Market Size of North America Compound Chocolate Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

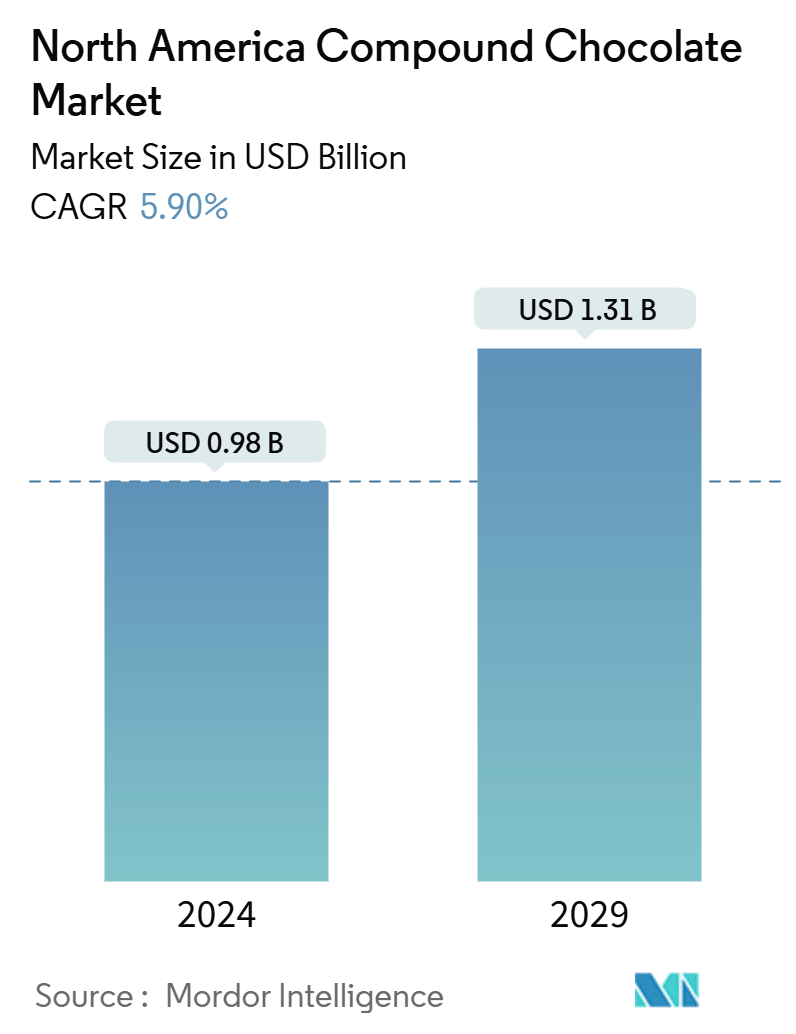

| Market Size (2024) | USD 0.98 Billion |

| Market Size (2029) | USD 1.31 Billion |

| CAGR (2024 - 2029) | 5.90 % |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order |

North America Compound Chocolate Market Analysis

The North America Compound Chocolate Market size is estimated at USD 0.98 billion in 2024, and is expected to reach USD 1.31 billion by 2029, at a CAGR of 5.90% during the forecast period (2024-2029).

North American consumers are increasingly gravitating towards snacking, seeking both indulgence and convenience. In response, manufacturers are turning to compound chocolate, using it to create in-demand snackable items such as chocolate-coated nuts, energy bars, and mini desserts. This strategy not only taps into the rising snacking trend but also provides a cost advantage. Many consumers are choosing milk and dark chocolates as preferred gifts, further boosting their consumption. On another front, single-origin chocolate, which offers detailed insights into its cocoa origins, is winning over consumers who value traceable supply chains. Additionally, the unique flavor profiles of single-origin chocolate, which vary by region, are drawing the attention of chefs, bakers, and chocolatiers who seek to elevate and differentiate their culinary creations.

Ingredient manufacturers, responding to the heightened demand for compound chocolate coatings, are adopting strategies like product innovation, expansion, mergers, acquisitions, and partnerships to gain a competitive edge. A notable example is Puratos' acquisition of Foley’s Chocolates in June 2023. Foley’s, a Canadian company celebrated for its authentic chocolate and compound coatings, propelled Puratos to become Canada's second-largest chocolate producer and the exclusive supplier of bakery, patisserie, and chocolate ingredients in the country. With a strategic focus on North America, Puratos is poised to introduce a range of health-oriented ingredients, aligning with evolving consumer tastes.

In conclusion, as North Americans indulge more in bakery and confectionery treats, the appetite for compound chocolate grows. Its versatility, cost benefits, and functional advantages solidify its status as a preferred choice. The increasing embrace by food manufacturers underscores its essential role in meeting consumer desires and addressing the operational needs of the bakery and confectionery sectors.

North America Compound Chocolate Industry Segmentation

The Food and Drug Administration (FDA) defines compound chocolates as cocoa products that incorporate either a cocoa butter substitute (CBS) or a cocoa butter equivalent (CBE). Commonly used vegetable fats include hard fats or semi-solid fats at room temperature, such as coconut oil and palm kernel oil.

The North American market for compound chocolate is categorized by flavor, product type, application, and geography. Flavors include dark, milk, white, and others. Product types encompass chocolate chips/drops/chunks, chocolate slabs, chocolate coatings, and others. Applications include bakery, confectionery, ice cream and frozen desserts, and others. The market growth is also analyzed in key countries like the United States, Canada, Mexico, and other parts of North America.

Market sizing is presented in USD value terms for all segments mentioned above.

| Flavor | |

| Dark | |

| Milk | |

| White | |

| Other Flavors |

| Product | |

| Chocolate Chips/Drops/Chunks | |

| Chocolate Slab | |

| Chocolate Coatings | |

| Other Products |

| Application | |

| Bakery | |

| Confectionery | |

| Ice Cream and Frozen Desserts | |

| Other Applications |

| Geography | |

| United States | |

| Canada | |

| Mexico | |

| Rest of North America |

North America Compound Chocolate Market Size Summary

The North American compound chocolate market is experiencing steady growth, driven by its technical advantages over traditional cocoa-based chocolates, such as lower costs and easier manufacturing processes. This makes compound chocolate an attractive option for food manufacturers across various sectors, including bakeries, confectionery, and frozen desserts. The flexibility in formulation and the use of vegetable fats like palm, soy, and coconut allow for innovative product development and a better sensory experience in snacks and baked goods. The increasing consumption of chocolate products, supported by their perceived health benefits, further fuels market expansion. Manufacturers are also introducing efficient alternatives to cocoa butter, enhancing the appeal of compound chocolate by simplifying production processes and offering tailored solutions to meet market demands.

The demand for chocolate and confectionery products in North America, particularly in the United States, is on the rise, with compound chocolate becoming a popular choice due to its cost-effectiveness and similar functionalities to regular chocolate. Milk compound chocolate, in particular, holds a significant market share, favored for its high micronutrient content and versatility in various applications. Major players like Hershey's have capitalized on this trend, benefiting from the growing popularity of milk chocolate. The market is relatively consolidated, with key players such as Barry Callebaut and Cargill leading the industry. These companies are focusing on business expansion and product innovation, with strategic partnerships and acquisitions further strengthening their market positions.

North America Compound Chocolate Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Drivers

-

1.1.1 High Consumption of Bakery Products

-

1.1.2 Food Manufacturers Inclination Toward Economical Confectionery Ingredients

-

-

1.2 Market Restraints

-

1.2.1 Rising Cocoa Prices Hampering Market Growth

-

-

1.3 Porter's Five Forces Analysis

-

1.3.1 Threat of New Entrants

-

1.3.2 Bargaining Power of Buyers/Consumers

-

1.3.3 Bargaining Power of Suppliers

-

1.3.4 Threat of Substitute Products

-

1.3.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION

-

2.1 Flavor

-

2.1.1 Dark

-

2.1.2 Milk

-

2.1.3 White

-

2.1.4 Other Flavors

-

-

2.2 Product

-

2.2.1 Chocolate Chips/Drops/Chunks

-

2.2.2 Chocolate Slab

-

2.2.3 Chocolate Coatings

-

2.2.4 Other Products

-

-

2.3 Application

-

2.3.1 Bakery

-

2.3.2 Confectionery

-

2.3.3 Ice Cream and Frozen Desserts

-

2.3.4 Other Applications

-

-

2.4 Geography

-

2.4.1 United States

-

2.4.2 Canada

-

2.4.3 Mexico

-

2.4.4 Rest of North America

-

-

North America Compound Chocolate Market Size FAQs

How big is the North America Compound Chocolate Market?

The North America Compound Chocolate Market size is expected to reach USD 0.98 billion in 2024 and grow at a CAGR of 5.90% to reach USD 1.31 billion by 2029.

What is the current North America Compound Chocolate Market size?

In 2024, the North America Compound Chocolate Market size is expected to reach USD 0.98 billion.