Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

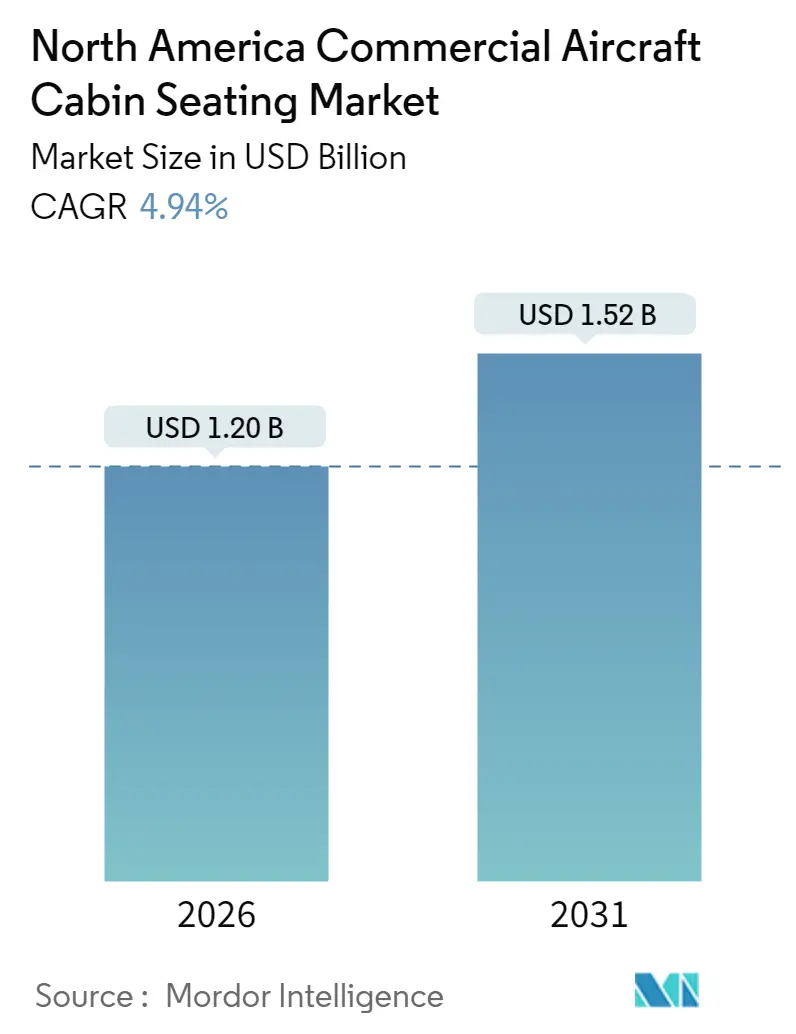

| Market Size (2026) | USD 1.2 Billion |

| Market Size (2031) | USD 1.52 Billion |

| Growth Rate (2026 - 2031) | 4.94% CAGR |

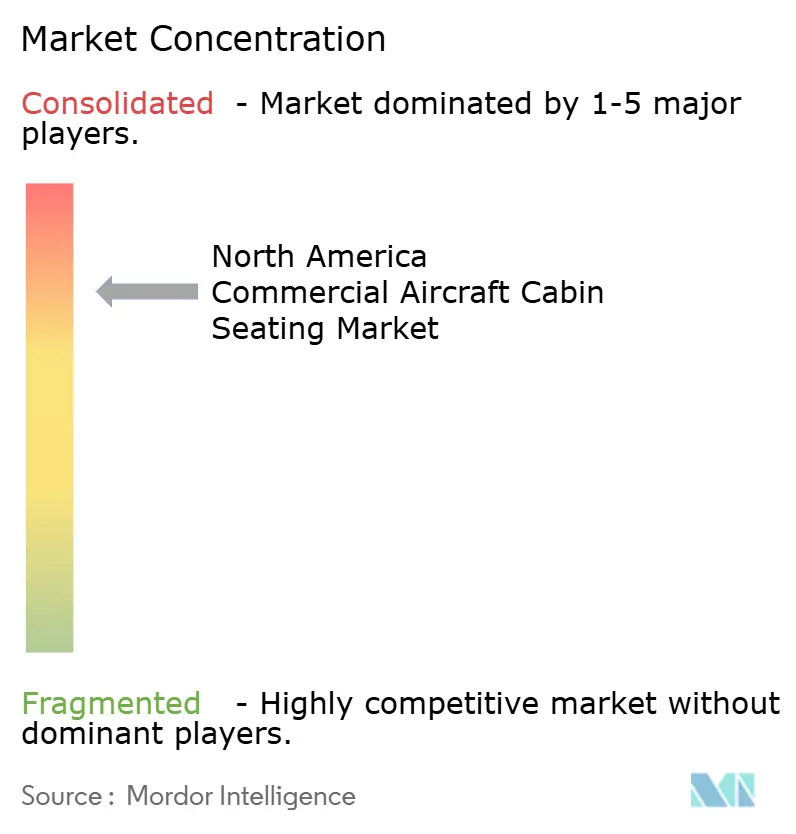

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Commercial Aircraft Cabin Seating Market Analysis by Mordor Intelligence

The North American commercial aircraft cabin seating market is expected to grow from USD 1.14 billion in 2025 to USD 1.2 billion in 2026 and is forecast to reach USD 1.52 billion by 2031 at 4.94% CAGR over 2026-2031. This outlook highlights how fleet renewal programs, premium cabin retrofits, and safety-driven seat replacement cycles converge to sustain growth. Airlines are pivoting toward higher-yield seating layouts that balance revenue enhancement with regulatory compliance, while suppliers race to deliver lighter, more innovative, and more modular seat families. Competitive intensity remains high because three Tier-1 manufacturers —Collins Aerospace, Safran, and Recaro —control most linefit positions and a growing portion of retrofit contracts. Their scale advantages in certification, global manufacturing, and after-sales support help them defend their market share even as smaller innovators carve out niches in composites and advanced ergonomics. Weight-reduction mandates linked to the adoption of sustainable aviation fuel (SAF) and emerging electric vertical take-off and landing (eVTOL) programs create long-tail demand pools, reinforcing the sector’s medium-term momentum. Supply-chain tightness surrounding foams and actuators still imposes cost pressure; yet, airlines continue to prioritize cabin updates over deferrals because premium seats deliver substantial payback through ancillary revenue streams.

Key Report Takeaways

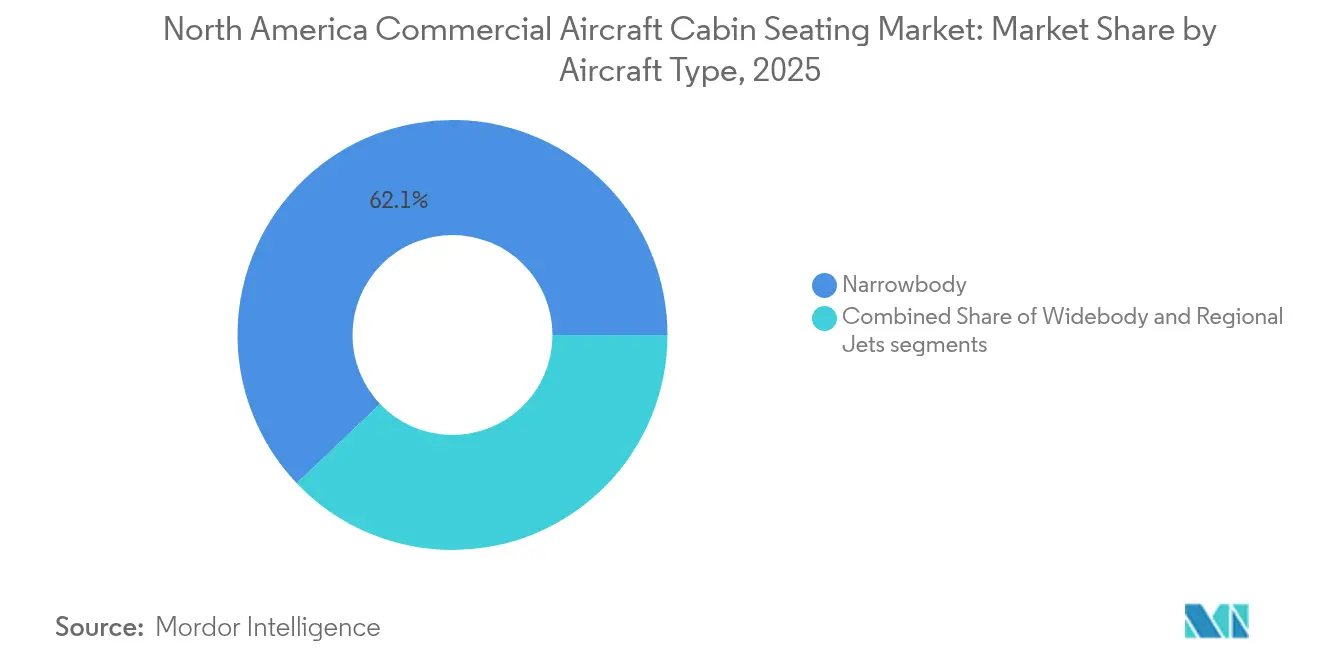

- By aircraft type, narrowbody programs held 62.10% of the commercial aircraft cabin seating market share in 2025, while the widebody category is projected to grow at a 5.78% CAGR through 2031.

- By seat class, the economy accounted for 53.65% of the commercial aircraft cabin seating market size in 2025, whereas the premium economy tracked a 7.49% CAGR from 2026 to 2031.

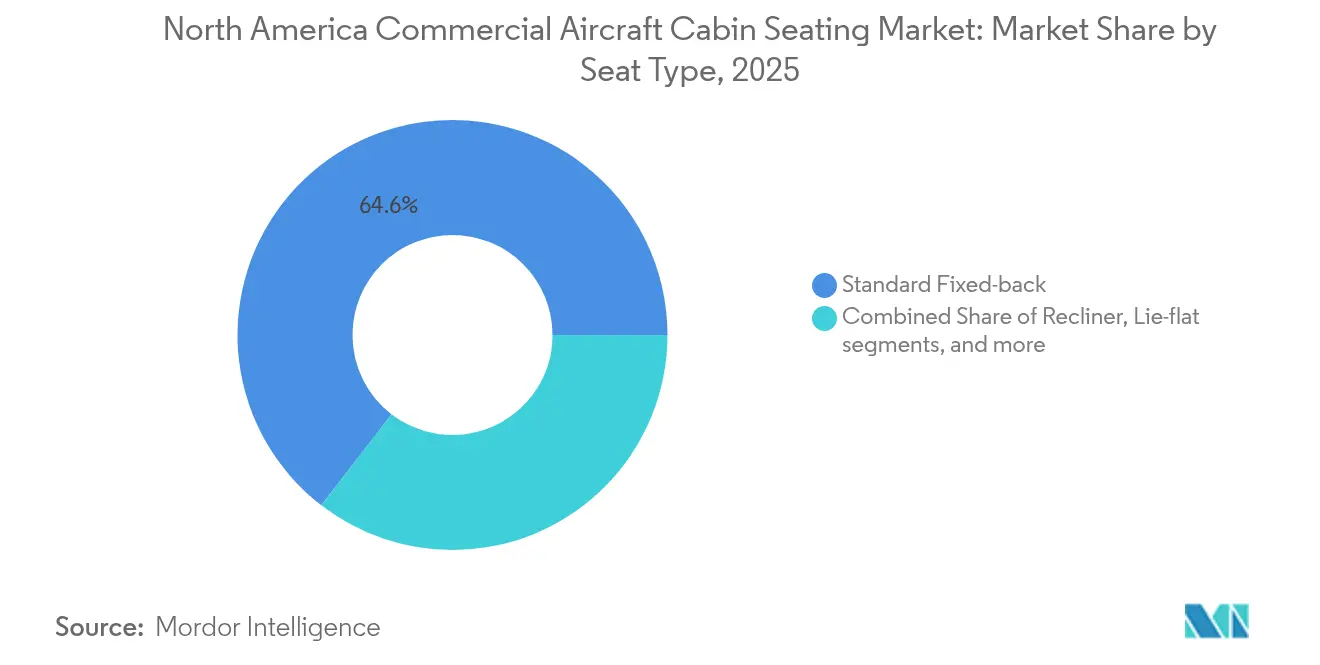

- By seat type, standard fixed-back designs captured 64.55% of the commercial aircraft cabin seating market share in 2025, while suite or full-privacy products are projected to advance at an 8.06% CAGR through 2031.

- By fit type, linefit installations accounted for 65.05% of the commercial aircraft cabin seating market size in 2025; retrofit activity is rising at a faster rate of 6.61% CAGR across the forecast horizon.

- By geogrpahy, the United States is expected to account for 92.10% of the regional market share in 2025. Additionally, the United States market is projected to grow at a CAGR of 4.26%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Commercial Aircraft Cabin Seating Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward lightweight composite seat frames | +0.8% | North America and global export demand | Medium term (2-4 years) |

| Airlines’ premium-cabin retrofits to capture high-yield flyers | +1.2% | United States and Canada core markets | Short term (≤ 2 years) |

| FAA 16G/21G dynamic-test rules triggering replacement cycles | +0.9% | United States primary, spillover to Canada | Medium term (2-4 years) |

| AAM and eVTOL certification creating new seat demand | +0.3% | North America and early-adopter EU hubs | Long term (≥ 4 years) |

| Integration of smart-seat sensors unlocking ancillary revenues | +0.4% | North America and trans-Atlantic operators | Medium term (2-4 years) |

| Long-term SAF adoption incentivizing seat weight reduction | +0.6% | Global, with North America leading compliance | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Shift Toward Lightweight Composite Seat Frames

Advanced composites such as carbon-fiber-reinforced plastics, titanium alloys, and high-performance thermoplastics are replacing aluminum because every kilogram removed from a seat saves fuel and, by extension, offsets the higher cost of SAF. Expliseat’s TiSeat 2X exemplifies the commercial traction of this material shift by delivering a 30% lower weight compared to legacy economy seats while maintaining 16G standards.[1]Expliseat Engineering Team, “TiSeat 2X Technical Data Sheet,” expliseat.com Airlines increasingly view lighter seats as a low-risk avenue to achieve near-term emissions reductions that regulators may soon formalize. Automated fiber-placement and resin-transfer-molding techniques lower production costs, enabling adoption beyond premium cabins. As composite prices converge with those of aluminum, North American carriers evaluate fleet-wide rollouts during thorough checks, locking in multi-year demand for raw materials and certification engineering.

Airlines’ Premium-Cabin Retrofits to Capture High-Yield Flyers

Retrofits aimed at premium economy and next-generation business suites generate up to 33% more revenue per square foot than baseline economy layouts, a spread too attractive for the US majors to ignore.[2]Collins Aerospace, “Seating Solutions Product Brief,” collinsaerospace.com American Airlines plans to upgrade 30 aircraft with Flagship Suite products by 2029. Delta Air Lines and United Airlines have already completed or announced similar programs that increase premium-seat density without adding new airframes. Korean Air, Finnair, and other overseas carriers provide proof points that North American airline boards study when green-lighting capital spend. Suppliers benefit because retrofits bypass OEM linefit scheduling constraints and often involve full ship-sets of seats, monuments, and associated electronics, resulting in average project values exceeding USD 5 million for a single B777 or A330.

FAA 16G/21G Dynamic-Test Rules Triggering Replacement Cycles

The Federal Aviation Administration's (FAA's) AC 20-146A mandates that seats withstand 16G forward and 21G downward dynamic loads, requirements that older seat families cannot meet without redesign. Operators with pre-2009 aircraft must replace non-compliant seats during major maintenance events to retain airworthiness certificates.[3]Federal Aviation Administration, “AC 20-146A – Aircraft Seat Safety Standards,” faa.gov Since many US fleets average 14-16 years of age, the resulting replacement wave will peak over the next two heavy-check cycles. Certification bottlenecks advantage incumbents with in-house sled-testing rigs and regulatory relationships, further concentrating market power among top suppliers.

Integration of Smart-Seat Sensors Unlocking Ancillary Revenues

Sensor-enabled seats capture occupancy, position, and biometric data, allowing airlines to offer pay-per-use upgrades, enhance crew efficiency, and schedule predictive maintenance. TG0’s single-surface pressure-mapping prototype, developed through Airbus BizLab, demonstrates that smart functionality can add less than 500 g to seat weight, preserving fuel-burn goals.[4]Airbus BizLab, “TG0 Pressure-Mapping Seat Sensor Prototype,” airbus.com Early field tests indicate ancillary revenue gains of USD 15-25 per passenger annually and maintenance savings of approximately 10% of seat-related expenditures. As Wi-Fi penetration approaches fleet-wide coverage in the US, airlines now have the connectivity backbone to monetize real-time seat data, accelerating adoption.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High certification costs and lead times | –0.7% | United States and Canada | Medium term (2-4 years) |

| Shortages of high-spec foams and actuators | –0.9% | Global supply chain, North American demand concentration | Short term (≤ 2 years) |

| Airline capex cyclicality tied to jet-fuel prices | –0.6% | North America core, global spillover | Short term (≤ 2 years) |

| Cabin floor-loading limits constraining seat redesigns | –0.4% | Global aircraft design constraints | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Certification Costs and Lead Times

Obtaining a supplemental type certificate for a new seat family can cost USD 2-5 million and run 18-24 months, reflecting extensive sled testing, flame-propagation trials, and electromagnetic interference checks under FAA and Transport Canada rules. Smaller suppliers face cash-flow stress because work starts long before revenue recognition, limiting market entry and curbing innovation velocity. Airlines also suffer when novel designs slip their schedules, forcing them to adopt already-certified products that may not align with their branding goals.

Shortages of High-Spec Foams and Actuators

Premium lie-flat and suite seats incorporate fire-resistant foams, precision actuators, and custom control units sourced from a narrow vendor pool. Pandemic-era shutdowns and semiconductor tightness created backlogs of 12-18 months for these components, delaying deliveries and inflating prices by up to 25% during 2024-2025. Although capacity is coming back online, further shocks ranging from specialty-chemical outages to geopolitical trade restrictions could again ripple through the supply chain, constraining the commercial aircraft cabin seating market during peak retrofit cycles.

Segment Analysis

By Aircraft Type: Widebody Upgrades Gain Altitude

The commercial aircraft cabin seating market size linked to narrowbody programs accounted for 62.10% of total revenue in 2025. Single-aisle aircraft dominate domestic networks in the United States and Canada, and operators such as Southwest, JetBlue, and WestJet refresh cabins every five to seven years to remain competitive. Narrowbody seat selections, therefore, prioritize maintainability and quick-turn features like replaceable dress covers and modular IFE docks. In contrast, the widebody segment is posting a faster 5.78% CAGR because the revival of transpacific and transatlantic travel drives demand for lie-flat suites and premium-economy recliners on the B787, A350, and A330-900neo. Widebody retrofits command higher bill-of-materials values, sometimes exceeding USD 15 million per aircraft, as they involve galleys, lavatories, and social areas.

Growth in regional jets is limited as scope-clause limits in US pilot contracts cap the number of 76-seat aircraft at major carriers. Nevertheless, Embraer’s E195-E2 and A220 blur the line between regional and mainline equipment, generating incremental seating orders that include mainline amenities such as power at every seat and Bluetooth-ready headsets. Airlines use these jets to right-size thin routes, thereby widening the addressable market for economy-plus and slimline recliners tailored to flights under three hours.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Seat Class: Premium Economy Unlocks New Margin Layers

Economy cabins still represent 53.65% of the commercial aircraft cabin seating market share, yet monetization strategies increasingly hinge on segmenting that space into basic economy, standard, and extra-legroom tiers. Airlines deploy modular seat tracks that allow densification or relaxation without structural rework. Premium economy is projected to expand at a 7.49% CAGR, as it offers a yield uplift of 50-70% over economy for a footprint that is only 6-8 inches deeper, making the return on invested capital highly attractive. Carriers that historically avoided a fourth cabin, such as United, which has since introduced its Polaris rollout, now champion premium economy seats around their business cabins, citing sustained demand among price-sensitive corporate travelers.

Business class suites are shifting to flush-door privacy concepts initially limited to first-class. Airlines believe that superior sleep quality and personal-space metrics justify the incremental weight, which can be offset by using carbon-composite frames and foam-core tray tables. First-class presence declines as operators like Delta and Air Canada down-gauge legacy first products. Yet, a boutique niche persists on transcontinental and ultra-long-haul routes, where ticket prices remain inelastic.

By Seat Type: Suites Outpace Fixed-Back Workhorses

Standard fixed-back seats captured 64.55% of the commercial aircraft cabin seating market share in 2025 because they dominate volume-driven narrowbody and regional jet cabins. Design priorities center on lightweight skeletons, quick-change dress covers, and cost-effective hard points for USB-C power. Recliner seats serve domestic first-class footprints on short-haul fleets, offering enhanced pitch without the engineering complexity of lie-flat mechanisms.

Suite and full-privacy modules enjoy the highest 8.06% CAGR because competing airlines treat door-equipped business seats as must-have differentiators on long-haul routes. Recaro’s R7, Collins’ Elements suite, and Safran’s Unity platform headline active campaigns, each integrating wireless charging pads, customizable mood lighting, and space-saving shield geometry. Lie-flat products without doors still hold a significant share on single-aisle transcontinental aircraft, where space and center-of-gravity constraints limit the feasibility of suites.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Fit Type: Retrofit Wave Redefines After-Market Economics

Linefit installations accounted for 65.05% of the commercial aircraft cabin seating market size in 2025 because every new airframe leaves the final assembly line with a complete cabin. Yet, chronic delivery delays at Airbus and Boeing force operators to utilize existing assets, making retrofit activity the growth engine with a 6.61% CAGR. Ship sets frequently bundle seats, PSUs, and lighting upgrades, with turnkey integrators coordinating STC paperwork to minimize downtime. Airlines such as WestJet and Alaska Air have publicly cited ROI windows of 18-24 months for premium-heavy retrofit programs that boost unit revenue without adding aircraft.

Retrofit schedules closely tied to C and D checks, incentivizing seat makers to pre-certify configurations for multiple aircraft types, allowing airlines to reuse standard parts across their fleets. That approach lowers inventory costs and simplifies maintenance, while allowing carriers to standardize their branding.

Geography Analysis

The US drives the bulk of the commercial aircraft cabin seating market demand, owing to its world’s largest domestic network and a premiumization race among American Airlines, Delta Air Lines, and United Airlines. American Airlines alone operates roughly 1,000 mainline aircraft, creating a replacement pool of more than 200,000 individual seats every eight-year cycle. FAA certification rules are the strictest worldwide, compelling suppliers to maintain test labs and engineering offices in-country to accelerate project turnarounds. The US carriers are also early adopters of smart-seat sensors because widespread on-board Wi-Fi and data analytics suites enable real-time monetization.

Canada contributes a sizable share anchored by Air Canada’s mainline and Rouge fleets, WestJet’s transition toward full-service positioning, and Porter’s E195-E2 expansion. Transport Canada’s bilingual labeling requirements and flammability directives add unique certification layers, but suppliers accept this complexity to retain access to over 400 active airframes. Cross-border commonality in aircraft types enables the US STCs to be transferred with minimal rework, thereby shortening lead times for Canadian retrofits.

Mexico delivers smaller yet faster-rising volumes. Passenger recovery in Mexican leisure markets, combined with continuing ULCC growth, spurs densified cabin layouts that favor lightweight, slimline designs. However, premium-economy adoption is gaining traction on long-haul routes to Europe and South America, signaling an upward shift in the mix that aligns with the broader regional trend. Regulatory convergence toward FAA standards is accelerating because many carriers lease the US-registered aircraft, which must meet American compliance thresholds regardless of operating base.

Competitive Landscape

Collins Aerospace invested USD 2 million to expand executive-seat production in Florida, an example of localized capacity expansion tailored to quick-turn VIP and corporate shuttle campaigns. Safran leverages broader interiors portfolios, bundling galleys, lavatories, and oxygen systems alongside seats to capture full-cabin work scopes, which dilutes the bidding field for single-commodity competitors.

Tier-II players, such as Expliseat, Geven, and STELIA, rely on niche competencies in composites, light aircraft, or regional-jet cabins. Expliseat’s 10-year deal with Air France for TiSeat 2X and Recaro’s 75,000-seat order from Eve’s eVTOL program illustrate how specialization can yield meaningful volume outside traditional airline linefits. However, these entrants must navigate capacity scaling and repetitive-strain testing hurdles to move into premium suites, a segment that sets the pricing ceiling.

Strategically, incumbents focus on predictive-maintenance ecosystems that lock airlines into proprietary digital platforms. Collins joined the Airbus Digital Alliance to integrate seat sensor data with Skywise, offering AOG-avoidance analytics that competitors without cloud backbones cannot replicate. Safran’s acquisition of Collins’ flight-control activities provides cross-selling leverage by marrying cockpit solutions with cabin offers, a bundle particularly attractive during widebody retrofit negotiations. Recaro emphasizes ergo-centric design IP and rapid custom trim changes as differentiators for boutique flag carriers seeking distinctive brand identities.

North America Commercial Aircraft Cabin Seating Industry Leaders

JAMCO Corporation

Collins Aerospace (RTX Corporation)

RECARO Aircraft Seating GmbH & Co. KG (RECARO Holding GmbH)

Safran SA

Thompson Aero Seating Limited (Aviation Industry Corporation of China)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Starling Aerospace acquired Pitch Aircraft Seating's assets, including 9.6 kg PF3000 economy seats, thereby expanding Starling's footprint in lightweight narrowbody applications.

- February 2025: FAA cleared a new three-point seat-belt airbag system for Airbus A321neo ACF/XLR models, unlocking higher-density layouts without compromising safety.

- December 2024: LifePort purchased PAC Seating, extending LifePort’s catalog into specialized medical-evacuation and executive-configured cabin products.

- September 2024: LATAM Airlines launched a USD 360 million program to retrofit 24 B787s with Recaro R7 door-equipped suites for long-haul routes.

North America Commercial Aircraft Cabin Seating Market Report Scope

By Aircraft Type

| Narrowbody |

| Widebody |

| Regional Jets |

By Seat Class

| First Class |

| Business Class |

| Premium Economy Class |

| Economy Class |

By Seat Type

| Standard Fixed-back |

| Recliner |

| Lie-flat |

| Suite/Full-privacy |

By Fit Type

| Linefit |

| Retrofit |

By Geography

| United States |

| Canada |

| Mexico |

| By Aircraft Type | Narrowbody |

| Widebody | |

| Regional Jets | |

| By Seat Class | First Class |

| Business Class | |

| Premium Economy Class | |

| Economy Class | |

| By Seat Type | Standard Fixed-back |

| Recliner | |

| Lie-flat | |

| Suite/Full-privacy | |

| By Fit Type | Linefit |

| Retrofit | |

| By Geography | United States |

| Canada | |

| Mexico |

Need A Different Region or Segment?

Customize Now

Market Definition

- Product Type - The seats that are integrated into the passenger aircraft and which are made up of a different combination of materials are included in this study.

- Aircraft Type - All the passenger aircraft such as narrowbody and widebody which are single-aisle and twin-aisle are included in this study.

- Cabin Class - Business and First Class, economy and premium economy are classes of air travel provided by the airlines that offer various services to the passengers.

| Keyword | Definition |

|---|---|

| Gross domestic product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| High Dynamic Range (HDR) | Dynamic range describes the ratio between the brightest and darkest parts of an image. HDR is used to capture a greater dynamic range than SDR. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| European Aviation Safety Agency (EASA) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| 4K Display | 4K resolution refers to a horizontal display resolution of approximately 4,000 pixels. |

| Organic Light Emitting Diode (OLED) | It is the light-emitting diode (LED) in which the emissive electroluminescent layer is a film of organic compound that emits light in response to an electric current. |

| Mean Time Between Failures (MTBF) | The mean time between failures is the predicted elapsed time between inherent failures of a mechanical or electronic system, during normal system operation. |

| (Low-Cost Carrier (LCCs) | It is an airline that is operated with an especially high emphasis on minimizing operating costs and without some of the traditional services and amenities provided in the fare |

| Electronically Dimmable Windows (EDW) | It is a type of window that blocks up to 99.96% of all visible light and provide full opacity, integrated into the window cassette of the sidewall panel. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step 1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step 2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step 3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF