Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 305.06 Million |

| Market Size (2030) | USD 453.59 Million |

| Growth Rate (2025 - 2030) | 8.26% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Commercial Aircraft Cabin Lighting Market Analysis by Mordor Intelligence

North America's commercial aircraft cabin lighting market stands at USD 305.06 million in 2025 and is forecasted to reach USD 453.59 million by 2030, advancing at an 8.26% CAGR. Robust narrowbody production schedules, an expanding retrofit pipeline, and airline focus on passenger-experience upgrades underpin this momentum. Continuous monthly deliveries of more than 90 single-aisle jets sustain OEM linefit demand, while the large US carrier retrofit programs accelerate aftermarket revenues. Regulatory preference for energy-efficient LED systems and rising premium-cabin investments further strengthen growth prospects. Suppliers able to navigate certification complexity, component shortages, and the shift toward smart, IoT-ready solutions are positioned to capture disproportionate value in the commercial aircraft cabin lighting market.

Key Report Takeaways

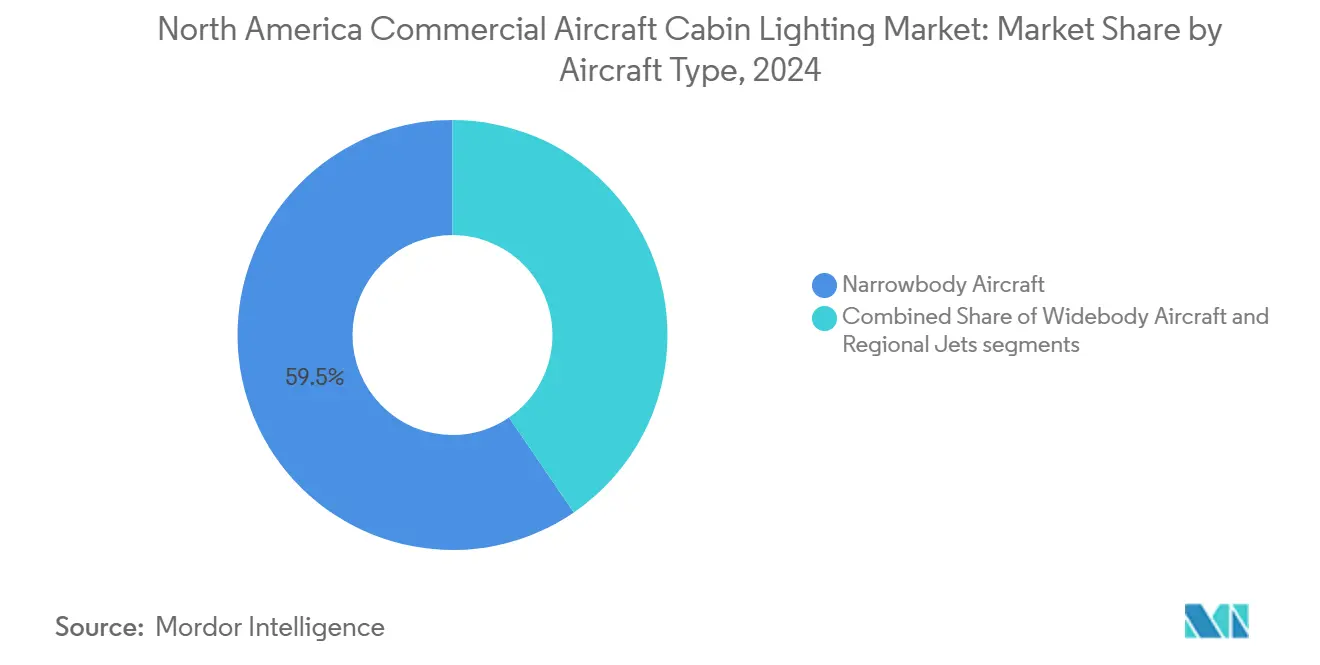

- By aircraft type, narrowbody aircraft led with 59.55% revenue share in 2024; regional jets are projected to expand at an 8.12% CAGR through 2030.

- By light type, reading lights commanded 37.12% of 2024 sales, while floor-path lighting strips are advancing at a 9.56% CAGR to 2030.

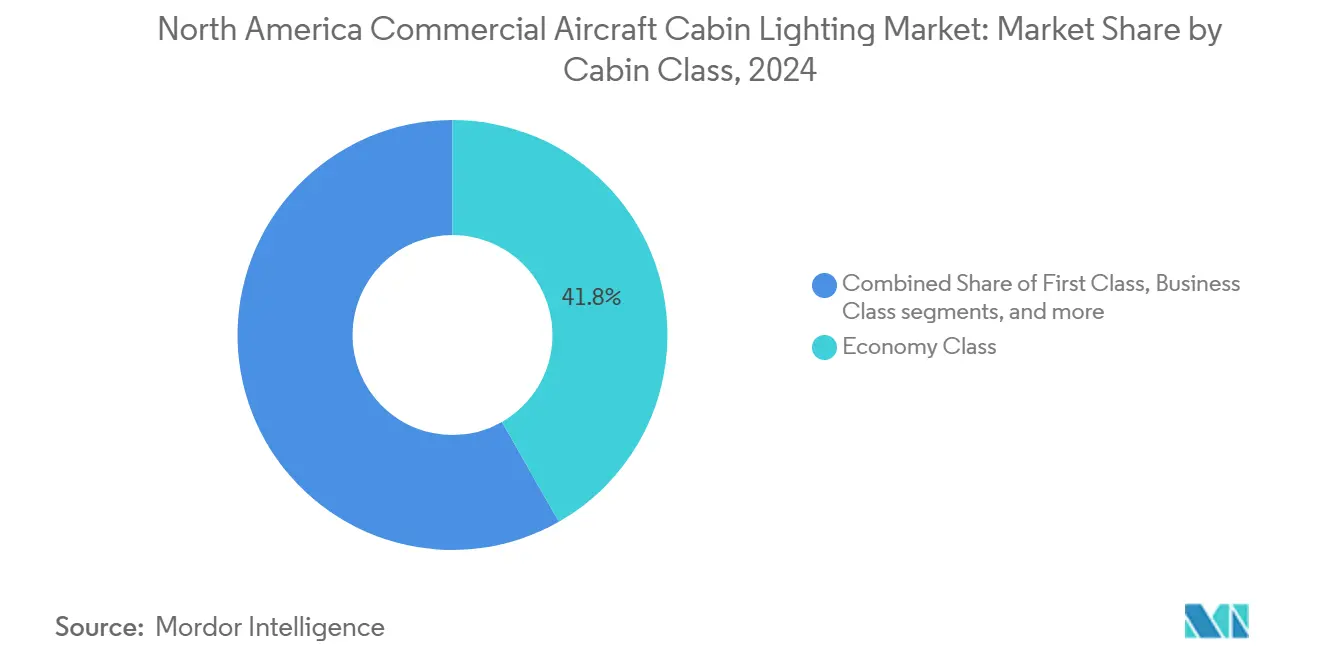

- By cabin class, economy class accounted for a 41.76% share in 2024; premium economy is growing the fastest at a 9.87% CAGR through 2030.

- By end user, OEM linefit installations held 56.45% share in 2024; aftermarket/retrofit activity is rising at a 9.23% CAGR to 2030.

- By geography, the United States captured 61.22% of 2024 revenue, whereas Canada is forecasted to register the quickest pace at a 7.23% CAGR through 2030.

North America Commercial Aircraft Cabin Lighting Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet growth of narrowbody aircraft | +2.1% | United States and Canada | Medium term (2-4 years) |

| Airline retrofit programs for LED mood-lighting | +1.8% | The US core; Canada secondary | Short term (≤ 2 years) |

| Regulatory push for energy-efficient cabin lighting | +1.4% | FAA and Transport Canada jurisdictions | Long term (≥ 4 years) |

| Rising premium-cabin upgrade investments | +1.2% | Major hub airports and premium routes | Medium term (2-4 years) |

| IoT-enabled smart lighting integration | +0.9% | Tech-forward carriers across new-build programs | Long term (≥ 4 years) |

| Circadian-rhythm adaptive lighting demand | +0.7% | Long-haul routes serving premium passenger segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fleet Growth of Narrowbody Aircraft

Monthly deliveries of more than 90 A320neo and B737 MAX aircraft continue through mid-2025, keeping assembly slots fully booked and ensuring a steady pull-through of linefit lighting ship-sets.[1]Antoine Fafard, “Data: Airbus & Boeing Narrowbody Deliveries For June 2025,” Aviation Week, aviationweek.com Airlines simultaneously accelerate retrofits on earlier-generation narrowbodies so that cabin ambiance matches new-build standards, expanding the aftermarket revenue pool. McKinsey projects single-aisle production to remain elevated through 2029, signaling multi-year visibility for lighting suppliers and allowing them to scale component procurement efficiently. The uniformity of narrowbody flight cycles also drives higher lamp-hour consumption, shortening replacement intervals compared with widebody fleets. This nonstop demand loop contributes a +2.1% lift to the forecast CAGR, making narrowbody output the single most powerful volume driver in the North American commercial aircraft cabin lighting market.

Airline Retrofit Programs for LED Mood-lighting

Delta’s completion of a 42-aircraft A330 LED upgrade in late 2024 proved that a full widebody retrofit can be executed in six hours of ground time without structural rewiring, cutting power draw by 40% and saving about 30 kg per airframe.[2]STG Aerospace Editorial Team, “STG Aerospace Supports Delta’s A330 Cabin Lighting Refresh,” stgaerospace.com Similar programs in the US and Canada validate the fast payback from energy savings and improved Net Promoter Scores, prompting carriers to allocate larger portions of interior-refresh budgets to lighting. Plug-and-play kits reduce engineering labor, enabling airlines to schedule work during routine A-checks instead of extended heavy checks. After retrofit, carriers gain branding flexibility through software-controlled color scenes that align with service cues. Together, these factors add about +1.8% to market CAGR, positioning retrofits as the fastest-growing revenue stream for suppliers.

Regulatory Push for Energy-efficient Cabin Lighting

FAA Engineering Brief 67D formally endorses LEDs but sets strict thresholds for brightness perception, flicker, and electromagnetic compatibility. This pushes airlines toward electronically controlled fixtures that can meet the new criteria at lower power settings.[3]Federal Aviation Administration, “Engineering Brief No. 67D, Light Sources Other than Incandescent and Xenon for Airport and Obstruction Lighting Fixtures,” faa.gov Transport Canada mirrors most of these rules, creating a contiguous market with harmonized certification pathways. Because six 700 K white LEDs achieve equal perceived brightness at only 67% of the luminance required by incandescent lamps, airlines realize direct fuel and emissions savings even before considering maintenance reductions. These savings translate into favorable total-cost-of-ownership calculations that accelerate purchase decisions. The regulatory tailwind adds roughly +1.4% to the projected CAGR by driving mandatory fleet-wide upgrades over the long term.

Rising Premium-cabin Upgrade Investments

Airlines increasingly rely on premium-economy cabins to boost unit revenues, and mood lighting is a centerpiece of the upgraded experience; Delta’s ongoing cabin revamp uses dynamic color scenes to distinguish service phases and support circadian comfort on transcontinental routes.[4]Kelly Yamanouchi, “Delta Is Revamping Its Aircraft Cabins With New Seat Colors, Mood Lighting,” ajc.com Premium-cabin fixtures feature RGBW emitters capable of millions of hues, allowing carriers to reinforce brand identity without hardware swaps. Passenger surveys show higher satisfaction scores when lighting synchronizes with boarding, meal, and rest periods, giving airlines a measurable return on investment. As more North American carriers densify premium-economy layouts, order volumes for zone-programmable lights rise. The trend contributes +1.2% to CAGR, anchored by sustained margins on higher-spec products.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electronic-component supply-chain volatility | −1.6% | Global, with strong North American manufacturing link | Short term (≤ 2 years) |

| Certification and compliance lead-time | −1.1% | Dual FAA/EASA certificate markets | Medium term (2-4 years) |

| Thermal-management issues in high-luminance LEDs | −0.8% | High-density cabin configurations | Medium term (2-4 years) |

| RF-interference risks in connected cabins | −0.6% | Next-generation connected aircraft | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electronic-component Supply-chain Volatility

Semiconductor shortages, geopolitical trade restrictions, and freight bottlenecks push lead times for LED drivers and microcontrollers beyond historical averages, forcing lighting OEMs to increase inventory buffers and redesign products around alternative chipsets. Price volatility undermines margin stability, while sudden allocation shifts disrupt promised delivery dates for airlines performing time-critical retrofits. Suppliers employing multi-tier transparency tools and near-shoring strategies contain risk exposure better than peers reliant on single-country sourcing. Nevertheless, prolonged volatility may delay project launches and dampen near-term shipment volumes for the commercial aircraft cabin lighting market.

Certification and Compliance Lead-time

The path from prototype to supplemental type certificate (STC) demands exhaustive photometric, thermal, and electromagnetic testing across numerous aircraft variants. Each modification—such as adding wireless control functionality—triggers new conformity inspections, prolonging time-to-market and escalating non-recurring engineering costs. Dual FAA-EASA approval is often mandatory for trans-Atlantic fleets, introducing nuanced interpretational differences that require additional documentation cycles. Vendors with established designated engineering representative (DER) networks and precedent data packages mitigate some delays, yet smaller entrants face steep barriers restricting overall competitive intensity. Extended certification windows may cause airlines to defer purchases, modestly tempering growth in the commercial aircraft cabin lighting market during the medium term.

Segment Analysis

By Aircraft Type: Narrowbodies sustain leadership, regional jets accelerate

Narrowbodies contribute 59.55% of 2024 revenue, reflecting their dominant role in domestic and short-haul operations where high utilization rates amplify cabin lighting replacement cycles. Steady A320neo and B737 MAX output underpins a resilient pipeline for OEM linefit contracts. Regional jets are projected to post the highest 8.12% CAGR to 2030 as carriers revitalize aging CRJ fleets through aftermarket programs that integrate slimline RGBW fixtures and photoluminescent escape markings. Regional aircraft's commercial cabin lighting market share is poised for faster proportional expansion relative to its large-jet counterpart.

While fewer in number, widebodies command sizable per-aircraft bill-of-materials owing to multiple passenger decks and extended cabin lengths. Retrofit campaigns on B787s and A330s are increasingly emphasizing wellness lighting sequences that synchronize with circadian rhythms on long-haul flights. Although widebody delivery volumes remain comparatively modest, their advanced control systems open premium opportunities for vendors offering software-defined customization. The aircraft-type mix collectively supports a balanced revenue stream for suppliers operating in the North American commercial cabin lighting market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Light Type: Reading lights dominate, floor-path strips outpace

Reading lights account for 37.12% of 2024 sales, thanks to their universal placement above every seat and the growing airline preference for glare-free, thumbwheel-dimmable designs. The integration of headphone holders and antimicrobial finishes further enhances unit value. The commercial aircraft cabin lighting market share, currently dominated by reading lights, is expected to erode slightly as operators channel incremental spending into safety-critical systems.

Expanding at a 9.56% CAGR, floor-path strips benefit from regulatory imperatives for quicker evacuation and the transition to maintenance-free photoluminescent materials that emit sufficient luminance throughout long-haul cycles. Next-generation products, such as the 70% lighter SuperSeal UltraLite models, reduce fuel burn and deliver life-cycle cost advantages, driving rapid adoption. Ceiling and sidewall panels, signage, and lavatory fixtures maintain stable demand through cabin refresh programs emphasizing brand consistency and energy savings. Collectively, these dynamics support robust order books for diversified manufacturers within the commercial aircraft cabin lighting market.

By Cabin Class: Economy drives volume, premium economy spurs growth

Economy cabins accounted for 41.76% of 2024 revenue due to seating density and the necessity of full-coverage lighting in single-aisle layouts. Operators, however, exert downward pricing pressure on standard white-light assemblies, limiting margin expansion. Premium economy is expected to exhibit the strongest growth, with a 9.87% CAGR through 2030, driven by airlines seeking new revenue streams without the footprint of complete business-class modules. Mood-lighting packages tailored to this mid-tier offering include soothing boarding hues and sleep-supportive amber tones, commanding price premiums over conventional white LED rails.

Business and first-class suites feature zonal RGBW fixtures that enable dynamic scenario programming for boarding, dining, relaxation, and wake routines, enhanced by individual passenger control via seat-side touch panels. This layered approach yields higher average selling prices per seat, offsetting the lower seat counts relative to economy cabins. Segment diversification, therefore, insulates suppliers against airline capacity planning swings, ensuring sustained opportunities across all cabin classes within the commercial aircraft cabin lighting market.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End User: OEM linefit holds majority, aftermarket retrofitting gains traction

OEM linefit installations contributed 56.45% of the 2024 value, as every new-build aircraft requires a full lighting suite delivered in sync with the final assembly lines. Supplier selection often occurs years in advance, rewarding incumbents possessing established quality records and strategic partnerships with airframers. Conversely, aftermarket activity grows faster at a 9.23% CAGR as operators retrofit legacy fleets to harmonize interior branding and reduce energy consumption. The commercial aircraft cabin lighting market size associated with retrofits is expected to continue expanding as quick-turn installation methodologies minimize aircraft downtime and deliver immediate operational savings.

Recent distribution agreements, such as Collins Aerospace’s extended pact with Satair, underscore how spare parts channels support long-term revenues and facilitate bundle sales of emergency, accent, and exterior lighting. Software-defined control architectures enable airlines to refresh cabin ambiance post-installation without requiring hardware swaps, thereby creating incremental licensing and service opportunities. Together, linefit and retrofit demand patterns sustain predictable, diversified cash flows for market participants.

Geography Analysis

North America’s aviation ecosystem provides an integrated platform of manufacturing prowess, airline density, and regulatory clarity that collectively nourish the commercial aircraft cabin lighting market. The US anchors this platform through its 61.22% revenue share, supported by continuous single-aisle assembly in Renton and Mobile, as well as widebody completions in Charleston. Linefit demand merges seamlessly with retrofit momentum as legacy fleets migrate to energy-saving LEDs, photoluminescent egress systems, and software-controlled ambience packages. FAA guidance ensures uniform performance criteria, yet introducing stricter flicker and thermal parameters requires vendors to iterate designs swiftly while maintaining cost targets.

Canada offers a contrasting growth profile, with a smaller installed base but a higher proportion of fleet renewal. A wave of A220 and B787 arrivals, combined with Bombardier-led regional-jet refurbishments, supplies ongoing linefit and retrofit opportunities. Government support for sustainable aviation, including incentives for weight and power reductions, aligns with LED lighting’s core value proposition, magnifying adoption rates. Transport Canada’s collaborative posture with the FAA expedites bilateral approvals, enabling North American suppliers to commercialize innovations across both countries without extensive redesign.

Mexico and select Caribbean carriers leverage proximity to US repair stations and surplus parts inventories to upgrade cabins at competitive costs. As tourism-driven routes rebound, operators prioritize passenger ambience to attract discretionary travelers. While absolute spending remains lower than the US or Canadian budgets, the compound effect of multiple narrowbody retrofits keeps growth momentum intact. Suppliers cultivating strategic MRO partnerships in these locations can tap into a cost-sensitive yet rapidly evolving customer segment within the broader commercial aircraft cabin lighting market.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

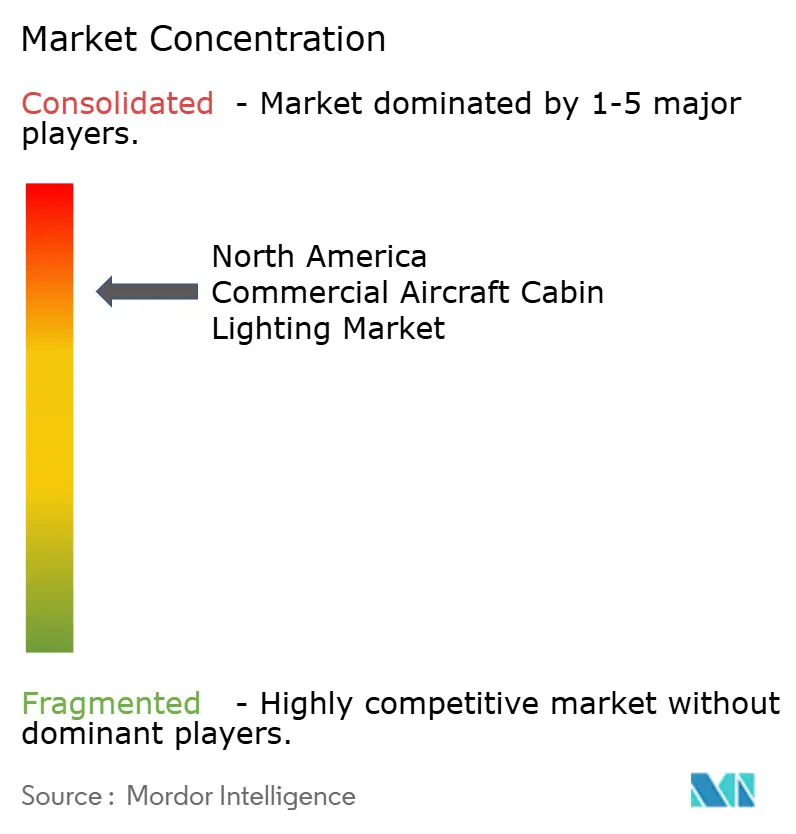

Competitiveness is consolidated, with heritage suppliers wielding certification portfolios that deter new entrants. Collins Aerospace, Luminator Holding LP, and Astronics Corporation collectively hold a commanding presence across both the OEM and retrofit channels, each leveraging long-standing relationships with Airbus, Boeing, and Tier 1 cabin-interior integrators. STG Aerospace leads retrofit installations through its liTeMood plug-and-play system deployed on more than 9,000 airframes, illustrating the advantage of minimal-downtime solutions that keep aircraft in revenue service.

Technological differentiation is increasingly software-centric. Collins Aerospace’s latest smart-panel architecture enables cabin crews to select pre-programmed scenes, synchronize lighting with in-flight entertainment cues, and monitor fixture health in real-time. ACL Digital’s wireless cabin control platform takes a further step, shifting data transmission to low-power mesh networks that reduce harness weight by 30% and cut installation labor in half. Such innovations foreshadow a future where lighting hardware acts as a data node within the connected cabin, unlocking predictive maintenance and dynamic branding experiences.

Mid-tier firms sustain competitiveness through niche specialization, be it ultra-light photoluminescent strips, OLED-based informational panels, or antimicrobial coatings suited for high-touch surfaces. Long approval cycles and stringent DO-160 qualifications keep the playing field stable; nevertheless, ongoing supply-chain volatility provides consolidation opportunities for capitalized players intent on vertical integration. As airlines demand bundled solutions that combine reading, signage, and floor-path products under unified control software, vendors able to deliver end-to-end packages will fortify market share in the commercial aircraft cabin lighting market.

North America Commercial Aircraft Cabin Lighting Industry Leaders

Astronics Corporation

Collins Aerospace (RTX Corporation)

Diehl Stiftung & Co. KG

Safran SA

Luminator Holding LP

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2025: Southwest Airlines unveiled a revamped aircraft interior, featuring a fresh seat design, larger overhead bins, in-seat power for every passenger, as well as updated carpeting and lighting.

- April 2025: Satair and Collins Aerospace announced a four-year extension of their distribution agreement for cabin interior components. This renewed contract also encompasses lighting solutions.

- March 2025: STG Aerospace announced the launch of the Curve, a new flexible cabin lighting product from STG Aerospace's universal lighting family. The Curve is intended for the business jet cabin market.

North America Commercial Aircraft Cabin Lighting Market Report Scope

By Aircraft Type

| Narrowbody Aircraft |

| Widebody Aircraft |

| Regional Jets |

By Light Type

| Reading Lights |

| Ceiling and Wall Lights |

| Signage Lights |

| Lavatory Lights |

| Floor-path Lighting Strips |

By Cabin Class

| First Class |

| Business Class |

| Premium Economy Class |

| Economy Class |

By End User

| OEM Linefit |

| Aftermarket/Retrofit |

By Geography

| United States |

| Canada |

| Mexico |

| By Aircraft Type | Narrowbody Aircraft |

| Widebody Aircraft | |

| Regional Jets | |

| By Light Type | Reading Lights |

| Ceiling and Wall Lights | |

| Signage Lights | |

| Lavatory Lights | |

| Floor-path Lighting Strips | |

| By Cabin Class | First Class |

| Business Class | |

| Premium Economy Class | |

| Economy Class | |

| By End User | OEM Linefit |

| Aftermarket/Retrofit | |

| By Geography | United States |

| Canada | |

| Mexico |

Need A Different Region or Segment?

Customize Now

Market Definition

- Product Type - The interior lights of aircraft which provide illumination for instruments, cabins, and other sections that are occupied by passengers are included in this study.

- Aircraft Type - All the passenger aircraft such as narrowbody and widebody which are single-aisle and twin-aisle are included in this study.

- Cabin Class - Business and First Class, economy and premium economy are classes of air travel provided by the airlines that offer various services to the passengers.

| Keyword | Definition |

|---|---|

| Gross domestic product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| High Dynamic Range (HDR) | Dynamic range describes the ratio between the brightest and darkest parts of an image. HDR is used to capture a greater dynamic range than SDR. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| European Aviation Safety Agency (EASA) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| 4K Display | 4K resolution refers to a horizontal display resolution of approximately 4,000 pixels. |

| Organic Light Emitting Diode (OLED) | It is the light-emitting diode (LED) in which the emissive electroluminescent layer is a film of organic compound that emits light in response to an electric current. |

| Mean Time Between Failures (MTBF) | The mean time between failures is the predicted elapsed time between inherent failures of a mechanical or electronic system, during normal system operation. |

| (Low-Cost Carrier (LCCs) | It is an airline that is operated with an especially high emphasis on minimizing operating costs and without some of the traditional services and amenities provided in the fare |

| Electronically Dimmable Windows (EDW) | It is a type of window that blocks up to 99.96% of all visible light and provide full opacity, integrated into the window cassette of the sidewall panel. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step 1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step 2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step 3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF