating the development of large-scale infrastructure projects and community developments. The focus on sustainable urban development and smart city initiatives continues to create new opportunities for construction firms and related service providers.

Construction Market in Other Regions

The broader North American construction market encompasses various regional submarkets, each with distinct characteristics and development patterns. While the United States and Canada dominate the market, different regions within these countries show varying levels of construction activity and specialization. The northern regions focus more on cold-weather-resistant construction and energy-efficient building designs, while southern regions emphasize hurricane-resistant structures and cooling efficiency. Coastal areas prioritize resilient infrastructure development to address climate change challenges, while inland regions focus on expanding transportation and logistics infrastructure. The construction industry across these regions continues to evolve with changing demographic patterns, environmental considerations, and technological advancements. Regional variations in building codes, labor availability, and material costs significantly influence construction practices and project feasibility across different locations.

Get Analysis on Important Geographic Markets

Download PDF

North America Construction Industry Overview

Top Companies in North America Construction Market

The North American construction industry features prominent players like Lennar Corporation, DR Horton, PulteGroup, Toll Brothers, Bechtel, Fluor Corp, and Parsons, among others. Companies are increasingly focusing on digital transformation through the adoption of Building Information Modeling (BIM), drones, and artificial intelligence to enhance operational efficiency. Strategic partnerships with technology providers are becoming commonplace as firms aim to become more digitally advanced. Market leaders are expanding their portfolios through diversification into new construction services segments while also focusing on sustainable building practices. Companies are investing in innovative construction technology methods like modular construction and prefabrication to reduce project timelines and costs. Additionally, there is an increasing emphasis on developing smart home technologies and building automation solutions to meet evolving customer demands.

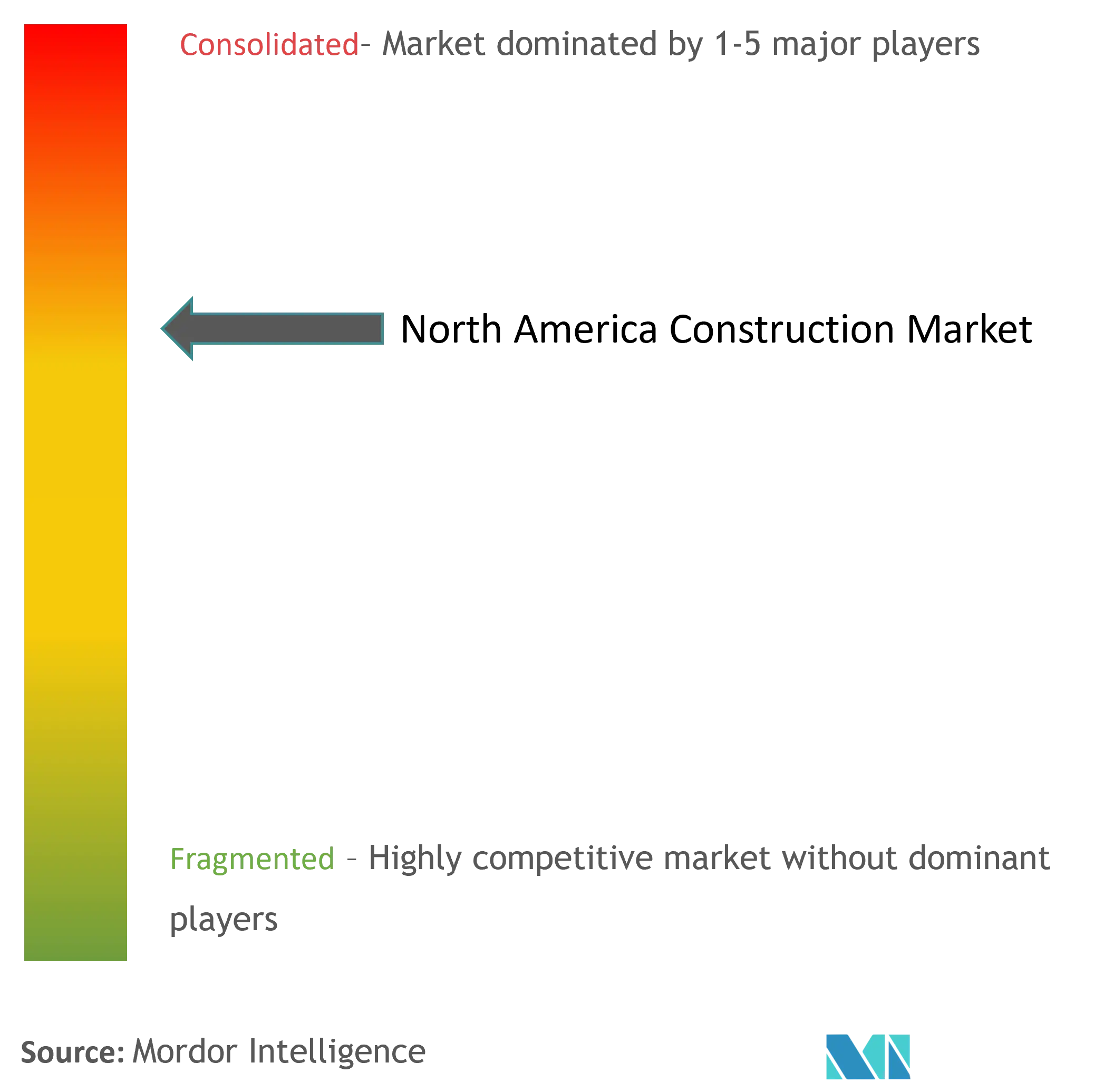

Fragmented Market with Strong Regional Players

The North American construction market exhibits a fragmented structure with the presence of both major international players and numerous small and medium-sized regional contractors. While large corporations dominate complex infrastructure and commercial projects, regional players maintain strong positions in residential and smaller commercial construction segments. The market has witnessed significant consolidation through mergers and acquisitions, particularly in the residential construction sector, as companies seek to expand their geographical presence and service offerings.

The competitive dynamics are characterized by a mix of specialized construction firms and diversified conglomerates that operate across multiple segments. Market leaders are strengthening their positions through vertical integration, acquiring companies across the construction value chain from materials suppliers to technology providers. The industry has seen increased participation from international construction giants, particularly in large-scale infrastructure projects, though local players maintain competitive advantages through established relationships and market knowledge.

Innovation and Sustainability Drive Future Growth

Success in the North American construction market increasingly depends on companies' ability to embrace technological innovation and sustainable practices. Market incumbents are focusing on developing proprietary construction technologies, establishing robust supply chain networks, and building strong relationships with key stakeholders. The ability to manage complex projects while maintaining cost efficiency and meeting stringent environmental standards has become crucial for maintaining market position. Companies are also investing in workforce development and specialized expertise to address the industry's skilled labor shortage.

For new entrants and growing players, differentiation through specialized services and technological capabilities offers a path to market share growth. The industry's high barriers to entry, particularly in terms of capital requirements and regulatory compliance, necessitate strategic partnerships and joint ventures. Companies must also consider the increasing influence of environmental regulations and sustainable building standards, which are reshaping project requirements and client expectations. Success factors include the ability to adapt to changing market demands, maintain strong financial positions, and develop innovative solutions for increasingly complex construction challenges. The role of construction consulting in navigating these complexities cannot be overstated, as firms seek to optimize their building systems and construction management processes.

North America Construction Market Leaders

-

Lennar Corporation

-

D. R. Horton Inc.

-

Kiewit Corporation

-

Hochteif USA Inc.

-

Hensel Phelps Construction Co.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

North America Construction Market News

- June 2023: AXA XL's North American construction insurance business launched the Sustainability Circle. It is a network comprising 21 leaders in the sustainable construction industry. The goal of the initiative is to assist clients achieve their sustainability goals and enhance their construction risk management efforts.

- April 2023: Greystar Real Estate Partners LLC (“Greystar”) opened its flagship manufacturing facility for its modular construction business, Modern Living Solutions (“MLS”), which focuses on attainable and sustainable housing. The milestone was met with a ribbon-cutting ceremony at the western Pennsylvania site where MLS employed 170 full-time employees to execute the ramp-up and operations of its first modular factory.

