Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

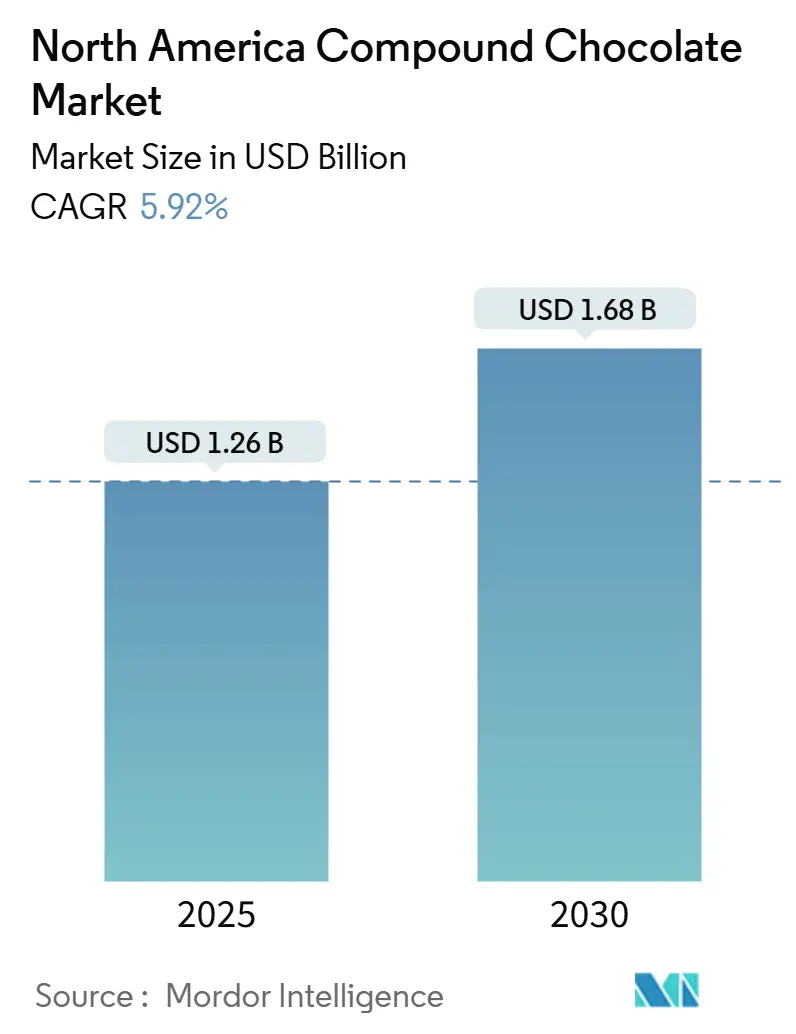

| Market Size (2025) | USD 1.26 Billion |

| Market Size (2030) | USD 1.68 Billion |

| Growth Rate (2025 - 2030) | 5.92% CAGR |

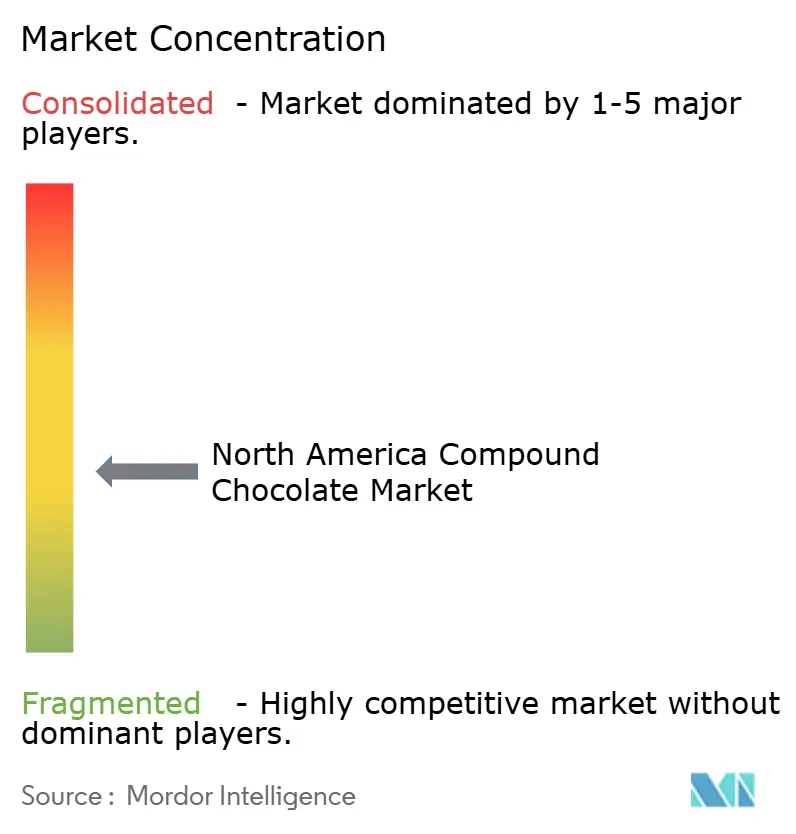

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Compound Chocolate Market Analysis by Mordor Intelligence

By 2030, the North American compound chocolate market, valued at USD 1.26 billion in 2025, is projected to reach USD 1.68 billion, marking a CAGR of 5.92%. This growth trajectory highlights the market's ability to navigate cocoa price fluctuations effectively. The World Bank reported that in 2024, cocoa prices averaged USD 7.33 per kilogram, a significant increase from USD 3.28[1]Source: World Bank, "World Bank Commodities Price Forecast", thedocs.worldbank.org. This surge is attributed to manufacturers' growing preference for compound formulations, which replace cocoa butter with more stable vegetable fats. The foodservice sector, which has been rebounding steadily, is a key driver of this demand. The International Foodservice Manufacturers Association anticipates a 0.9% growth in 2024, followed by a 1.0% uptick in 2025. Compound chocolates boast functional advantages, including easier processing and superior heat resistance, making them popular among bakeries, confectioners, and quick-service restaurants. Moreover, as consumers increasingly seek flavor diversity and prioritize clean-label products, there has been a notable rise in the incorporation of botanical, protein, and plant-based elements in compound chocolates. To further bolster their market position, players are making strategic moves, investing in digital supply chains and sourcing certified sustainable fats, ensuring resilience against procurement challenges and tightening regulations.

Key Report Takeaways

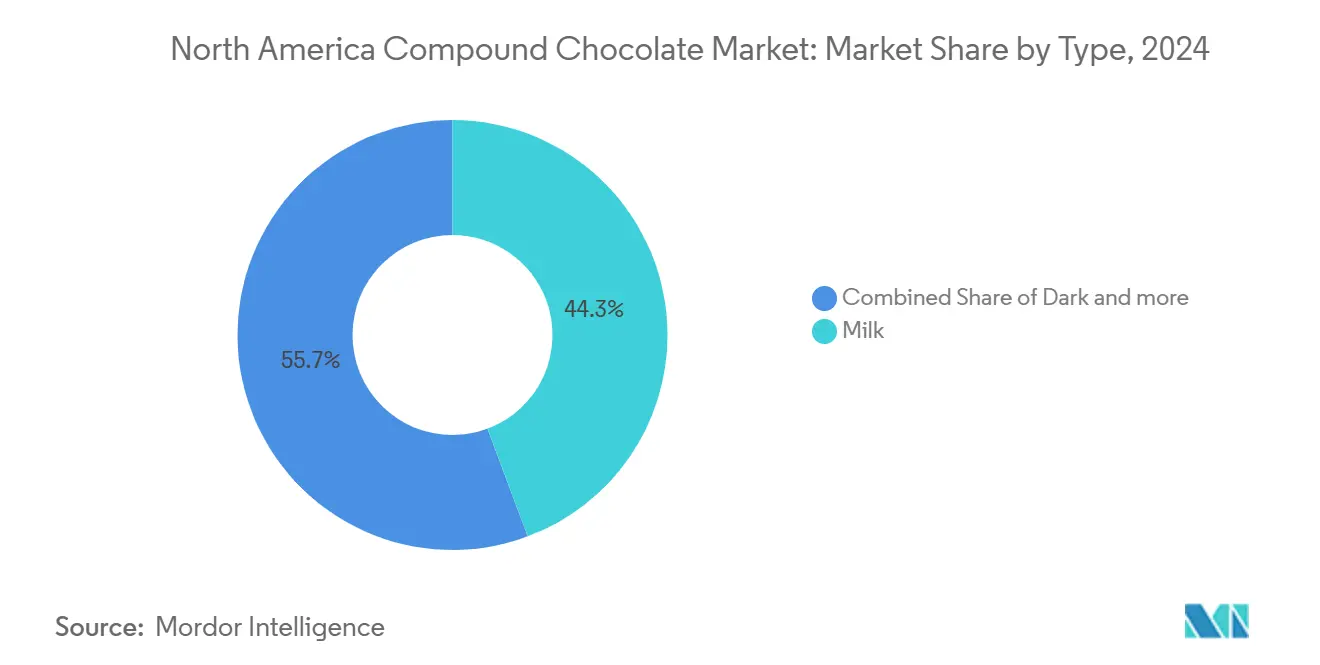

- By type, milk chocolate captured 44.30% of the North American compound chocolate market share in 2024, while dark chocolate is projected to advance at a 5.80% CAGR through 2030.

- By form, chips/drops/chunks controlled 36.30% of the North American compound chocolate market size in 2024, while fillings and spreads are set to expand at a 6.80% CAGR to 2030.

- By distribution channel, retail accounted for a 53.82% revenue share of the North American compound chocolate market size in 2024, and foodservice exhibits the strongest momentum, with a 6.47% CAGR forecasted to 2030.

- By geography, the United States led with a 32.43% share in 2024, whereas Canada recorded the fastest 6.16% CAGR outlook through 2030.

North America Compound Chocolate Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Versatility and functional benefits for food manufacturers | +1.2% | North America, with the strongest adoption in the United States industrial segments | Medium term (2-4 years) |

| Growth of the foodservice industry | +0.8% | United States and Canada, concentrated in the QSR and fast casual segments | Short term (≤ 2 years) |

| Surge in home baking and cooking | +0.6% | North America, particularly suburban United States and Canadian markets | Short term (≤ 2 years) |

| Innovation in flavor and inclusion | +0.9% | North America, led by premium segments in urban centers | Medium term (2-4 years) |

| Product diversity and customization | +0.7% | North America is, strongest in private label and co-manufacturing | Medium term (2-4 years) |

| Advancements in fat crystallization technology | +0.5% | North America, concentrated in major manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Versatility and functional benefits for food manufacturers

Food processors are increasingly adopting compound chocolate, driven by the need for manufacturing flexibility. These processors are turning to cost-effective alternatives to traditional chocolate, seeking to eliminate tempering requirements and broaden processing windows. By utilizing fractionated palm kernel oil and coconut oil in their formulations, manufacturers can achieve sensory profiles similar to those of chocolate. This approach not only mirrors the desired taste but also curtails the need for hefty investments in temperature-controlled production lines. The advantages of compound chocolate extend beyond mere processing ease. It boasts superior heat resistance and is less susceptible to fat bloom. These traits are especially vital for products aimed at foodservice channels, where temperature control can be inconsistent. Furthermore, with the advent of advanced oleogel systems, manufacturers can now cut saturated fat content by up to 39% without sacrificing taste or texture. This innovation meets the rising demand for clean-label products while ensuring functionality remains intact. Given these technical advantages, compound chocolate is emerging as a strategic ingredient for manufacturers, enabling them to optimize costs and differentiate their products in a competitive market.

Growth of the foodservice industry

Despite broader economic pressures, certain segments of the foodservice industry are showing resilience, leading to a targeted demand for compound chocolate applications. The National Restaurant Association reported that in June 2025, the U.S. restaurant industry's performance index reached a score of 100[2]Source: National Restaurant Association, "Restaurant Performance Index June 2025", restaurant.org. This segmentation is crucial for compound chocolate suppliers. Fast casual operators, for instance, often seek versatile coating and filling solutions. These solutions not only maintain quality over extended hold times but also support the rapid cycles of menu innovation. While the foodservice industry is projected to grow in 2025, it's essential to note the significant differences across various channels. Data from the US Census Bureau indicate that in 2024, sales from U.S. food service and drinking places reached approximately USD 1,121.3 billion, up from USD 1,094.08 billion the previous year. [3]. This trend indicates a growing demand for compound chocolate, particularly in the educational foodservice and hospitality sectors. As operators increasingly prioritize both operational efficiency and premium menu offerings, there's a growing opportunity for compound chocolate formulations. These formulations promise a chocolate-like indulgence while ensuring predictable cost management.

Surge in home baking and cooking

Shifts in consumer baking habits are driving a retail surge in demand for compound chocolate products. These products not only simplify home baking but also promise professional-quality results. What began as a pandemic-driven necessity has evolved into a lasting lifestyle change, with consumers now prioritizing ingredients that streamline the baking process without compromising on quality. Compound chocolate stands out for home bakers, thanks to its resilience to temperature fluctuations and the absence of tempering requirements. This makes it an ideal choice for those without professional tools or climate control. While sales of premium chocolates are on the rise, sales of everyday chocolate remain stagnant. This trend underscores consumers' willingness to invest in perceived quality enhancements. Such dynamics present a golden opportunity for positioning compound chocolate as a top-tier baking ingredient. With the retail channel commanding a 53.82% market share, it's evident that accessibility is key for consumers. Furthermore, the burgeoning e-commerce landscape is bridging the gap, allowing niche home baking communities to access specialized compound chocolate products tailored to their specific needs.

Innovation in flavor and inclusion

Manufacturers are rapidly innovating flavors, using the flexible formulation of compound chocolate to integrate trending ingredients and cater to shifting consumer tastes. Ingredients such as adaptogens, botanicals, and protein enhancements are driving growth in the nutritional balance chocolate sector, with turmeric, reishi, and spirulina at the forefront. The launch of plant-based compound bars by The Functional Chocolate Co., which combines Fair Trade cacao with botanicals supported by clinical research, underscores the market's growing embrace of premium functional formulations. Compound chocolate's ability to accommodate water-sensitive inclusions and heat-sensitive ingredients offers a distinct edge over traditional chocolate. This allows manufacturers to seamlessly integrate probiotics, prebiotics, and temperature-sensitive botanicals, ensuring stability. Such innovative capabilities resonate with many North American consumers eager for novel chocolate experiences, particularly Gen Z and Millennials who prioritize plant-based choices.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from pure chocolate products | -1.1% | North America is, strongest in premium retail segments | Medium term (2-4 years) |

| Sustainability and ethical sourcing concerns | -0.8% | North America, concentrated in conscious consumer segments | Long term (≥ 4 years) |

| Volatility in vegetable fat prices | -0.9% | North America, affecting all manufacturing segments | Short term (≤ 2 years) |

| Stringent food labeling regulations | -0.4% | US and Canada, impacting all commercial segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from pure chocolate products

As consumers increasingly equate pure chocolate with quality and authenticity, the compound chocolate market faces hurdles in its expansion. While premium chocolate segments flourish, everyday chocolate sales remain stagnant, underscoring consumers' readiness to invest in perceived quality. This trend poses challenges for compound chocolate, often viewed as a budget-friendly substitute. Brands championing single-origin, bean-to-bar, and artisanal chocolates emphasize transparency and craftsmanship, inadvertently casting compound chocolate in a less favorable light, even though it boasts functional benefits in certain uses. The perception issue deepens with major players like Hershey making strategic moves, such as acquiring premium brands like Lily's Sweets for USD 425 million, hinting at a pivot towards the more lucrative pure chocolate market. Yet, compound chocolate holds its ground in industrial settings, where its functionality, consistency, and cost predictability take precedence over consumer perceptions. This dynamic points to a split market: one side catering to premium consumer segments and the other focused on B2B applications.

Volatility in vegetable fat prices

In 2024, the World Bank reported a rise in palm oil prices, with the average reaching a nominal USD 963 per metric ton, up from USD 886. This price surge, coupled with erratic swings in soybean oil and broader commodity fluctuations, often spurred by geopolitical tensions and natural calamities, places a financial strain on manufacturers of compound chocolate. These producers, who rely on palm oil, coconut oil, and other vegetable fats, face both margin pressures and uncertainties in their supply chains. While cocoa butter prices adhere to set futures markets, the pricing of vegetable fats is swayed by a myriad of factors. These include Indonesia's palm oil export policies, weather conditions in Brazil, and disruptions in sunflower oil production from Ukraine. Such unpredictability has led manufacturers to bolster their price buffers from 25% to 30%. They've also turned to advanced hedging strategies. However, these measures risk diminishing the cost benefits that compound chocolate holds over its traditional counterpart, especially during surges in vegetable fat prices. The situation is further complicated by sustainability mandates that narrow sourcing avenues. For instance, Cargill's pledge in January 2024 to exclusively use RSPO-certified palm oil not only limits their supply flexibility but could also drive up costs.

Segment Analysis

By Type: Dark Chocolate Drives Premium Positioning

In 2024, milk chocolate commands a 44.30% market share, underscoring its entrenched consumer appeal and versatile applications. Meanwhile, dark chocolate, with a 5.80% CAGR projected through 2030, hints at shifting market dynamics, driven by its perceived health benefits and premium allure. Consumers are increasingly associating dark chocolate with its antioxidant properties and lower sugar content. This perception resonates with many North Americans who now expect their chocolate treats to offer health advantages. White chocolate finds its niche, predominantly in bakery and confectionery coatings, where its neutrality accentuates the visibility of other vibrant inclusions. The "Others" category showcases specialty offerings, from sugar-free and protein-enhanced to botanical-infused chocolates, catering to distinct market segments.

Compound chocolate formulations shine in dark chocolate applications, utilizing cocoa butter equivalents to achieve the desired snap and mouthfeel. This approach not only curbs costs but also enhances heat stability. The segment's upward trajectory is in sync with regulatory shifts, notably the FDA's updated definition of "healthy" food labeling, set for February 2025. This change could benefit dark chocolate formulations that align with the new nutritional benchmarks. Leveraging advanced oleogel technologies, dark compound chocolate formulations can now replace up to 50% of cocoa butter. This innovation retains sensory qualities, bolsters cost-efficiency, and champions clean-label strategies.

Note: Segment shares of all individual segments available upon report purchase

By Form, Fillings and Spreads Lead Innovation

In 2024, the chips/drops/chunks segment commands a 36.30% market share, underscoring its prevalent use in both home baking and industrial settings. Here, the emphasis on uniform sizing and consistent melting properties drives the choice. Meanwhile, the fillings and spreads segment emerges as the frontrunner, boasting a robust 6.80% CAGR through 2030. Innovations in texture modification and flavor delivery fuel this growth. Notably, compound chocolate offers advantages such as superior oil migration resistance and a longer shelf life compared to traditional fillings. These attributes are pivotal for manufacturers catering to retail and foodservice sectors, especially those with extended distribution timelines.

Slabs and blocks cater to industrial clients, providing bulk formats for subsequent processing. Coatings applications, on the other hand, capitalize on compound chocolate's ease of handling and resilience to temperature variations. The "Others" category serves as a catch-all for emerging formats, including powder applications and niche molding compounds. Highlighting the sector's dynamism, Fraunhofer IVV's research unveils ultrasonic treatments that bolster crystal formation. This advancement is particularly beneficial for filling applications, curbing oil migration and prolonging shelf life. Furthermore, adherence to FDA's 21 CFR 163 mandates meticulous formulation oversight, ensuring clear labeling distinctions between chocolate and its compound counterparts across all formats.

By Distribution Channel, Foodservice Momentum Accelerates

In 2024, retail channels capture a 53.82% market share, underscoring the significance of home baking and consumer accessibility. However, foodservice channels are on a faster track, boasting a 6.47% CAGR growth rate projected through 2030. This disparity in growth rates can be attributed to the recovery patterns in foodservice and the unique operational benefits that compound chocolate offers in commercial kitchens. Notably, the fast-casual restaurant sector is expanding more rapidly than its counterparts, fueling a specific demand for compound chocolate. This ingredient not only aids in menu innovation but also simplifies operations.

Industrial channels cater to B2B clients, such as food manufacturers, co-packers, and private label producers. These clients appreciate the processing benefits and cost predictability that compound chocolate offers. The segment is witnessing consolidation, with major manufacturers pursuing vertically integrated supply chains and uniform ingredient specifications. In a bid to enhance supply chain efficiency and elevate customer experience, Barry Callebaut has partnered with Microsoft for digital transformation. This move could hasten the industrial channel's adoption of compound chocolate, thanks to the enhanced service capabilities. Meanwhile, distribution dynamics are evolving. There's a clear divide: premium consumer applications lean towards traditional chocolate, while B2B applications are increasingly favoring compound chocolate, driven by its technical benefits.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

In 2024, the United States solidifies its position as North America's dominant player, commanding 32.43% of the region's value. In 2023, U.S. imports of chocolate and its compound ingredients exceeded USD 4.04 billion, underscoring a sophisticated logistics network that spans East Coast port clusters, Midwestern rail hubs, and temperature-controlled trucking corridors. Major multinationals, including Mondelez, Ferrero, and Barry Callebaut, capitalize on the U.S.'s strategic proximity to Canadian fat processors and cocoa sources in Latin America, streamlining their operations. The FDA's January 2028 deadline for nutrition labeling is set to synchronize reformulation efforts across states, facilitating the introduction of low-sugar compound bars and enhanced bakery products.

Canada is on a growth trajectory, with projections indicating a 6.16% CAGR through 2030. This surge is fueled by provincial investments in state-of-the-art food-processing parks and enhancements to the cold chain. In 2024, Canada accounted for nearly 50% of the U.S.'s chocolate ingredient imports, highlighting the strength of their cross-border supply chains. Foley’s Candies’ acquisition of Brockmann Chocolate boosts Canada's output capacity, allowing local facilities to cater to both domestic retailers and U.S. private labels with tailored compound spreads. Notably, Agriculture and Agri-Food Canada has observed a surge in demand for freezer-to-oven bakery items, a segment that prominently features compound coatings and fillings.

Mexico plays a dual role, supplying 15.1% of the U.S.'s chocolate imports and fostering indigenous compound manufacturing hubs in Toluca and Monterrey. Thanks to the USMCA's streamlined rules of origin, duties on vegetable-fat inputs have been reduced. This benefits Mexican plants that export compound chips back to the U.S. at competitive prices. However, Barry Callebaut's 2024 temporary shutdown in Toluca highlighted vulnerabilities in the logistics chain. In response, there's been a push for expanded capacity in the Bajío corridor. As Mexico contemplates specific tariff changes, compound suppliers are diversifying their sources, procuring palm fractions from refineries on the Pacific coast and specialty fat processors in Yucatán. Additionally, cross-border agricultural collaborations are exploring high-oleic sunflower oil as a viable alternative to palm fat, aiming to lessen dependence on Asian palm sources.

Competitive Landscape

The North American compound chocolate market is moderately fragmented. In 2024, Barry Callebaut, Cargill, and Blommer together accounted for over half of the sales in an oligopolistic market. They capitalized on advantages such as scale benefits in fat procurement, technical expertise, and diverse manufacturing sites. In Q1 2024/25, Barry Callebaut experienced a 1.9% decline in North American volumes, attributed to facility shutdowns and subdued OEM demand. In response, the company forged a USD 559 million digital transformation partnership with Microsoft, aiming to enhance automation in scheduling, inventory, and real-time quality control. Cargill stands out with its 100% RSPO-certified palm pipelines and collaborative studios that expedite customer innovations. Meanwhile, Blommer is bolstering its partnerships by offering tailored flavor systems to snack manufacturers.

AAK, a second-tier player, is focusing on specialty fat customization and collaborative pilot-plant trials, positioning itself to secure niche contracts in the burgeoning plant-based and sugar-free markets. Regional players, often backed by private equity, are adopting roll-up strategies, merging with mid-sized filling and planning specialists. This approach not only broadens their geographic footprint but also deepens their category expertise. Disruptors like WNWN Food Labs are venturing into uncharted territory, crafting cocoa-free chocolate alternatives and igniting discussions on redefining indulgence beyond conventional supply chains.

Today, competitive edge is increasingly tied to ESG credentials, technical services, and dependable supply chains. Multinational corporations are proactively offering lifecycle assessments and carbon dashboards, aligning with retailer mandates for scope 3 reporting. Through vertical integration and direct sourcing from farmers, these companies not only shield themselves from supply chain disruptions but also meet stringent provenance audits. Such strategies elevate entry barriers, solidifying the dominance of established players. Yet, they simultaneously carve out opportunities for nimble innovators to delve into micro-segments, driving swift flavor innovations.

North America Compound Chocolate Industry Leaders

-

Barry Callebaut Group

-

Cargill Incorporated

-

Fuji Oil Holdings Inc.

-

Puratos Group

-

AAK AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Ferrero North America introduced Ferrero Rocher-branded chocolate squares with a crispy chocolate shell, creamy filling, and crunchy hazelnut center. The product was made available in milk hazelnut, dark hazelnut, white hazelnut, caramel hazelnut, and assorted varieties.

- May 2025: Owned by Mondelēz International, Hu introduced new individually-wrapped filled chocolate bites. Targeting the on-the-go and post-dinner market, the bites come in three flavors: hazelnut butter, cashew butter, and creamy coconut.

- May 2025: The global chocolate manufacturer, Mars launched a new selection of Halloween products. The line includes new M&M's milk chocolate, peanut milk chocolate, and peanut butter milk chocolate blends. The seasonal portfolio also featured new variety packs for chocolate and candy brands such as Snickers, Milky Way, and Twix.

- February 2025: Former NFL player Ed McCaffrey and his family launched a line of plant-based, gluten-free, and non-GMO protein bites in the U.S. The company launched with three flavors: Chocolate Chip Cookie Dough, Birthday Cake, and Fudge Brownie, and these protein bites are designed to provide clean energy and are rich in fiber.

North America Compound Chocolate Market Report Scope

The Food and Drug Administration (FDA) defines compound chocolates as cocoa products that incorporate either a cocoa butter substitute (CBS) or a cocoa butter equivalent (CBE). Commonly used vegetable fats include hard fats or semi-solid fats at room temperature, such as coconut oil and palm kernel oil.

The North American market for compound chocolate is categorized by flavor, product type, application, and geography. Flavors include dark, milk, white, and others. Product types encompass chocolate chips/drops/chunks, chocolate slabs, chocolate coatings, and others. Applications include bakery, confectionery, ice cream and frozen desserts, and others. The market growth is also analyzed in key countries like the United States, Canada, Mexico, and other parts of North America.

Market sizing is presented in USD value terms for all segments mentioned above.

By Type

| Dark |

| Milk |

| White |

| Others |

By Form

| Chips/Drops/Chunks |

| Slabs and Blocks |

| Coatings |

| Fillings and Spreads |

| Others |

By Distribution Channel

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| Industrial | |

| Foodservice |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Type | Dark | |

| Milk | ||

| White | ||

| Others | ||

| By Form | Chips/Drops/Chunks | |

| Slabs and Blocks | ||

| Coatings | ||

| Fillings and Spreads | ||

| Others | ||

| By Distribution Channel | Retail | Supermarkets/Hypermarkets |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| Industrial | ||

| Foodservice | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Key Questions Answered in the Report

How large is the compound chocolate market in North America in 2025?

The compound chocolate market size equals USD 1.26 billion in 2025 and is projected to reach USD 1.68 billion by 2030 at a 5.92% CAGR.

Which segment grows fastest through 2030?

Dark compound chocolate records the quickest 5.80% CAGR as consumers pursue perceived health benefits and premium flavor depth.

Why do foodservice operators prefer compound coatings?

Compound chocolate’s no-temper processing, extended heat tolerance, and predictable costing suit quick-service and campus kitchens that need consistent performance under variable holding temperatures.

What is driving Canadian market momentum?

Investments in advanced processing parks, integration with U.S. supply chains, and rising demand for convenience bakery goods push Canada toward a 6.16% CAGR through 2030.

How are suppliers addressing sustainability concerns?

Leading firms adopt 100% RSPO-certified palm oil, publish traceability dashboards, and invest in carbon-reduction programs to meet retailer and consumer expectations.

Which companies dominate the competitive landscape?

Barry Callebaut, Cargill, and Blommer together control just over 50% of regional sales, leveraging scale advantages in sourcing, technology, and multi-site manufacturing.

Page last updated on: