Latin America Cold Chain Logistics Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

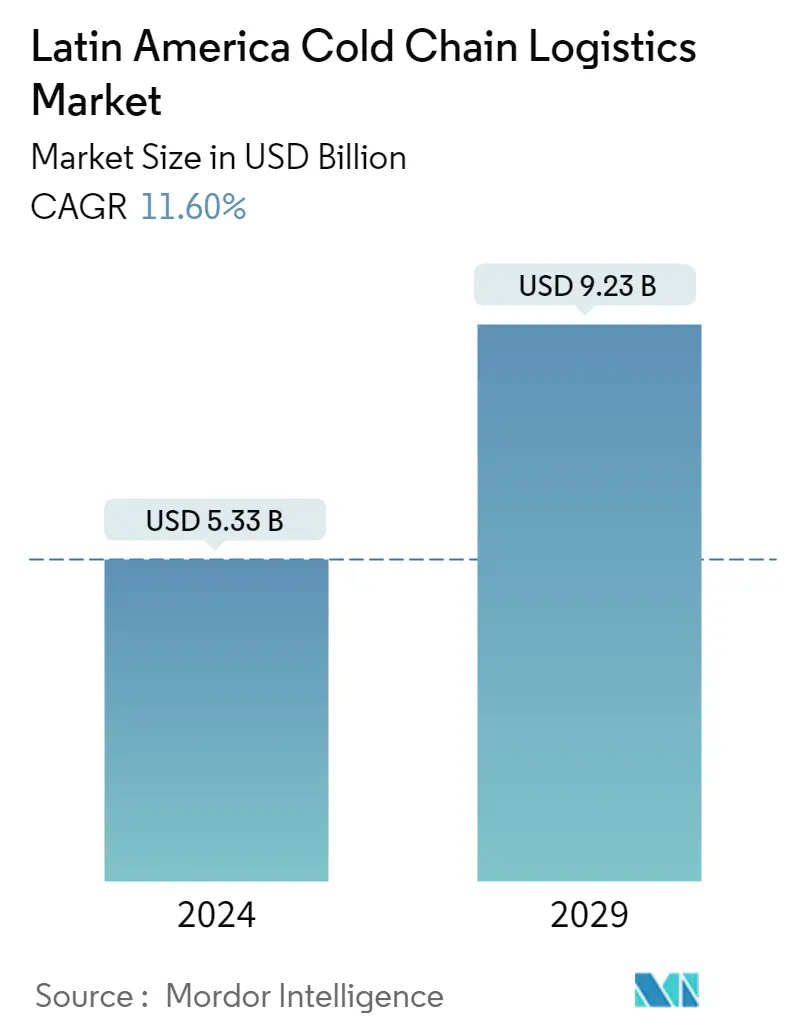

| Market Size (2024) | USD 5.33 Billion |

| Market Size (2029) | USD 9.23 Billion |

| CAGR (2024 - 2029) | 11.60 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Latin America Cold Chain Logistics Market Analysis

The Latin America Cold Chain Logistics Market size is estimated at USD 5.33 billion in 2024, and is expected to reach USD 9.23 billion by 2029, growing at a CAGR of 11.60% during the forecast period (2024-2029).

The characteristics and reality of the Latin American market are highly varied. As a result, businesses from all industries operating in this region must adjust to these conditions to continue doing business. LATAM does not precisely exclude chilled cargo from this obligation due to the difficulties traversing long land expanses between production and marketing hubs. It is crucial to preserve the freshness and quality of the food, medications, and other supplies that must be stored and transported under these conditions by keeping the cold chain at the proper temperatures.

The COVID-19 pandemic initially harmed the cold chain market in Latin America. Still, as the pandemic progressed and more perishable goods were traded internationally, technology advancements in refrigerated transport and storage, government support for infrastructure development, and a surge in MNCs' expansion of food chains, the market for cold chain logistics in LATAM began to grow.

Latin America's perishable food supply chain is still robust, with food traveling to retail establishments. In addition, it is stated that warehouses are operating at total capacity and that a workforce shortage is a problem. These considerations are encouraging the already-established regional players to consolidate and develop technologically to address the region's shortage of refrigerated space.

For instance, in October 2022, Agro-industrial and logistics firm Frigorifico Modelo (Frimosa), based in Montevideo, Uruguay, announced that its cold storage operations would be acquired by Emergent Cold Latin America (Emergent Cold LatAm or the Company), a provider of refrigerated storage and logistics services in Latin America. The main building of Frimosa in Polo Oeste, which includes a warehouse with 22,000 cold storage pallets, a separate bonded warehouse, and a sizable amount of ground for expansion, will be purchased by Emergent Cold LatAm. Additionally, in Asunción, Paraguay, Emergent Cold LatAm will purchase a brand-new 8,400-pallet warehouse.

Latin America Cold Chain Logistics Market Trends

Increasing Consumer Demand for Perishable Goods the warehousing space is growing in the region

The warehousing & storage industry in Latin America has been driven by the development and growth of e-commerce, increasing trade volume, and the increasing need of enterprises for effective warehousing & inventory management. Furthermore, increased investment and adoption of the Internet of Things (IoT) and automation combined with infrastructure development also contribute to the growth of the industry.

Cold warehousing & storage is in high demand in Latin America due to the high perishable food demand. In addition, cold storage & warehousing is also in high demand in the pharmaceutical industry due to the high-temperature requirements of various drugs.

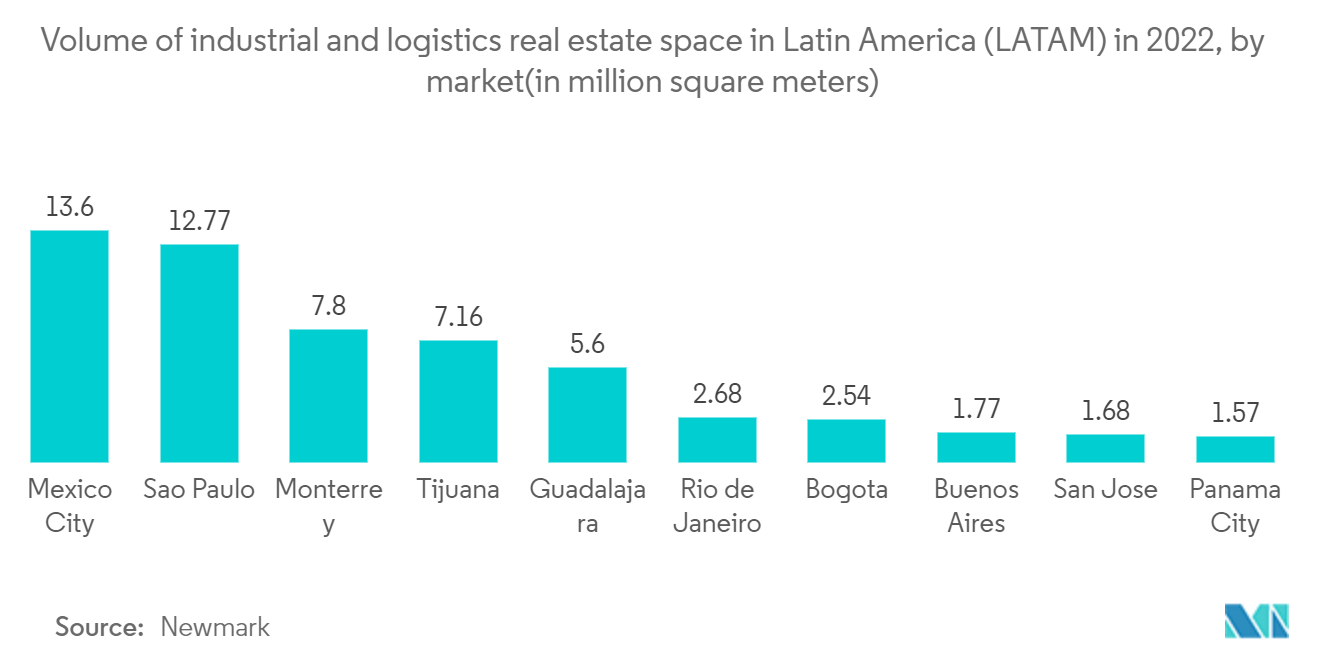

Currently, Brazil is the largest market for warehousing with about 50% of the overall industrial market share. Other major markets include Mexico, Columbia, Chile & Argentina.

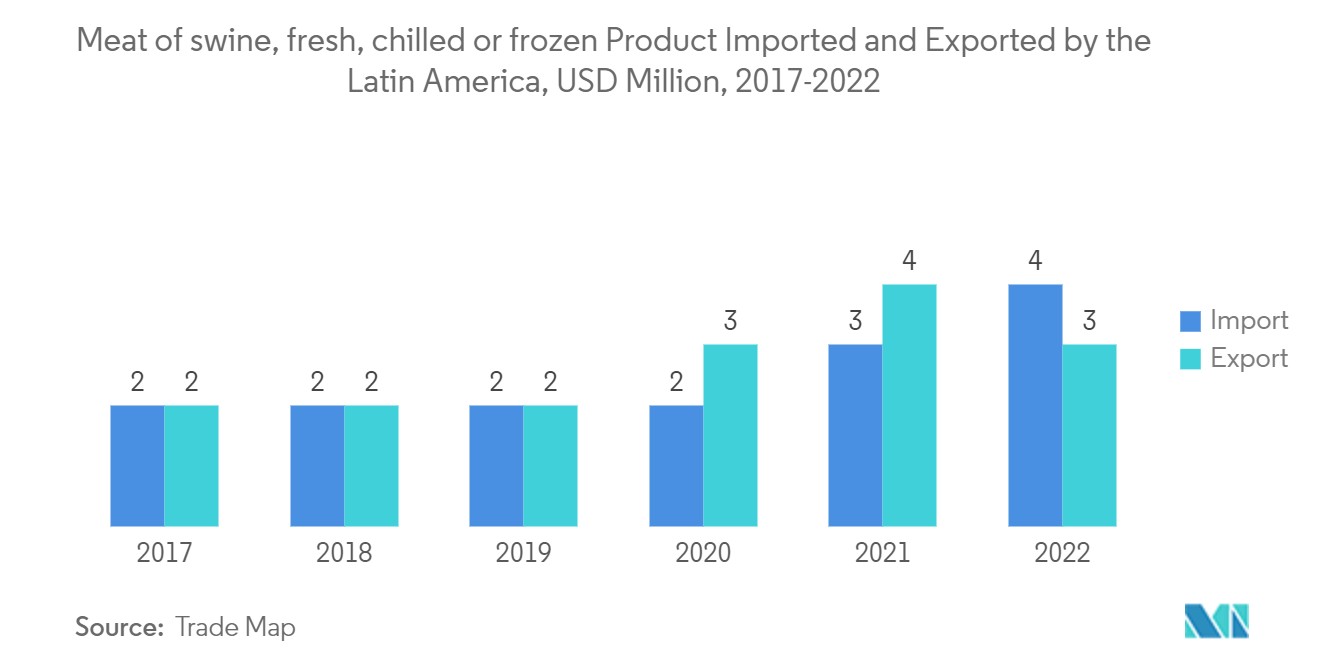

Fresh and frozen food growth outpaces those of other product categories.

As consumer demand increased, large food retailers benefited from expanding sales over the past few years. According to recent industry data, fresh produce and frozen food goods, which require cold chain logistics, are growing faster than other food products.

Food products that are fresh or frozen can continue to be substantially more significant than other product categories. Therefore, cold chain operations that can stop food from rotting in transportation may become considerably more critical. Food in cans and packages might be less significant to manufacturers. It can compel businesses to spend money on 3PL companies that can handle their cold chain logistics and systems.

Latin America Cold Chain Logistics Industry Overview

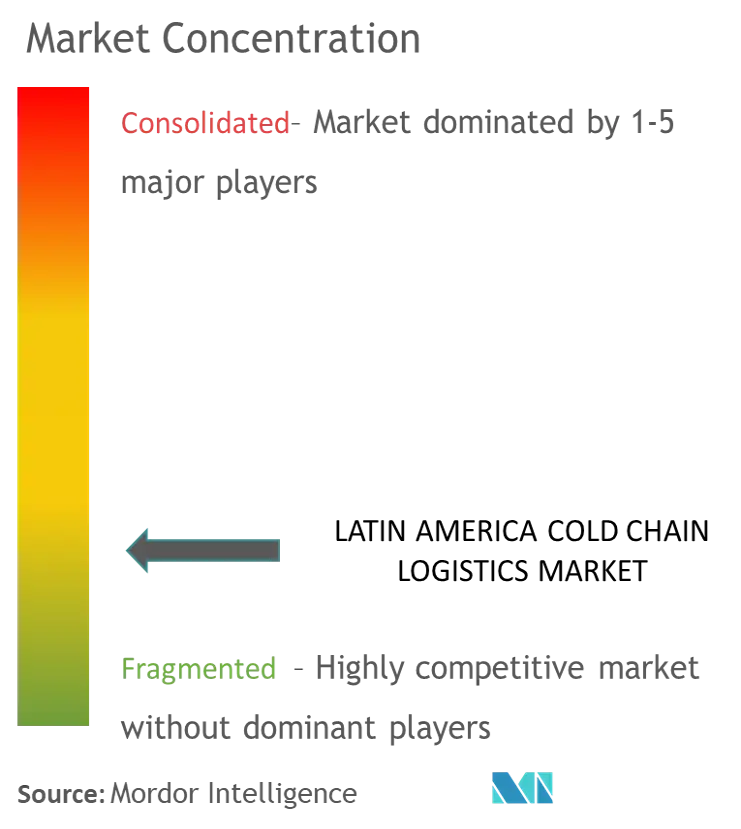

Due to the existence of both domestic and foreign businesses, the market is fragmented. Brazil is the biggest market in this area, followed by Mexico, Argentina, and Columbia.

The most prominent players in the LATAM region's cold storage market continue to grow due to mergers and consolidation. Many businesses in developed markets keep growing and buying up rival businesses.

For the smooth exchange of information with customers during transportation, cold chain businesses in the area are implementing more advanced and contemporary cold chain technologies, such as radio frequency identification in warehouses, cloud storage, the internet of things, and electronic data interchange.

Latin America Cold Chain Logistics Market Leaders

-

Frialsa Frigorificos SA

-

Comfrio SoluCoes LogIsticas

-

Friozem Armazéns Frigorificos

-

Superfrio Armazéns Gerais

-

Americold Logistics

*Disclaimer: Major Players sorted in no particular order

Latin America Cold Chain Logistics Market News

- June 2023: Canadian Pacific announced a strategic partnership to co-host American warehouse facilities on Canadian Pacific's (CPKC) network. Supported by rail transportation, the goal is to construct the first facility on CPKC's network in Kansas City (Mo.), Kansas, to combine cold storage and added-value services with accelerated intermodal transport solutions connecting key markets in the U.S., Midwest, and Mexico.

- November 2022: Emergent Cold Latin America (Emergent Cold LatAm), the region's fastest-growing cold storage logistics provider, announced the acquisition of a distribution facility in Recife, Brazil. The business now made two investments in northeastern Brazil. A building area of over 19,000 sq m and 18,500 pallet positions of storage space make up the new Emergent Cold LatAm location. It is conveniently situated in Recife, one of the biggest cities in Brazil and the most important business center in the northeast.

- October 2022: The fastest-growing refrigerated storage and logistics service provider in Latin America announced the expansion of its temperature-controlled facility in Panama City, Panama. This planned expansion will add more than 8,300 pallet positions to the facility, bringing its total capacity to 28,300 pallets.

Latin America Cold Chain Logistics Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS AND INSIGHTS

4.1 Market Overview (Current Scenario of the Cold Chain Logistics Market)

4.2 Impact of COVID-19 on the Cold Chain Logistics Market

4.3 Government Regulations (Related to Cold Storage and Transport)

4.4 Insights into Refrigerants and Packaging Materials

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Growth in E-commerce

4.5.1.2 Healthcare Sector is the market

4.5.2 Restraints

4.5.2.1 Supply Chain Disruptions

4.5.2.2 Lack of Temperature- Controlled Warehouses

4.5.3 Opportunities

4.5.3.1 Technological Innovations

4.6 Industry Attractiveness - Porter's Five Forces Analysis

4.6.1 Bargaining Power of Suppliers

4.6.2 Bargaining Power of Consumers

4.6.3 Threat of New Entrants

4.6.4 Threat of Substitutes

4.6.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

5.1 By Service

5.1.1 Cold Storage/Refrigerated Warehousing

5.1.2 Refrigerated Transportation

5.1.3 Value-added Services (Order Management, Blast Freezing, Labeling, Inventory Management, etc.)

5.2 By Temperature

5.2.1 Chilled

5.2.2 Frozen

5.2.3 Ambient

5.3 By End User

5.3.1 Fruits and Vegetables

5.3.2 Dairy Products (Milk, Butter, Cheese, Ice Cream, etc.)

5.3.3 Fish, Meat, and Seafood

5.3.4 Processed Food

5.3.5 Pharmaceutical (Includes Biopharma)

5.3.6 Bakery and Confectionery

5.3.7 Other End Users

5.4 By Country

5.4.1 Mexico

5.4.2 Brazil

5.4.3 Chile

5.4.4 Colombia

5.4.5 Rest of Latin America

6. COMPETITIVE LANDSCAPE

6.1 Overview

6.2 Company Profiles

6.2.1 Frialsa Frigorificos SA

6.2.2 Comfrio Solucoes Logisticas

6.2.3 Friozem Armazens Frigorificos Ltda

6.2.4 Superfrio Armazens Gerais Ltda

6.2.5 Americold Logistics

6.2.6 Brasfrigo

6.2.7 Arfrio Armazens Gerais Frigorificos

6.2.8 Ransa Comercial SA

6.2.9 Localfrio

6.2.10 Qualianz*

- *List Not Exhaustive

6.3 Other Companies (Key Information/Overview)

6.4 Key Vendors and Suppliers (Cold Storage Equipment Manufacturers, Carrier Manufacturers, and Technology Providers for the Cold Chain Industry)

7. FUTURE OF THE MARKET

8. APPENDIX

8.1 Detailed Imports and Exports Statistics of Frozen Food Products

Latin America Cold Chain Logistics Industry Segmentation

Cold chain logistics combines temperature-controlled transportation with a planned supply chain to preserve products' quality and shelf life, including fresh agricultural produce, seafood, frozen food, and pharmaceutical medications. The research offers a thorough background analysis of the Latin America (LATAM) cold chain logistics market, covering the most recent technology advancements, market trends, in-depth details on significant sectors, and the industry's competitive environment. The study also took into account the effects of COVID-19.

The Latin America Cold Chain Logistics Market is segmented by service (cold storage/refrigerated warehousing, refrigerated transportation, and value-added services), temperature (chilled, frozen and ambient), end-user (fruits and vegetables, dairy products (milk, butter, cheese, ice cream, etc.), fish, meat, and seafood, processed food, pharmaceutical (includes biopharma), bakery and confectionery, and other end-users), and country (Mexico, Brazil, Chile, Colombia, and rest of Latin America). The report offers Market size and forecasts for Latin America Cold Chain Logistics Market in value (USD) for all the above segments.

| By Service | |

| Cold Storage/Refrigerated Warehousing | |

| Refrigerated Transportation | |

| Value-added Services (Order Management, Blast Freezing, Labeling, Inventory Management, etc.) |

| By Temperature | |

| Chilled | |

| Frozen | |

| Ambient |

| By End User | |

| Fruits and Vegetables | |

| Dairy Products (Milk, Butter, Cheese, Ice Cream, etc.) | |

| Fish, Meat, and Seafood | |

| Processed Food | |

| Pharmaceutical (Includes Biopharma) | |

| Bakery and Confectionery | |

| Other End Users |

| By Country | |

| Mexico | |

| Brazil | |

| Chile | |

| Colombia | |

| Rest of Latin America |

Latin America Cold Chain Logistics Market Research FAQs

How big is the Latin America Cold Chain Logistics Market?

The Latin America Cold Chain Logistics Market size is expected to reach USD 5.33 billion in 2024 and grow at a CAGR of 11.60% to reach USD 9.23 billion by 2029.

What is the current Latin America Cold Chain Logistics Market size?

In 2024, the Latin America Cold Chain Logistics Market size is expected to reach USD 5.33 billion.

Who are the key players in Latin America Cold Chain Logistics Market?

Frialsa Frigorificos SA , Comfrio SoluCoes LogIsticas , Friozem Armazéns Frigorificos, Superfrio Armazéns Gerais and Americold Logistics are the major companies operating in the Latin America Cold Chain Logistics Market.

What years does this Latin America Cold Chain Logistics Market cover, and what was the market size in 2023?

In 2023, the Latin America Cold Chain Logistics Market size was estimated at USD 4.78 billion. The report covers the Latin America Cold Chain Logistics Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Latin America Cold Chain Logistics Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Latin America Cold Chain Logistics Industry Report

Statistics for the 2024 Latin America Cold Chain Logistics market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Latin America Cold Chain Logistics analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.

Latin America Cold Chain Logistics Market Report Snapshots