North America Construction Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Current Economic and Construction Market Scenario

- 4.2 Technological Innovations in the Construction Sector

- 4.3 Impact of Government Regulations and Initiatives on the Industry

- 4.4 Review and Commentary on the Impact of Heavy Equipment Prices on the Construction Industry

- 4.5 Comparison of the Key Industry Metrics of North American Countries (Analyst View)

- 4.6 Comparison of Construction Cost Metrics of North American Countries (Analyst View)

- 4.7 Impact of COVID-19 on the Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Population Growth and Disposable Income

- 5.1.2 Demand from Office Sector Returning Post COVID-19

- 5.1.3 Non-residential Construction on Upward Trend

-

5.2 Market Restraints

- 5.2.1 Interests and Financing

- 5.2.2 Increase in Cost of Raw Materials

-

5.3 Market Opportunities

- 5.3.1 Green Building Initiatives

- 5.3.2 Technology Advancements

-

5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6. MARKET SEGMENTATION

-

6.1 By Country

- 6.1.1 Canada

- 6.1.2 United States

-

6.2 By Sector

- 6.2.1 Commercial Construction

- 6.2.2 Residential Construction

- 6.2.3 Industrial Construction

- 6.2.4 Infrastructure (Transportation) Construction

- 6.2.5 Energy and Utilities Construction

-

6.3 By Construction Type

- 6.3.1 Additions

- 6.3.2 Demolition and New Constructions

7. COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

-

7.2 Company Profiles

- 7.2.1 Lennar Corporation

- 7.2.2 D. R. Horton Inc.

- 7.2.3 Kiewit Corporation

- 7.2.4 Hochteif USA Inc.

- 7.2.5 Hensel Phelps Construction Co.

- 7.2.6 Tutor Perini Corporation

- 7.2.7 PulteGroup Inc.

- 7.2.8 The Whiting-Turner Contracting Company

- 7.2.9 Toll Brothers Inc.

- 7.2.10 NVR Inc.

- 7.2.11 Graham Income Trust

- 7.2.12 PCL Construction Group Inc.

- 7.2.13 SNC-Lavalin Construction Inc.

- 7.2.14 Aecon Group Inc.

- 7.2.15 Kajima U.S.A. Inc.*

- *List Not Exhaustive

8. FUTURE OF THE MARKET

9. APPENDIX

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

North America Construction Industry Segmentation

Construction is the installation, maintenance, and repair of buildings and other stationary structures. It includes the construction of roadways and service facilities that form fundamental components of structures and are required for their operation. Construction encompasses the processes involved in constructing buildings, infrastructure, industrial facilities, and related operations from start to finish.

The North American construction market is segmented by country (Canada and the United States), sector (commercial construction, residential construction, industrial construction, infrastructure (transportation) construction, and energy and utilities construction), and construction type (additions and demolition and new construction). The report offers market size and forecasts in value (USD) for all the above segments.

| By Country | Canada |

| United States | |

| By Sector | Commercial Construction |

| Residential Construction | |

| Industrial Construction | |

| Infrastructure (Transportation) Construction | |

| Energy and Utilities Construction | |

| By Construction Type | Additions |

| Demolition and New Constructions |

Need A Different Region or Segment?

Customize Now

North America Construction Market Research FAQs

How big is the North America Construction Market?

The North America Construction Market size is expected to reach USD 2.58 trillion in 2025 and grow at a CAGR of 4.82% to reach USD 3.26 trillion by 2030.

What is the current North America Construction Market size?

In 2025, the North America Construction Market size is expected to reach USD 2.58 trillion.

Who are the key players in North America Construction Market?

Lennar Corporation, D. R. Horton Inc., Kiewit Corporation, Hochteif USA Inc. and Hensel Phelps Construction Co. are the major companies operating in the North America Construction Market.

What years does this North America Construction Market cover, and what was the market size in 2024?

In 2024, the North America Construction Market size was estimated at USD 2.46 trillion. The report covers the North America Construction Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the North America Construction Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

North America Construction Market Research

Mordor Intelligence provides a comprehensive analysis of the construction industry and building sector. We leverage decades of expertise in construction consulting and market research. Our extensive report covers the full range of construction services. This includes residential construction, commercial construction, civil construction, and infrastructure construction. The analysis addresses crucial areas such as construction management, construction technology, and emerging trends in smart construction and building automation. Our report PDF, available for download, offers detailed insights into construction materials, building materials, and construction chemicals. It also includes a thorough analysis of the construction equipment and construction machinery markets.

The report provides invaluable insights for stakeholders across the construction sector. It is beneficial for those involved in architectural services, specialists in engineering construction, and experts in heavy construction. We deliver a detailed analysis of emerging trends like modular construction, prefabricated construction, and sustainable construction. Traditional segments such as building renovation and remodeling are also covered. The research examines developments in construction software, building systems, and green construction initiatives. It offers comprehensive coverage of construction equipment rental services and real estate construction developments. Our analysis supports strategic decision-making across the entire value chain, from construction services providers to materials suppliers. All insights are available in an easy-to-read report PDF format.